ASX 200 Live Today - Wednesday, 25th February

The S&P/ASX 200 is set to snap a three-day losing streak after a strong overnight lead. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Wednesday, February 25. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

That's all for today

[2:40 pm] Thanks for tuning in. A massive day for markets, with the ASX 200 up 0.90%, slightly off session highs but still on track to log a fresh all-time high. A broad effort from Financials (+0.39%) and Materials (+2.1%) as well as the Tech (+5.9%) bounce and Staples (+5.0%) strength. Today's CPI print was a little hot, with headline inflation up 3.8% year-on-year in January vs. market expectations of 3.7%, the RBA's trimmed mean CPI was 3.4%, up from 3.3% in December. The likelihood of an RBA hike in March remains low (~15%) but May is very live (~74%). Notwithstanding the risks of more rate pain ahead, the market is in a good place. Tech stocks are bouncing, Staples are surging, Miners are at all-time highs and Financials are still grinding higher. Tomorrow will be the biggest day for corporate earnings, with a long list of larger caps due to report, including Sigma Healthcare, Lynas, Qantas, Atlas Arteria, Worley and more.

Woolworths set to record largest one-day gain

[2:24 pm] Woolworths is still hovering session highs, up almost 12% to the highest since September 2024. Going back to 2004, this will mark the stock's largest one-day increase.

Date | Close | % Chg |

|---|---|---|

25/02/2026 | $35.30 | 11.92% |

17/03/2020 | $35.19 | 9.72% |

30/03/2020 | $33.68 | 9.60% |

25/07/2016 | $21.46 | 8.24% |

13/03/2020 | $32.72 | 6.74% |

3/11/2008 | $26.17 | 6.58% |

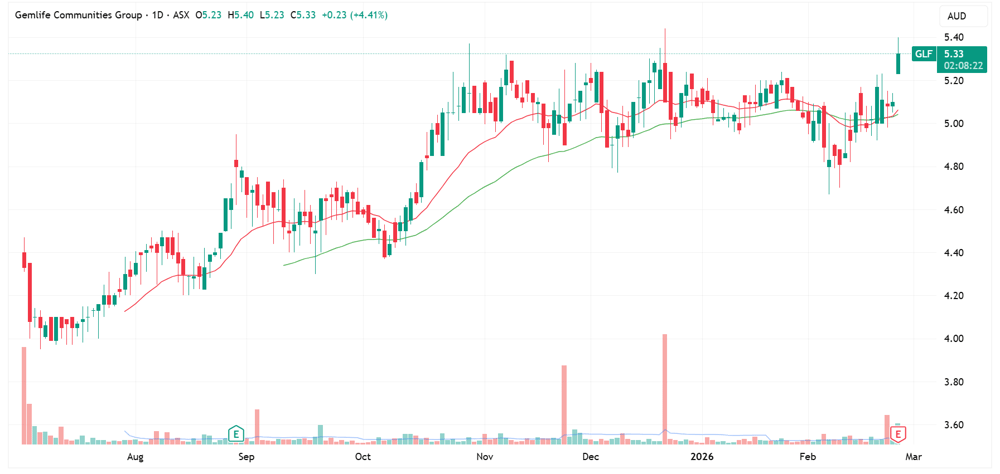

Gemlife is breaking out

[1:53 pm] Gemlife is breaking out to all-time highs, currently up 4.4% after its 2025 result broadly beat both prospectus and consensus expectations.

Gemlife daily price chart (Source: TradingView)

Didn't get to cover the result this morning, but here are the key numbers:

Revenue up 5.8% to $281.7m vs. $272.4m ests (3% beat)

Underlying EBITDA up to $113.5m vs. $106.7m ests (6% beat)

Underlying NPAT up 10.1% to $90.0m vs. $87.9m ests (2% beat)

Average home sale price rose 18% to $833,000 (ex GST), with average build margins up 24% to $418,000, reflecting a deliberate shift toward premium product

Settlements of 312 came in below the prospectus forecast of 333, though 38 completed and sold homes are expected to settle in FY26

Gearing of 29.5% sits within the 25-35% target range, and a February 2026 debt refinancing extended maturity and reduced the cost of debt by 25bps

Helia sharply higher as ~12% dividend up for grabs

[1:50 pm] Helia is trading 18.7% higher, trending sharply higher from a 10.5% open. The 1H26 result was mostly in-line with expectations, with a generous special dividend.

