News | Market Wraps

Evening Wrap: ASX 200 firms on surging iron ore, copper, and base metals stocks - but lithium plays shine brightest

The S&P/ASX 200 closed 4.7 points higher, up 0.06%.

Mentioned

The S&P/ASX 200 closed 4.7 points higher, up 0.06%.

Strong gains in iron ore, copper, and other base metals stocks were the feature of today's trade on the ASX. The reason? News that China's massive property market may finally be showing signs of turning around. It's early days, but it was enough to spur investors to snap up beaten down resources plays.

Also of particular interest, local lithium stocks staged a strong rally as their international counterparts moved sharply higher overnight.

Click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key upcoming economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on Chinese blue-chip and property shares plus Iron Ore in today's ChartWatch.

Let's dive in!

Today in Review

Thu 13 Feb 25, 5:37pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,540.0 | +0.06% |

| All Ords | 8,804.2 | +0.05% |

| Small Ords | 3,203.1 | +0.34% |

| All Tech | 4,071.1 | -0.15% |

| Emerging Companies | 2,386.5 | +0.45% |

Currency | ||

| AUD/USD | 0.6293 | +0.22% |

US Futures | ||

| S&P 500 | 6,085.75 | +0.21% |

| Dow Jones | 44,541.0 | +0.18% |

| Nasdaq | 21,907.25 | +0.47% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Materials | 17,154.6 | +1.52% |

| Consumer Discretionary | 4,222.1 | +0.88% |

| Industrials | 8,015.4 | +0.11% |

| Information Technology | 2,860.3 | -0.21% |

| Real Estate | 3,913.0 | -0.28% |

| Financials | 9,233.9 | -0.30% |

| Communication Services | 1,661.6 | -0.54% |

| Health Care | 43,223.4 | -0.66% |

| Energy | 8,707.1 | -0.78% |

| Consumer Staples | 11,758.6 | -0.97% |

| Utilities | 8,524.4 | -2.36% |

Markets

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 4.7 points higher at 8,540.0, 0.41% from its session high and just 0.06% from its low. In the broader-based S&P/ASX 300 (XKO), advancers beat decliners by a modest 156 to 125.

Lithium stocks staged a welcome countertrend rally today. Mineral Resources (ASX: MIN) (+7.0%) had a becoming a substantial shareholder notice from UBS, and Patriot Battery Metals (ASX: PMT) (+5.2%), Liontown Resources (ASX: LTR) (+9.2%) and Wildcat Resources (ASX: WC8) (+10.0%) each delivered presentations at the Bell Potter Unearthed Conference, but there were few obvious stock specific news drivers to explain the sector’s good fortune.

It may simply be a case of a rising tide lifting all ships as the benchmark sector ETF – the Global X Lithium & Battery Tech ETF (NYSE: LIT) logged just shy of a 3% gain overnight. It was spurred by gains in Chinese lithium major Gangfeng Lithium (SZSE: 002460) which gained over 7% after it announced it had commenced production at its Argentinian Mariana project. Gangfeng has pulled back a little since, but along with EV battery supply chain behemoth Contemporary Amperex Technology Co. Limited (CATL) (SZSE: 300750) – who rallied on news it is seeking a listing in Hong Kong – is still showing gains of around 5% over the last two trading sessions. US-based Albermarle also rallied modestly overnight on quarterly earnings.

It certainly wasn’t lithium minerals prices that sparked today’s rally, those have been flat-to-down over the past couple of trading sessions. The benchmark May lithium carbonate contract on GFEX was -0.3% lower today and is down 1.0% for the week, while the Platts Australian Spodumene 6% assessment was down 1.2% yesterday and is down 1.8% for the week. (Oh, and not a single ASX lithium stock qualifies for my ChartWatch uptrends lists either!)

More broadly across the Materials (XMJ) (+1.5%) sector – today's best performing – prices were supported by generally higher base metals prices overnight, but also by news that China’s property market may finally be showing tentative signs of turning around. A report by a major Chinese newspaper suggested that land auctions in major centres Beijing, Zhengzhou, Shenzhen and Hangzhou have recorded premiums this year – a stark contrast to previous auctions that garnered little interest from developers.

I have technical analysis on the FTSE China A50 Index, the Hang Seng China A Properties Index, and Iron Ore for you tonight’s ChartWatch.

