News | Market Wraps

Evening Wrap: ASX 200 cheers RBA rate cut as interest rate sensitives power ahead, resources and energy stocks lag

The S&P/ASX 200 closed 48.2 points higher, up 0.58%.

Mentioned

The S&P/ASX 200 closed 48.2 points higher, up 0.58%.

Aussie investors joined Aussie mortgage holders today in rejoicing the 0.25% cut in the Reserve Bank of Australia's (RBA) official cash rate. It was kind of lucky for investors that they did, because stocks were paring back early gains when the interest rate cut news broke.

Best today, naturally, the interest rate sensitives – i.e., those stocks that tend to prosper in a lower interest rate environment. So here, Real Estate, Information Technology, Financials, and Consumer Discretionary stocks did best.

Unfortunately, the bigger global picture, that of "uncertainty" – a word used by RBA Governor Michelle Bullock about 1000 times in her speech – weighed on Energy and Resources stocks. Gold stocks in particular came in for some harsh treatment.

To make sense of all the above, I have detailed technical analysis on the Nasdaq Composite, S&P/ASX 200, and GFEX Lithium Carbonate Futures in today's ChartWatch.

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key upcoming economic data in tonight's Evening Wrap.

Let's dive in!

Today in Review

Tue 20 May 25, 5:41pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,343.3 | +0.58% |

| All Ords | 8,573.4 | +0.57% |

| Small Ords | 3,158.4 | +0.27% |

| All Tech | 3,907.5 | +1.30% |

| Emerging Companies | 2,268.4 | -0.43% |

Currency | ||

| AUD/USD | 0.6401 | 0.00% |

US Futures | ||

| S&P 500 | 5,964.25 | -0.31% |

| Dow Jones | 42,814.0 | -0.17% |

| Nasdaq | 21,439.75 | -0.41% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Information Technology | 2,770.4 | +2.30% |

| Real Estate | 3,843.0 | +1.41% |

| Communication Services | 1,797.7 | +1.22% |

| Financials | 8,967.8 | +0.79% |

| Consumer Discretionary | 4,105.5 | +0.69% |

| Industrials | 8,308.9 | +0.53% |

| Health Care | 41,496.2 | +0.33% |

| Consumer Staples | 12,440.8 | +0.18% |

| Materials | 16,320.6 | -0.12% |

| Energy | 7,705.4 | -0.15% |

| Utilities | 9,341.8 | -0.55% |

Markets

%20intraday%20chart%2020%20May%202025.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 48.2 points higher at 8,343.3, 0.58% from its session low and just 0.23% from its high. In the broader-based S&P/ASX 300 (XKO) advancers beat decliners by a reassuring 181 to 98.

It looked like a typical "rate-sensitives rally" today. As discussed in yesterday's wrap, bond proxy sectors like Real Estate Investment Trusts (XPJ) (+1.4%) were hit Monday on the sharp rise nearly across the globe in long term risk-free yields.