Underlying NPAT up 12% to $247.0m vs. Macquarie ests of $240.8m (2.5% miss)

GWP up 23% to $240.0m, reflecting strong new business momentum

Insurance revenue down 4% to $371.5m vs. Macquarie ests of $363m (2% beat)

Final ordinary dividend of 16 cps plus a special dividend of 67 cps vs. Macquarie ests of 16 cps ordinary and 60 cps special (9.2% beat)

FY26 insurance revenue guidance of $320-370m implies a further step-down from FY25's $371.5m but above Macquarie ests of $319m (8.1% beat at the midpoint)

The backstory with Helia: In August 2025, Helia said its CBA had entered into a contract with another LMI provider (40% of 1H25 GWP), while ING (21% of 1H25 GWP) intended to proceed negotiations with an alternate provider. So a massive loss to the business.

What's interesting is that the loss of these contracts frees up regulatory capital, a metric known as Prescribed Capital Amount (PCA). Helia's PCA is currently sitting at 2.03x compared to its target range of 1.4-1.6x. This has enabled Helia to dish out some special dividends over the last couple of years, with its dividend yield ranging from 16-27% since FY21.

Today's ordinary plus special dividend of 83 cents equates to a dividend yield of 12.9% at current prices ($6.39).

Iress higher, but fades early gains

[1:40 pm] Iress currently up 10.1% ($7.46) but down sharply from intraday highs of 18.5% ($8.02). The 1H26 result was broadly ahead of expectations, with guidance implying some upgrades to consensus. This is a pretty common theme this reporting season, with large gap ups being sold into. To recap the numbers:

Revenue up 6.5% to $561.7m vs. $555.5m ests (1% beat)

UPAT of $73.9m vs. $68.0m ests (9% beat), comfortably above guidance of $67-71m

Total 2025 dividend up 140% to 24 cps vs. 23.8 cps ests (0.8% beat)

FY26 UPAT guidance of $84-90m (midpoint $87m) vs. $77.1m ests (13% beat at midpoint)

FY26 adjusted EBITDA guidance of $116-123m came in well below $141.2m ests (15% miss at midpoint)

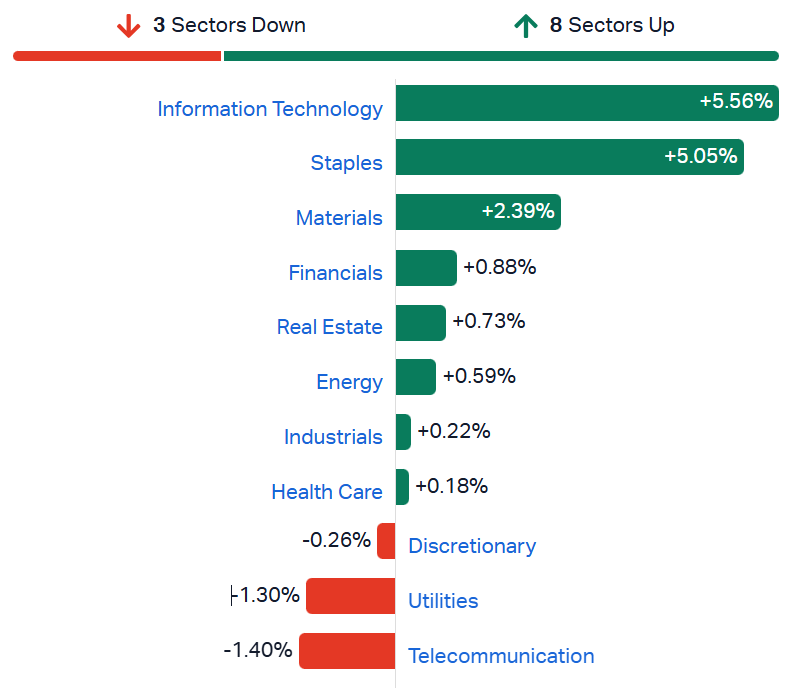

ASX 200 at all-time highs

[1:38 pm] Alright back from a break. You may have noticed a new name on the blog lately, Warren is our newest team member, relatively new to markets, and we're working on getting him up to speed with some solid content on the site.