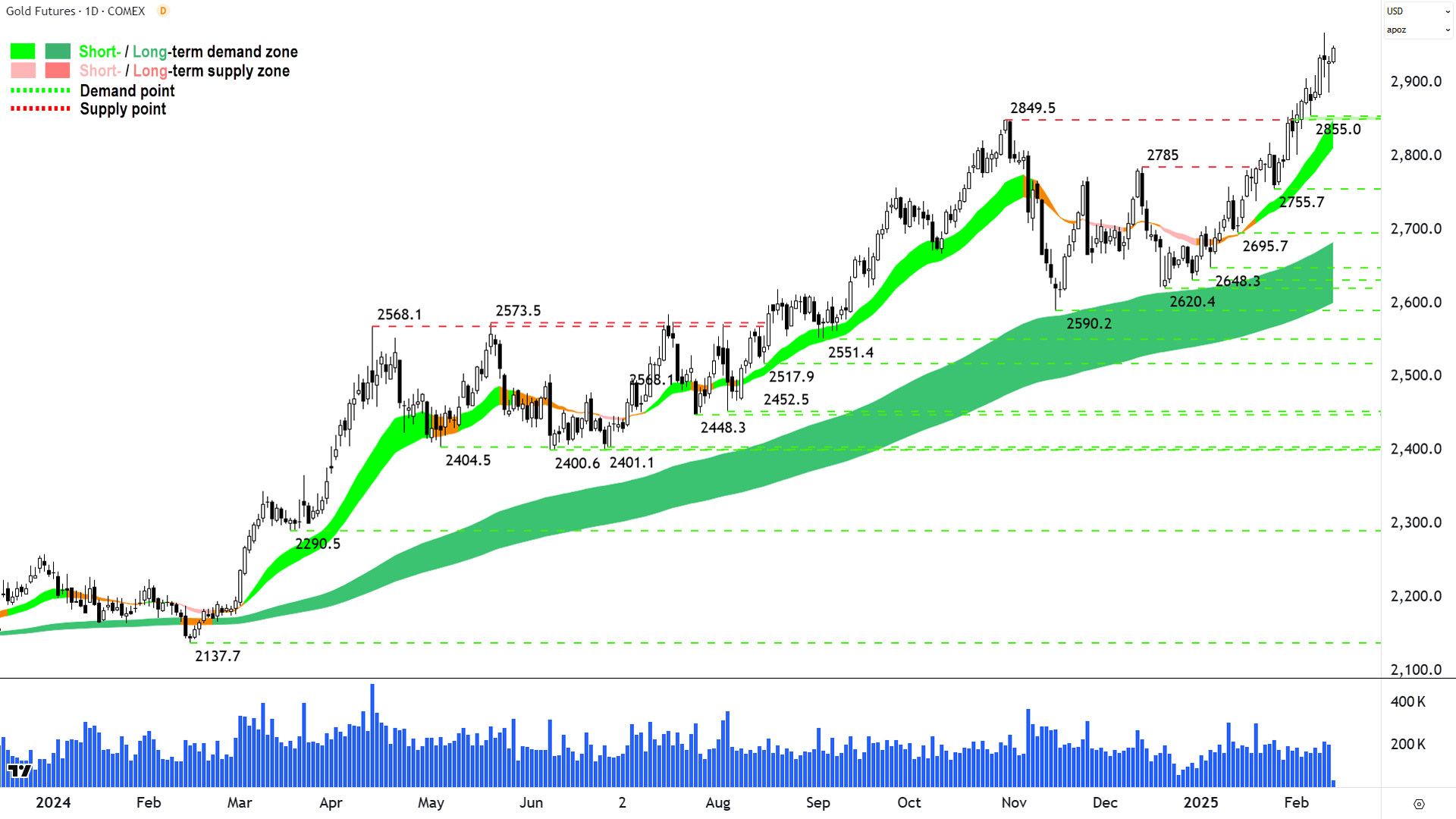

A sub-sector of Materials, the Gold (XGD) (+0.87%) sub-index was the next best performing area of the market today, responding in kind to another push towards record highs in the gold price in Asian trade today. Basically the reverse of yesterday's outcome for local gold plays.

%20COMEX%20Chart%2013%20February%202025.png)

Gold Futures (Front month, back-adjusted) COMEX (click here for full size image)

{kind=link}

Consumer Discretionary (XDJ) (+0.87%) was the only other major sector index to outperform the benchmark ASX 200. Better than expected first half results from online homewares retailer Temple & Webster (ASX: TPW) (+13.0%) and news of a strategic review at gaming and wagering technology company Aristocrat Leisure (ASX: ALL) (+2.4%) helped proceedings there.

