ASX 200 Live Today - Tuesday, 21st April

The S&P/ASX 200 is set to rise after trading around breakeven in the last two sessions. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, April 21. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 lower as resource and banks slip

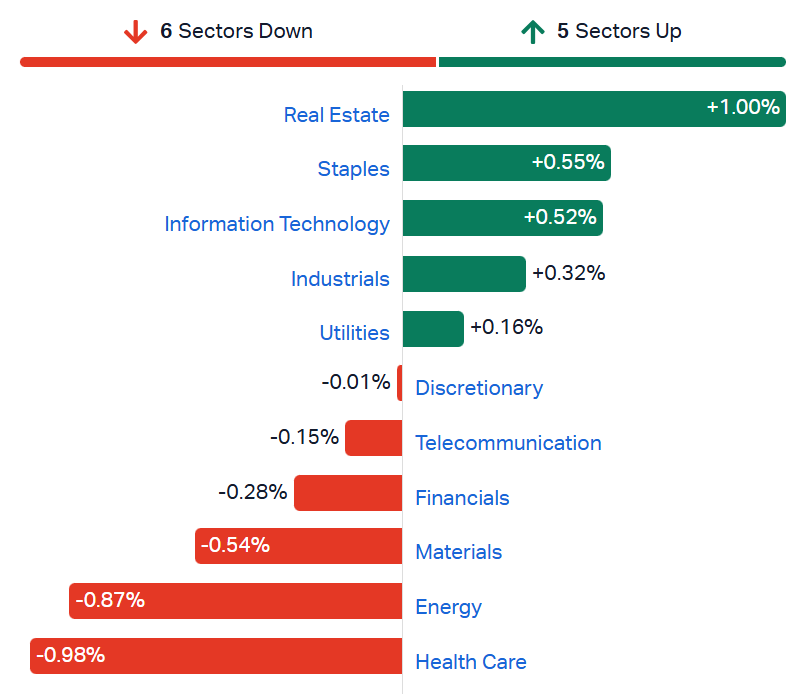

[2:15 pm] That's all for today. A fairly quiet and rangebound session, with the S&P/ASX 200 currently down 0.26%. The yield-sensitive real estate sector is a notable gainer today, up 1.0% to the highest since 4 March. It's now rallied 10.8% since the 30 March low. While the ASX 200 is trading slightly lower, a few risk-oriented indices like the Small Ords (+0.51%), Emerging Companies (+0.32%) and All Tech (+0.40%) continue to edge higher. On the flip side, Financials are on track to fall for a seventh straight session. Westpac's Q2 trading update last Tuesday likely kickstarted this pullback, which noted below consensus earnings momentum and margin headwinds.

ASX 200 sectors (Source: Market Index)

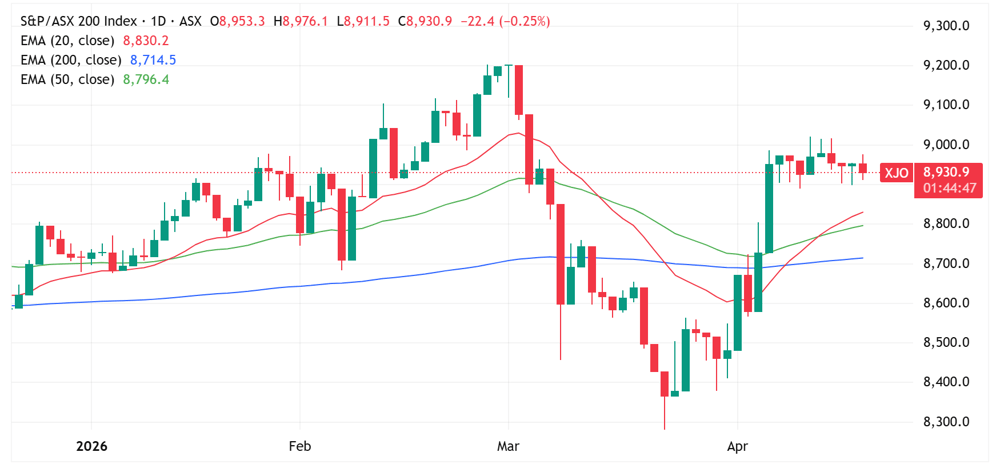

The ASX 200 to experience volatile intraday moves, where rallies are faded but dips are bought, however, closing prices have been extremely narrow. In the last nine sessions, the index has closed within a 52 point range (~0.60%).

ASX 200 daily price chart (Source: TradingView)

On a side note, missed a pretty cool catalyst today. Overnight, USA Rare Earth acquired Brazil’s Serra Verde Group in a US$2.8 billion cash-and-stock deal. Serra's flagship project is Pela Ema, an ionic adsorption clay deposit, with a Mineral Resource of 911Mt at 0.12% TREO (typical of ionic clay deposits to have big tonnage and low grades). This move has driven sharp gains for local rare earth plays (with Brazilian projects), including Viridis Mining (+28.9%) and Brazilian Rare Earths (+9.1%).

CMRG lifts BHP iron ore ban, supporting price realisations

[1:29 pm] UBS notes China's CMRG has reportedly lifted bans on Chinese mills procuring BHP iron ore following executive visits, marking de-escalation in a seven-month pricing dispute and removing a key overhang.

