The ASX 200 snapped its four-day losing streak as a mixed inflation print — headline CPI cooled to 4% but trimmed mean surprised to the upside at 3.6% — kept investors on edge. A remarkable reversal in WiseTech Global (WTC) drove the information technology sector to its biggest single-day gain in months, while gold stocks, energy, and materials continued to suffer against a backdrop of weaker commodity prices.

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key economic data in tonight's Evening Wrap. Also, I have detailed technical analysis on the Nasdaq Composite and the S&P/ASX 200 in today's ChartWatch.

Let’s dive in!

Today in Review

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,808.4 | +0.24% |

| All Ords | 9,012.6 | +0.27% |

| Small Ords | 3,476.9 | -0.16% |

| All Tech | 2,929.1 | +3.03% |

| Emerging Companies | 2,993.0 | +0.10% |

Currency | ||

| AUD/USD | 0.6909 | -0.11% |

US Futures | ||

| S&P 500 | 7,449.75 | +0.16% |

| Dow Jones | 52,020.0 | -0.12% |

| Nasdaq | 29,826.0 | +0.54% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Information Technology | 1,779.8 | +5.21% |

| Health Care | 25,267.2 | +2.14% |

| Consumer Staples | 13,070.7 | +0.70% |

| Real Estate | 3,713.1 | +0.64% |

| Consumer Discretionary | 3,871.4 | +0.57% |

| Industrials | 8,503.4 | +0.56% |

| Financials | 9,373.0 | +0.27% |

| Utilities | 9,730.3 | +0.20% |

| Communication Services | 1,620.9 | +0.01% |

| Materials | 23,926.5 | -0.63% |

| Energy | 9,580.7 | -1.04% |

ASX 200 Intraday Chart

%20intraday%20chart_24%20Jun.png)

Markets

The S&P/ASX 200 (XJO) finished 21.4 points higher at 8,808.4, 0.27% from its session low and 0.17% from its high. Despite the win at benchmark level, in the broader-based S&P/ASX 300 (XKO) it was hardly convincing with advancers beating decliners by a narrow147 to 133.

Information Technology (XIJ) (+5.2%) delivered the session's most dramatic performance — and the most puzzling. WiseTech Global (WTC) (+14.3%) staged a stunning reversal from its two-session 22% collapse, despite no material new announcement from the company today. The move may reflect a delayed market response to yesterday's company statement in which WTC affirmed it was not part of any legal proceedings and that executive chairman Richard White was "not aware of any such investigation" — but with no further clarity on the AFP reports, the rebound looked more like short-covering than any genuine resolution of the governance concerns.

Xero (XRO) (+8.2%) also surged as its fortunes have been closely tied to those of WTC, and possibly also in response to a positive Citi research note on the company released today. Codan (CDA) (+4.1%) and Life360 (360) (+3.4%) were also firmer.

Health Care (XHJ) (+2.1%) delivered another strong session as the sector's recovery from its horrific rolling 12-month trough continues with gathering conviction. The CPI print, while mixed, eased benchmark bond yields modestly — which helps long-duration healthcare valuations — while the sector's non-cyclical earnings character continued to attract capital fleeing global growth uncertainty.

Telix Pharmaceuticals (TLX) (+8.0%) was the standout, alongside Ramsay Health Care (RHC) (+3.5%), Pro Medicus (PME) (+3.5%), ResMed (RMD) (+3.3%), and CSL (CSL) (+2.6%) — the latter now up almost 20% across the past month.

Consumer Staples (XSJ) (+0.7%) was the next most clearly defensive beneficiary — non-discretionary earnings with reliable dividend yields are exactly what investors reach for when global growth signals are uncertain. Woolworths (WOW) (+1.6%), Bega Cheese (BGA) (+1.1%), and The A2 Milk Company (A2M) (+1.0%) all advanced.