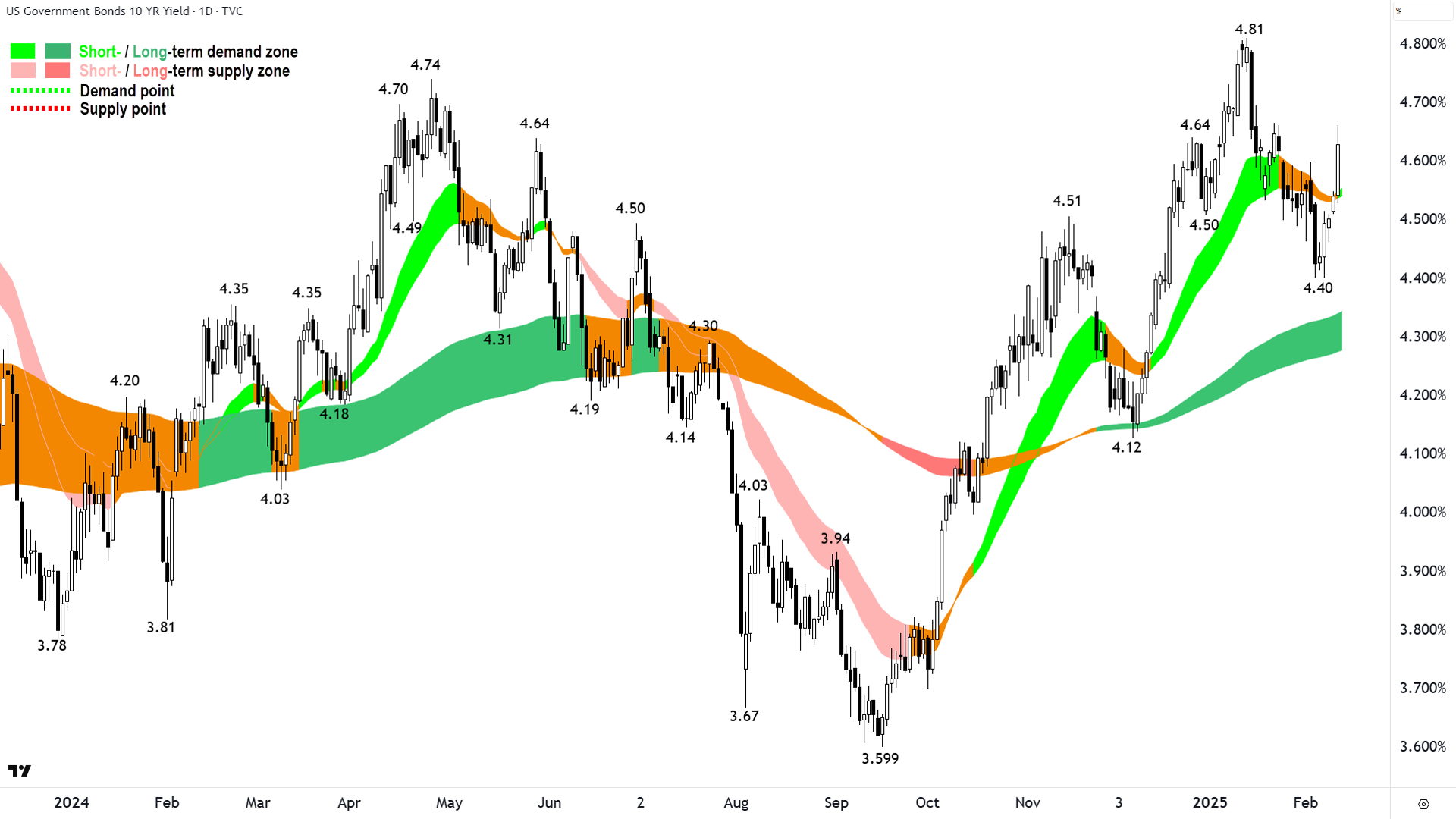

Contrasting the winning sectors, another sharp rise in benchmark risk-free market yields overnight hurt the likes of bond proxies Utilities (XUJ) (-2.4%) and Real Estate Investment Trusts (XPJ) (-0.33%), as well as high-PE-long duration Health Care (XHJ) (-0.66%) and Communication Services (XTJ) (-0.54%).

Elsewhere, a dip in energy commodity prices dragged on stocks in the beleaguered Energy (XEJ) (-0.78%) sector.

US 10 Year T-Bond Yield (click here for full size image)

