News | Market Wraps

Evening Wrap: ASX 200 extends losses as Santa rally fizzles, tech, banks, energy and resources down, but gold shines again

The S&P/ASX 200 closed 39.4 points lower, down 0.47%.

Mentioned

The S&P/ASX 200 closed 39.4 points lower, down 0.47%.

Before we get into it: Share your predictions for 2025 in Livewire’s Outlook Series Survey. In return, you’ll get first access to top picks, prediction, and exclusive expert insights for 2025. Need a reason to take part? Our readers' 2024 stock picks delivered. Big: +20% on ASX stocks, +25% on ETFs! Complete the quick survey.

Real Estate stocks rely heavily on debt to fund their investments, so lower market yields in the wake of the RBA's dovish tilt yesterday helped the sector to strong gains today.

Also doing well today, was the Gold sub-index – the gold price is on the rise again, and the sector is seeing substantial renewed interest.

Otherwise, it was a generally dour day’s trade for Australian stocks, with further profit taking in highflying Technology, Financial, and Healthcare names, as well as a disappointing return to (poor) form for Energy and Resources stocks.

Click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all of the key upcoming economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on Gold and Silver in today's ChartWatch.

Let's dive in!

Today in Review

Wed 11 Dec 24, 5:09pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,353.6 | -0.47% |

| All Ords | 8,610.4 | -0.46% |

| Small Ords | 3,159.7 | -0.14% |

| All Tech | 3,851.0 | -0.79% |

| Emerging Companies | 2,303.6 | +0.33% |

Currency | ||

| AUD/USD | 0.6371 | -0.10% |

US Futures | ||

| S&P 500 | 6,051.0 | +0.08% |

| Dow Jones | 44,332.0 | -0.01% |

| Nasdaq | 21,430.75 | +0.12% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Real Estate | 3,926.1 | +0.81% |

| Consumer Discretionary | 4,000.2 | +0.09% |

| Communication Services | 1,683.3 | -0.26% |

| Consumer Staples | 11,842.6 | -0.33% |

| Materials | 17,286.2 | -0.41% |

| Financials | 8,736.6 | -0.61% |

| Health Care | 45,136.4 | -0.63% |

| Utilities | 8,914.4 | -0.70% |

| Energy | 8,449.6 | -1.00% |

| Industrials | 7,598.4 | -1.02% |

| Information Technology | 2,756.6 | -1.35% |

Markets

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 39.4 points lower at 8,353.6, 0.51% from its session high and just 0.14% from its low. In the broader-based S&P/ASX 300 (XKO), advancers lagged decliners by approximately 2 to 1 for a third day in a row (Today: 71 to 155).

The Real Estate Investment Trusts (XPJ) (+0.87%) was the best performing sector today, likely in response to the sharp fall in local risk-free market yields. Markets are betting on RBA rate cuts coming sooner and more frequently over the next 18 months in the wake of the RBA Board meeting and interest rate decision yesterday.

Australian 2-Year Government Bond Yield chart 10 December 2024 (click here for full size image)

{kind=link}

Real Estate stocks rely heavily on debt to fund their investments, so lower market yields generally means cheaper sources of funding. It also means less competition from risk-free bonds which are seen to have similar, long duration income streams. Also, lower rates more generally helps tenants pay their rent.

Also doing well today was the Gold (XGD) (+0.16%) sub-index – the gold price is on the rise again, and the sector has seen renewed interest since Macquarie’s gold and gold sector update released last week. I have detailed technical analysis on the gold price (and the silver price) in this evening’s ChartWatch section below.

In what was a generally dour day’s trade for Australian stocks, the Consumer Discretionary (XDJ) (+0.09%) sector was the only other major ASX sector to scrape in with a win – albeit a small one. It was also the only casualty from yesterday’s big sector rotation (see yesterday’s Evening Wrap) to reverse it’s fortunes today.