The ASX 200 has rocketed its way to a fresh all-time high. Lots of moving pieces including:

Tech (+5.6%) still down around 5% in the last four sessions, but a meaningful bounce amid a narrative shift that Anthropic/Claude is more of a partner for software companies, not an absolute replacement

Staples (+4.7%) rallying off the back of Woolworths (+11.0%)

Materials (+2.4%) at fresh all-time highs, with BHP (+2.7%) rallying to a record high of $56

Financials (+0.8%) snapping a two-day losing streak, still up ~7.5% since early Feb

Overall, the most important sectors (Banks and Miners) continue to charge ahead, along with a bounce from tech and surging Staples.

ASX 200 sectors (Source: Market Index)

Uranium stocks lift despite flat price signals

[12:50 pm] The broader market is in a risk-on mood, which is typically supportive for uranium equities. Sprott’s Physical Uranium Trust, a useful barometer for uranium pricing, slipped 0.2% overnight and has been broadly flat since early February.

Ticker | Company | % Chg | Price |

|---|---|---|---|

PEN | Peninsula Energy | 6.44% | $0.78 |

DEV | Devex Resources | 4.44% | $0.24 |

NXG | Nexgen Energy | 4.42% | $18.18 |

DYL | Deep Yellow | 4.39% | $2.74 |

AGE | Alligator Energy | 4.26% | $0.05 |

T92 | Terra Critical Minerals | 3.75% | $0.08 |

BOE | Boss Energy | 3.72% | $1.68 |

PDN | Paladin Energy | 2.72% | $13.78 |

BMN | Bannerman Energy | 1.82% | $4.48 |

AEE | Aura Energy | 1.33% | $0.15 |

EL8 | Elevate Uranium | 1.33% | $0.38 |

LOT | Lotus Resources | 1.14% | $2.23 |

By Warren Masilamony

Tech stocks lift ASX

[12:21 pm] Tech stocks are up today as Anthropic’s new automation plugins were seen as positive to software providers rather than disruptive, easing recent AI displacement fears. The sector is up 5.4% today but remains down 19.3% over the past month.

Ticker | Company | % Chg | Price |

|---|---|---|---|

WTC | Wisetech Global | 9.75% | $47.18 |

360 | Life360 Inc | 7.22% | $23.33 |

NXT | Nextdc | 5.65% | $14.03 |

XRO | Xero | 4.51% | $75.08 |

TNE | Technology One | 2.43% | $23.14 |

CDA | Codan | 0.46% | $34.75 |

By Warren Masilamony

Lithium stocks broadly higher

[11:42 am] Chinese lithium carbonate futures jumped 10.5% on Tuesday and have added a further 4.2% in early Wednesday trade to 167,000 yuan a tonne, giving the sector a strong lead.

Ticker | Company | % Chg | Price |

|---|---|---|---|

LTR | Liontown | 9.48% | $1.99 |

IGO | Igo | 4.13% | $8.70 |

PLS | Pls Group | 3.92% | $4.91 |

MIN | Mineral Resources | 1.71% | $58.27 |

By Warren Masilamony

Results movers: Woolworths, Wisetech, Helia and more

[10:38 am] Overall, a very positive day for reporters, with plenty of stocks up 5-15%.

Tabcorp (+15.8%): Sharply higher after 1H26 earnings and dividends came in well-above expectations.

Iress (+13.4%): 2025 results were slightly ahead of expectations, 2026 guidance also mostly ahead.

Helia (+13.3%): The ordinary and special dividend (16 cps and 67 cps respective) was 9.2% ahead of Macquarie expectations, guidance implied a step down in growth, but much better-than-feared

Woolworths (+9.2%): Absolutely ripping from the open, with 1H26 earnings and dividends ~5% ahead of consensus, FY26 EBIT guidance upgraded towards the upper end of "mid-to-high" single digits

Wisetech (+7.2%): Very volatile open, 1H26 result was mostly 1-5% ahead, e2open integration tracking ahead of schedule, FY26 guidance reaffirmed

Domino's (-10.0%): Not a terrible result, with 1H26 numbers mostly in-line. However, same store sales of -2.5% was below market expectations of a 0.9% decline. SSS in the first weight weeks of FY26 was also down 7.2%. Not a good look.

DroneShield lifts governance after ASX scrutiny

[10:23 am] DRO has tightened its disclosure and director trading controls after an independent governance review, following ASX concerns about its continuous disclosure arrangements.

Trading Policy upgrade includes a new “front page test”, longer blackout periods through to the day after results, and tighter approval processes.