{kind=link}

ChartWatch

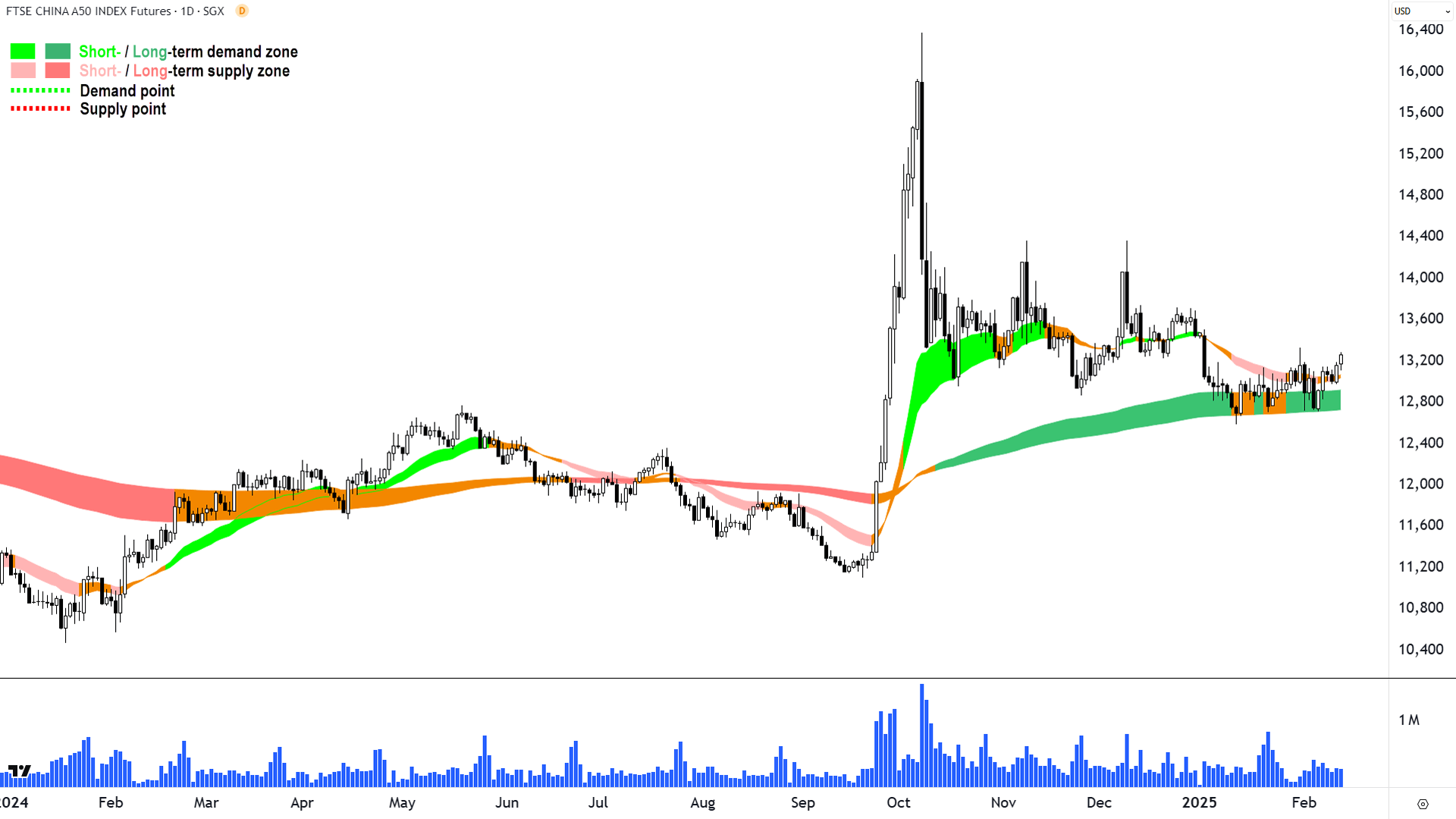

FTSE China A50 Index Futures

The Great Wall of Dynamic Demand does it again! 🧱 (click here for full size image)

{kind=link}

The last time we covered the China A50 was in ChartWatch in the Evening Wrap on 7 January.

In that update, we were tracking yet another failure to launch for Chinese shares in the wake of months of big promises of sweeping stimulus measures – but with few actually materialising.

Fortunately for Chinese investors (and a little selfishly, for us too!), things haven’t deteriorated any further. The China A50 share index has steadied at the ever-reliable dynamic demand we've come to expect at the long term trend ribbon. The Great Wall of Dynamic Demand – if you will! 🧱

If we both squint really hard, perhaps there’s even a fledgling short term uptrend developing here – or at least if price action (back to rising peaks and rising troughs) and candles (predominantly white and or with downward pointing shadows) are to believe. 🧐

The short term trend ribbon is yet to deliver us its vote of demand-side control confidence, but it does appear to be turning higher after recently neutralising the previous short term downtrend.

All in all I suggest the new uptrend more likely to improve here than fall off a cliff, but it’s hard to get too much more excited that that. A close above the 31-Jan point of supply at 13328 would allow for greater confidence, and a close above the 25-Dec point of supply at 13719 for greater confidence again.

Alternatively, a close below the Great Wall of Dynamic Demand would likely lead to talk of “falling off a cliff” scenarios…📉

