News | Market Wraps

Evening Wrap: ASX 200 bounces on surging commodity stocks, Mineral Resources leads lithium charge on big UBS upgrade

The S&P/ASX 200 closed 64.4 points higher, up 0.83%.

Mentioned

The S&P/ASX 200 closed 64.4 points higher, up 0.83%.

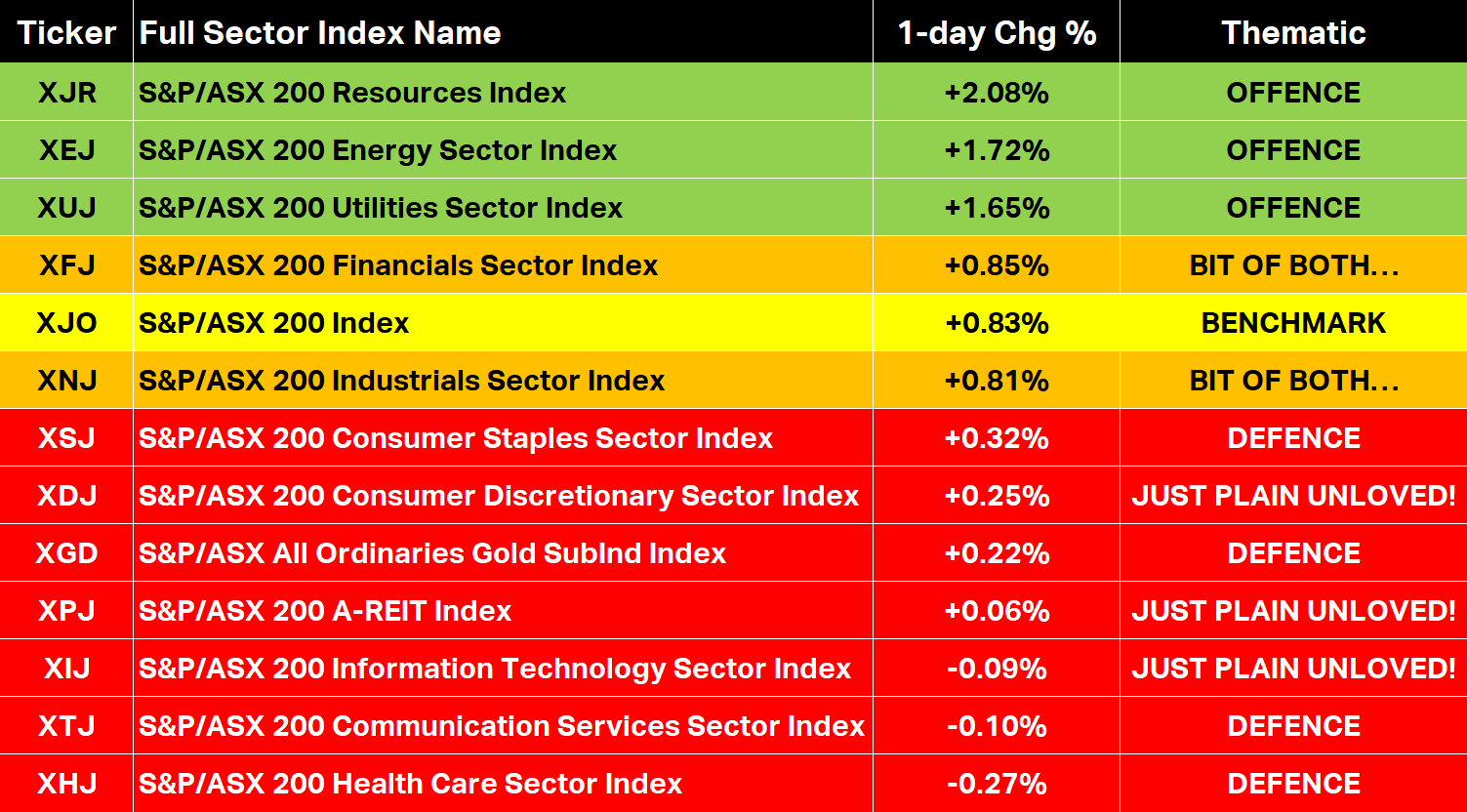

There was plenty of talk about Chinese stimulus drove the strong performance in commodity-related sectors like Resources (XJR), Energy (XEJ), and Utilities (XUJ), today – the three best to be fair...

But it was a double rating upgrade (from SELL straight to BUY) for Mineral Resources (MIN) from major broker UBS that was more likely responsible for a massive rally in beaten down lithium and battery metals stocks.