Disclosure Policy changes include setting up a disclosure committee and clearer internal responsibilities and protocols to lower risk of disclosure breaches that can trigger halts and volatility.

Minimum Shareholding Policy introduced, with the CEO expected to hold shares worth 200% of annual salary within 12 months and each director to hold shares worth their annual base fee within 3 years.

The measures are aimed at strengthening disclosure and trading controls and reducing the risk or perception of inappropriate trading. DRO is down 1.3% at $3.01 in morning trade.

By Warren Masilamony | Company page: (DRO)

Top ASX 200 gainers and losers

[10:20 am] A very results driven day, with Tabcorp and Woolworths rallying on better-than-expected numbers, while Domino's continues to see challenges with sales growth.

Ticker | Company | % Chg | Price |

|---|---|---|---|

TAH | Tabcorp | 17.65% | $1.00 |

WOW | Woolworths Group | 7.48% | $33.90 |

ARB | ARB Corp | 6.41% | $22.73 |

LTR | Liontown | 6.34% | $1.93 |

L1G | L1 Group | 5.46% | $1.26 |

360 | Life360 | 5.35% | $22.93 |

IPX | Iperionx | 5.24% | $6.43 |

MGH | Maas Group | 5.15% | $4.29 |

WTC | Wisetech Global | 4.49% | $44.92 |

GDG | Generation Development Group | 3.90% | $4.26 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

DMP | Domino's Pizza | -7.57% | $20.03 |

VEA | Viva Energy Group | -6.04% | $1.76 |

SDF | Steadfast Group | -5.00% | $3.99 |

MND | Monadelphous Group | -4.56% | $30.95 |

DBI | Dalrymple Bay | -3.87% | $5.22 |

LOV | Lovisa | -3.82% | $23.94 |

RMD | Resmed | -2.90% | $35.47 |

TLS | Telstra Group | -2.76% | $5.11 |

TLC | Lottery Corporation | -1.56% | $5.37 |

PXA | Pexa Group | -1.40% | $14.04 |

Domino's posts in-line H1 result but near-term sales remain pressured

[9:53 am] Domino's delivered a broadly in-line first half as deliberate discounting reductions improved franchise economics, though top-line softness persisted across most regions with early 2H trading further disrupted by weather.

Network sales down 1.6% to $2.04bn vs. $2.08bn ests (2% miss)

Same store sales down (2.5%) vs. (0.9%) ests

Franchise partner profitability rose 4.5% to ~$103,000 EBITDA (rolling 12 months), the highest level in three years

EBIT up 1.0% to $101.5m vs. $98.7m ests (3% beat)

Underlying NPAT up 2.2% to $60.1m vs. $59.5m ests (1% beat)

Interim dividend up 16.3% on FY25 final dividend to 25 cps

Europe was the standout in the first half with underlying EBIT up 23.2% and SSS of +1.3%, while ANZ EBIT fell 9.3% and Asia rose 8.2% on improved unit economics despite SSS of (6.1%)

Second half first eight weeks SSS down (7.2%), heavily impacted by severe weather disruptions across Europe and the timing shift of Lunar New Year affecting Malaysia, Taiwan and Singapore, ANZ January franchisee profitability delivered strong double-digit growth as targeted promotions returned medium and high-frequency customers

Full-year guidance reaffirmed, consistent with market expectations at the time of the AGM

Company page: Domino's Pizza (DMP)

WiseTech 1H26 slightly ahead, reaffirms guidance as e2open integration accelerates

[9:47 am] WiseTech delivered a solid first half ahead of consensus across all key metrics, with e2open consolidation driving headline growth while organic momentum and AI-driven efficiency gains remain the key investor focus.

Revenue up 76% to $672.0m vs. $651.2m ests (3% beat)

Organic revenue growth of 7% and CargoWise revenue up 12% to $372.4m

EBITDA up 31% to $252.1m vs. $248.8m ests (1% beat)

EBITDA margin contracted 13 pp to 38% reflecting e2open consolidation costs (in-line with ests)

Underlying NPAT up 2% to $114.5m vs. $108.9m ests (5% beat)

Interim dividend up 1% to 6.8 cps

e2open's $50m annualised cost synergy target was achieved in January, roughly 18 months ahead of schedule

AI-driven headcount reductions of up to 50% flagged in product, development and customer service

FY26 guidance reaffirmed with EBITDA of $550-585m and revenue of $1.39-1.44bn

Company page: WiseTech Global (WTC)

Woolworths beats H1 expectations, raises full-year profit outlook

[9:40 am] Woolworths delivered a solid first half with earnings well ahead of consensus, supported by Australian Food momentum, and upgraded its full-year EBIT growth outlook to the upper end of its guided range.