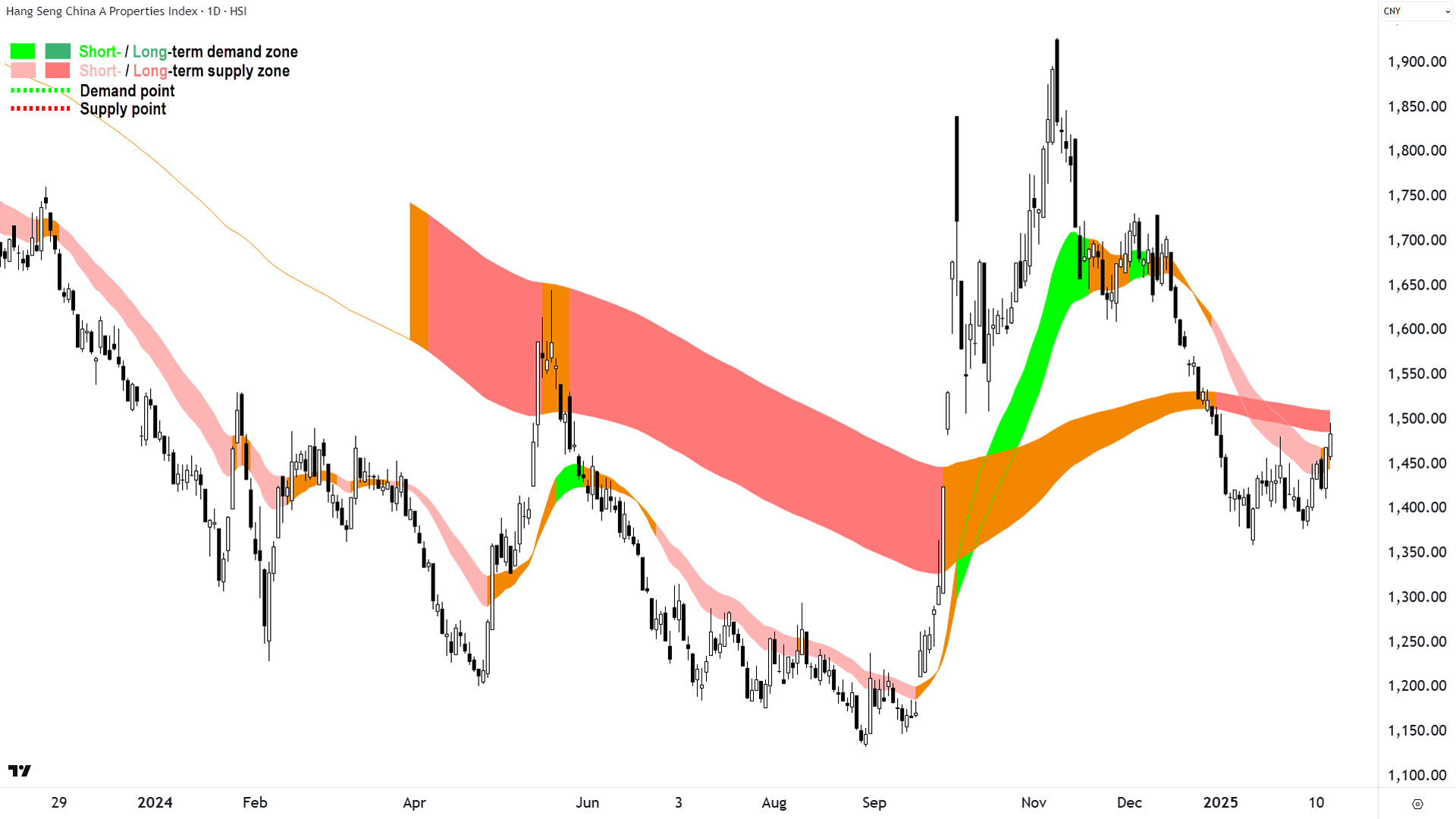

Hang Seng China A Properties Index

Still plenty of work to prove the demand-side is back in control here... (click here for full size image)

{kind=link}

Not nearly as good here, but at least the price action is improving to retest the dynamic supply at the long term downtrend ribbon (Great Wall of Dynamic Supply? 🤔). Candles are arguably predominantly demand-side in nature since the 13-Jan trough at 1359.

Today’s live candle appears so far to be closing above the 21-Jan point of supply at 1481 – and if it can stay this way – is also a good indication the demand-side is moving back into the market with some force.

Plenty more confirmation is required in the price action, and in getting and staying above the short and long term trend ribbons – but this is another chart that suggests things are improving for Chinese stocks – and more specifically, with respect to Chinese property stocks.