Ban lifted on US dollar denominated BHP iron ore purchases including Jimblebar, Jinbao and Newman fines, with Jimblebar fines alone representing around 25% of WAIO exports

Early evidence of improved trading terms with Jimblebar fines discounts tightening to around 7% from around 11% the week prior

Potential reversal of weaker price realisations estimated to be worth US$0.3bn EBITDA for BHP, though final resolution expected to slightly weaken overall price realisations for miners

Chinese lithium prices slip

[1:25 pm] Chinese lithium prices opened relatively flat, now down 4.2% to 171,700 yuan a tonne. Prices rallied as much as ~7% between 16-20 April to just over 180,000 or within 5% of early January highs. The bellwether PLS Group is now pulling back from record highs, currently down 2.0% to $5.92.

UBS flags travel sector air pocket but sees value in key picks

[1:15 pm] UBS sees the Middle East conflict creating a near-term earnings air pocket and more challenging 18-month macro backdrop for travel-exposed names. Though some sharp share price declines point to a handful of value picks, including SDR, WEB and KLS.

Macro outlook materially revised, including 2 additional interest rate increases in CY26 (4 total), 1.5% to inflation and -1% reduction to GDP, with RBA wanting households to cut spending

Sector exposure scores (worst = 60): THL 39, FLT 36, WEB 32, CTD 28, SKO 20, KLS 18, SDR 17

SDR preferred on defensive topline (75% of gross profit from subscriptions) with AI concerns seen as overdone, shares down 57% since 4Q25 peak, trading on 19.9x 1yr fwd EV/EBITDA with 2yr EBITDA CAGR of +76%

WEB trading on 8.8x 1yr fwd PE following 42% share price decline since 4Q25, still forecasting 2yr EPS CAGR of +15% despite ~11% revenue exposure to the Middle East and no Australian consumer exposure

KLS well contracted with monthly fuel escalation and annual WPI linkages, 1yr fwd PE of 9x vs long-run 15x, with Sep 26 business sale expected to clear balance sheet concerns

Analysts' take on Qube

[12:44 pm] Qube revised FY26 earnings guidance lower on Monday, citing Middle East conflict-driven fuel cost and supply chain disruption (~$10-20m EBIT impact) alongside adverse weather events in WA and NZ (~$3-5m EBIT), though the agreed Macquarie Asset Management Consortium scheme at $5.20 per share remains unaffected with the meeting expected in June 2026.

Analysts broadly viewed the headwinds as transitory with FY27 normalisation expected once fuel costs moderate and weather patterns stabilise, supported by contractual pass-through mechanisms, though timing of recovery remains uncertain. Shares finished flat on the day.

Jarden retained Neutral, target unchanged at $5.00. Impacts are predominantly transitory with FY27 normalisation expected, and the MAM deal continues to drive share price appreciation despite likely material consensus downgrades.

Ord Minnett retained Hold, target unchanged at $5.20. The deal agreement shields valuation amid current volatility and operational scale advantage is preserved through the disruption, with near-term challenges appropriately repriced.

Tech stocks eye six day win streak

[12:42 pm] The S&P/ASX 200 Tech Index is currently up 0.31%, eyeing a potential six-day win streak. While the index is tracking higher, today's gains are a little more mixed, with names like Pro Medicus and TechnologyOne trading slightly lower.

Ticker | Company | % Chg | Price | 1 Yr % Chg |

|---|---|---|---|---|

NXL | Nuix | 4.7% | $1.33 | -43.9% |

CDA | Codan | 4.6% | $36.47 | 149.5% |

MP1 | Megaport | 3.0% | $8.83 | -9.9% |

OCL | Objective Corporation | 2.1% | $12.07 | -21.0% |

BVS | Bravura Solutions | 1.8% | $2.22 | 4.7% |

MAQ | Macquarie Technology Group | 1.5% | $71.75 | 24.1% |

DTL | Data#3 | 1.2% | $7.43 | 2.4% |

XRO | Xero | 1.0% | $82.95 | -46.1% |

HSN | Hansen Technologies | 0.8% | $5.05 | 0.6% |

WTC | Wisetech Global | 0.5% | $45.74 | -44.9% |

360 | Life360 | 0.3% | $22.54 | 18.6% |

WBT | Weebit Nano | 0.2% | $4.09 | 155.6% |

DDR | Dicker Data | 0.1% | $9.04 | 11.5% |

SDR | Siteminder | 0.0% | $3.32 | -11.2% |

IRE | Iress | -0.1% | $7.09 | -8.6% |

PPS | Praemium | -0.4% | $0.74 | 11.7% |

AD8 | Audinate Group | -0.9% | $2.64 | -53.5% |

CAT | Catapult Sports | -1.2% | $3.24 | -11.2% |

TNE | Technology One | -1.9% | $29.92 | 8.1% |

PME | Pro Medicus | -2.1% | $141.81 | -30.3% |

DGT | Digico Infrastructure REIT | -2.4% | $2.06 | -17.6% |

Analysts' take on NAB

[11:46 am] NAB pre-announced a series of balance sheet adjustments on Monday, ahead of its 1H26 results, including increased forward-looking impairment charges across sectors exposed to geopolitical risk, a partially underwritten DRP at a discount to bolster capital, and an accelerated software amortisation charge to align its capitalisation policy with peers. The stock dipped 3.6% on the day.

