News | Market Wraps

Evening Wrap: ASX 200 rally gathers pace on massive Mineral Resources rally, uranium stocks melt-up continues

The S&P/ASX 200 closed 73.5 points higher, up 0.92%.

Mentioned

The S&P/ASX 200 closed 73.5 points higher, up 0.92%.

Notch up another scintillating day of gains for the ASX 200 – and another day where the nerve-racking events of Liberation Day seem to be but a distant memory. You gotta love markets. Panic. Forget. Rally. Repeat!

Talking about P.F.R.R., uranium and ASX uranium stocks have both been doing quite a bit of it lately. Heroes at the start of 2024, to zeroes just a couple of weeks ago – to heroes again! The uranium price is rallying – we flagged it here in ChartWatch at nearly the exact low of ASX U-stocks’ doldrums – plus you would also know from reading our Wrap that Sprott Inc. has been buying the dip.

Add in a better-than-expected quarterly update from Boss Energy (BOE) (+14.3%) today, and it was rocket ship emojis under the entire ASX U-sector 🚀!

Also rising like a phoenix from the ashes, was dog of 2024 Minerals Resources (MIN) (+13.1%). Every dog has its day, and today MIN shares saw plenty of bargain hunting – as well as quite likely a great deal of short covering – after it also released a better-than-expected quarterly report.

The abovementioned results from BOE and MIN helped drive Energy (XEJ) (+2.5%) and Resources (XJR) (+1.7%) towards the top of the sector leaderboard, but the love was widely spread as Information Technology (XIJ) (+1.5%) and Real Estate (XPJ) (+1.1%) also shared in the gains.

Gold bugs were really the only group of investors to be disappointed, as the Gold sub-index (XGD) (-0.17%) dipped – but most of that was due to a poorly received quarterly report from major constituent Northern Star Resources (NST) (-4.7%).

To make sense of all the above, I have detailed technical analysis on the Nasdaq Composite, S&P/ASX 200, and US Bonds in today's ChartWatch.

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key upcoming economic data in tonight's Evening Wrap.

Let's dive in!

Today in Review

Tue 29 Apr 25, 5:15pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,070.6 | +0.92% |

| All Ords | 8,287.9 | +1.02% |

| Small Ords | 3,054.3 | +2.09% |

| All Tech | 3,496.7 | +1.60% |

| Emerging Companies | 2,229.3 | +1.10% |

Currency | ||

| AUD/USD | 0.643 | 0.00% |

US Futures | ||

| S&P 500 | 5,557.25 | +0.08% |

| Dow Jones | 40,393.0 | +0.06% |

| Nasdaq | 19,549.0 | +0.11% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Energy | 7,364.8 | +2.46% |

| Utilities | 9,372.3 | +2.29% |

| Information Technology | 2,365.3 | +1.45% |

| Materials | 16,155.5 | +1.43% |

| Real Estate | 3,632.3 | +1.11% |

| Industrials | 7,879.9 | +0.91% |

| Consumer Discretionary | 3,944.3 | +0.80% |

| Communication Services | 1,723.8 | +0.67% |

| Health Care | 40,856.5 | +0.61% |

| Financials | 8,694.2 | +0.60% |

| Consumer Staples | 12,308.0 | -0.03% |

Markets

%20intraday%20chart%2029%20April%202025.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 73.5 points higher at 8,070.6, 0.92% from its session high and just 0.08% from its low. In the broader-based S&P/ASX 300 (XKO), advancers beat decliners by an emphatic 247 to 31.

We’ve often discussed the concept of a “new normal” in this Wrap over the last couple of months since President Trump began pulling the levers on US trade and broader US economic policy. At times, it’s felt like there’s been a new “new normal” every few days.

In the beginning, markets tanked. More recently, markets have largely recovered (on a total return basis, i.e., adding back dividends, at today’s close the S&P/ASX 200 is about 4.6% away from the all-time high – and some 10.0% above its correction low).

Here’s my take on the latest new normal (i.e., markets now believe):

Calmer heads will prevail. Deals on trade / tariffs will be done and a crisis will be averted. President Trump (or at least his advisors) understand that sudden, unflagged (in terms of size) policy actions have impacts on markets – and those impacts can at times be too important and dangerous to be ignored – so we shouldn’t get any more.