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Ora Banda Mining (OBM) | $0.710 | +$0.07 | +10.9% | -4.1% | +208.7% |

Star Entertainment (SGR) | $0.195 | +$0.015 | +8.3% | -9.3% | -65.8% |

Eagers Automotive (APE) | $12.11 | +$0.61 | +5.3% | +2.5% | -11.6% |

Iperionx (IPX) | $4.53 | +$0.12 | +2.7% | +12.7% | +221.3% |

Temple & Webster (TPW) | $13.21 | +$0.32 | +2.5% | +14.4% | +58.2% |

Centuria Capital Group (CNI) | $1.885 | +$0.045 | +2.4% | +2.7% | +18.2% |

Region Group (RGN) | $2.16 | +$0.05 | +2.4% | -0.5% | -2.3% |

Stockland (SGP) | $5.08 | +$0.11 | +2.2% | -2.3% | +21.2% |

Tabcorp (TAH) | $0.570 | +$0.01 | +1.8% | +11.8% | -16.2% |

Goodman Group (GMG) | $37.61 | +$0.63 | +1.7% | +3.0% | +62.1% |

Westgold Resources (WGX) | $3.06 | +$0.04 | +1.3% | +9.7% | +39.1% |

Ramelius Resources (RMS) | $2.40 | +$0.03 | +1.3% | +18.2% | +50.9% |

Resolute Mining (RSG) | $0.415 | +$0.005 | +1.2% | -7.8% | -2.4% |

BWP Trust (BWP) | $3.34 | +$0.04 | +1.2% | -2.1% | -6.7% |

Genesis Minerals (GMD) | $2.77 | +$0.03 | +1.1% | +20.4% | +50.5% |

Wesfarmers (WES) | $74.98 | +$0.77 | +1.0% | +8.2% | +39.6% |

National Storage Reit (NSR) | $2.38 | +$0.02 | +0.8% | -4.8% | +0.8% |

Waypoint Reit (WPR) | $2.41 | +$0.02 | +0.8% | -3.6% | -0.8% |

ARB Corporation (ARB) | $39.97 | +$0.31 | +0.8% | -4.0% | +20.9% |

HMC Capital (HMC) | $11.70 | +$0.09 | +0.8% | +8.4% | +105.3% |

G8 Education (GEM) | $1.370 | +$0.01 | +0.7% | +1.9% | +42.0% |

Centuria Industrial Reit (CIP) | $2.88 | +$0.02 | +0.7% | -5.0% | -9.7% |

Healthco Health & Wellness Reit (HCW) | $1.045 | +$0.005 | +0.5% | -7.1% | -27.2% |

Charter Hall Infrastructure Reit (CQE) | $2.55 | +$0.01 | +0.4% | -2.3% | -9.3% |

Perseus Mining (PRU) | $2.78 | +$0.01 | +0.4% | +10.8% | +48.7% |

Today's strongest stocks from the strongest ASX sectors

Elsewhere, the big fund managers continued to take big 2024 profits on Information Technology (XIJ) (-1.35%) and Financials (XFJ) (-0.61%), as well as high-PE winners in Health Care (XHJ) (-0.63%) and Communication Services (XTJ) (-0.26%).

Perhaps the most disappointing aspect of today's trade, however, was that the two beneficiary sectors of yesterday's big sector rotation – Energy (XEJ) (-1.0%) and Resources (XJR) (-0.51%) – went back to their 2024 losing ways.

The bump (and pump) post the latest promise (all promise and no substance!) of China stimulus on Monday appears to be fading, with most base metals price lower overnight, iron ore softer again today, and energy commodities barely moved. Can't take a trick...🤦

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Imdex (IMD) | $2.40 | -$0.15 | -5.9% | -11.1% | +27.3% |