Elsewhere, the high-PE high flyers of the pre-correction bull market (remember those days!?) continued to struggle. Here, Information Technology (XIJ) and Consumer Discretionary (XDJ) missed out on today's ASX 200 rally completely.

Click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key upcoming economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on the NASDAQ Composite and S&P/ASX 200 in today's ChartWatch.

Let's dive in!

Today in Review

Mon 17 Mar 25, 6:03pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 7,854.1 | +0.83% |

| All Ords | 8,082.1 | +0.86% |

| Small Ords | 3,030.5 | +0.87% |

| All Tech | 3,468.5 | +0.54% |

| Emerging Companies | 2,224.4 | +1.29% |

Currency | ||

| AUD/USD | 0.633 | +0.08% |

US Futures | ||

| S&P 500 | 5,605.25 | -0.62% |

| Dow Jones | 41,297.0 | -0.51% |

| Nasdaq | 19,577.25 | -0.68% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Materials | 16,674.6 | +1.97% |

| Energy | 7,880.6 | +1.72% |

| Utilities | 9,076.9 | +1.65% |

| Financials | 8,091.6 | +0.85% |

| Industrials | 7,704.3 | +0.81% |

| Consumer Staples | 11,388.8 | +0.32% |

| Consumer Discretionary | 3,775.1 | +0.25% |

| Real Estate | 3,589.8 | +0.13% |

| Information Technology | 2,346.7 | -0.09% |

| Communication Services | 1,628.7 | -0.10% |

| Health Care | 40,804.9 | -0.27% |

Markets

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished points higher at 7,854.1, 0.79% from its session high and just 0.06% from its low. In the broader-based S&P/ASX 300 (XKO), advancers beat decliners by an emphatic 203 to 72.

Plenty of talk in other media outlets about Chinese stimulus and how it is the reason for the strong performance in commodity-related sectors like Resources (XJR) (+2.1%), Energy (XEJ) (+1.7%), and Utilities (XUJ) (+1.6%), today – the three best to be fair...

I've also heard about surging commodity prices today...

Well, a couple of points on this rhetoric (i.e., an easy excuse for journos in a rush and looking to get anything plausible up on site!).

The China stimulus announcement was fluff (as usual).

Yesterday, Beijing released a “special action plan” with all the usual language we'd expect...boost consumption, promises of income support for certain workers, a study to establish a childcare subsidy scheme, expand domestic demand...etc.

Actual specifics and or details on exactly how all of the above will be done: Zip. Nada. Nothing (also pretty typical!)