Real Estate (XPJ) (+0.7%) caught the same modest easing in benchmark bond yields — when risk-free rates ease, the stable income streams of property trusts become comparatively more attractive, drawing buyers back to a sector that has been under sustained pressure in recent months.

Consumer Discretionary (XDJ) (+0.6%) benefited from the same lower-yield tailwind alongside improving confidence that the RBA may remain on hold for an extended period if CPI continues to ease. Collins Foods (CKF) (+2.8%), Aristocrat Leisure (ALL) (+1.8%), and Wesfarmers (WES) (+1.0%) all gained.

%20COMEX%20chart_24%20Jun.png)

Gold Futures (Front month, back-adjusted) COMEX

The Gold Sub-Index (XGD) (-2.7%) extended its painful correction for a fifth consecutive session — the precious metals rout that has accompanied the Fed's hawkish pivot and the unwinding of the Iran war premium is now running at pace. COMEX gold futures fell 1.1% to US$4,105/oz after dropping 1.3% overnight, while COMEX silver futures eased 0.2% to US$61.90/oz after plunging 5.3% overnight. The sector has now given back the majority of the gains accumulated during the 15-week Iran conflict. Westgold Resources (WGX) (-2.4%), Evolution Mining (EVN) (-2.3%), Perseus Mining (PRU) (-2.3%), and Newmont (NEM) (-2.2%) were the sharpest fallers.

Energy (XEJ) (-1.0%) continued to absorb the oil price collapse — ICE Brent crude futures fell 1.6% to US$75.83/bbl, touching their lowest level since the Iran war started, as more tankers transit the reopening Strait of Hormuz and the Iran oil-sales licence granted by the US adds further supply-side pressure. Beach Energy (BPT) (-8.5%) was the session's sharpest individual mover with no confirmed company-specific trigger — the decline appeared to reflect a combination of sector-wide pressure and possibly BPT-specific positioning. Karoon Energy (KAR) (-2.8%), Woodside Energy (WDS) (-1.4%), and Santos (STO) (-1.0%) were also lower.

Materials (XMJ) (-0.6%) continued to drift on a combination of softer copper and broader risk-off positioning — COMEX copper futures fell 0.4% to US$6.124/lb after dropping 3.4% overnight, while SGX iron ore futures edged up 0.9% to US$98.30/t in a modest recovery. Base metals stocks were broadly lower as base metals prices on the LME tumbled on Tuesday — South32 (S32) (-1.9%), Sandfire Resources (SFR) (-1.3%), Rio Tinto (RIO) (-1.2%), and BHP (BHP) (-0.7%) all fell.

Lithium Carbonate Futures (Benchmark month, back-adjusted) GFEX

Lithium stocks snapped a four-day losing streak as GFEX lithium carbonate futures rebounded 3.1% to CNY 162,120/t — a meaningful recovery after the recent string of heavy falls. Elevra Lithium (ELV) (+8.6%), IGO (IGO) (+5.5%), Wildcat Resources (WC8) (+4.9%), Core Lithium (CXO) (+3.5%), Pilbara Minerals (PLS) (+3.5%), Vulcan Energy Resources (VUL) (+3.2%), and Liontown Resources (LTR) (+1.1%) all advanced.

Today's best ASX Top 300 gainers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