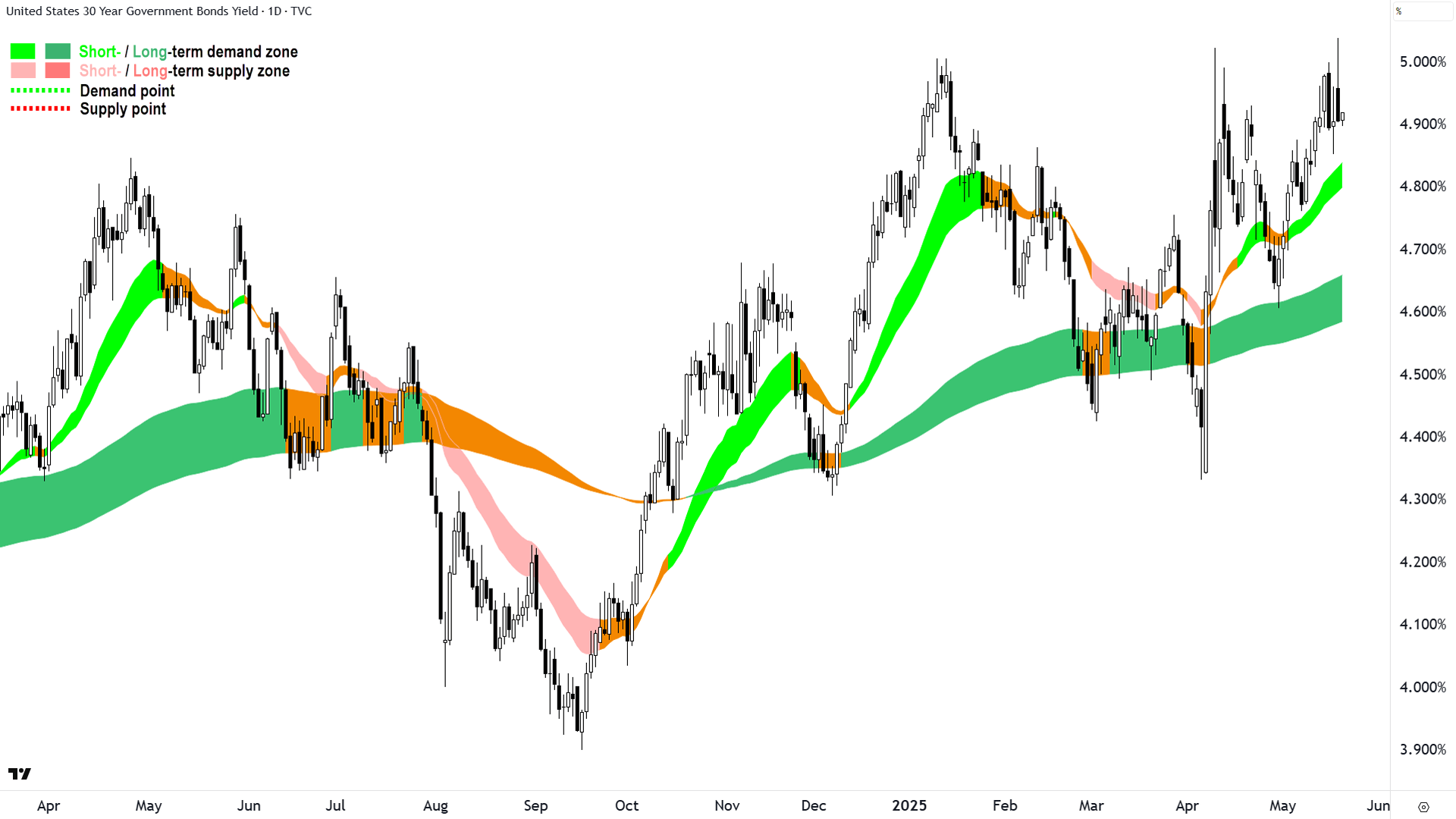

Fast forward to today, and those yields, dangerously high just 24-hours ago, have reversed. The yield on US 30's in particular stepped back from the Moody's downgrade ledge, falling 13.3 basis points from its high. That's over half of a typical Federal Reserve rate cut! (the last candle in the chart below is live, so discount it!).

US 30 Year T-Bond Yield chart daily chart (click here for full size image)

{kind=link}

Long duration Information Technology (XIJ) (+2.3%), today's best performing sector, is another interest rate sensitive, as are Financials (XFJ) (+0.79%) and Consumer Discretionary (XDJ) (+0.68%).

Communication Services (XTJ) (+1.2%) is an interesting sector. It contains a bunch of long-duration tech like stocks (REA Group (REA) (-0.4%) and CAR Group (CAR) (+1.1%)), but is dominated by bond proxy and Defence with a Capital 'D' – Telstra (TLS) (+2.2%). Telstra's performance today says it all.

Investors will be cheering gains on roughly 2 out of every 3 stocks in their portfolios today, but it's the 1 out of 3 left behind that's disturbing. Both global growth proxies Energy (XEJ) (-0.15%) and Resources (XJR) (-0.16%) missed the rally today. Funds are again playing their favourites (like they very much did before the correction where it was possible for the ASX 200 to make new highs and the XEJ and XJR regular multi-year and 12-month lows respectively).

Within Resources, the Gold Sub-Index (XGD) (-1.0%) continued it's wild ride since the gold price started wobbling on 22 April. The gold price was up last night, but given those long term risk-free yields backed off, and the world didn't come to an end...it's down modestly in Asian trade today.