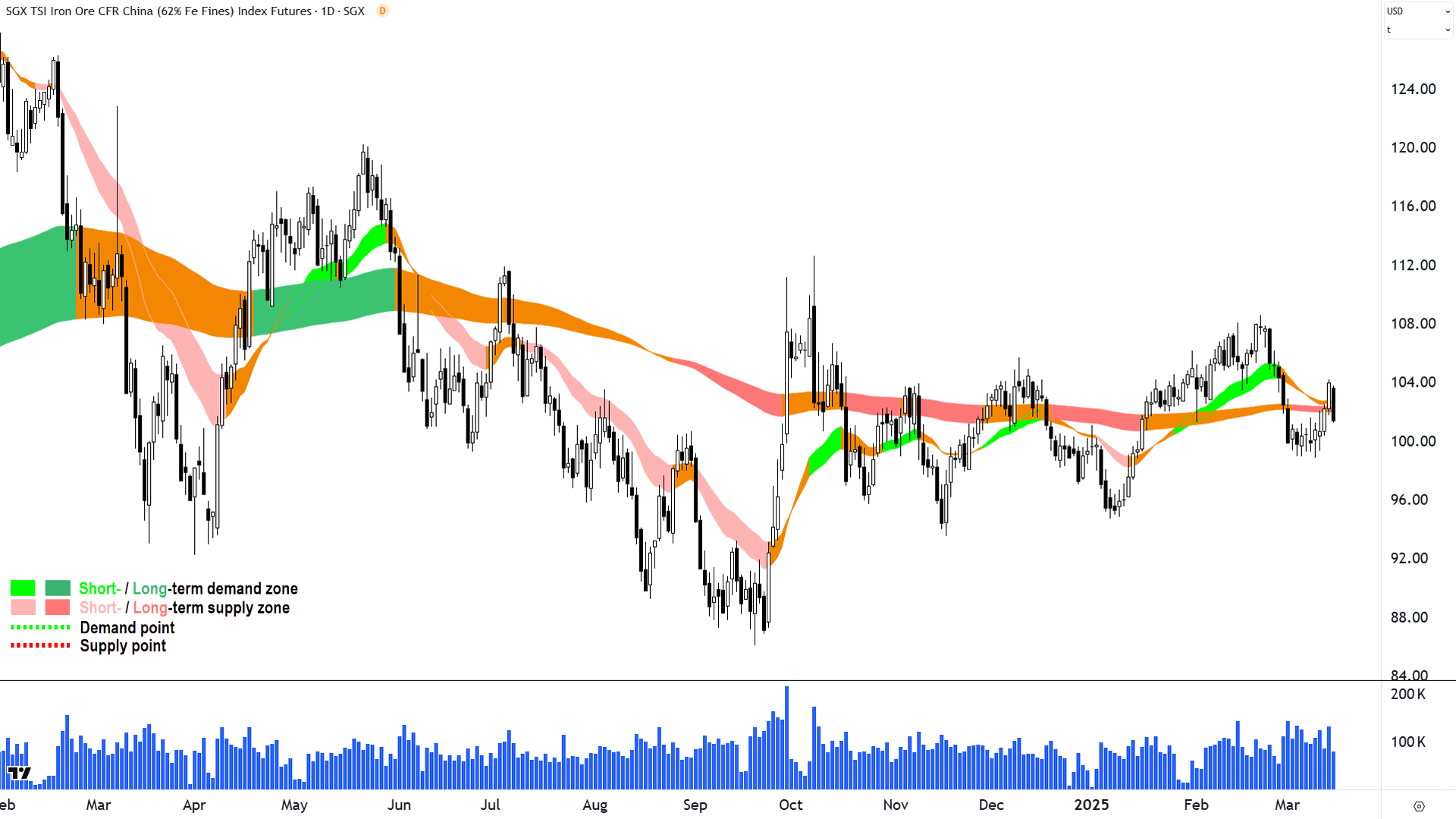

Commodities are up, but hardly spectacular...and iron ore is down sharply in Singapore...

%20ICE%20chart%2017%20March%202025.png)

Brent Crude Oil Futures (Front month, back-adjusted) ICE (click here for full size image)

{kind=link}

%20COMEX%20chart%2017%20March%202025.png)

High Grade Copper Futures (Front month, back-adjusted) COMEX (click here for full size image)

{kind=link}

%20SGX%20chart%2017%20March%202025.png)

Iron Ore 62% (Front month, back-adjusted) SGX (click here for full size image)

{kind=link}

I'm not saying the stimulus excuse had nothing to do with today's moves, just that it's more of a convenient coincidence. I suggest today was more about the usual fund rotations that shape the daily ebb-and-flow of trading on the ASX.

My observation is that there is a skew towards moving into low-PE and out of high-PE since the Valentine's Day peak. Resources and Energy are about as low-PE as you can get. They're also growth-oriented, which has worked against them in the correction. Still, due to their risk-on nature, let's call them OFFENCE.

Also, we've seen defensives like the Gold (XGD) sub-index (+0.22%) and Consumer Staples (XSJ) (+0.32%), and to a lesser extent Communication Services (XTJ) (-0.10%) (mainly Telstra), hold up better during the correction. Let's call these DEFENCE. It makes sense these sectors were collectively relatively weaker today as funds swung from DEFENCE back to a bit of OFFENCE.

High-PE like Consumer Discretionary (XDJ) (+0.25%) and Information Technology (XIJ) (-0.09%), have been shunned during the correction. Worryingly for those invested in these sectors, it's turning into a bit of shunned no matter what – benchmark up or benchmark down. Health Care (XHJ) (-0.27%), is also high-PE, and today I suspect also got doubly tagged as DEFENCE.

Financials (XFJ) (+0.85%) and Industrials (XNJ) (+0.85%) are a bit of both OFFENCE and DEFENCE, so today it makes sense they were roughly market-performs.

I think this idea of OFFENCE/Low-PE vs DEFENCE is a far more important theme than China stimulus in explaining how Aussie stocks traded today (well, they're all really just excuses...aren't they! 🤔)

17 March ASX Sector Indices Performance Table (click here for full size image)

{kind=link}

In stock-specific moves, and helping drive some of the flows back to low-PE resources, was UBS's upgrade of Mineral Resources (ASX: MIN) (+11.6%) to BUY from SELL. The broker did cut MIN's price target, though, to $28.60 from $33.00. It's unusual to see a broker shift through two gears from sell to buy without going through hold first.