| Wisetech Global (WTC) | $32.86 | +$4.10 | +14.3% | -11.4% | -69.8% |

| BCI Minerals (BCI) | $0.415 | +$0.04 | +10.7% | +16.9% | +20.3% |

| Elevra Lithium (ELV) | $11.52 | +$0.91 | +8.6% | -16.1% | +412.0% |

| Xero (XRO) | $70.31 | +$5.31 | +8.2% | -7.3% | -63.8% |

| Telix Pharmaceuticals (TLX) | $15.73 | +$1.17 | +8.0% | +18.1% | -35.5% |

| Tasmea (TEA) | $9.65 | +$0.62 | +6.9% | +57.9% | +186.4% |

| Regis Healthcare (REG) | $6.61 | +$0.36 | +5.8% | +7.8% | -14.9% |

| GenusPlus Group (GNP) | $10.68 | +$0.57 | +5.6% | +11.3% | +180.3% |

| IGO (IGO) | $7.93 | +$0.41 | +5.5% | -13.9% | +96.3% |

| FireFly Metals (FFM) | $1.815 | +$0.09 | +5.2% | -8.3% | +82.3% |

| Iluka Resources (ILU) | $7.59 | +$0.34 | +4.7% | -5.5% | +117.5% |

| Reliance Worldwide Corporation (RWC) | $3.72 | +$0.16 | +4.5% | +18.1% | -11.6% |

| Neuren Pharmaceuticals (NEU) | $12.90 | +$0.52 | +4.2% | -5.6% | +2.9% |

| Codan (CDA) | $43.86 | +$1.72 | +4.1% | +9.8% | +118.0% |

| Lynas Rare Earths (LYC) | $19.34 | +$0.75 | +4.0% | +2.5% | +110.7% |

| Lindian Resources (LIN) | $0.91 | +$0.035 | +4.0% | +28.2% | +766.7% |

| Sunrise Energy Metals (SRL) | $18.59 | +$0.71 | +4.0% | +26.8% | +1942.9% |

| Ramsay Health Care (RHC) | $41.23 | +$1.40 | +3.5% | +8.3% | +15.4% |

| Core Lithium (CXO) | $0.295 | +$0.01 | +3.5% | 0.0% | +235.2% |

| Pro Medicus (PME) | $178.99 | +$6.06 | +3.5% | +39.9% | -35.9% |

Today's worst ASX Top 300 losers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

| Predictive Discovery (PDI) | $0.83 | -$0.105 | -11.2% | +15.3% | +118.4% |

| Beach Energy (BPT) | $0.86 | -$0.08 | -8.5% | -23.9% | -35.3% |

| Bellevue Gold (BGL) | $1.325 | -$0.085 | -6.0% | -13.4% | +49.7% |

| Arafura Rare Earths (ARU) | $0.245 | -$0.015 | -5.8% | -21.0% | +48.5% |

| Alkane Resources (ALK) | $1.515 | -$0.09 | -5.6% | +3.8% | +102.0% |

| Ora Banda Mining (OBM) | $1.165 | -$0.065 | -5.3% | -12.4% | +33.9% |

| Insurance Australia Group (IAG) | $7.87 | -$0.41 | -5.0% | 0.0% | -13.4% |

| West African Resources (WAF) | $3.01 | -$0.15 | -4.7% | 0.0% | +36.2% |

| Capricorn Metals (CMM) | $12.68 | -$0.62 | -4.7% | -4.4% | +22.0% |

| Kingsgate Consolidated (KCN) | $5.53 | -$0.27 | -4.7% | -7.4% | +150.2% |

| Resolute Mining (RSG) | $1.03 | -$0.05 | -4.6% | -15.9% | +66.1% |

| Genesis Minerals (GMD) | $5.58 | -$0.24 | -4.1% | -5.4% | +23.5% |

| Meridian Energy (MEZ) | $4.70 | -$0.20 | -4.1% | -3.1% | -10.1% |

| Mader Group (MAD) | $7.82 | -$0.32 | -3.9% | -6.0% | +25.7% |

| Lovisa Holdings (LOV) | $21.98 | -$0.85 | -3.7% | +0.4% | -27.5% |

| GR Engineering Services (GNG) | $5.32 | -$0.20 | -3.6% | +3.3% | +63.7% |

| Southern Cross Gold Consolidated (SX2) | $9.25 | -$0.33 | -3.4% | 0.0% | +20.1% |