Revenue up 3.4% to $37.14bn vs. $37.21bn ests (in-line)

EBIT up 14.4% to $1.66bn vs. $1.56bn ests (6% beat)

NPAT ex-items up 16.4% to $859m vs. $798.3m ests (8% beat)

Interim dividend up 15.4% to 45 cps vs. 43 cps ests (4.6% beat)

FY26 EBIT growth now expected at the upper end of the mid-to-high single digit range, with Australian Food H2 sales tracking up 5.8% (7.2% ex-tobacco) in the first seven weeks

Morgans commentary before the result: "We expect management to maintain guidance for FY26 Australian Food EBIT to return to mid to high-single digit growth."

BIG W is on track to be EBIT and cash flow positive in FY26 though heavily weighted to H1, with early H2 sales flat on the prior year

Company page: Woolworths Group (WOW)

Tabcorp delivers strong 1H26 earnings beat

[9:36 am] Tabcorp significantly beat expectations on underlying earnings, with cost reductions and operating leverage driving a 190 basis point EBITDA margin improvement despite modest top-line growth.

Revenue up 1.0% to $1.34bn vs. $1.34bn ests (in-line)

Adjusted EBITDA up 14.3% to $217.4m vs. $198.9m ests (9% beat)

EBITDA margin expanding 190 bps to 16.2% vs. Morgans ests of 15.0% (120 bp beat)

Underlying NPAT up 61.5% to $35.7m vs. $26.6m ests (34% beat)

Interim dividend up 50% to 1.5 cps vs. 1.1 cps ests (36% beat)

Company flagged franked dividends are unlikely near term given carried losses

Domestic wagering turnover up 0.3%, with sport turnover up 6.9% and Digital-In-Venue turnover up 12.3%, partially offset by below-average yields

Outlook points to steady turnover levels with $120-140m capex guidance, a $5m World Cup spend, and cost discipline expected to continue offsetting inflationary pressures

Company page: Tabcorp Holdings (TAH)

Worley wins Danish hydrogen pipeline contract

[9:32 am] Worley has secured a five-year EPCM contract to help build Denmark's national hydrogen transmission network, reinforcing its position in European clean energy infrastructure.

The contract covers EPCM services for approximately 41 km of new hydrogen pipeline and conversion of approximately 89 km of existing natural gas pipeline, with commissioning expected by late 2030

Company page: Worley (WOR)

Helia delivers strong FY25 earnings growth and substantial capital returns

[9:29 am] Helia posted solid underlying profit growth in FY25, supported by strong GWP momentum, though insurance revenue declined and claims crept higher, with FY26 guidance pointing to a softer revenue outlook.

Underlying NPAT up 12% to $247.0m vs. Macquarie ests of $240.8m (2.5% miss)

GWP up 23% to $240.0m, reflecting strong new business momentum

Insurance revenue down 4% to $371.5m vs. Macquarie ests of $363m (2% beat)

Total incurred claims ratio of (17.0%) vs. (9.5%) in the prior period, a meaningful deterioration though still well below through-the-cycle average levels

Final ordinary dividend of 16 cps plus a special dividend of 67 cps vs. Macquarie ests of 16 cps ordinary and 60 cps special (9.2% beat)

FY26 insurance revenue guidance of $320-370m implies a further step-down from FY25's $371.5m but above Macquarie ests of $319m (8.1% beat at the midpoint)

I will take a closer look at Helia later this afternoon. In summary, they've lost some major contracts in the last 12-24 months, but sitting on a very strong capital position (hence the special dividends). The company still has capacity for more capital return initiatives, even as earnings continue to slip.

Company page: Helia Group (HLI)

Fortescue delivers strong first half, lifts interim dividend 24%

[9:23 am] Fortescue posted a solid first half underpinned by record iron ore shipments and strong margin expansion, with EBITDA comfortably ahead of estimates and a higher dividend.