ChartWatch

NASDAQ Composite Index

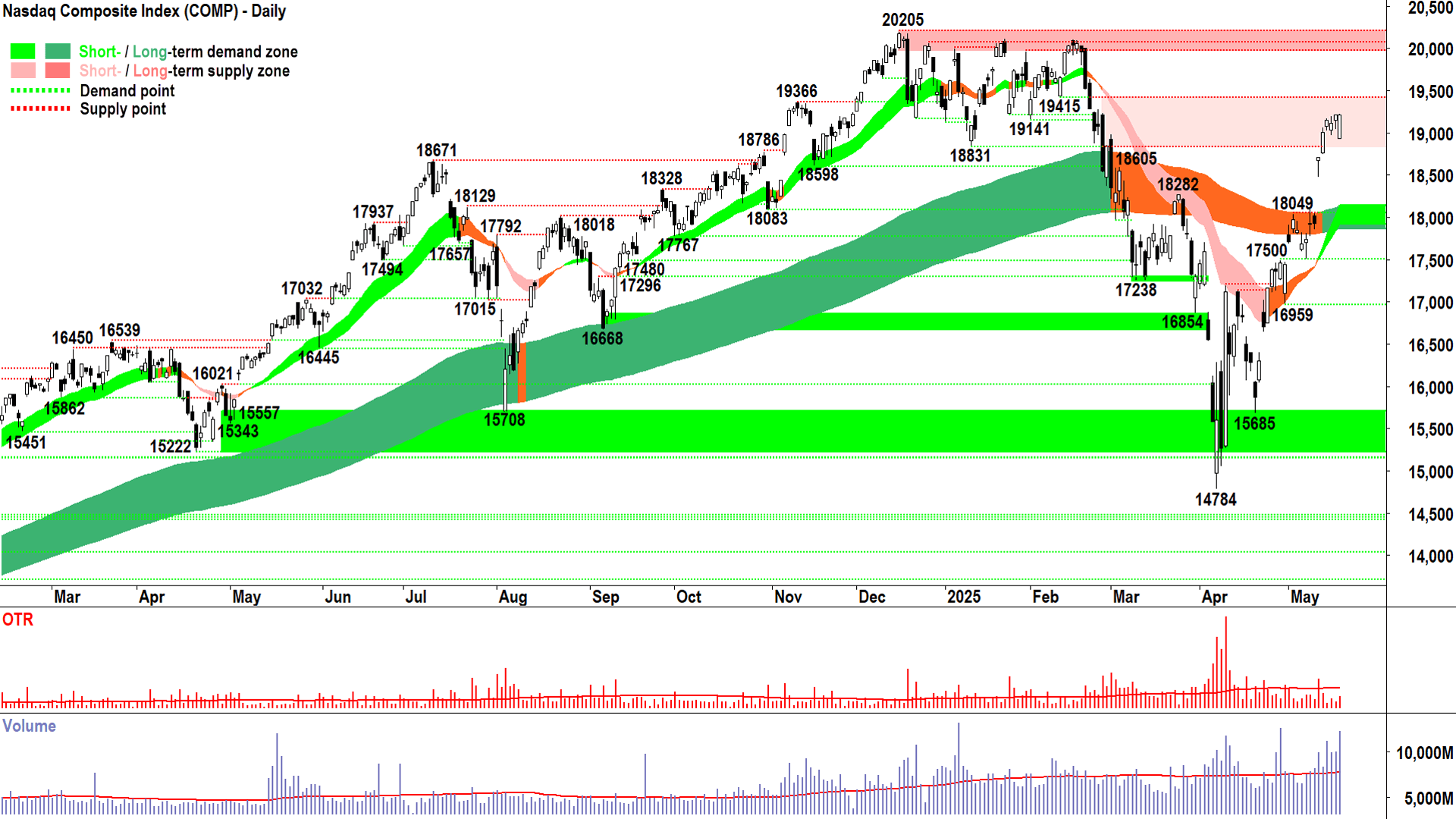

Put your hand down! 👇 (click here for full size image)

{kind=link}

Put your hands up if you were at all surprised by last night's Comp candle? 🖐️

No. I didn’t think so.

Moody’s downgrade…Open 270-odd points down at 18937.4.

What was the session low? 🤔

18937.4.

I put to you there was substantial selling to create that lower open, and indeed throughout the day – look at that massive volume…

Yet, the Comp couldn’t back-step even 0.1 of a point on a near-20,000 index.