| Vault Minerals (VAU) | $4.60 | -$0.16 | -3.4% | +4.5% | +76.9% |

| IPH (IPH) | $3.86 | -$0.13 | -3.3% | +1.3% | -12.7% |

| Greatland Resources (GGP) | $12.87 | -$0.43 | -3.2% | -1.3% | +76.3% |

Chartwatch

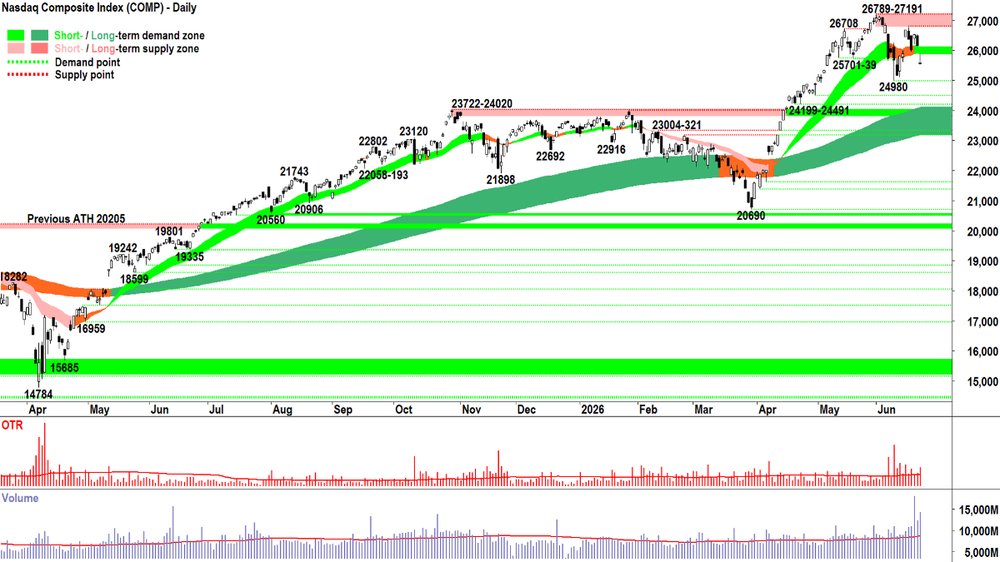

Nasdaq Composite Index

A very decent supply side showing

Analysis

Yes, that was a very decent supply side showing last night. Gap and run. Of sorts... Because, given the upward pointing shadow, it was actually more like:

Gap lower (major shift in market thinking about fundamentals causes violent shift in price discovery)

Intraday rally (i.e., still some BTD lurking in the system from traders conditioned in the bull run that pullbacks only mean one thing: BUY!)

Upward pointing shadow – terminated precisely at the short term uptrend ribbon (indicating it behaved as a zone of dynamic excess supply). Upward pointing shadows = STR (i.e., not FOMO, not HOFU... Rather: NUTE and FOHO!)

Close near session low

Above average volatility (see OTR indicator = Tuesday's candle MATTERED!)

Substantially above average volume (see Volume indicator = massive demand and supply side engagement! Demand took the bait, bought the dip in numbers, but found a wall of supply. A huge amount of demand was consumed... And now stuck in losing positions, creates latent supply at / above the high of Tuesday's candle.

Put all of the above together, then add in the 3 out of last 4 candles prior to Tuesday being supply side candles, plus the lower peak (26789-27191) and you get a building picture of increasing supply side control.

24980 is now the critical point of demand for the Comp. Beneath it, and we are facing a possible multi month cycle high logged at 27191.

Even if this doesn't eventuate, I propose the short term uptrend that began in early-April is now unequivocally over. This is short term equilibrium. At best, because at worst, it's already bona fide supply side control. ⚠️

The long term trend is now under some proper pressure – I propose, even, possibly even neutralised itself.

If that's my Analysis, then I must Accept that the time for the FRP bravado of the +6,000 point April-May rally is over. Now is the time for conservatism, for balance. ⚖️

View

Yep, feeling far more at ease with my decision nearly a couple weeks back now to go to 1/2RP. All things considered, it seems like a very sensible place to be!