In the research note, titled "Mineral Resources Darkest before dawn", UBS noted that whilst issues such as "high operational and financial leverage to its underlying commodities (iron ore and lithium) at a time when the outlook for both had deteriorated", "levering up to complete its Onslow Iron project", and the "emergence of governance issues" are all "concerns" that "haven't fully resolved yet" – the broker had "reassessed funding and operational scenarios with resultant EPS upgrades of 6%/45% in FY26/27E." This, along with the recent share price rout, meant they now "see enough upside to upgrade to a Buy rating".

ChartWatch

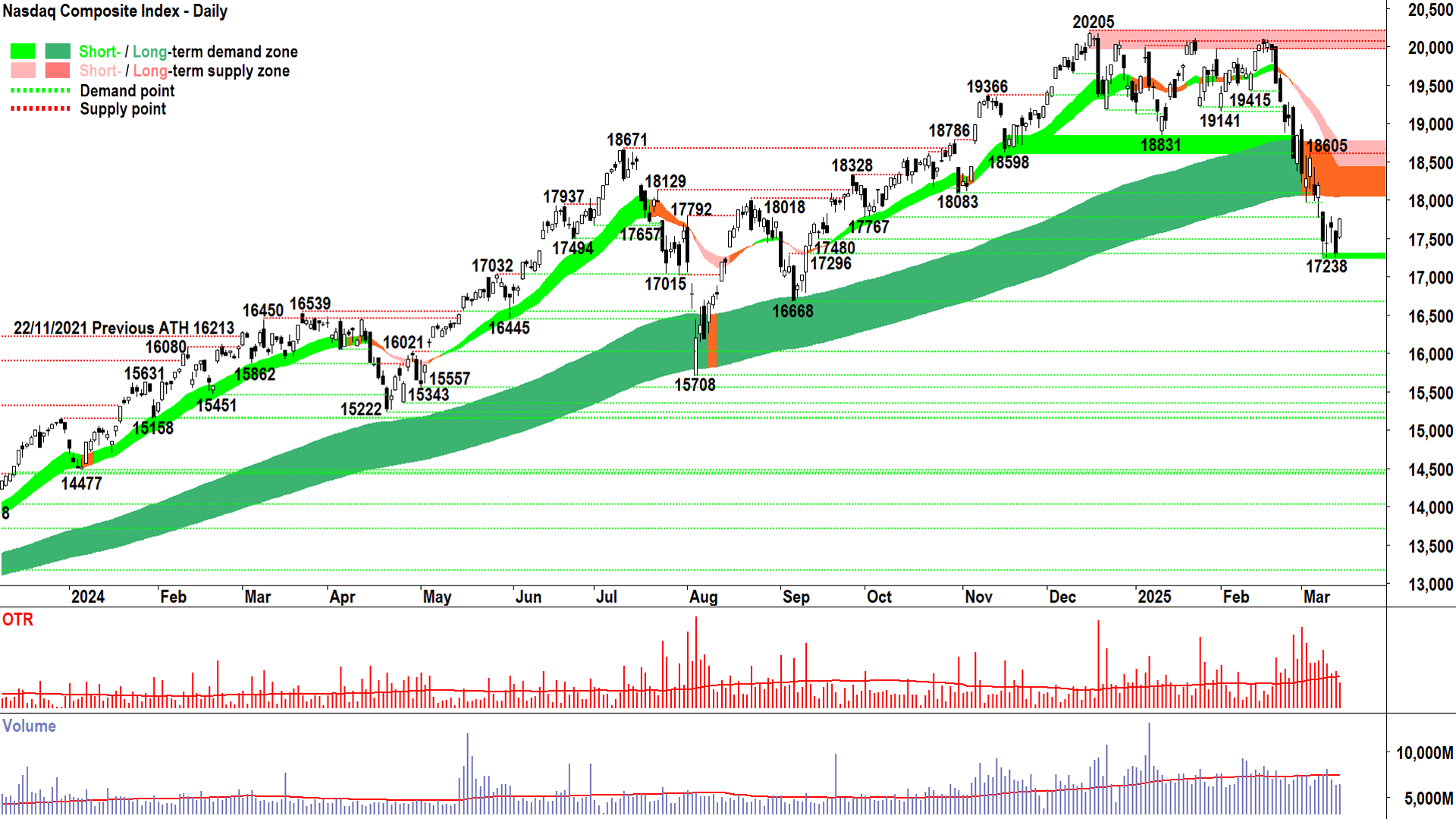

NASDAQ Composite Index

Front row seats to the unfolding spectacle! (click here for full size image)

{kind=link}

Another zebra day – as in – the full black supply candle on Thursday was followed by a 220-point opening up-gap and full white demand candle on Friday. ⬛🕯️⬜🕯️

It’s representative of the extreme uncertainty across the demand-supply environment – neither longs nor shorts are very committed to their positions. It’s go with the flow of daily sentiment sort of stuff.