What does this tell you about the latent demand in the system!? 🤯

This rally is real. It’s credible. And perhaps last night’s emphatic signal to the demand-supply environment clears the path to 20205 and a new all-time high – as in, why would the supply-side want to get in the way of this?

20205 or not, anything higher from here is quite an achievement considering where we were just 29 candles ago at 14784.

Nothing in my analysis needs to change, nor will it until we see anything that even resembles supply-side control. Enough said.

S&P/ASX 200 (XJO)

%20chart%2020%20May%202025.png)

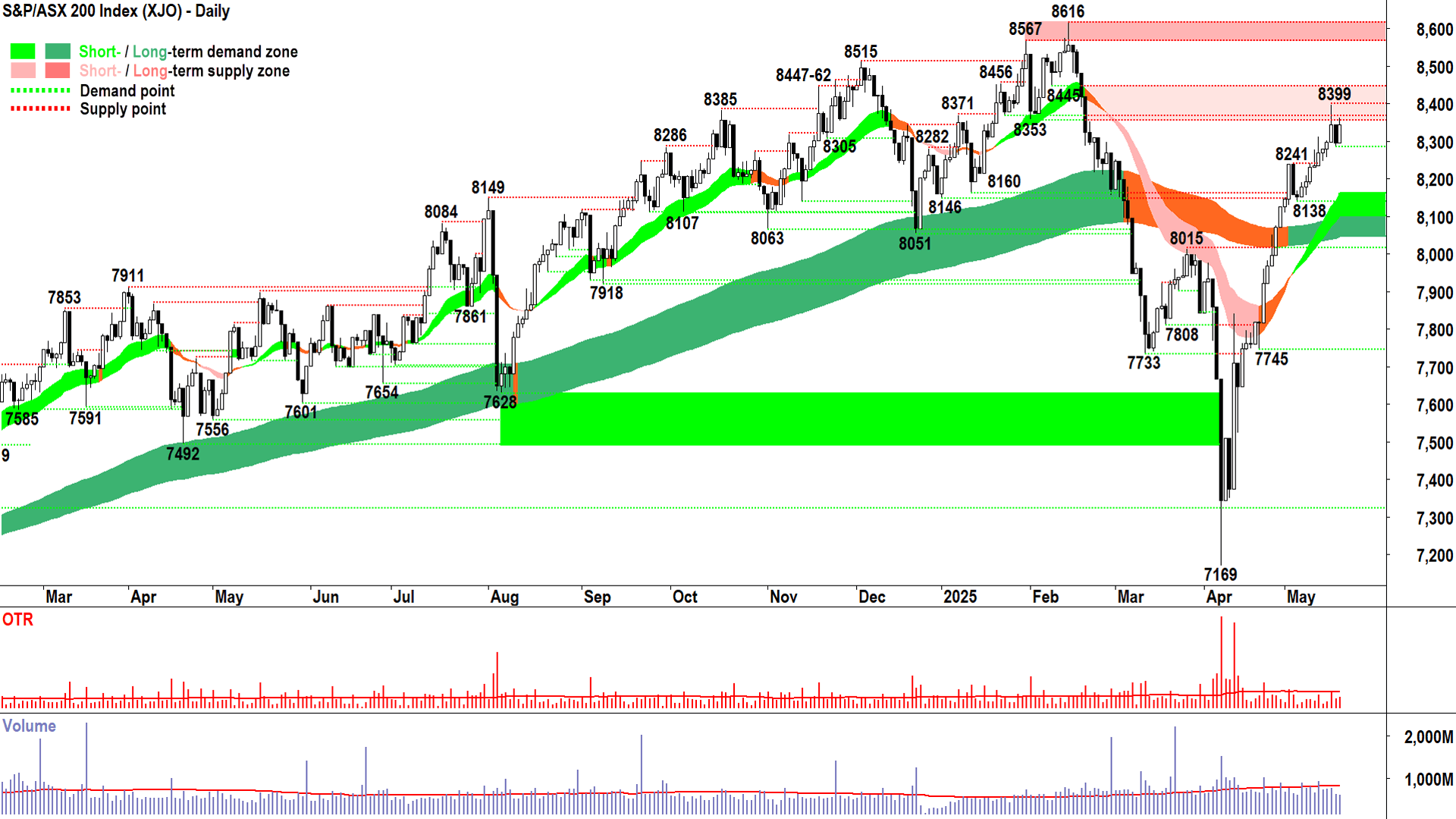

An interesting chart (click here for full size image)

{kind=link}

"Decent, though still a smidge of lingering doubt".