Key Levels

26789-27191 is the key zone of supply. 24980 is the key point of demand. The short term uptrend ribbon (presently 25875-26102) could now begin to act as a zone of dynamic excess supply.

S&P/ASX 200 (XJO)

%20chart_24%20Jun.png)

Hey, it could have been worse, right!? 🤔

Analysis

Analyse? Well, I can't analyse a candle that barely exists! 🤏🔬

Hey, it could have been worse, right!? 🤔

We appear to be experiencing what could be described as 'resilience'.

How long it lasts... No idea!

The trend ribbons are the main game now: Hold Them ✅ vs Break Them ❌

One more candle... ??? 🙈

View

Hanging in at 2/3RP 🪣 on the OTP but still leaning to cutting back to 1/2RP (i.e., my personal allowable capital allocation limit for my investments in Australian stocks is 67%, but I'm happy to drift this towards 50%).

Key levels

8984-9022 is the key zone of supply. Beyond that, it's 9201. Demand is in the 8485-8561 range, but the short- and long-term trend ribbons (presently 8695-8776) will likely also increasingly come into play as a dynamic zone of excess demand.

(Glossary of acronyms! OTP (Old Tin Pot): S&P/ASX 200 | MOTN: More Often Than Not | FOMO: Fear Of Missing Out | HOFU: Holding On For Upside | BTD: Buy The Dip | NUTE: No Urgency To Enter | FOHO: Fear Of Holding On | STR: Sell The Rally | RP: Risk Position)

This week's ChartWatch Live Webinar: Why Elon Musk should sell 1.6 billion SpaceX shares right away... (and a major Nasdaq top signal!)

***NEW VIDEO DROPPED!!! 📺***

BHP & RIO vs CSL battle royale! Is the ASX Resources run over!? Copper, Iron Ore, Lithium and more

ChartWatch LIVE Webinar

ChartWatch LIVE Webinars – WEEKLY Wednesday's @ 12pm AEDT

Learn more about technical analysis and trend following through real case studies on ASX stocks. Australia's premier technical analyst, Carl Capolingua, shares his unique insights on stocks as requested by viewers. Ask about a company in your portfolio or anything related to trading and investing and get Carl's expert opinion.

Places are limited so >REGISTER NOW!<

Economy

Today

09:30 AUS May Consumer Price Index (CPI)

Headline: -0.7% m/m and +4.0% p.a. vs -0.4% m/m and +4.3% p.a. forecast and +0.4% and +4.2% p.a. in April (better than expected, as fuel prices moderated)

Trimmed mean: +0.4% m/m and +3.6% p.a. vs +0.3% m/m and +3.6% p.a. forecast and +0.3% m/m and 3.4% p.a. in April (roughly in-line, still too high for the RBA!)

Later this week

Thursday

09:30 AUS May Employment Data

Change: +30,300 m/m forecast vs -18,600 m/m in April

Unemployment rate: 4.4% forecast vs 4.5% in April

09:30 AUS May Household Spending (+0.6% m/m forecast vs -1.1% m/m in April)

20:30 USA May Personal Consumption Expenditures (PCE) Data

Core PCE Index: +0.3% m/m forecast vs +0.2% m/m in April

Personal Income: +0.4% m/m forecast vs +0.0% m/m in April

Personal Spending: +0.6% m/m forecast vs +0.5% m/m in April

Friday

07:30 JPN May Core CPI (+1.6% p.a. forecast vs +1.3% p.a. in May)

20:30 USA May Wholesale Inventories (+0.3% m/m forecast vs +0.6% m/m in April)

Interesting Movers

Trading higher

- Elevra Lithium (ELV) $11.52+8.6%

Rose after it announced Van Eck Associates Corporation had become a substantial shareholder in the company. Van Eck now owns 6.57% of ELV's shares.

- Lindian Resources (LIN) $0.91+4.0%

Rose after it announced the establishment of a regional office in Singapore to support its international sales, marketing and logistics functions; management said the move supports maintaining an efficient global corporate and tax structure.