Thursday’s sentiment was bearish, Friday’s was “relief rally” was bullish. Don't get in the way.

A couple of the same variety of candle in a row (i.e., either demand-side or supply-side) would be nice – and probably given the recent demand-supply environment confusion – quite telling.

So, if we can get another demand-side follow up tonight (i.e., white-bodied and or a long downward pointing shadow), I expect we’ve got a date with the wall of dynamic demand likely at the short/long term trend ribbons combination. It kicks in just north of 18k.

The candles in that dynamic supply zone will be even more telling, and so too will be the price action. If we can breeze through it, and make it to the other side with some nice candles – it’s back to bull market kind of stuff.

Alternatively, if we log a peak in there, or worse, a peak-then-lower-peak…along with a good sprinkling of supply-side candles (i.e., black-bodied and or long upward pointing shadows), then it will be lights out for the bull market kind of stuff.

It’s decision time for investors: Bull or bear for the next 6 months and beyond? We have front row seats to the unfolding spectacle!

(17238 is now confirmed as an important point of demand…We do NOT want to see a close below there…📉)

S&P/ASX 200 (XJO)

%20chart%2017%20March%202025.png)

V-shaped or NOT V-shaped? (click here for full size image)

{kind=link}

A bit of ditto here, no surprise there – we’re following overseas leads not dictating them.

If we are a leader, it has been only in terms of how sharp our sell off has been (they sneezed, and we caught the cold 😷!!!).

A credible demand-side showing today, and unlike the Comp – two in a row! Woo-hoo for us!!! 💪

As we’ve discussed here before, when it comes to rallies, only V-shaped ones stand any chance of meaningfully succeeding.

Quick, large, emphatic demand-side showings. Preferably into a volume and volatility climax.

Those are the ones that are supported by:

Sell side capitulation (the supply overhang is largely now already in the market, creating a relative supply vacuum)

Demand-side accumulation, speculative buying (buy the dippers both small/speculative and massive/positional)

Short covering – yes shorts locking in their winnings means buying, means they’re part of the demand-side…why are they locking in their winnings? Because they don’t think there’s much downside in the price!

It’s easy to see how when you get the above 3 factors working together that you’ll end up with a V-shaped rally.

The alternative is a NOT V-shaped rally. Something less steep, less emphatic, or only a bump along the bottom, or no rally at all – don’t pass Go – just straight down.

As with the Comp, the short/long term trend ribbon combo will be the target of any rally – V-shaped or otherwise from here. That zone kicks in around 8070. You know the drill from here…watch the candles and price action for signs of who’s in control 🧐.

(7733 is the critical point of demand here...We do NOT want to see a close below there…📉)

Economy

Today

China Data Dump Jan-Feb (mixed bag, property doldrums remain elephant in the room...)

New Home Prices m/m: -0.14% actual vs -0.07% previous (value fell 9.8% y/y worse the -8.5% forecast)

Industrial Production y/y: +5.9% actual vs +5.3% forecast vs +6.2% previous (strongest: manufacturing of railways/ships, machineries, computers and metal products)

Retail Sales y/y: +4.0% actual vs +3.8% forecast vs +3.7% previous (solid beat, in line with recent trends)

Fixed Asset Investment ytd/y: +4.1% actual vs +3.2% forecast vs +3.2% previous (again, railways and computers strongly support, also autos)

Unemployment Rate: +5.4% actual vs +5.1% forecast vs +5.1% previous (highest level in 12 months)

Later this week

Monday

20:30 USA Core Retail Sales February (+0.3% m/m forecast vs -0.4% m/m in January)

Tuesday

20:30 USA Housing Data February

Building Permits: 1.45 million forecast vs 1.47 million in January

Housing Starts: 1.38 million forecast vs 1.37 million in January

Wednesday

Tentative JPN BOJ Policy Rate, Monetary Policy Statement, Press Conference (no change <0.50% forecast)

Thursday

02:00 USA Federal Reserve Funds Rate, FOMC Statement of Economic Projections

No change at 4.25%-4.50% forecast

02:00 USA Federal Reserve Press Conference

08:30 AUS Employment Change February (+31,400 forecast vs +44,000 in January)

Unemployment Rate: 4.1% forecast, unchanged from January

22:00 USA Existing Home Sales February (3.94 million forecast vs 4.08 million in January)

Friday

No major economic data releases are scheduled for this day

Latest News

Interesting Movers

Trading higher

+40.0% Donaco International (DNA) - DNA enters Scheme Implementation Deed.