Clarity Pharmaceuticals (CU6) | $5.17 | -$0.32 | -5.8% | -30.7% | +248.1% |

IPH (IPH) | $4.72 | -$0.23 | -4.6% | -10.9% | -28.9% |

South32 (S32) | $3.52 | -$0.16 | -4.3% | -2.5% | +12.5% |

Mesoblast (MSB) | $1.630 | -$0.07 | -4.1% | +7.6% | +471.9% |

Superloop (SLC) | $2.16 | -$0.09 | -4.0% | +11.6% | +220.0% |

Australian Clinical Labs (ACL) | $3.42 | -$0.13 | -3.7% | -4.7% | +19.2% |

Computershare (CPU) | $32.01 | -$1.17 | -3.5% | +9.5% | +35.6% |

Nanosonics (NAN) | $3.04 | -$0.1 | -3.2% | -8.4% | -30.8% |

Champion Iron (CIA) | $6.11 | -$0.2 | -3.2% | +8.3% | -21.3% |

Wisetech Global (WTC) | $121.79 | -$3.81 | -3.0% | -7.9% | +81.1% |

Kelsian Group (KLS) | $3.59 | -$0.11 | -3.0% | -6.0% | -46.3% |

Suncorp Group (SUN) | $18.92 | -$0.56 | -2.9% | +0.6% | +36.1% |

QBE Insurance Group (QBE) | $19.05 | -$0.52 | -2.7% | +2.6% | +31.2% |

Smartgroup Corporation (SIQ) | $7.74 | -$0.21 | -2.6% | -4.4% | -5.6% |

Cleanaway Waste (CWY) | $2.75 | -$0.07 | -2.5% | 0% | +6.2% |

Objective Corporation (OCL) | $16.97 | -$0.43 | -2.5% | -2.7% | +44.1% |

Bluescope Steel (BSL) | $21.62 | -$0.54 | -2.4% | -0.9% | +2.2% |

Beach Energy (BPT) | $1.215 | -$0.03 | -2.4% | -2.8% | -18.5% |

Ampol (ALD) | $27.35 | -$0.65 | -2.3% | -2.6% | -19.5% |

Ramsay Health Care (RHC) | $37.94 | -$0.9 | -2.3% | -1.2% | -21.8% |

Bravura Solutions (BVS) | $2.12 | -$0.05 | -2.3% | +40.4% | +165.0% |

MA Financial (MAF) | $6.00 | -$0.14 | -2.3% | -10.7% | +9.9% |

Audinate Group (AD8) | $7.58 | -$0.17 | -2.2% | -20.2% | -46.6% |

Develop Global (DVP) | $2.41 | -$0.05 | -2.0% | +7.1% | -16.3% |

Today's weakest stocks from the weakest ASX sectors

ChartWatch

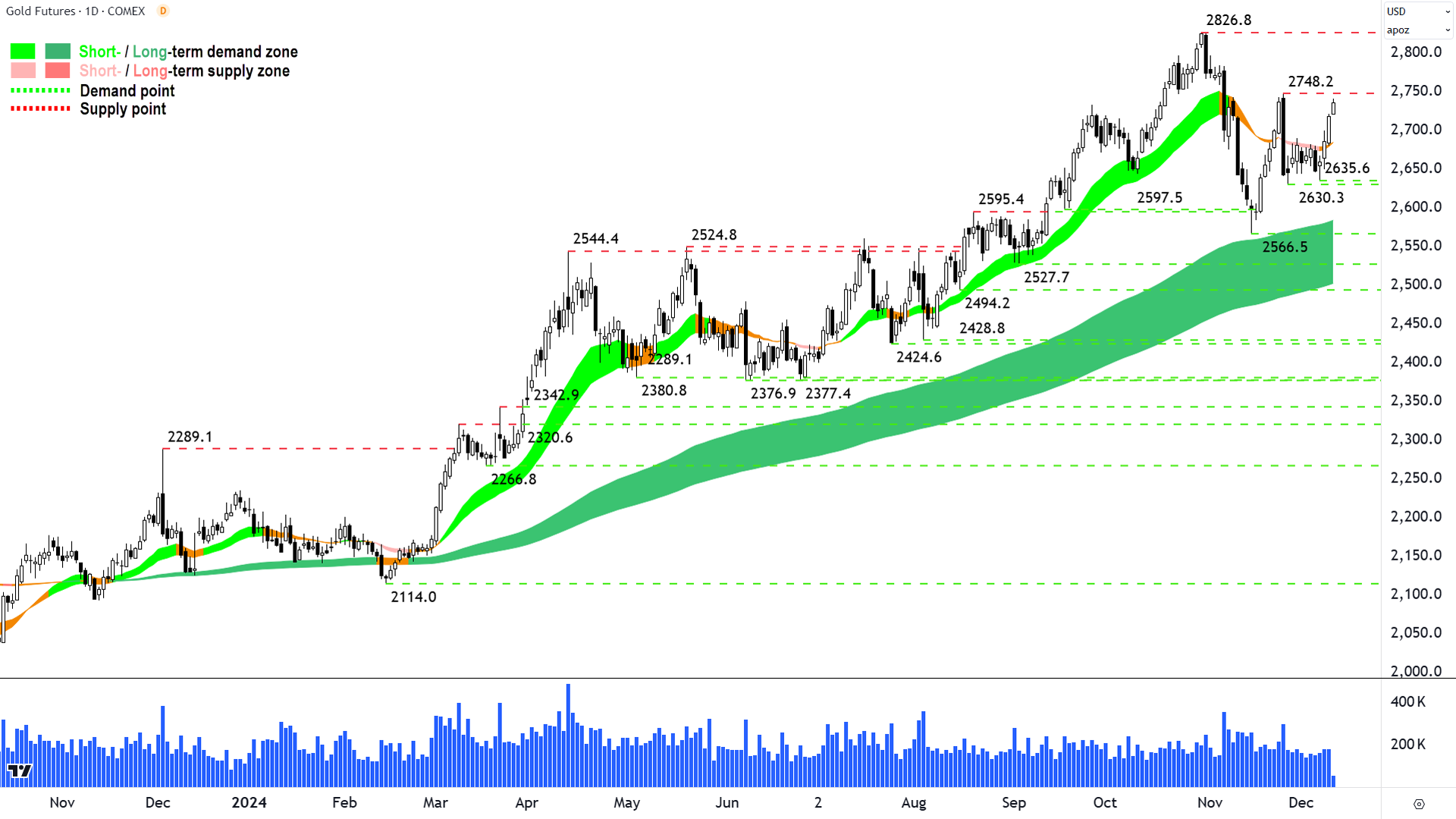

Gold Futures (Front month, back-adjusted) COMEX

%20COMEX%20chart%2011%20December%202024.png)

I stand corrected...for now! (click here for full size image)

{kind=link}

The last time we covered gold was in ChartWatch in the Evening Wrap on 4 December.

Many of you will recall that I’ve been sceptical of the sustainability of the gold bull market since the massive supply-signal (long black candle with low session close) on 25 Nov. I viewed that as confirmation the tide was turning after the post-US election rout.

In the last update, I noted that my expectations had not played out – that gold was putting up a decent fight – if only by not following through to the downside after that 25 Nov market signal.

More specifically, I noted that if the gold price could quickly “regain the midpoint of the 25 Nov candle is a minimum, but preferably also quickly above the next key point of supply at 2448.2” it would restart the long term uptrend and set up a retest of the 2826.8 all-time high.