- Paladin Energy (PDN) $9.70+3.3%

Rose after it announced Van Eck Associates Corporation had increased its shareholding in the company. Van Eck now owns 8.94% of PDN's shares, up from 7.10% prior.

- Nickel Industries (NIC) $0.95+1.6%

Rose after it agreed to invest US$169 million for a 17.5% interest in PT Teluk Metal Industry HPAL project in Indonesia; the project will produce mixed hydroxide precipitate for the EV battery supply chain.

Trading Lower

- Predictive Discovery (PDI) $0.83-11.2%

Fell after it announced Grant Thornton Audit Pty Ltd has been appointed as auditor following the resignation of PKF Perth.

- Baby Bunting Group (BBN) $1.47-10.6%

Fell after it downgraded its second half profit forecast to $11 million to $12 million — around 12% below consensus and well down from prior guidance; downgrade driven by weaker sales in non-refurbished stores.

- Credit Clear (CCR) $0.20-9.1%

Fell after it announced the ACCC has commenced proceedings against ARMA Group Holdings Pty Ltd and Force Legal Pty Ltd, two wholly owned subsidiaries; management said the companies deny the allegations and intend to defend the proceedings.

- Tasman Resources (TAS) $0.06-8.3%

Fell after it acquired energy services provider JPS Group in a deal worth up to $75 million, and after reaffirming its earnings guidance for the 2026 fiscal year of underlying EBIT of $117 million and underlying net profit of $72.5 million.

- KMD Brands (KMD) $0.06-4.6%

Fell after it announced plans to undertake a 1 for 25 share consolidation to rationalise the number of shares on issue (reducing shares from about 1.8 billion to about 72 million).

Broker Moves

Company | Broker | Action | Rating | Price Target |

|---|---|---|---|---|

AGLAGL Energy | Morgan Stanley | Retained | Underweight | $9.28 |

ALXAtlas Arteria | Citi | Retained | Neutral | $5.10 |

BNZBenz Mining Corp | Canaccord Genuity | Retained | Speculative Buy | $3.15 |

BPTBeach Energy | Morgans | Downgraded | Sell(from Hold) | $0.81(from $1.10) |

CCLCuscal | Ord Minnett | Retained | Buy | $5.45 |

CKFCollins Foods | Citi | Upgraded | Buy(from Neutral) | $10.30(from $10.45) |

CNICenturia Capital Group | Jefferies | Retained | Buy | $2.66(from $2.50) |

| Moelis Australia | Downgraded | Hold(from Buy) | $2.18(from $2.23) | |

IAGInsurance Australia Group | Macquarie | Downgraded | Neutral(from Outperform) | $8.50(from $9.00) |

IELIDP Education | Morgan Stanley | Retained | Equal Weight | $2.50(from $5.50) |

IGLIVE Group | Bell Potter | Retained | Buy | $3.25 |

ILUIluka Resources | Argonaut Securities | Retained | Buy | $9.50 |

| Canaccord Genuity | Upgraded | Buy(from Hold) | $8.45(from $8.10) | |

| Goldman Sachs | Retained | Buy | $8.80 | |

| JPMorgan | Retained | Neutral | $7.10(from $7.30) | |

| Macquarie | Retained | Outperform | $8.00(from $8.40) | |

| Ord Minnett | Retained | Buy | $9.00 | |

INAIngenia Communities Group | Citi | Retained | Buy | $5.42(from $5.00) |

INRioneer | Ord Minnett | Retained | Speculative Buy | $0.40 |

IPXIperionX | Canaccord Genuity | Retained | Speculative Buy | $9.20(from $8.90) |

JDOJudo Capital Holdings | Citi | Retained | Buy | $2.20 |

ORGOrigin Energy | Morgan Stanley | Retained | Underweight | $11.00 |

QANQantas Airways | Ord Minnett | Retained | Buy | $11.50(from $10.50) |

RWCReliance Worldwide Corporation | Macquarie | Retained | Outperform | $4.90(from $4.50) |

| Morgans | Retained | Hold | $3.60(from $3.25) | |

| Ord Minnett | Retained | Hold | $4.00 | |

SFRSandfire Resources | Macquarie | Downgraded | Neutral(from Outperform) | $21.00 |