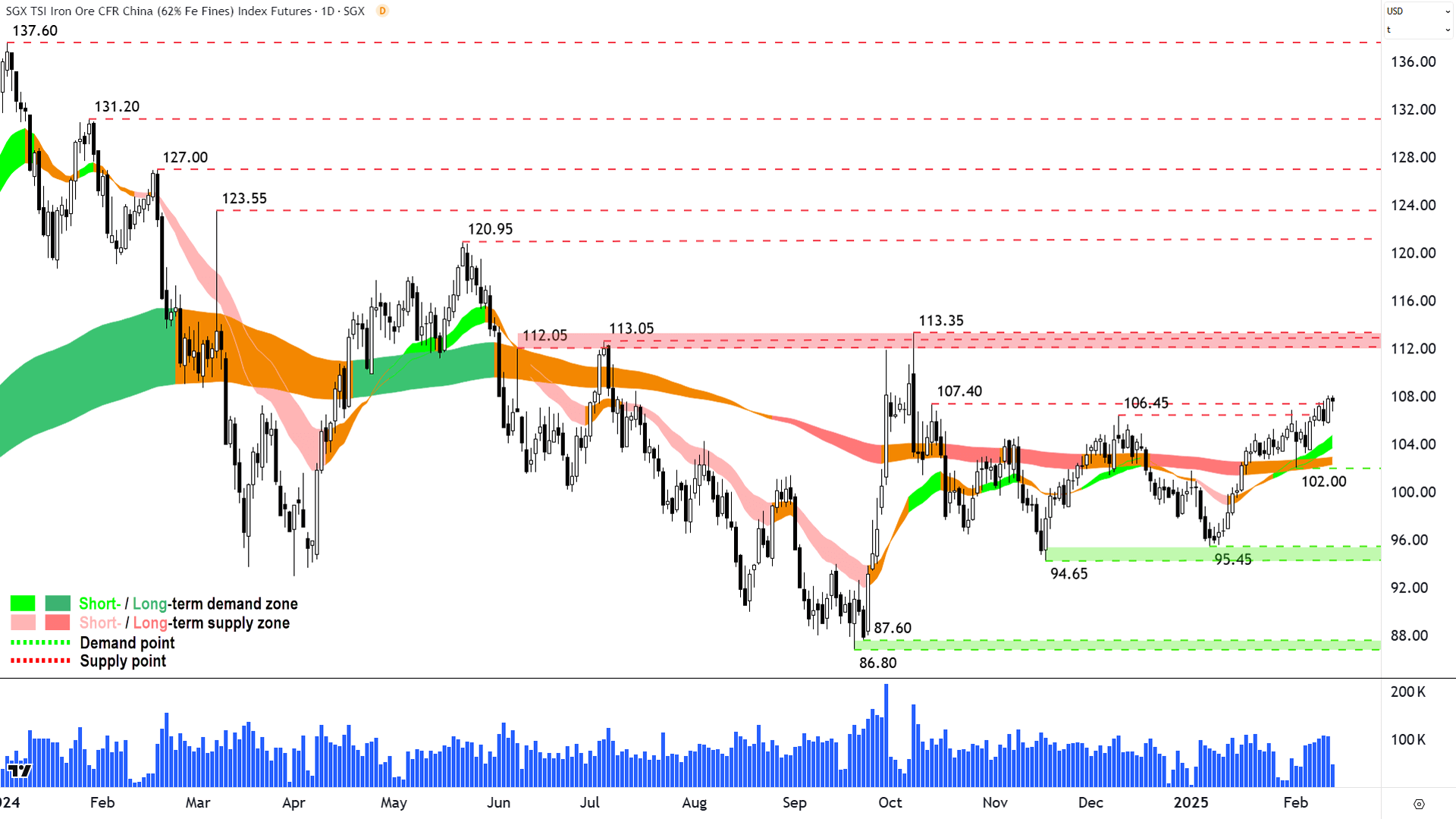

Iron Ore 62% (Front month, back-adjusted) SGX

%20SGX%20Chart%2013%20February%202025.png)

Chinese stocks' recovery helping iron ore (click here for full size image)

{kind=link}

The natural conclusion of our analysis of Chinese stocks is to check out the chart of Iron Ore. The last time we covered it was in the Evening Wrap on 30 January.

In that update, we were tracking, ironically, another fledgling short term uptrend. Even better, at the time, iron ore had reclaimed the long term trend ribbon.

The short term uptrend continues to progress well and the price action remains higher peaks and higher troughs, plus candles continue to look predominantly demand-side in nature. The short term uptrend ribbon appears to be acting as a zone of dynamic demand, as does the long term trend ribbon (neutral).

These are all ticks for likely demand-side control.

With the 106.45-107.40 zone of supply now cleared, the next logical overhead supply zone to seek out is 112.05-113.35. I expect this to be a major impediment to the prevailing short term trend – it will take some serious demand to consume.

Demand is likely to be encountered at the short term uptrend ribbon, but also down to the static point of demand at 102. The short term uptrend remains intact as long as the iron ore price does not close below that level.

It’s a gradual but steady uptrend here – but in many ways that’s more than sufficient for our wildly profitable bulk iron ore producers.

Economy

Today

AUS MI Inflation Expectations January

4.6% p.a. vs 4.0% p.a. in December = Big jump to a scary number and will not be cheered by the RBA! 👎

Later this week

Friday

00:30 USA Core Producer Price Index (PPI) January (+0.3% m/m and +3.3% p.a. forecast vs 0.0% m/m and +3.5% p.a. in December)

Saturday

00:30 USA Core Retail Sales January (+0.3% m/m forecast vs +0.4% m/m in December)

Latest News

Interesting Movers

Trading higher

+13.1% Horizon Minerals (HRZ) - Continued positive response to 12-Jun Phillips Find - Processing of First Ore, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, added to ChartWatch ASX Scans Uptrends list yesterday 🔎📈

+13.0% Temple & Webster Group (TPW) - Half Yearly Report and Accounts and Half Year Presentation, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+10.0% Wildcat Resources (WC8) - Investor Presentation - Bell Potter Unearthed Conference, general strength across the broader Lithium sector today.

+9.2% Liontown Resources (LTR) - Investor Presentation - Bell Potter Unearthed Conference, general strength across the broader Lithium sector today.

+7.4% Pantoro (PNR) - No news since 10-Feb East Coast Roadshow Presentation, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+7.0% Mineral Resources (MIN) - Becoming a substantial holder, general strength across the broader Lithium sector today.

+7.0% Domain Australia (DHG) - Appendix 4D and Financial Statements, Domain HY25 Investor Presentation, and Appointment of Interim CEO Greg Ellis.

+5.7% Firefly Metals (FFM) - FireFly Resources Rising Stars Brisbane Presentation, general strength across the broader Resources sector today.

+5.7% IGO (IGO) - No news, general strength across the broader Lithium sector today.

+5.5% Develop Global (DVP) - No news, general strength across the broader Lithium sector today, rise is consistent with prevailing short term uptrend and long term trend is transitioning from down to up, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.4% Sigma Healthcare (SIG) - No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.3% Metals X (MLX) - No news, general strength across the broader Resources sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.1% Andean Silver (ASL) - Appendix 4D and 2025 Half-Year Financial Statements and 2025 Half-Year Results Presentation Slides.

+5.0% ASX (ASX) - N and N.

+4.7% Pilbara Minerals (PLS) - Change in substantial holding (State Street is a rumoured active short seller, this suggests a smaller interest in PLS), general strength across the broader Lithium sector today.

Trading lower

-12.6% Insurance Australia Group (IAG) - IAG 1H25 Appendix 4D and Half Year Report and IAG 1H25 Results Presentation.