JPMorgan retained Neutral, lowered target from $46.10 to $43.90. Prior forward-looking adjustment rundown left inadequate headroom for deterioration, and while the software policy change removes earnings distortion, current valuation appears fair given macroeconomic uncertainty.

Morgans retained Sell, lowered target from $37.27 to $34.56. The equity raise came earlier than anticipated and the software charge reflects belated recognition of true cost levels, with shareholder returns challenged by provision build and dilution.

Goldman Sachs retained Sell, lowered target from $41.71 to $40.10. Cash earnings reflect multiple headwinds converging in a single half and forward impairment guidance pivots away from management's previous cycle peak commentary, though CET1 now approaches peer levels.

Lynas trading lower after soft quarterly

[11:43 am] Lynas is currently down 2.5% but off session lows of -4.3% after quarterly revenue and production figures missed market expectations.

Gross sales revenue up 115% year-on-year to $265.0m vs. ests $329.7m (20% miss)

NdPr production up 32% to 1,996t vs. ests 2,200t (9% miss)

Total REO production up 69% to 3,233t vs. ests 3,900t (17% miss)

Average selling price across all rare earth products was $84.60/kg, in line with the prior quarter, with the stable blended price reflecting a higher mix of lower-value products offsetting the NdPr price uplift

Lynas also noted: "To date, we have not experienced any material disruptions due to the current global fuel supply situation. However, price increases are expected for a number of materials. It is difficult to forecast the magnitude and duration of these price increases."

Despite the soft quarterly and cost pressures, Lynas highlighted plenty of de-risking events from the quarter, including:

Malaysia operating licence renewed for 10 years from March 2026, a materially longer term than prior 3-year renewals, providing significantly greater investment and supply chain certainty

Lynas signed a 12-year updated supply agreement with Japanese partners JARE, including firm offtake of 5,000t per annum NdPr at a US$110/kg floor price and firm offtake of 50% of all heavy rare earth oxides produced

A letter of intent was signed with the US Government for approximately US$96m in rare earth purchases over four years, also with a US$110/kg NdPr floor price

Banks whipsaw, Financials down for seventh straight session

[11:34 am] The S&P/ASX 200 Financials Index is currently down 0.5% despite trading 0.45% higher in early trade. ANZ experienced a big swing from a 1.1% gain to falling as much as 3.0%, now down 2.5%. If the index closes lower, it'll mark seven straight days of declines.

Ticker | Company | % Chg | Price |

|---|---|---|---|

ANZ | ANZ Group | -2.53% | $36.97 |

BEN | Bendigo & Adelaide Bank | -0.68% | $11.01 |

CBA | Commonwealth Bank | -0.65% | $178.98 |

BOQ | Bank Of Queensland | -0.62% | $7.27 |

WBC | Westpac | -0.36% | $39.88 |

NAB | National Australia Bank | -0.04% | $41.01 |

MQG | Macquarie Group | 0.58% | $241.06 |

Morgan Stanley cuts REIT price targets ~7% on higher rate assumptions

[11:07 am] Rising Australian bond yields have prompted Morgan Stanley to overhaul its interest rate assumptions across its 22-stock REIT coverage, with the broker below consensus on the majority of names.

The downward revision was driven by a 50 bps uplift in the risk-free rate assumption to 4.5% (from 4.0%), removal of all cap rate compression from base case valuations, and adoption of 4.0% cost of debt from June 2028 onwards.

Arena REIT (ARF) target cut to $3.75 from $4.00

Dexus (DXS) target raised to $6.47 from $6.37

GPT Group (GPT) target cut to $5.83 from $6.13

Lendlease (LLC) target cut to $3.89 from $4.80

Scentre Group (SCG) target cut to $4.41 from $4.71

Vicinity Centres (VCX) target cut to $2.63 from $2.68

Charter Hall (CHC) target cut to $26.89 from $27.75

Waypoint REIT (WPR) target cut to $2.50 from $2.70

Centuria Capital (CNI) target cut to $2.05 from $2.40

Centuria Industrial REIT (CIP) target cut to $3.35 from $3.59

Centuria Office REIT (COF) target cut to $1.00 from $1.12

BWP Trust (BWP) target cut to $4.10 from $4.15

HMC Capital (HMC) target cut to $2.80 from $3.35

Analysts' take on Viva Energy

[11:03 am] Viva Energy's Q1 trading update on Monday delivered exceptional refining margins that materially exceeded consensus, driven by Middle East geopolitical disruption tightening regional product supply, with brokers viewing the recent Geelong refinery fire as a contained, manageable event offset by insurance coverage and a return to 90% capacity expected within weeks.

Analysts broadly upgraded FY26 earnings forecasts and viewed the incident as a buying opportunity, though caution remains around weak Convenience shop sales reflecting consumer cost-of-living pressures and the sustainability of elevated refining margins into H2.

The stock dipped 9.0% on Monday, and currently up 2.8% to $2.37.

JPMorgan retained Neutral, raised target from $2.50 to $2.60. Geelong recovery is tracking well and margin upside more than offsets production disruptions, with conservative forward guidance creating earnings upside risk.