Revenue up to $8.44bn vs. $8.34bn ests (1% beat)

Underlying EBITDA up 23% to $4.49bn vs. $4.21bn ests (7% beat)

Attributable NPAT of $1.91bn vs. $1.93bn ests (1% miss)

Interim dividend up 24% to 62 cps

(I don't have any first half ests handy unfortunately)

Record first half iron ore shipments of 100.2Mt, up 3% on 1H25

Free cash flow of $1.5bn and cash on hand of $4.7bn, leaving net debt at just $1.0bn

FY26 guidance reaffirmed across shipments (195-205Mt), C1 hematite costs ($17.50-18.50/wmt) and capex ($3.3-4.0bn metals, ~$300m energy)

Company page: Fortescue (FMG)

Flight Centre 1H26 ahead of expectations, reaffirms full-year guidance

[9:13 am] Flight Centre delivered a stronger-than-expected first half with record TTV and a cost margin low, and maintained full-year guidance that implies meaningful 2H acceleration.

Revenue up to $1.41bn vs. $1.38bn ests (2% beat)

Underlying EBITDA up 9% to $213m vs. $204.5m ests (4% beat)

UPBT up 4% to $125m vs. $119.8m ests (4% beat),

Growth constrained by a ~$7m net interest headwind from recent capital management initiatives

Group TTV up 7% to $12.54bn

Interim dividend up 9% to 12 cps fully franked vs. 14 cps ests (14% miss)

FY26 UPBT guidance reaffirmed at $315-350m vs. $329.9m ests (1% beat)

The guidance implies 15% growth on FY25 and a typical 38/62% first-half/second-half skew. Second half to be supported by stronger leisure seasonality, an Asia turnaround and scaling productivity initiatives.

Company page: Flight Centre Travel Group (FLT)

Iress beats 2025 guidance across the board

[9:08 am] Iress closed out FY25 ahead of its own guidance on all key metrics, though forward guidance for EBITDA came in well below analyst expectations, likely reflecting reinvestment headwinds.

Revenue up 6.5% to $561.7m vs. $555.5m ests (1% beat)

Adjusted EBITDA up 14.9% to $136.2m vs. $130.6m ests (4% beat), ahead of guidance of $128-132m

UPAT of $73.9m vs. $68.0m ests (9% beat), comfortably above guidance of $67-71m

Total 2025 dividend up 140% to 24 cps vs. 23.8 cps ests (0.8% beat)

FY26 guidance was a little mixed:

FY26 UPAT guidance of $84-90m (midpoint $87m) vs. $77.1m ests (13% beat at midpoint)

FY26 adjusted EBITDA guidance of $116-123m came in well below $141.2m ests (15% miss at midpoint)

FY26 revenue guidance of $520-528m (midpoint $524m) vs. $530.3m ests (1% miss)

Company page: Iress (IRE)

SiteMinder posts strong ARR growth but losses wider than expected

[9:03 am] SiteMinder delivered accelerating revenue and ARR momentum in H1 FY26, though earnings came in below estimates and the adjusted NPAT loss was wider than consensus anticipated.

Revenue up 25.5% to $131.1m vs. $131.6m ests (in-line)

Adjusted EBITDA more than doubled to $12.3m vs. $13.6m ests (10% miss)

Adjusted gross margin up 98 bps to 67.8% vs. Morgans ests of 66.3% (150 bp beat)

Adjusted NPAT loss of ($3.9m) vs. ($0.1m) ests

ARR grew 29.7% to $280.3m, with transaction ARR surging 51.3% to $111.7m and subscription ARR up 18.4% to $168.6m

ARPU rose 11.3% to $435, driven by a 22.8% jump in transaction ARPU to $178, reflecting growing Smart Platform adoption across 53,000 total properties

Outlook calls for continued strong ARR growth in second half with further EBITDA and free cash flow improvement, with the company targeting an acceleration towards 30% revenue growth in the medium term

The result reads relatively soft, with in-line revenue and wider than expected loss, though margins ahead. SiteMinder shares have nosedived 51% YTD.

Company page: SiteMinder (SDR)

Alcoa eyes data centre land sales

[8:57 am] Alcoa is exploring the sale of closed and curtailed aluminium sites to data centre and AI operators, aiming to extract value from otherwise idle assets.