Would you agree that this is an appropriate description of today’s candle? 🤔

The “smidge” refers to that modest upward pointing shadow, tipping once again into that increasingly pesky 8353-8445 supply zone.

But looking up to the intraday chart, the shadow would have been substantially larger if now for the rally that followed the RBA interest rate decision.

Technical analysis doesn’t care why the shadow was shortened – simply that it was. Simply, that there was sufficient excess demand in the system to close the price near the high of the session.

Today’s candle also sets yesterday's low of 8284 as a higher trough (I didn’t label it to save on clutter), so the price action remains in good shape.

Add to that a couple more checks: The trend ribbons are double green and continue to rise ✅, and candles remain predominantly demand-side in nature ✅.

In conclusion, there’s little need to do much here either, save again for monitoring the price action around 8399 / the 8353-8445 supply zone.

Like the Comp, I suspect that we’re also just one emphatic demand-side showing away from locking in a path to a new high.

I say this because the technicals here continue to indicate some lingering supply-side doubt, showing up as upward pointing shadows or black bodies on days the demand-side is less motivated. The supply side must be suitably convinced that higher prices are a lock, that they’re better off holding back their supply.

Once this occurs, trends, price action, and candles suggest there’s plenty of latent demand in the system to knock 8616 🤞.

GFEX Lithium Carbonate Futures (benchmark month, back-adjusted)