If you believe this, and the net effect of the stuff El Presidente has done so far will amount to no more than 4.6% worth of damage to Australian stocks (putting aside all other factors) – then you agree that the recent rally is about right.

If you don’t, and you think the impact will likely be greater, then you’re probably not #YOLOing or #FOMOing into this rally just yet. Perhaps even, you might be thinking about using this rally to convert a little bit of risk into cash if you feel you missed your chance to do so on the way down.

I’m not your financial advisor, so I have absolutely no business telling you what you should do. I am simply pointing out the logical alternatives.

As a technical analyst, personally I must believe the excess demand that’s created this rally is being driven by fully informed and rational investors. Professionals that have assessed the risks, assessed the prices of various assets, and have shifted their demand and supply accordingly to properly balance each.

I must assume that ultimately, these investors wish to make foolish decisions with their capital as little as we endeavour do.

So, why am I finding it just a little difficult to believe this rally? 🤔

Ha! To the charts we go…🏃➡️

ChartWatch

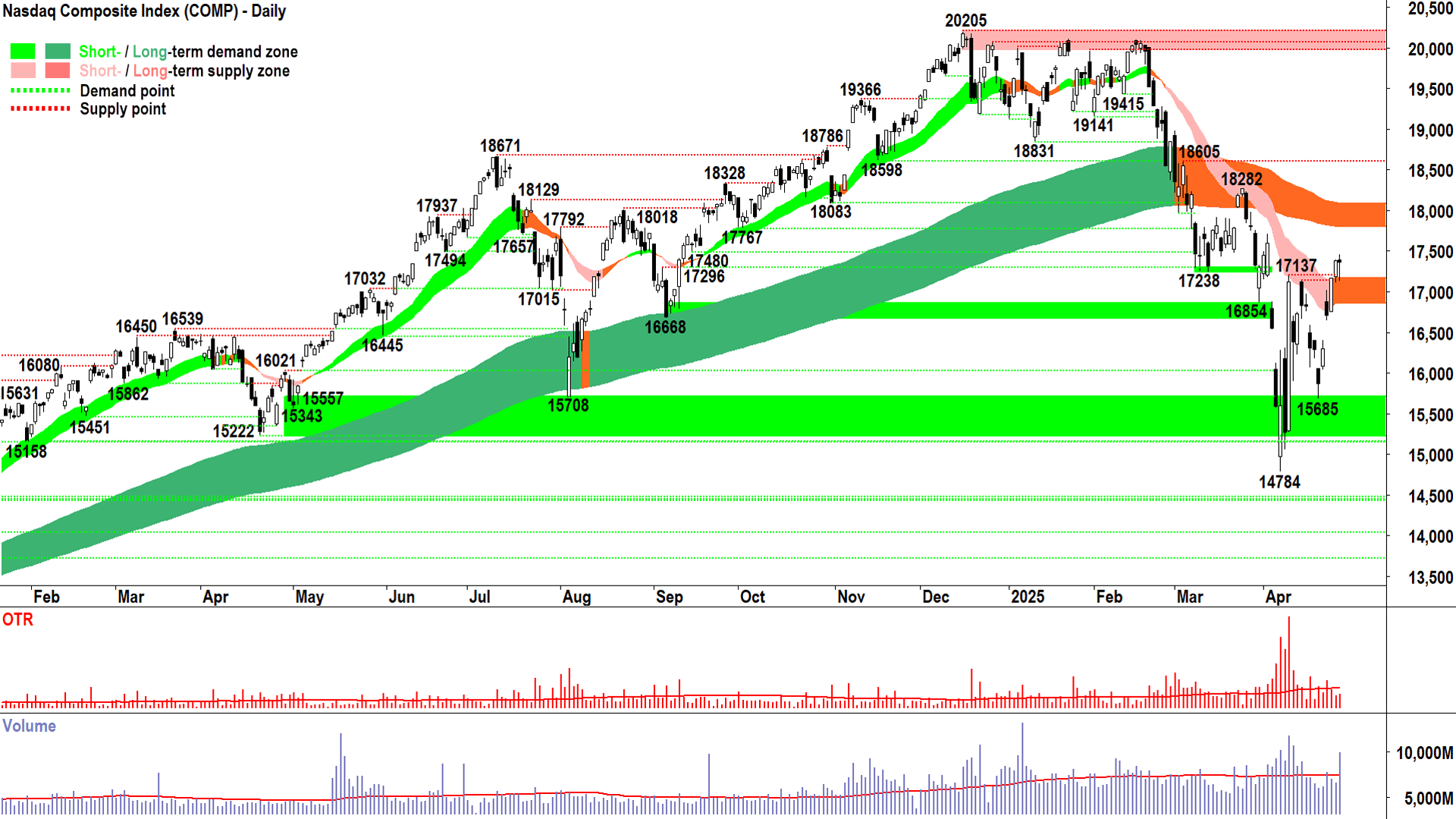

NASDAQ Composite Index

You must do the work! 🔨 (click here for full size image)

{kind=link}

I trust you’ll agree that I haven’t let any scepticism of my interpretation of the macro narrative to impact my technical calls.

Nothing is as pure as trends, price action and candles. Demand versus supply.

Whether you agree with it or not!

So, let’s do the work. Let's start from the top and work our way down to a granular level.

1. Trends – What do we know?

Short term trend is neutral – telling us there’s roughly a balance between demand and supply-side control among traders. The price has closed back above the short term trend ribbon, perhaps the demand-side have a slight edge in the short term.

Long term trend is neutral – telling us there’s also roughly a balance between demand and supply-side control among long term investors. The price remains below the long term trend ribbon, perhaps the supply-side have a slight edge in the long term.