RBC Capital Markets retained Outperform, target unchanged at $2.50 . Regional scarcity underpins an extended refining margin timeline driving significant earnings upgrades, with agricultural sector activity confirming broad-based demand recovery.

UBS retained Buy, lowered target from $2.70 to $2.65. Insurance coverage significantly limits financial exposure from the incident and margin strength adequately compensates for production outages, though the repair timeline remains an uncertain variable for guidance.

China EV sales recovering but lithium supply keeps medium-term price ceiling in place

[11:01 am] Morgan Stanley's March EV data shows tentative demand recovery in China, though destocking and supply-side dynamics limit the near-term read-through for lithium equities.

China BEV sales up 72% month-on-month and 3% year-on-year in March, though down 0.6% year-to-date. Morgan Stanley forecasts CY26 wholesale sales growth of 9%

Recovery was driven by post-CNY order pickup and new model launches, though channel destocking remained the priority for most EV brands.

EV prices edged lower across most brands with OEMs shifting toward upgrade and financing incentives rather than discounts on new models

Morgan Stanley's commodities team models a ~117kt lithium deficit for CY26, but sees supply expansions and restarts keeping medium-term prices close to incentive levels

Spot spodumene at ~US$2,400/t vs. Morgan Stanley's long-term real price of US$1,510/t

The Jianxiawo restart is not expected until Q4 CY26, and China licensing issues continue to limit other supply candidates, though Reuters reported some improvement out of Zimbabwe on 13 April

Top ASX 200 gainers

[10:09 am] Plenty of growth and risk-oriented names trading higher, including Droneshield, Wisetech and Block. Viva is also bouncing after suffering a 9.0% dip on Monday.

Ticker | Company | % Chg | Price |

|---|---|---|---|

SRL | Sunrise Energy Metals | 8.77% | $12.78 |

DRO | Droneshield | 4.71% | $3.78 |

WTC | Wisetech Global | 3.58% | $47.12 |

XYZ | Block | 3.48% | $102.30 |

GDG | Generation Development Group | 2.97% | $4.69 |

LNW | Light & Wonder | 2.77% | $126.99 |

EOS | Electro Optic Systems | 2.70% | $10.27 |

VEA | Viva Energy Group | 2.61% | $2.36 |

CDA | Codan | 2.58% | $35.78 |

XRO | Xero | 2.43% | $84.15 |

Top ASX 200 losers

[10:09 am] Challenger sold off after a downbeat 3Q26 FUM update, Hub24 also lower on a mixed FUM update, also some softness across the gold sector.

Ticker | Company | % Chg | Price |

|---|---|---|---|

CGF | Challenger | -4.59% | $8.01 |

HUB | Hub24 | -4.11% | $91.53 |

CEN | Contact Energy | -4.10% | $7.71 |

GYG | Guzman Y Gomez | -2.38% | $20.54 |

LYC | Lynas Rare Earths | -2.35% | $19.91 |

MCY | Mercury | -1.85% | $5.31 |

WAF | West African Resources | -1.74% | $3.38 |

PRU | Perseus Mining | -1.59% | $5.58 |

EVN | Evolution Mining | -1.41% | $13.63 |

YAL | Yancoal Australia. | -1.21% | $6.52 |

ASX 200 opens higher

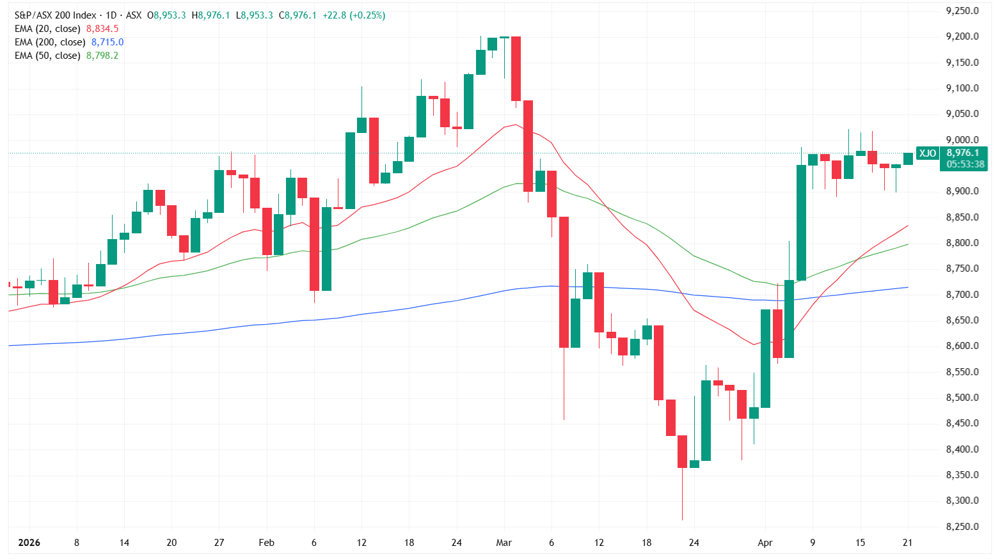

[10:07 am] ASX 200 up 0.23% in early trade, having maintained a rather narrow trading range in the last nine trading sessions. Nine out of eleven sectors are currently positive, with notable gains from Tech (+1.42%), Industrials (+0.63%) and Discretionary (+0.50%).