+11.6% Mineral Resources (MIN) - Becoming a substantial holder, upgraded to buy from sell at UBS (but price target cut to $28.60 from $33.00), unusual to see a broker shift through two gears from sell to buy without going through hold first.

+10.7% Astral Resources (AAR) - Takeover Update - Offer Declared Best and Final.

+10.5% Orthocell (OCC) - No news, rise is consistent with prevailing long term uptrend 🔎📈

+9.1% Spartan Resources (SPR) - Investor Presentation - Combination of Ramelius & Spartan, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+8.9% Silver Mines (SVL) - No news, likely responding to recent strong performance of the silver price.

+7.7% Vulcan Energy Resources (VUL) - No news, general strength across the broader Resources sector today.

+7.3% IGO (IGO) - No news, general strength across the broader Resources sector today, (also very likely some rub off from the MIN performance today - lithium is a heavily shorted area of the market).

+7.1% Pilbara Minerals (PLS) - No news, general strength across the broader Resources sector today, (also very likely some rub off from the MIN performance today - lithium is a heavily shorted area of the market).

+6.5% Chalice Mining (CHN) - No news, likely short covering in broader battery metals stocks post-MIN move.

+6.2% Liontown Resources (LTR) - No news since , general strength across the broader Resources sector today, (also very likely some rub off from the MIN performance today - lithium is a heavily shorted area of the market).

Trading lower

-5.5% Droneshield (DRO) - No news, pulled back in the wake of recent sharp rally.

-5.5% Novonix (NVX) - No news since 14-Mar Change of Director's Interest Notice, (on market disposal of 894,681 shares valued at $221,780), fall is consistent with prevailing short and long term downtrends, one of the most Featured (highest conviction) stocks in ChartWatch ASX Scans Downtrends list 🔎📉

-3.7% Adriatic Metals (ADT) - Results of General Meeting.

-3.6% Appen (APX) - No news, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down, a recent regular in ChartWatch ASX Scans Downtrends list 🔎📉

-3.6% Spark New Zealand (SPK) - No news, fall is consistent with prevailing short and long term downtrends, one of the most Featured (highest conviction) stocks in ChartWatch ASX Scans Downtrends list 🔎📉

-3.4% Clarity Pharmaceuticals (CU6) - No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

Broker Moves

Aussie Broadband (ABB)

Retained at buy at Citi; Price Target: $4.80 from $4.60

Retained at buy at Ord Minnett; Price Target: $4.49

Audinate Group (AD8)

Retained at underperform at Macquarie; Price Target: $6.30

Auckland International Airport (AIA)

Retained at neutral at UBS; Price Target: NZ$8.20

Ampol (ALD)

Retained at outperform at Macquarie; Price Target: $29.45

Aristocrat Leisure (ALL)

Retained at outperform at Macquarie; Price Target: $80.00

ALS (ALQ)

Retained at outperform at Macquarie; Price Target: $16.25

Amcor (AMC)

Retained at outperform at Macquarie; Price Target: $18.20

ANZ Group (ANZ)

Retained at sell at Citi; Price Target: $25.25

Retained at neutral at Macquarie; Price Target: $28.00

APA Group (APA)

Retained at outperform at Macquarie; Price Target: $8.14

ARB Corporation (ARB)

Retained at neutral at Citi; Price Target: $39.54

Retained at buy at Ord Minnett; Price Target: $45.00

Austal (ASB)

Retained at neutral at Citi; Price Target: $4.09 from $4.30

AUB Group (AUB)

Retained at outperform at Macquarie; Price Target: $35.45

BHP Group (BHP)

Retained at outperform at Macquarie; Price Target: $42.00

Boss Energy (BOE)

Retained at buy at Bell Potter; Price Target: $4.80

Brazilian Rare Earths (BRE)

Retained at buy at Ord Minnett; Price Target: $5.50

Bluescope Steel (BSL)

Retained at equal-weight at Morgan Stanley; Price Target: $24.00

Car Group (CAR)

Upgraded to neutral from underweight at Jarden; Price Target: $33.00 from $34.60

Commonwealth Bank of Australia (CBA)

Retained at sell at Citi; Price Target: $90.75

Cuscal Group (CCL)

Retained at buy at Ord Minnett; Price Target: $3.61

Collins Foods (CKF)

Retained at buy at Goldman Sachs; Price Target: $8.25 from $10.00

Cochlear (COH)

Retained at outperform at CLSA; Price Target: $330.00

Coles Group (COL)

Retained at outperform at Macquarie; Price Target: $22.00

Conrad Asia Energy (CRD)

Retained at buy at Bell Potter; Price Target: $1.600

CSL (CSL)