So far so good on that path of price action. Gold has indeed pushed towards the top of the 25 Nov candle – itself now an important point of supply – and it's done so with some credible demand-side candles (i.e., those with white bodies and or downward pointing shadows).

A close above 2748.2 is really all that stands in the way of gold making a new high.

2630.3-2635.6 is now demand. As long as the gold price continues to close above there, I suggest the recently acquired upside momentum remains intact. Either that, or we see some nasty supply-side candles between here and 2826.98 (i.e., those with black bodies and or upward pointing shadows).

It's pretty simple. The candles and the price action will tell the story. One just needs to wait and watch for the clues! 🧐

Silver Futures (Front month, back-adjusted) COMEX

%20COMEX%20chart%2011%20December%202024.png)

That long term uptrend ribbon is a magical thing... (click here for full size image)

{kind=link}

The last time we covered silver was in ChartWatch in the Evening Wrap on 4 December.

In that update, I note that there appeared to be some “shopping” going on for silver in the long term uptrend dynamic demand zone.

More specifically, I noted that “A close back above 32.04 is critical to restart silver’s short and long term uptrends. Ideally it occurs on a long white-bodied candle with a high session close”.

That scenario did indeed play out, although the 9 Dec demand-side candle could have closed closer to its high for my liking. Still, I view the recent price action and candles as a credible restart of silver’s short and long term uptrends (back to rising peaks and rising troughs and predominantly demand-side candles).

35.15-35.47 is the key zone of supply and the next logical upside target.

Demand is 31.32, but really, it’s the long term uptrend ribbon. A close below 31.32 likely kills this new short term uptrend, whilst a close below 30.09 likely kills the long term one.

Until then, I can’t see any reason not to trust the new short/long term trend combination.

(Note that the Global X Physical Silver (ASX: ETPMAG) and Global X Physical Gold (ASX: GOLD) ETFs have appeared in recent ChartWatch ASX Scans Uptrends lists.)

Economy

Today

There weren't any major data releases in our time zone today

Later this week

Thursday

12:30 USA Core CPI November (+0.3% m/m forecast vs +0.3% m/m previous)

11:30 AUD Employment Change & Unemployment Rate November

Change: +26,000 forecast vs +15,900 in October

U-Rate: 4.2% forecast vs 4.1% in October

Friday

00:15 EUR ECB interest rate decision (3.15% forecast vs 3.40% previous)

00:30 USA Core PPI (+0.3% m/m forecast vs +0.2% m/m previous)

Latest News

Interesting Movers

Trading higher

+10.9% Ora Banda Mining (OBM) - No news, several gold stocks received a boost today from a firming in the gold price (see ChartWatch section above for gold technical analysis).