Conclusion from Trends: The market is unable to make any clear decision one way or the other about being invested or being in cash. Equilibrium smacks of indecision = Stay out / run with moderate risk-exposure levels. A close above, test, and then hold of the long term trend ribbon will confirm a new long term uptrend phase has begun – it’s potentially not very far away in terms of price and time – perhaps the best course of action is to simply wait for that.

2. Price Action – What do we know?

In the short term, we observe rising peaks and rising troughs – this is indicative of supply removal and demand reinforcement, respectively. Traders appear to be moving back into the market.

In the longer term, it's disturbing the last major low at 14784 took out major lows at 15708 and 15222. Ultimately, until the price closes above 20205, some degree of doubt must remain.

Conclusion from Price Action: The structure of the recent rally from 14784 is consistent with major bear market lows of the past, particularly when considering volume and volatility. It is a credible reversal that should not be discounted easily. Perhaps a close back above 18282 will provide even greater confidence – and by then the all important close back above the long term trend ribbon also.

3. Candles – What do we know?

These are only short term tools, but since the massive “reciprocal” tariff about-face candle of 9 April – there has been in my opinion a credible predominance of demand-side candles (i.e., white-bodied and or downward pointing shadows). Including even last night’s candle – sure, far from perfect – but still demonstrative of buy the dip activity.

Conclusion from Candles: There is a credible short term rally underway that (again) should not be discounted easily.

Conclusions from the technicals

Pretty much the same as I’ve said here before. Cautiously optimistic but still operating at reduced risk-exposure levels until longer term confirmation signals are confirmed (e.g., long term trend ribbon requirement / 18282 point of supply dealt with). I'm open to adding risk on a case-by-case basis – but only on optimal trends – possibly using short exposure to hedge out at some of this new risk.

That’s a bit of work, I trust, however, it was worthwhile! Now consider whether this is the type of work you could be doing regularly with your portfolio. Would it be worthwhile?

Also consider that every stock in your portfolio probably should be held to this degree of scrutiny as well! 🔬

It’s up to you, of course – but as with anything in life – you must put the effort into your investing if you want the best results!