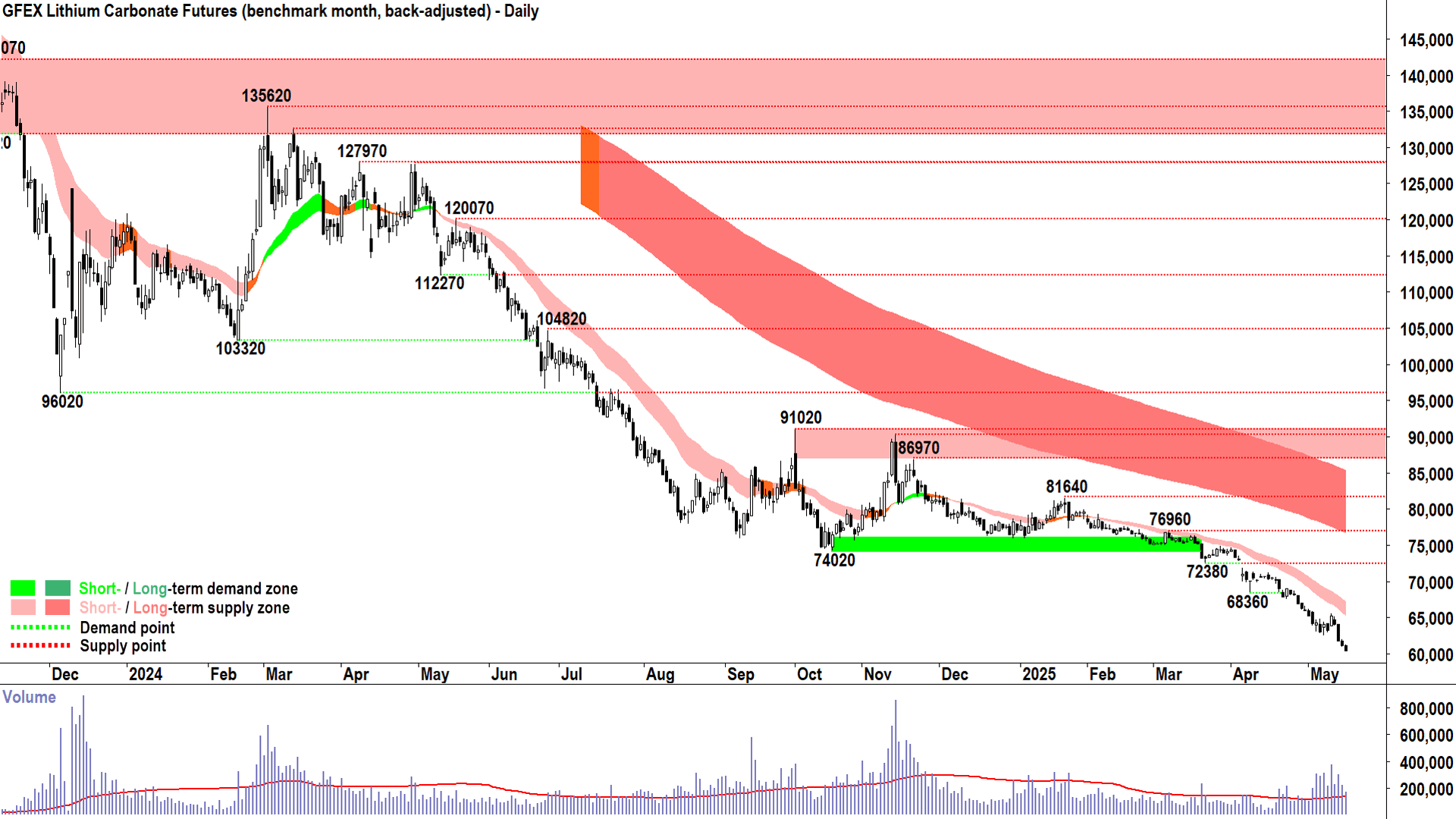

This is what pure consensus looks like 📉 (click here for full size image)

{kind=link}

I wanted to put this one in tonight to compare and contrast against a demand-side dominated market like the Comp (and to a lesser extent, our market!).

Consensus is the holy grail of trend following.

It occurs when the demand-side thinks X is great/terrible value so they just want to own/not own it, and simultaneously the supply-side thinks X is great/terrible value so they they just want to own/not own it.

It's that simple, and when you think about it...It frames the value of our opinion in this whole price discovery process: Zero, zip, nada, nothing.

Consensus among the demand-and-supply-sides yields the largest and lowest volatility trends. Large and low volatility trends equals high probability and high profitability trades.

Consensus just makes our lives easier.

Consensus comes in different shapes and forms, for example, those last 6 candles on the Comp - pure consensus that owning Comp stocks is better than not owning them.

GFEX lithium carbonate is another picture of pure consensus – only this time with the price heading the other way 📉.

Economy

Today

Reserve Bank of Australian Official Cash Rate (OCR), Monetary Policy Statement, Press Conference

OCR: -0.25% to 3.85% p.a. as forecast vs 4.10% previous

RBA: "The Board judged that the risks to inflation have become more balanced. Inflation is in the target band and upside risks appear to have diminished as international developments are expected to weigh on the economy. With inflation expected to remain around target, the Board therefore judged that an easing in monetary policy at this meeting was appropriate. "

Governor Bullock: "There was a bit of a discussion about hold, and that was put aside pretty quickly. The discussion then was about a cut and then how big. There was a discussion about 50 or 25. The Board was of the view that 25 was right for this occasion. With inflation in the band and employment doing well, we think there is a bit of scope to lower interest rates, and when you add the international uncertainty, then yes. On balance the Board was of the view that 25 basis points was the right thing for now. It doesn't rule out that we may might need to take action in the future, but for now that was the right number."

Later this week

Wednesday

10:30 AUS MI Leading Index m/m

Thursday

09:00 AUS Flash Manufacturing Purchasing Managers Index (PMI) May:

Manufacturing: 51.7 in April

Services: 51.0 in April

18:00 EUR Flash Manufacturing PMI:

Manufacturing: 49.3 forecast and 49.0 in April

Services: 50.6 forecast and 50.1 in April

23:45 USA Flash Manufacturing PMI:

Manufacturing: 49.9 forecast and 50.2 in April

Services: 50.7 forecast and 50.8 in April

Friday

00:00 Existing Home Sales April (4.15 million forecast vs 4.02 million in March)

Saturday

00:00 New Home Sales April (696,000 forecast vs 724,000 in March)

Latest News

Interesting Movers

Trading higher

+40.5% Dateline Resources (DTR) – No news since 19-May Dateline Fully Funded for Colosseum Gold Feasibility Study, rise is consistent with prevailing short term uptrend and long term trend is transitioning from down to up, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

+25.0% Kingston Resources (KSN) – Investor Presentation-Misima Divestment & Corporate Outlook and Misima Gold Project Sold to Ok Tedi for $95 Million.