ASX 200 daily chart (Source: TradingView)

Lynas Q3 FY26: Record quarterly revenue but production below consensus

[9:56 am] Lynas delivered its highest quarterly revenue since 4Q22 on stronger NdPr pricing and volumes, though production fell short of expectations.

Gross sales revenue up 115% year-on-year to $265.0m vs. ests $329.7m (20% miss)

Revenue jump driven by higher NdPr and total REO volumes, and a 25% increase in average NdPr selling price quarter-on-quarter

NdPr production up 32% to 1,996t vs. ests 2,200t (9% miss)

Total REO production up 69% to 3,233t vs. ests 3,900t (17% miss)

Average selling price across all rare earth products was $84.60/kg, in line with the prior quarter, with the stable blended price reflecting a higher mix of lower-value products offsetting the NdPr price uplift

First production of samarium oxide achieved in March, ahead of the April 2026 target, adding a new high-value product to the portfolio used in aerospace, electronics and medical applications

Company page: Lynas Rare Earths (LYC)

Broker moves: Morgans cautious on auto retailers, Bell Potter initiates food and beverage coverage

[9:45 am] A mixed bag of rating changes with Morgans cutting targets sharply across the auto parts space while Bell Potter sees value in Collins Foods among its new fast food coverage.

ARB Corp. upgraded to accumulate from hold, though target cut sharply to $22.04 from $31.85 (Morgans)

Super Retail Group downgraded to hold from accumulate, target nudged up to $12.90 from $12.67 (Morgans)

Bapcor downgraded to trim from hold, target slashed to $0.61 from $1.41 (Morgans)

Collins Foods initiated at buy with a $10.80 target (Bell Potter)

Domino's Pizza initiated at hold with an $18.00 target (Bell Potter)

Guzman y Gomez initiated at hold with a $22.10 target (Bell Potter)

Challenger 3Q26 update: Annuity momentum solid but funds management under pressure

[9:41 am] Challenger delivered strong annuity sales growth in Q3 but saw a sharp drop in FUM driven by institutional equity outflows and market weakness, while EPS guidance was tightened at the top end.

Total Life sales of $1.72bn, down from $2.60bn last quarter but up 19% year-on-year

Annuity net book growth of $274m or 1.7% for the quarter, supported by higher sales and a moderating maturity rate of 4% of opening annuity liabilities

Funds Management FUM down 10% to $104.5bn from $116.2bn last quarter, driven by net outflows of $8.0bn (predominantly $7.3bn from institutional equity strategies at Fidante), $3.4bn in negative market movements and $0.3bn in client distributions

Total AUM fell to $116.3bn from $128.2bn last quarter

FY26 normalised basic EPS guidance tightened to $0.66-0.70 vs. prior guidance of $0.66-0.72, sitting above the midpoint of ests at $0.65

Company page: Challenger (CGF)

West African Resources to sell 25% Kiaka stake to Burkina Faso government

[9:36 am] A government decree has formalised the compulsory acquisition of a 25% interest in WAF's Kiaka gold operation, with proceeds to be returned to shareholders via a special dividend.

The Burkina Faso government has published a decree authorising state mining vehicle SOPAMIB to acquire an additional 25% equity interest in Kiaka SA, valued ~A$175m

WAF plans to distribute the full cash proceeds from the 25% stake sale to shareholders via a special dividend

WAF's Sanbrado and Toega operations are explicitly excluded from the decree and are not subject to any additional government participation request

From a valuation standpoint, this is straight up robbery, valuing Kiaka at A$700 million on a 100% basis. Here's some perspective as to why:

A July 2024 feasibility study for Kiaka noted post-tax NPV of US$1.18bn (A$1.8bn) at an assumed gold price of US$2,100/oz

Kiaka recently entered into production. In the first five months of operational ramp up, it generated A$445 million of revenue at an average realised price of US$3,850/oz

Macquarie modelling (Nov-25) values Kiaka at A$1.72bn

Company page: West African Resources (WAF)

Rio Tinto's take on commodity markets

[9:27 am] Rio's market commentary points to a broadly constructive commodity backdrop, with the Middle East conflict creating meaningful supply disruptions that are net positive for several of Rio's key exposures.

Iron ore fundamentals are mixed: China Q1 crude steel and pig iron production fell 1% year-on-year, steel exports dropped 10% partly due to new licensing rules, and seaborne supply was constrained by cyclones in Australia and heavy rain in Brazil, with major producer shipments down 17% quarter-on-quarter. Higher energy costs are lifting the global cost curve, favouring lower-cost producers like Rio

Copper hit a record high of US$6.28/lb in late January before pulling back to US$5.52/lb at quarter end amid Middle East-driven risk-off, recovering to US$6.00/lb by mid-April. The concentrate market is extremely tight with spot treatment and refining charges at a record low of -$95/t, a strong signal for miners

Aluminium is the standout beneficiary of the Middle East conflict, with smelter curtailments in a region accounting for 23% of ex-China production driving expectations of an enhanced global deficit in 2026. The US Midwest duty-paid premium hit a record high of US$2,523/t and LME prices reached near four-year highs in March