Upgraded to outperform from hold at CLSA; Price Target: $290.00 from $282.50

Retained at outperform at Macquarie; Price Target: $360.30

Corporate Travel Management (CTD)

Retained at neutral at UBS; Price Target: $17.60

DigiCo REIT (DGT)

Retained at positive at E&P; Price Target: $5.13

Doctor Care Anywhere Group (DOC)

Retained at buy at Bell Potter; Price Target: $0.120

Electro Optic Systems (EOS)

Retained at buy at Ord Minnett; Price Target: $1.800

Evolution Mining (EVN)

Retained at neutral at Citi; Price Target: $6.00

Fletcher Building (FBU)

Retained at buy at Citi; Price Target: NZ$3.90

Flight Centre Travel Group (FLT)

Retained at buy at UBS; Price Target: $20.00

Genesis Minerals (GMD)

Retained at hold at Ord Minnett; Price Target: $3.10

Goodman Group (GMG)

Retained at outperform at Macquarie; Price Target: $36.31

Graincorp (GNC)

Retained at outperform at Macquarie; Price Target: $8.76

GPT Group (GPT)

Retained at outperform at Macquarie; Price Target: $5.38

Insurance Australia Group (IAG)

Retained at neutral at Goldman Sachs; Price Target: $8.15

Retained at outperform at Macquarie; Price Target: $8.50

IDP Education (IEL)

Retained at outperform at Macquarie; Price Target: $16.00

IGO (IGO)

Retained at outperform at Macquarie; Price Target: $5.50

James Hardie Industries (JHX)

Downgraded to neutral from overweight at Jarden; Price Target: $53.50 from $54.00

Retained at outperform at Macquarie; Price Target: $65.00

Light & Wonder (LNW)

Retained at outperform at Macquarie; Price Target: $198.00

Lotus Resources (LOT)

Retained at buy at Canaccord Genuity; Price Target: $0.340

Liontown Resources (LTR)

Retained at buy at Bell Potter; Price Target: $1.250 from $1.400

Retained at neutral at Citi; Price Target: $0.600

Retained at neutral at Goldman Sachs; Price Target: $0.690 from $0.710

Retained at neutral at Macquarie; Price Target: $0.650

Retained at hold at Morgans; Price Target: $0.660 from $0.680

Retained at hold at Ord Minnett; Price Target: $0.670 from $0.680

Lynas Rare Earths (LYC)

Retained at buy at Ord Minnett; Price Target: $7.80

Macquarie Technology Group (MAQ)

Retained at positive at E&P; Price Target: $105.34

Mirvac Group (MGR)

Retained at outperform at Macquarie; Price Target: $2.56

Retained at equal-weight at Morgan Stanley; Price Target: $2.25

Mineral Resources (MIN)

Upgraded to buy from sell at UBS; Price Target: $28.60 from $33.00

Metro Mining (MMI)

Retained at buy at Shaw and Partners; Price Target: $0.170

Megaport (MP1)

Retained at positive at E&P; Price Target: $17.59

Retained at outperform at Macquarie; Price Target: $14.30

National Australia Bank (NAB)

Retained at sell at Citi; Price Target: $26.50

Downgraded to underweight from overweight at Jarden; Price Target: $30.00 from $38.00

Retained at neutral at Macquarie; Price Target: $35.00

Newmont Corporation (NEM)

Retained at outperform at Macquarie; Price Target: $95.00

Northern Star Resources (NST)

Retained at neutral at Citi; Price Target: $17.90

Northern Minerals (NTU)

Retained at buy at Ord Minnett; Price Target: $0.030 from $0.033

Nexgen Energy (NXG)

Retained at buy at Shaw and Partners; Price Target: $14.40 from $14.60

Nextdc (NXT)

Retained at positive at E&P; Price Target: $27.76

Retained at outperform at Macquarie; Price Target: $21.20

Orica (ORI)

Retained at buy at UBS; Price Target: $22.00 from $21.00

Pinnacle Investment Management Group (PNI)

Retained at buy at Ord Minnett; Price Target: $28.00

Prospect Resources (PSC)

Retained at buy at Canaccord Genuity; Price Target: $0.400

Qantas Airways (QAN)

Retained at buy at Goldman Sachs; Price Target: $11.80

Retained at neutral at UBS; Price Target: $9.30

Qoria (QOR)

Retained at buy at Ord Minnett; Price Target: $0.580

QPM Energy (QPM)

Retained at buy at Bell Potter; Price Target: $0.110

Regis Healthcare (REG)

Retained at buy at Ord Minnett; Price Target: $7.40

Ramsay Health Care (RHC)