Management flagged 10 sites are being assessed for sale into the data centre/AI space, with the first transaction expected in H1 2025 and two more potentially following shortly after

The shift in strategy reflects the surge in demand for large, infrastructure-ready land parcels driven by AI buildout, with management focused on capturing value across the full chain before divesting

Company page: Alcoa (AAI)

Acrow posts record revenue but earnings slip on higher costs

[8:54 am] Acrow delivered record sales in 1H26, broadly in-line with estimates, though earnings declined as cost pressures weighed on margins.

Revenue up 23% to $156.0m vs. $155.0m ests (in line), within guidance range of $153-157m

Underlying EBITDA down 3% to $38.0m vs. $38.4m ests (1% miss)

Underlying NPAT down 22% to $12.9m vs. $13.1m ests (2% miss),

Interim dividend down 31% to 2.0 cps

Industrial Access division drove the result, representing 62% of group revenue

FY26 guidance maintained for 22% revenue growth and 2% EBITDA growth on the prior period, suggesting the margin headwinds are expected to persist into the second half

Company page: Acrow (ACF)

Steadfast misses but reaffirms full-year guidance

[8:50 am] Steadfast posted a clean H1 result with EBITA and NPAT ahead of expectations, though a revenue miss reflects a different mix, and full-year guidance was maintained comfortably.

Revenue of $900.7m vs. $972.6m ests (7% miss)

EBITA up 12.6% to $293.6m vs. $292.8m ests (in line)

Underlying NPAT up 7% to $137.5m vs. Macquarie ests of $157.4m (12% miss)

Interim dividend of 8.2 cps vs. 8.3 ests (1.2% miss)

FY26 underlying NPAT guidance reaffirmed at $315-325m vs. $315.1m ests and underlying EBITA guidance reaffirmed at $650-665m vs. $644.5m ests

Company page: Steadfast Group (SDF)

Wagners delivers strong H1 beat, upgrades full-year guidance

[8:47 am] Wagners posted a solid first half with earnings well ahead of estimates and guidance, driven by strong momentum across both its core construction materials and composite fibre technology divisions.

Revenue up 21% to $251.7m vs. $247.2m ests (2% beat)

Operating EBIT up 72% to $35.0m vs. $32.0m ests (9% beat)

Also exceeding the company's own guidance range of $31-33m

NPAT up 70% to $21.0m vs. $18.5m ests (14% beat)

Construction Materials revenues rose 21% to $156.5m, while Composite Fibre Technology revenues surged 36% to $47.3m, both pointing to broad-based demand strength

Full-year FY26 Operating EBIT guidance upgraded to $62-66 million vs. $54 million consensus (18.5% beat). Wagners has been trading mostly sideways year-to-date but up 145% in the last twelve months.

Company page: Wagners Holding (WGN)

Results coverage kicks off

[8:45 am] Alright, that's enough overnight stuff. Time to dig into some results.

Notable reporters today include: Fortescue (FMG), Woolworths Group (WOW), Wisetech Global (WTC), Yancoal Australia (YAL), Vault Minerals (VAU), Steadfast Group (SDF), L1 Group (L1G), Flight Centre Travel Group (FLT), DroneShield (DRO), Domino's Pizza Enterprises (DMP), Tabcorp Holdings (TAH), Silex Systems (SLX), Generation Development Group (GDG), Centuria Capital Group (CNI), Sunrise Energy Metals (SRL), Helia Group (HLI), MAAS Group Holdings (MGH), Service Stream (SSM), IRESS (IRE), Elevra Lithium (ELV), SiteMinder (SDR), Amplitude Energy (AEL), Bapcor (BAP), Duratec (DUR), Accent Group (AX1), IVE Group (IGL), Energy One (EOL), Resimac Group (RMC)

Oh yeah, one more thing. Lots of fading action from yesterday's results, with names like Dalrymple Bay, Monadelphous, Kelsian, Cedar Woods and more reporting strong results, gapping up but finishing the session at worst levels.

US tariff rollout sparks legal challenges and ally pushback

[8:43 am] The post-SCOTUS tariff regime is underway but faces mounting legal, diplomatic, and procedural uncertainty that could reshape the final outcome.