+17.4% MTM Critical Metals (MTM) – Clarification of Exec Rem - Expiry Date of Perf Rights, rise is consistent with prevailing short and long term uptrends, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

+11.3% Technology One (TNE) – TNE Half Year FY25 Results and SaaS Plus - Delivers Upgrades FY Profit Growth to 13%-17%, rise is consistent with prevailing short and long term uptrends, one of the most Featured (highest conviction) stocks in ChartWatch ASX Scans Uptrends list 🔎📈

+7.9% Australian Finance Group (AFG) – No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+6.8% Electro Optic Systems (EOS) – 2025 AGM - CEO Presentation.

+5.7% Iperionx (IPX) – No news 🤔

+5.5% Aspen Group (APZ) – No news since 19-May Sale of Eureka Group Shares, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.5% Antipa Minerals (AZY) – No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+4.4% Liontown Resources (LTR) – No news, today’s move is consistent with recent volatility.

+4.2% Perenti (PRN) – No news since 19-May Barminco signs A$500m Agnew contract, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+4.1% South32 (S32) – No news 🤔

+3.9% Domino’s Pizza Enterprises (DMP) – No news since 19-May Announcement regarding ANZ CEO.

+3.9% Generation Development Group (GDG) – No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+3.7% Audinate Group (AD8) – No news, initiated at outperform at CLSA with a price target of $10.85.

Trading lower

-34.6% OFX Group (OFX) – FY25 Results, repelled perfectly from long term downtrend ribbon! 🔎📉

-12.4% Monash IVF Group (MVF) – FY25 Profit Guidance Update, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-11.9% Koonenberry Gold (KNB) – Enmore 4th drill hole returns 149.5m @ 0.94g/t gold, general weakness across the broader Gold sector today.

-11.8% Coronado Global Resources (CRN) – No news, fall is consistent with prevailing short and long term downtrends, the most Featured (highest conviction) stock in ChartWatch ASX Scans Downtrends list 🔎📉

-8.9% Kogan.Com (KGN) – Kogan.com May 2025 Business Update, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-8.5% Nanosonics (NAN) – No news 🤔

-7.3% Infomedia (IFM) – No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.7% Regal Partners (RPL) – No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.7% Brightstar Resources (BTR) – High-grade results incl 16m @ 8g/t Au in Menzies drilling, general weakness across the broader Gold sector today.

-5.3% Austin Engineering (ANG) – No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.0% Catalyst Metals (CYL) – No news since 19-May Completion of the Henty disposal, general weakness across the broader Gold sector today.

-4.5% Energy One (EOL) – No news, pulled back in the wake of recent sharp rally.

-4.4% Resmed Inc (RMD) – No news, US-based company released positive results for its sleep apnoea treatment seen as a threat to RMD's products.

-4.2% Polynovo (PNV) – No news, repelled perfectly from long term downtrend ribbon! 🔎📉

-3.4% Bellevue Gold (BGL) – No news, general weakness across the broader Gold sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

Broker Moves

Audinate Group (AD8)

Initiated at outperform at CLSA; Price Target: $10.85

Atlas Arteria (ALX)

Retained at buy at Citi; Price Target: $5.70

BHP Group (BHP)

Retained at neutral at UBS; Price Target: $40.00

Breville Group (BRG)

Retained at overweight at Morgan Stanley; Price Target: $36.50 from $40.00

Credit Corp Group (CCP)

Retained at neutral at Macquarie; Price Target: $16.27

DigiCo REIT (DGT)

Retained at buy at UBS; Price Target: $5.60

Fisher & Paykel Healthcare Corporation (FPH)

Downgraded to neutral from buy at UBS; Price Target: NZ$39.00 from NZ$37.30

Goodman Group (GMG)

Retained at buy at Citi; Price Target: $40.00

Retained at buy at UBS; Price Target: $36.00

Gentrack Group (GTK)

Retained at buy at Bell Potter; Price Target: $13.20 from $13.50

Retained at overweight at Morgan Stanley; Price Target: $13.50

Retained at buy at Shaw and Partners; Price Target: $11.80

Upgraded to neutral from sell at UBS; Price Target: NZ$12.00 from NZ$11.75

Infratil (IFT)

Retained at buy at UBS; Price Target: NZ$14.00

James Hardie Industries (JHX)