-6.9% Alliance Aviation Services (AQZ) - HY25 Interim Report and HY25 Results Presentation, fall is consistent with prevailing short and long term downtrends 🔎📉

-6.8% Lotus Resources (LOT) - No news, general weakness across the broader Uranium sector today, fall is consistent with prevailing short and long term downtrends 🔎📉

-6.6% AGL Energy (AGL) - Continued negative response to 12-Feb FY25 Half-Year Results Presentation.

-5.7% Treasury Wine Estates (TWE) - Appendix 4D and 2025 Interim Results and 2025 Interim Results Investor and Analyst Presentation.

-5.4% Graincorp (GNC) - GrainCorp provides FY25 earnings guidance, fall is consistent with prevailing short and long term downtrends 🔎📉

-5.2% Silex Systems (SLX) - No news, general weakness across the broader Uranium sector today.

-4.7% Orora (ORA) - ORA - Appendix 4D and Interim Financial Report and ORA - HY25 Investor Presentation.

-4.6% Suncorp Group (SUN) - Continued negative response to 12-Feb HY25 Results Presentation.

Broker Moves

AGL Energy (AGL)

Retained at neutral at Goldman Sachs; Price Target: $11.90 from $11.65

Retained at buy at Jefferies; Price Target: $13.32 from $12.38

Retained at outperform at Macquarie; Price Target: $12.29 from $12.08

Retained at overweight at Morgan Stanley; Price Target: $12.66 from $12.88

Retained at outperform at RBC Capital Markets; Price Target: $13.00 from $12.50

Retained at neutral at UBS; Price Target: $11.50 from $11.00

Amotiv (AOV)

Retained at buy at Canaccord Genuity; Price Target: $14.40

Retained at buy at Citi; Price Target: $14.13 from $12.65

Retained at buy at Goldman Sachs; Price Target: $12.20 from $13.00

Retained at overweight at JP Morgan; Price Target: $12.00 from $13.00

Retained at outperform at Macquarie; Price Target: $12.94 from $13.64

Retained at add at Morgans; Price Target: $12.95 from $12.80

Retained at outperform at RBC Capital Markets; Price Target: $13.50 from $14.00

Retained at buy at UBS; Price Target: $12.60 from $13.00

Arena Reit. (ARF)

Retained at neutral at Macquarie; Price Target: $3.96 from $3.99

Retained at equal-weight at Morgan Stanley; Price Target: $4.65

Andean Silver (ASL)

Retained at buy at Canaccord Genuity; Price Target: $2.85

ASX (ASX)

Retained at sell at UBS; Price Target: $65.00

Bluebet (BBT)

Retained at add at Morgans; Price Target: $0.470 from $0.430

BHP Group (BHP)

Retained at neutral at UBS; Price Target: $42.00

Bannerman Energy (BMN)

Retained at buy at Shaw and Partners; Price Target: $7.40

Bravura Solutions (BVS)

Downgraded to underweight from neutral at JP Morgan; Price Target: $2.15 from $1.90

Upgraded to outperform from neutral at Macquarie; Price Target: $3.17 from $2.05

Retained at positive at Wilsons; Price Target: $3.17 from $2.06

Commonwealth Bank of Australia (CBA)

Retained at sell at Citi; Price Target: $91.50

Retained at underperform at Macquarie; Price Target: $105.00

Retained at underweight at Morgan Stanley; Price Target: $127.00 from $119.00

Retained at reduce at Morgans; Price Target: $102.00 from $95.31

Retained at sell at Ord Minnett; Price Target: $105.00

Computershare (CPU)

Retained at neutral at Citi; Price Target: $40.90 from $35.00

Retained at neutral at Goldman Sachs; Price Target: $38.00 from $35.50

Downgraded to hold from buy at Jefferies; Price Target: $39.50 from $34.00

Retained at hold at Morgans; Price Target: $34.43

Downgraded to hold from accumulate at Ord Minnett; Price Target: $42.00 from $36.25

Domain Australia (DHG)

Retained at neutral at Citi; Price Target: $3.20

Retained at neutral at E&P; Price Target: $3.00

Retained at neutral at UBS; Price Target: $3.10

Downer EDI (DOW)

Retained at sector perform at RBC Capital Markets; Price Target: $5.75

Retained at neutral at UBS; Price Target: $5.75

Dexus Industria Reit. (DXI)

Retained at outperform at Macquarie; Price Target: $3.18 from $3.05

Evolution Mining (EVN)

Retained at neutral at Citi; Price Target: $6.00

Retained at neutral at Goldman Sachs; Price Target: $5.35 from $5.10

Retained at hold at Jefferies; Price Target: $5.50

Downgraded to underweight from neutral at JP Morgan; Price Target: $4.90 from $4.95

Retained at underperform at Macquarie; Price Target: $5.50

Retained at equal-weight at Morgan Stanley; Price Target: $5.55

Downgraded to lighten from hold at Ord Minnett; Price Target: $5.30 from $5.35

Retained at underperform at RBC Capital Markets; Price Target: $4.30

Retained at sell at UBS; Price Target: $5.45 from $5.40

Firefly Metals (FFM)

Retained at buy at Canaccord Genuity; Price Target: $1.950

Retained at buy at Shaw and Partners; Price Target: $1.900

Graincorp (GNC)

Retained at outperform at RBC Capital Markets; Price Target: $10.75

Guzman y Gomez (GYG)