Lithium carbonate prices continued to rally in Q1 on expectations of market tightness, driven by strong BESS demand, Chinese mine curtailments and Zimbabwean export restrictions, though global EV sales were down 8% year-on-year to February following policy pullbacks in China and the US

China's economy re-accelerated to 5% real GDP growth in Q1 from 4.5% in Q4 2025, with its high reliance on coal, renewables and substantial oil stockpiles limiting the impact of higher global energy prices, providing a relatively resilient demand backdrop for Rio's commodities

Company page: Rio Tinto (RIO)

Rio Tinto 1Q26: Strong operational performance despite cyclone disruption

[9:24 am] Rio delivered solid production growth across its copper and iron ore assets, though Pilbara shipments were impacted by two cyclones in the quarter.

Copper production up 9% year-on-year driven by the continued ramp-up of Oyu Tolgoi, with drilling now underway at Resolution Copper following completion of the historic land exchange in March

Pilbara iron ore production was the second highest Q1 since 2018, up 13% year-on-year, though shipments were impacted by approximately 8Mt from two tropical cyclones

First Simandou high-grade shipment successfully delivered to China with first sales realised in April

Aluminium delivered another strong quarter with the integrated value chain offsetting weather-related bauxite disruptions, while lithium assets Fenix 1B and Sal de Vida reached mechanical completion with first production on track for H2 2026

The $650m annualised productivity benefits program is now fully implemented as promised, with further initiatives underway targeting throughput, operating costs and central costs beyond the initial target

Middle East conflict has had limited direct operational impact to date, with commodity prices responding favourably

Rio flagged relatively limited visibility on supply chain impacts in H2, and notes higher diesel costs (consuming around 1.6bn litres annually, two-thirds in the Pilbara) are steepening the cost curve

Company page: Rio Tinto (RIO)

Australian Clinical Labs hit with class action over 2022 Medlab cyberattack

[9:19 am] A representative proceeding has been filed in the Supreme Court of Victoria against ACL relating to a data breach that occurred over three years ago.

The class action, filed by Michelle Raab-Ivanov, covers customers of Medlab Pathology and ACL whose personal information was affected by a cyberattack on Medlab Pathology in February 2022

Claims are brought on the basis of alleged breaches of the Australian Consumer Law (s60), duty of care and equitable duty, though no quantum of damages has been specified

ACL has denied the alleged breaches and says it intends to vigorously defend the claim

Company page: Australian Clinical Labs (ACL)

Hub24 delivers record March quarter inflows

[9:18 am] Hub24 posted strong Q3 FY26 platform flows despite negative market movements.

Platform net inflows up 9% to $4.0bn (ex-large migrations), a record March quarter, with retail flows strong despite a one-off institutional client outflow in March

Total FUA up 22% on pcp to $151.7bn, with platform FUA broadly stable over the quarter as $4.0bn in net inflows was offset by $4.1bn in negative market movements

Hub24 ranked first for both quarterly and annual net inflows for a ninth consecutive quarter, and achieved the largest quarterly and annual market share gains of all platform providers, with market share rising to 9.7% from 8.3% in the pcp

I don't have any quarterly consensus data handy. While total FUA is up strongly year-on-year, it's actually down 0.3% quarter-on-quarter ($151.7bn vs. $152.3bn a quarter ago), though largely attributed to negative market movements. Inflows for the March quarter ($4.0bn) still down vs. the $5.6 billion in the December quarter.

Company page: HUB24 (HUB)

BHP reviewing Queensland coal asset

[9:07 am] BHP and Mitsubishi Development are conducting a formal ranking of their Queensland coal mines by financial health, according to Bloomberg.

The 50:50 BHP Mitsubishi Alliance is ranking each underground and open-cut mine by costs and financial health. The process is not public, per sources within the joint venture

BHP's share of Queensland coal JV production was 9.2Mt in the six months to 31 December 2025, with the mines returning zero profit to BHP over that period, per the company's half-year report

BHP Chairman Ross McEwen declared "zero" new capital investment across the Queensland coal business at a Sydney conference last month, and an internal email seen by Bloomberg warned staff the mines were unprofitable

Queensland's royalty regime remains the central grievance. The tiered system introduced in 2022 takes 30% of revenue on coal sold above $225/t and up to 40% above $300/t, levied on revenue rather than profit

BHP closed its Saraji South mine and cut roughly 750 jobs in September 2024, citing high royalties and weak market conditions

Source: Bloomberg

Yancoal 1Q26 production update: Volumes and prices soft amid rising cost pressures

[9:04 am] Yancoal delivered a modest decline in production and realised prices in Q1, with full-year guidance retained but diesel-driven cost pressures flagged as a risk to the top end of the cost range.