CBP implemented a 10% global tariff overnight rather than the 15% Trump had flagged, with an administration official signalling the higher rate is still coming

Legal questions are mounting around the use of Section 122 as the authority for tariffs, which applies to balance-of-payments deficits and may not clearly cover the current context; the administration is also reportedly exploring Section 232 tariffs on national security grounds as a separate vehicle

The EU is pushing back, arguing the new cumulative tariff rate breaches the ceiling agreed with the US last northern summer; the EU parliament has suspended ratification of that deal, and EU trade chief Sefcovic flagged a transition period of up to four months may be needed

China signalled it could adjust its countermeasures "in due course," keeping the door open to escalation

FedEx has become the first major US company to file suit in the US Court of International Trade seeking a full tariff refund, a significant development given the administration previously argued refund availability was a key reason tariffs could be collected while legality was being tested

Trump's State of the Union address tonight is expected to cover trade and tariffs, potentially offering more clarity on the administration's direction

Anthropic Expands Claude Into Finance, HR and Design With New Cowork Tools

[8:42 am] Anthropic is pushing Claude deeper into professional workflows, with a particular focus on financial services, as it looks to justify its $380 billion valuation.

Anthropic unveiled new Claude Cowork plugins targeting HR, investment banking, design, financial analysis, equity research, private equity and wealth management, developed alongside partners including FactSet

Claude is now used for at least 25% of tasks across one in two US jobs, up from one in three a year ago, according to Anthropic's head of economics

Novo Nordisk cut a 10-week clinical study report process down to 10 minutes using a customised Claude tool, illustrating the productivity gains on offer for enterprise customers

Financial data stocks FactSet, S&P Global and Moody's each rose at least 2% during the event, suggesting the market views Anthropic's finance push as a partnership opportunity rather than a pure displacement threat

Anthropic's head of product pushed back on the idea that individual product releases are driving sector-wide selloffs, though the company's recent Opus model release did contribute to a slump in financial services stocks

Source: Bloomberg

AMD Secures Blockbuster Meta Deal

[8:40 am] AMD lands a landmark multi-year chip supply agreement with Meta, marking a significant step in its challenge to Nvidia's AI dominance.

Meta will deploy 6 gigawatts of AMD-based data centre infrastructure over five years starting H2 2026, with the deal valued at "double-digit billions" of dollars per gigawatt

As part of the arrangement, Meta receives warrants to purchase 160 million AMD shares in stages, vesting upon deployment milestones and AMD share price targets as high as $600. This deal gives Meta up to 10% ownership of AMD

AMD shares surged 8.8% on the news, their best single-day gain since November, though the stock had been down 8.2% year-to-date heading into the announcement

Meta confirmed it will continue purchasing from Nvidia and developing its own in-house chips, with AMD's processors expected to serve inference workloads across different data centres

Source: Bloomberg

China's Lunar New Year spending hits record highs amid cautious optimism

[8:39 am] Chinese consumers splurged during the 2026 Lunar New Year break, according to Bloomberg, with headline figures pointing to a consumption recovery, though underlying data tells a more nuanced story.

Total domestic tourism spending rose to 803.5bn yuan ($117bn), up 126.5bn yuan from a year earlier, partly aided by the holiday being one day longer

Domestic tourist trips reached 596 million, up 95 million year-on-year, with hotel nights up 75% and theme park/attraction bundle orders up 140% (per Alibaba's Fliggy platform)

Average daily sales at key retail and catering enterprises rose 8.6% in the first four days, while Hainan duty-free sales surged ~33% to 2.7bn yuan

However, per-trip spending of 1,348 yuan came in slightly below last year's record of 1,351 yuan and only 9% above 2019 levels, suggesting headline totals flatter underlying demand

Box office takings were the lowest since 2017 at under 6bn yuan, and CICC flagged that sustained consumption growth still requires policy support given sluggish household income growth and weak consumer confidence

Source: Bloomberg

A solid overnight bounce

[8:39 am] A fairly positive overnight session, with the S&P 500 (+0.77%) recovering most of yesterday's (-1.04%) pullback. Software stocks tried to bounce, with the iShares Expanded Tech-Software ETF up 1.9% (but still down 4% in the last three sessions. Starting to see the AI vs. software narrative shift to partnerships and collaboration instead of outright replacement. Also seeing some pushback against the dire/bearish scenarios in the Citrini report, which drove tech and financials sharply lower yesterday.

Good morning!

[8:30 am] ASX 200 futures are up 21 pts (+0.23%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks bounced and closed at session highs

Broad gains across the board, with strength nearly everywhere offsetting pockets of softness in Energy and Healthcare

Software stocks bounced after Anthropic's enterprise agent event highlighted partnerships and collaboration with companies instead of being an outright replacement