Retained at overweight at Morgan Stanley; Price Target: $38.50

Insurance Australia Group (IAG)

Retained at buy at Citi; Price Target: $9.65

Retained at neutral at UBS; Price Target: $9.15

Imdex (IMD)

Retained at hold at Bell Potter; Price Target: $2.70 from $2.25

Upgraded to neutral from sell at Citi; Price Target: $2.85 from $1.95

Retained at neutral at Macquarie; Price Target: $2.90 from $2.20

Retained at add at Morgans; Price Target: $3.20 from $2.40

Retained at neutral at UBS; Price Target: $2.95 from $2.60

Orora (ORA)

Retained at neutral at Citi; Price Target: $2.80

Retained at neutral at UBS; Price Target: $2.57

Origin Energy (ORG)

Retained at buy at Citi; Price Target: $11.50

Retained at buy at UBS; Price Target: $11.90

Paladin Energy (PDN)

Retained at buy at Shaw and Partners; Price Target: $15.80

Pro Medicus (PME)

Retained at sector perform at RBC Capital Markets; Price Target: $295.00

Perpetual (PPT)

Retained at buy at Bell Potter; Price Target: $25.40

Qantas Airways (QAN)

Downgraded to neutral from outperform at Macquarie; Price Target: $9.30 from $8.40

Ramsay Health Care (RHC)

Retained at hold at Ord Minnett; Price Target: $41.45

South32 (S32)

Retained at neutral at Citi; Price Target: $3.90

Retained at outperform at RBC Capital Markets; Price Target: $4.20

Siteminder (SDR)

Retained at overweight at Morgan Stanley; Price Target: $6.80

Suncorp Group (SUN)

Retained at neutral at Citi; Price Target: $20.00 from $19.90

Retained at buy at Goldman Sachs; Price Target: $21.00 from $20.50

Retained at neutral at Macquarie; Price Target: $19.10 from $18.00

Retained at overweight at Morgan Stanley; Price Target: $22.60 from $22.10

Retained at add at Morgans; Price Target: $22.33 from $21.01

Retained at accumulate at Ord Minnett; Price Target: $21.00 from $20.35

Retained at neutral at UBS; Price Target: $20.85 from $20.70

Seven West Media (SWM)

Retained at buy at Ord Minnett; Price Target: $0.210

Telstra Group (TLS)

Retained at buy at Goldman Sachs; Price Target: $4.50

Temple & Webster Group (TPW)

Retained at buy at Citi; Price Target: $13.50

Retained at outperform at RBC Capital Markets; Price Target: $16.00

Retained at neutral at UBS; Price Target: $11.80

Treasury Wine Estates (TWE)

Retained at buy at Citi; Price Target: $12.97

Retained at overweight at Morgan Stanley; Price Target: $14.60

Retained at buy at UBS; Price Target: $14.00

Wesfarmers (WES)

Retained at underweight at Morgan Stanley; Price Target: $60.70

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| BGE | Bridge Saas Ltd | $0.031 | +55.00% |

| FME | Future Metals NL | $0.016 | +45.46% |

| MVL | Marvel Gold Ltd | $0.011 | +37.50% |

| MPR | Mpower Group Ltd | $0.012 | +33.33% |

| MRZ | Mont Royal Resources Ltd | $0.032 | +28.00% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| DUN | Dundas Minerals Ltd | $0.033 | -26.67% |

| RAS | Ragusa Minerals Ltd | $0.02 | -20.00% |

| XGL | Xamble Group Ltd | $0.016 | -20.00% |

| PBL | Parabellum Resources Ltd | $0.043 | -18.87% |

| MGL | Magontec Ltd | $0.21 | -17.65% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| EXT | Excite Technology Services Ltd | $0.019 | +18.75% |

| NMR | Native Mineral Resources Holdings Ltd | $0.067 | +17.54% |

| HRZ | Horizon Minerals Ltd | $0.069 | +13.12% |

| TPW | Temple & Webster Group Ltd | $16.14 | +13.03% |

| HVY | Heavy Minerals Ltd | $0.235 | +11.91% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| XGL | Xamble Group Ltd | $0.016 | -20.00% |

| UBI | Universal Biosensors Inc | $0.075 | -12.79% |

| SCP | Scalare Partners Holdings Ltd | $0.14 | -12.50% |

| SOC | Soco Corporation Ltd | $0.07 | -12.50% |

| 1MC | Morella Corporation Ltd | $0.02 | -9.09% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| PCI | Perpetual Credit Income Trust | $1.175 | +0.86% |

| WVOL | Ishares MSCI World Ex Aust Minimum Volatility ETF | $43.65 | +0.35% |

| IAGPF | Insurance Australia Group Ltd | $105.30 | +0.19% |

| GCI | Gryphon Capital Income Trust | $2.04 | -0.49% |

| CTD | Corporate Travel Management Ltd | $15.21 | -1.30% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| VUL | Vulcan Energy Resources Ltd | $4.06 | +1.00% |

| PLY | Playside Studios Ltd | $0.205 | -2.38% |

| RFG | Retail Food Group Ltd | $1.91 | -1.04% |

| PXA | Pexa Group Ltd | $11.89 | +0.34% |

| RHI | Red Hill Minerals Ltd | $3.77 | -5.75% |