Attributable saleable coal production down 5% to 9.0Mt

ROM coal production (100% basis) down 1% 15.0Mt

Average realised coal price down 7% to $146/t

FY26 guidance unchanged, including attributable saleable production of 36.5-40.5Mt, cash operating costs of $90-98/t and capex of $750-900m

Higher diesel prices (~$7/t of direct mining costs) are expected to push costs toward the top end of the range

Seaborne coal market dynamics are mixed

Gas-to-coal switching is a potential tailwind as Middle East LNG supply disruption drives Japan, South Korea and Taiwan to ease restrictions on coal-fired generation

High post-winter stockpiles in those countries are tempering near-term demand

China and India, the two largest importers, reduced imports by 5% and 12% respectively in Q1 due to elevated domestic stockpiles

Cash balance of $2.01bn at 31 March 2026

Company page: Yancoal Australia (YAL)

China's iron ore port stocks fall to near three-month low

[9:01 am] Port inventories are tightening as outflows accelerate and shipment arrivals drop sharply, though stocks remain well above year-ago levels, according to Mysteel.

Total iron ore stocks at China's 47 major ports fell 2.28 million tonnes (1.3%) week-on-week to 174.65 million tonnes as of 16 April, nearing a three-month low, per Mysteel. Though inventories remain 20% above the same period last year

The drawdown was driven by a combination of rising outflows and falling inflows. Daily outflows across the sampled ports rose 64,800 tonnes/day (2%) to an average of 3.36 million tonnes/day during 9-15 April

Australian and Brazilian-origin stocks both declined over the period, with Brazilian ore falling to its lowest level in over a year

Source: Mysteel

Refinery fires mount globally

[8:57 am] A string of oil and gas infrastructure incidents across four countries in less than a week is drawing attention, though the causes appear to vary significantly.

A major blaze has broken out at HPCL's Rajasthan refinery in India, marking the fourth significant oil and gas infrastructure incident in five days globally

The cluster of incidents spans Australia (Viva Energy's Geelong refinery fire, 15 April), Pakistan (deadly gas pipeline explosion in Haripur killing eight, 16 April), Russia (drone strikes on the Novokuybyshevsk and Syzran refineries, 18 April) and now India

The Russian incidents are attributable to Ukrainian drone strikes

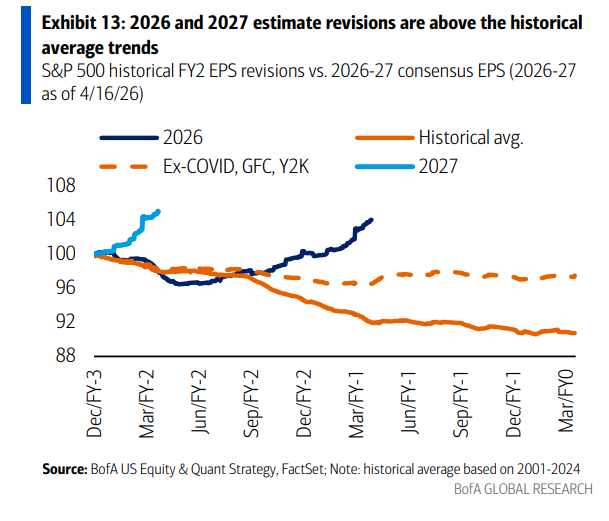

Nvidia carrying the S&P 500 earnings revisions

[8:54 am] S&P 500 EPS estimates for 2026 and 2027 continue to climb higher, bucking a long-term trend of downward revisions throughout the year, according to BofA.

However, strip out Nvidia and the rest of the Mag 7 are actually lagging the broader S&P 500 on earnings growth.

Mag 7 Q1 2026 earnings growth is estimated at 22.8% year-on-year, well above the 10.1% for the remaining 493 S&P 500 companies, but strip out Nvidia and that figure collapses to just 6.4%, meaning the other 493 companies are outgrowing the rest of the Mag 7

After Nvidia, the next largest contributors to S&P 500 earnings growth in Q1 2026 are Micron, Eli Lilly, Broadcom and Sandisk

US tariff refund portal opens amid scepticism and legal risk

[8:51 am] Over $160 billion in tariff refunds are now claimable following a Supreme Court ruling, but importers and trade lawyers expect the process to be slow, complex and legally fraught.

The Trump administration launched the CAPE portal , through which importers can file claims for tariffs paid under the now-invalidated emergency tariff authority, with CBP promising a single consolidated refund amount

Citi estimates Walmart is owed $10.2bn, Target $2.2bn, Nike $1bn, Home Depot $540m, Kohl's $550m and Gap $400m, though Wall Street is not expected to build refunds into forward guidance given timing uncertainty

Walmart CFO John David Rainey flagged the process will likely be slow and complex, but confirmed refunds would be recognised as a P&L benefit if and when received

A separate legal risk exists for companies that passed tariff costs through to customers, who could face lawsuits from direct or indirect customers if they collect refunds

Source: CNBC

Apple names John Ternus as next CEO, replacing Tim Cook

[8:46 am] Tim Cook will step down on 1 September after 15 years, handing the reins to hardware chief John Ternus as Apple looks to close the gap on AI rivals.

Ternus, 50, becomes CEO on 1 September with Cook transitioning to executive chairman, where he will focus on government and policy engagement globally

Ternus has spent 25 years at Apple leading hardware development across iPhone, iPad, AirPods, Mac and Apple Silicon, and has been hardware engineering chief since 2021

His appointment comes at a key moment as Apple has lagged behind OpenAI, Google and Anthropic in AI, with Cook's tenure marked by missed opportunities in the space

Ternus is a strong AI believer and recently reorganised the hardware engineering division around an AI platform

Source: Bloomberg

Trump "highly unlikely" to extend ceasefire

[8:44 am] The two-week ceasefire expires on Thursday, as Trump rules out an extension and both sides manoeuvre for leverage.