+10.9% WA1 Resources (WA1) - No news since 9-Nov West Arunta Project - Luni Metallurgical Results, but it was retained at buy at Canaccord Genuity with a price target of $28.00, bounced out of the long term trend ribbon.

+9.0% Southern Cross Electrical Engineering (SXE) - Project awards circa $125m.

+8.6% Silex Systems (SLX) - GLE selected by US DOE as an awardee for LEU Program, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈.

+8.3% The Star Entertainment Group (SGR) - No news, bounce within severe long term downtrend.

+8.2% Syrah Resources (SYR) - No news, interesting chart, back to rising peaks and rising troughs, but the long term downtrend ribbon remains the key overhead supply zone that must be dealt with to turn the long term downtrend around.

+5.4% Silver Mines (SVL) - No news, small bounce after getting belted on the back of yesterday's Placement to Raise $25 Million.

+5.3% Eagers Automotive (APE) - No news, likely getting some love after yesterday's dovish RBA meeting and rising expectations in markets that cuts are going to come sooner and be deeper than previously expected, closed back above long term trend ribbon.

+4.4% Immutep (IMM) - Continued positive response to yesterday's Initiation of TACTI-004 phase 3 trial in 1st line NSCLC, rise is consistent with prevailing short term uptrend, closed above long term downtrend ribbon.

+4.1% Integral Diagnostics (IDX) - CAJ: Scheme becomes Effective.

+3.2% Weebit Nano (WBT) - Response to ASX Compliance Letter.

+2.7% Iperionx (IPX) - Results of Meeting, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈.

Trading lower

-13.6% Paradigm Biopharmaceuticals (PAR) - No news, consistent with recent extreme volatility, has struggled since 9-Dec Successful Completion of $16M Placement for Phase 3…yet another share price pop = immediate capital raise! 🤦

-5.9% Imdex (IMD) - No news, closed below short term uptrend ribbon.

-5.8% Clarity Pharmaceuticals (CU6) - No news, fall is consistent with prevailing short term downtrend, long term trend is transitioning from up to down. I note it made its first appearance in ChartWatch ASX Scans Downtrends list based on 9-Dec candle - watch out for it to be a Feature in tomorrow's edition! 🔎📉

-4.6% IPH (IPH) - No news, unless you call a wall of excess supply news…fall is consistent with prevailing short and long term downtrends, one of the most Featured stocks in ChartWatch ASX Scans Downtrends list in 2024 🔎📉.

-4.3% South32 (S32) - No news, but there were a couple of broker notes today regarding the 10-Dec Mozal Aluminium Update (see Broker Moves section below for details).

-4.1% Mesoblast (MSB) - No news, consistent with recent volatility.

-4.1% Cettire (CTT) - No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉.

-4.0% Superloop (SLC) - No news, ASX tech stocks have been doing it tough last couple of sessions on sector rotations.

-3.2% Nanosonics (NAN) - No news, fall is consistent with prevailing short and long term downtrends, a recent addition to ChartWatch ASX Scans Downtrends list 🔎📉.

Broker Notes

Boab Metals (BML)

Retained at buy at Shaw and Partners; Price Target: $0.40

Domino's Pizza Enterprises (DMP)

Downgraded to neutral from buy at Citi; Price Target: $33.25 from $37.50

Develop Global (DVP)

Retained at buy at Bell Potter; Price Target: $3.50

Endeavour Group (EDV)

Retained at neutral at Jarden; Price Target: $5.00

Retained at buy at Jefferies; Price Target: $5.70

Retained at hold at Ord Minnett; Price Target: $4.20

Retained at buy at UBS; Price Target: $5.00

Firefly Metals (FFM)

Retained at buy at Argonaut Securities; Price Target: $1.90 from $1.95

Retained at buy at Euroz Hartleys; Price Target: $1.94

Retained at buy at Shaw and Partners; Price Target: $1.90

Generation Development Group (GDG)

Initiated at overweight at Morgan Stanley; Price Target: $4.75

Goodman Group (GMG)

Retained at accumulate at Ord Minnett; Price Target: $41.00 from $35.00

GQG Partners (GQG)

Retained at neutral at UBS; Price Target: $2.32 from $2.30

Imdex (IMD)