SHLSonic Healthcare | Citi | Retained | Neutral | $19.00(from $21.50) |

SUNSuncorp Group | Macquarie | Retained | Outperform | $20.60(from $20.30) |

TCGTuraco Gold | Canaccord Genuity | Retained | Speculative Buy | $1.80(from $1.75) |

TCLTransurban Group | Citi | Retained | Neutral | $15.80 |

TGNTungsten Mining NL | Euroz Hartleys | Initiated | Speculative Buy | $0.38 |

TWETreasury Wine Estates | Goldman Sachs | Initiated | Neutral | $5.20 |

VEAViva Energy Group | Jefferies | Retained | Hold | $2.25 |

| JPMorgan | Retained | Neutral | $2.40(from $2.60) | |

| Morgan Stanley | Retained | Equal Weight | $2.39(from $2.56) | |

| RBC Capital Markets | Retained | Outperform | $2.60(from $2.70) | |

VFYVitrafy Life Sciences | Bell Potter | Retained | Speculative Buy | $5.15(from $3.00) |

WA1WA1 Resources | Bell Potter | Retained | Speculative Buy | $27.20(from $24.40) |

WTCWisetech Global | Ord Minnett | Retained | Buy | $60.00(from $88.00) |

XROXero | Citi | Retained | Buy | $113.60 |

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| AVE | Avecho Biotechnology Ltd | $0.021 | +40.00% |

| TGH | Terragen Holdings Ltd | $0.02 | +25.00% |

| BNZ | BENZ Mining Corp | $2.63 | +24.06% |

| UM1 | Unity Metals Ltd | $0.145 | +20.83% |

| LKO | Lakes Blue Energy NL | $0.615 | +20.59% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| KM1 | Kali Metals Ltd | $0.08 | -23.81% |

| COI | Comet Ridge Ltd | $0.10 | -23.08% |

| NOR | Norwood Systems Ltd | $0.031 | -18.42% |

| BTE | Botala Energy Ltd | $0.04 | -18.37% |

| LIS | Li-S Energy Ltd | $0.115 | -17.86% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| AVE | Avecho Biotechnology Ltd | $0.021 | +40.00% |

| FTI | Fortifai Ltd | $1.12 | +12.56% |

| AVR | Anteris Technologies Global Corp | $15.00 | +10.05% |

| GLE | GLG Corp Ltd | $0.155 | +6.90% |

| TEA | Tasmea Ltd | $9.65 | +6.87% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| COI | Comet Ridge Ltd | $0.10 | -23.08% |

| BTE | Botala Energy Ltd | $0.04 | -18.37% |

| VIT | Vitura Health Ltd | $0.022 | -15.39% |

| BAK | BARKLY Rare EARTHS Ltd | $0.16 | -13.51% |

| AHE | Adheris Health Ltd | $0.013 | -13.33% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| WVOL | iShares MSCI World Ex Aust Minimum Volatility ETF | $45.62 | +0.66% |

| EGH | Eureka Group Holdings Ltd | $0.685 | +0.74% |

| IAGPF | Insurance Australia Group Ltd | $104.96 | +0.06% |

| GCI | Gryphon Capital Income Trust | $2.08 | +0.48% |

| VVLU | Vanguard Global Value Equity Active ETF | $82.60 | +1.46% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| DBF | Duxton Farms Ltd | $0.445 | -1.11% |

| KAR | Karoon Energy Ltd | $1.37 | -2.84% |

| NVX | Novonix Ltd | $0.16 | -3.03% |

| REA | REA Group Ltd | $131.58 | +0.05% |

| SPK | Spark New Zealand Ltd | $1.45 | -2.03% |