Trump confirmed the ceasefire expires "Wednesday evening Washington time" and described an extension as "highly unlikely," with VP Vance, Jared Kushner and Steve Witkoff heading to Pakistan for a second round of talks

Hardline IRGC figures pushing for a tough stance while more pragmatic leaders including President Pezeshkian and Foreign Minister Araghchi are seen as more open to a deal

Despite the standoff, US and Iranian officials reportedly still see a reasonable chance of an agreement within days

Trump has demanded Iran relinquish enriched uranium stockpiles and abandon any weapons ambitions, while Tehran insists its programme is for peaceful purposes and has resisted surrendering its uranium

Earnings beats failing to move stocks as macro noise dominates

[8:42 am] Despite a solid start to Q1 earnings season, share price reactions to beats are running well below historical norms as geopolitics and macro uncertainty crowd out the micro.

Of the 28 S&P 500 companies that have beaten both earnings and sales estimates so far, shares have outperformed the index by just 0.85% on average post-result

This marks the weakest reaction since early last year and below the long-run average of 1.2%, per Bloomberg Intelligence

BofA's Savita Subramanian notes that solid Q1 results alone are proving insufficient, with large geopolitical moves swamping earnings reactions and guidance taking on greater importance than usual

Wells Fargo's Sameer Samana points out that prices had run up sharply before the big banks even reported, compressing the scope for positive surprises to drive further upside

Red flags are emerging beneath the surface, as the share of S&P 500 companies lowering their forward guidance has hit the highest level since Q2 last year, per Bloomberg Intelligence

Source: Bloomberg

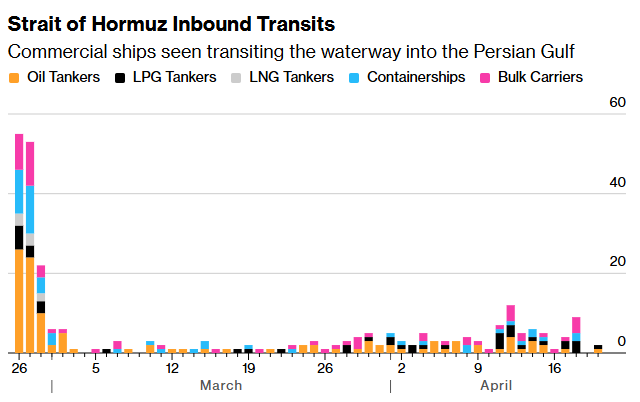

Strait of Hormuz traffic: Back to zero

[8:40 am] A nice chart from Bloomberg showing tariff through the Strait has dropped to near zero amid ongoing US-Iran tensions.

Source: Bloomberg

US market drivers: Geopolitics, earnings and systematic flows

[8:38 am] Markets face a mixed backdrop this week as geopolitical risk, technical buying support and a ramping earnings season pull in different directions.

US-Iran tensions have re-escalated over the weekend, effectively closing the Strait of Hormuz, though equity markets appear relatively composed. This is consistent with the recent pattern of escalate-to-de-escalate dynamics and the market's historical tendency to look through geopolitical noise

Systematic strategy flows remain a key mechanical tailwind, with Goldman Sachs estimating CTAs are now net long $10bn in S&P 500 after buying $33bn last week, with a further $23bn of expected buying this week. Meanwhile BofA puts total systematic demand at $40-55bn in a flat-to-up tape

Q1 earnings season accelerates with roughly 20% of the S&P 500 reporting this week. Early reads have been broadly positive, particularly macro and consumer commentary from the major banks, though softer guidance and narrow breadth behind upward estimate revisions are worth watching

US-Iran tensions linger as ceasefire deadline looms

[8:37 am] Weekend developments have left the situation murky, with Friday's optimism fading amid renewed hostilities and diplomatic uncertainty.

Friday headlines on a potential nuclear deal and reopening of the Strait of Hormuz have faded, with Hormuz traffic back to a virtual standstill

Trump accused Tehran of ceasefire violations and renewed threats to target Iran's power plants and bridges, while the US navy disabled and seized an Iranian-flagged cargo ship in the Gulf of Oman, with Iran vowing retaliation

Vance, Witkoff and Kushner dispatched to Islamabad for another round of talks, with the current ceasefire set to lapse tomorrow barring new developments

Equity downside has been limited, with the narrative that both sides are seeking off-ramps holding despite an extended and bumpy process

Good morning!

[8:30 am] ASX 200 futures are up 48 pts (+0.53%) as of 8:30 am AEST.

US indices mostly lower, but off worst levels

S&P 500 (-0.24%) bounced off session lows of -0.58%, this follows a historic 12.3% rally in 13 days (the second fastest rebound rally since 1950)

Nasdaq snapped a 13-day win streak, which was the longest stretch of gains since 1992

A relatively uneventful and cautious session as US-Iran tensions ratcheted back up over the weekend, offset by mechanical support from systematic strategies, solid Q1 earnings and a pickup in M&A activity

Apple CEO Tim Cook to step down after 15-year tenure, John Ternus named as incoming CEO