Upgraded to outperform from neutral at Macquarie; Price Target: $37.70 from $38.65

Resmed Inc (RMD)

Retained at outperform at Macquarie; Price Target: $45.10

Siteminder (SDR)

Retained at buy at Ord Minnett; Price Target: $7.20

Sims (SGM)

Retained at neutral at Citi; Price Target: $15.50

Stockland (SGP)

Retained at overweight at Morgan Stanley; Price Target: $6.50

Sigma Healthcare (SIG)

Initiated at neutral at Goldman Sachs; Price Target: $2.70

Stanmore Resources (SMR)

Retained at buy at Citi; Price Target: $3.40

Santos (STO)

Retained at outperform at Macquarie; Price Target: $8.95

Suncorp Group (SUN)

Retained at buy at Goldman Sachs; Price Target: $22.00 from $24.67

Transurban Group (TCL)

Retained at neutral at Macquarie; Price Target: $12.82

Telstra Group (TLS)

Retained at outperform at Macquarie; Price Target: $4.40

Treasury Wine Estates (TWE)

Retained at buy at Citi; Price Target: $13.85

Retained at buy at Ord Minnett; Price Target: $12.00

Vault Minerals (VAU)

Retained at buy at Ord Minnett; Price Target: $0.520

Viva Energy Group (VEA)

Retained at buy at Ord Minnett; Price Target: $3.40

Westpac Banking Corporation (WBC)

Retained at sell at Citi; Price Target: $26.25

WEB Travel Group (WEB)

Retained at buy at UBS; Price Target: $6.15

Whitehaven Coal (WHC)

Retained at buy at Citi; Price Target: $8.60

Woolworths Group (WOW)

Retained at neutral at Macquarie; Price Target: $30.80

Waypoint Reit (WPR)

Retained at accumulate at Ord Minnett; Price Target: $2.72

Wisetech Global (WTC)

Retained at buy at Citi; Price Target: $115.00

Retained at outperform at Macquarie; Price Target: $152.70

Xero (XRO)

Retained at outperform at Macquarie; Price Target: $191.90

Block (XYZ)

Retained at outperform at Macquarie; Price Target: $175.00

Zip Co. (ZIP)

Retained at buy at Ord Minnett; Price Target: $3.60

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| TOU | Tlou Energy Ltd | $0.014 | +75.00% |

| BEZ | Besra Gold Inc | $0.059 | +59.46% |

| SMP | Smartpay Holdings Ltd | $0.78 | +47.17% |

| DNA | Donaco International Ltd | $0.042 | +40.00% |

| SCP | Scalare Partners Holdings Ltd | $0.22 | +33.33% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| RFA | Rare Foods Australia Ltd | $0.014 | -33.33% |

| RLT | Renergen Ltd | $0.55 | -26.67% |

| HIQ | HITIQ Ltd | $0.028 | -17.65% |

| ARC | ARC Funds Ltd | $0.10 | -16.67% |

| TG6 | TG Metals Ltd | $0.11 | -15.39% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| DNA | Donaco International Ltd | $0.042 | +40.00% |

| CAE | Cannindah Resources Ltd | $0.084 | +16.67% |

| MPK | Many Peaks Minerals Ltd | $0.34 | +13.33% |

| NMG | New Murchison Gold Ltd | $0.017 | +13.33% |

| MPW | Metal Powder Works Ltd | $0.45 | +12.50% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| SWP | Swoop Holdings Ltd | $0.12 | -11.11% |

| CG1 | Carbonxt Group Ltd | $0.046 | -9.80% |

| NUZ | Neurizon Therapeutics Ltd | $0.10 | -9.09% |

| MDR | Medadvisor Ltd | $0.11 | -8.33% |

| ACR | ACRUX Ltd | $0.023 | -8.00% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| GLDN | Ishares Physical Gold ETF | $37.61 | -0.61% |

| GXLD | Global X Gold Bullion ETF | $47.08 | -0.70% |

| ASIA | Betashares Asia Technology Tigers ETF | $11.22 | +0.45% |

| AIZ | Air New Zealand Ltd | $0.565 | 0.00% |

| INCM | Betashares Global Income Leaders ETF | $19.36 | -0.16% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| PGC | Paragon Care Ltd | $0.39 | 0.00% |

| NWL | Netwealth Group Ltd | $26.42 | -1.20% |

| ACQ | Acorn Capital Investment Fund Ltd | $0.755 | +0.67% |

| FLT | Flight Centre Travel Group Ltd | $14.09 | +2.77% |

| AMP | AMP Ltd | $1.25 | +0.40% |