Retained at buy at UBS; Price Target: $50.00 from $60.00

Kogan.Com (KGN)

Retained at outperform at RBC Capital Markets; Price Target: $6.50

Lendlease Group (LLC)

Retained at buy at Citi; Price Target: $7.50

Retained at neutral at JP Morgan; Price Target: $6.40 from $6.15

Retained at outperform at Macquarie; Price Target: $7.79 from $7.24

Retained at equal-weight at Morgan Stanley; Price Target: $7.12

Mineral Resources (MIN)

Retained at buy at UBS; Price Target: $26.10

New Hope Corporation (NHC)

Retained at neutral at Citi; Price Target: $3.85 from $4.20

Retained at sell at Goldman Sachs; Price Target: $3.00 from $2.90

Retained at neutral at Macquarie; Price Target: $4.00 from $4.25

Nextdc (NXT)

Retained at buy at UBS; Price Target: $19.80

Paragon Care (PGC)

Upgraded to buy from hold at Bell Potter; Price Target: $0.520

Ramsay Health Care (RHC)

Retained at neutral at Goldman Sachs; Price Target: $39.00 from $38.70

Regis Resources (RRL)

Retained at outperform at RBC Capital Markets; Price Target: $4.80

Transurban Group (TCL)

Retained at neutral at Macquarie; Price Target: $13.70 from $12.82

Trajan Group (TRJ)

Retained at buy at Bell Potter; Price Target: $1.500

Electro Optic Systems (EOS)

Retained at buy at Ord Minnett; Price Target: $1.800

Mystate (MYS)

Retained at buy at Ord Minnett; Price Target: $4.53

Core Lithium (CXO)

Retained at hold at Ord Minnett; Price Target: $0.110 from $0.100

Elementos (ELT)

Retained at speculative buy at Morgans; Price Target: $0.300

South32 (S32)

Retained at buy at Citi; Price Target: $3.70 from $4.00

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| ZNO | ZOONO Group Ltd | $0.065 | +66.67% |

| DTR | Dateline Resources Ltd | $0.052 | +40.54% |

| MM1 | Midas Minerals Ltd | $0.22 | +39.68% |

| LTP | LTR Pharma Ltd | $0.39 | +39.29% |

| LM1 | Leeuwin Metals Ltd | $0.165 | +26.92% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| DUB | Dubber Corporation Ltd | $0.021 | -44.74% |

| OFX | OFX Group Ltd | $0.86 | -34.60% |

| DTZ | DOTZ Nano Ltd | $0.062 | -28.74% |

| EPX | Ep&T Global Ltd | $0.021 | -25.00% |

| DAL | Dalaroo Metals Ltd | $0.023 | -23.33% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| ZNO | ZOONO Group Ltd | $0.065 | +66.67% |

| DTR | Dateline Resources Ltd | $0.052 | +40.54% |

| MM1 | Midas Minerals Ltd | $0.22 | +39.68% |

| KSN | Kingston Resources Ltd | $0.115 | +25.00% |

| MPK | Many Peaks Minerals Ltd | $0.60 | +21.21% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| OFX | OFX Group Ltd | $0.86 | -34.60% |

| GBE | Globe Metals & Mining Ltd | $0.024 | -17.24% |

| PLN | Pioneer Lithium Ltd | $0.10 | -13.04% |

| ENL | Enlitic Inc | $0.031 | -12.86% |

| CRN | Coronado Global Resources Inc | $0.15 | -11.77% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| PCI | Perpetual Credit Income Trust | $1.19 | 0.00% |

| WVOL | Ishares MSCI World Ex Aust Minimum Volatility ETF | $44.26 | +0.87% |

| IAGPF | Insurance Australia Group Ltd | $104.27 | +0.07% |

| GCI | Gryphon Capital Income Trust | $2.05 | 0.00% |

| IHD | Ishares S&P/ASX DIV Opportunities Esg Screened ETF | $14.74 | -0.87% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| AVH | Avita Medical Inc | $2.05 | +1.99% |

| NWSLV | News Corporation | $41.40 | 0.00% |

| AOF | Australian Unity Office Fund | $0.485 | 0.00% |

| SKC | Skycity Entertainment Group Ltd | $0.905 | -2.16% |

| LTP | LTR Pharma Ltd | $0.28 | -8.20% |