Retained at sell at Citi; Price Target: $1.95

Incitec Pivot (IPL)

Retained at neutral at Macquarie; Price Target: $3.15

Moneyme (MME)

Retained at buy at Morgans; Price Target: $0.21 from $0.22

Orica (ORI)

Retained at outperform at Macquarie; Price Target: $20.78

Pilbara Minerals (PLS)

Upgraded to buy from hold at Bell Potter; Price Target: $2.95

Perpetual (PPT)

Retained at buy at Bell Potter; Price Target: $24.76

Retained at outperform at CLSA; Price Target: $23.50 from $23.91

Retained at overweight at Jarden; Price Target: $24.40 from $22.70

Retained at overweight at JP Morgan; Price Target: $23.00 from $23.50

Retained at equal-weight at Morgan Stanley; Price Target: $20.60

Retained at buy at UBS; Price Target: $23.60

Pexa Group (PXA)

Retained at outperform at Macquarie; Price Target: $14.64 from $16.90

Region Group (RGN)

Retained at buy at Citi; Price Target: $2.60

South32 (S32)

Retained at equal-weight at Macquarie; Price Target: $3.30

Retained at equal-weight at Morgan Stanley; Price Target: $3.30

Silex Systems (SLX)

Retained at buy at Canaccord Genuity; Price Target: $6.21

Santana Minerals (SMI)

Retained at buy at Shaw and Partners; Price Target: $1.14

Smart Parking (SPZ)

Retained at buy at Shaw and Partners; Price Target: $1.10

Strickland Metals (STK)

Retained at buy at Canaccord Genuity; Price Target: $0.16

Transurban Group (TCL)

Retained at neutral at Macquarie; Price Target: $13.00 from $12.67

Retained at buy at UBS; Price Target: $14.75 from $14.55

VHM (VHM)

Retained at buy at Canaccord Genuity; Price Target: $1.15

WA1 Resources (WA1)

Retained at buy at Canaccord Genuity; Price Target: $28.00

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| NXD | Nexted Group Ltd | $0.17 | +47.83% |

| APC | Australian Potash Ltd | $0.024 | +33.33% |

| EMH | European Metals Holdings Ltd | $0.17 | +30.77% |

| HE8 | Helios Energy Ltd | $0.013 | +30.00% |

| HOR | Horseshoe Metals Ltd | $0.013 | +30.00% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| INF | Infinity Lithium Corporation Ltd | $0.023 | -30.30% |

| EE1 | EARTHS Energy Ltd | $0.011 | -21.43% |

| OLH | Oldfields Holdings Ltd | $0.06 | -20.00% |

| 8VI | 8VI Holdings Ltd | $0.042 | -19.23% |

| GIB | Gibb River Diamonds Ltd | $0.034 | -19.05% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| MTM | MTM Critical Metals Ltd | $0.19 | +8.57% |

| POL | Polymetals Resources Ltd | $0.99 | +6.45% |

| SDI | SDI Ltd | $1.22 | +6.09% |

| SHO | Sportshero Ltd | $0.021 | +5.00% |

| WHI | Whitefield Income Ltd | $1.30 | +4.00% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| INF | Infinity Lithium Corporation Ltd | $0.023 | -30.30% |

| EE1 | EARTHS Energy Ltd | $0.011 | -21.43% |

| ACR | ACRUX Ltd | $0.033 | -17.50% |

| KEY | KEY Petroleum Ltd | $0.05 | -16.67% |

| LYN | Lycaon Resources Ltd | $0.091 | -13.33% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| PCI | Perpetual Credit Income Trust | $1.16 | +0.43% |

| WVOL | Ishares MSCI World Ex Aust Minimum Volatility ETF | $42.74 | -0.16% |

| GCI | Gryphon Capital Income Trust | $2.05 | 0.00% |

| VVLU | Vanguard Global Value Equity Active ETF | $76.03 | -0.28% |

| IHD | Ishares S&P/ASX DIV Opportunities Esg Screened ETF | $14.68 | -0.34% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| INA | Ingenia Communities Group | $4.62 | -1.49% |

| IRE | Iress Ltd | $8.88 | 0.00% |

| BOE | Boss Energy Ltd | $2.52 | -1.18% |

| RTH | Ras Technology Holdings Ltd | $0.89 | +4.71% |

| AD8 | Audinate Group Ltd | $7.58 | -2.19% |