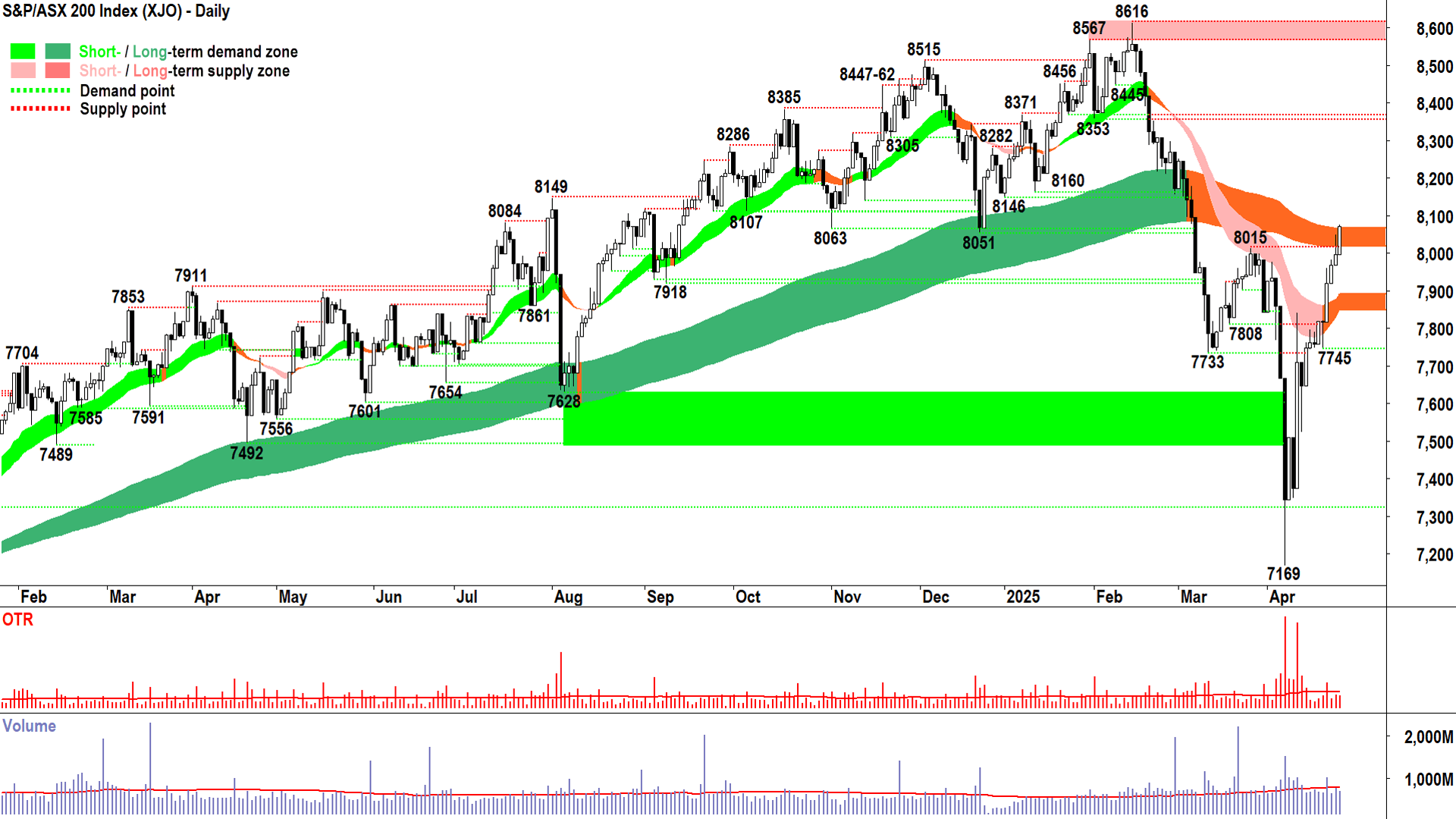

S&P/ASX 200 (XJO)

%20chart%2029%20April%202025.png)

Potentially not long now… (click here for full size image)

{kind=link}

I won’t redo the above analysis here – I invite you to do it in your own time though. I think we can agree it will be similar, but perhaps (and this might be surprising for many), the old ASX 200 is in better shape than many global stock indices.

For example, the interaction with the long term trend ribbon began today – and looking at today’s strong demand-side candle, it appears to have played out very well indeed. No discernible evidence of excess supply at the long term trend ribbon = ✅.

Add in, today's candle sliced straight through what could have been (should have been?) a significant pressure point of supply at 8015.

In short: The price action and candles show a decisive wall of excess demand since the 7169 low. It has been one-way traffic for Aussie stocks – a wall of demand and a vacuum of supply. We went from everyone wanting out, to everyone hanging in.

And as long as it stays that way, who are we to not sit back and simply enjoy the ride? 🤷

But, as we must do so…with our seatbelts firmly engaged…and on the lookout for potential potholes…e.g., nasty big black candles, or those with long upward pointing shadows (demonstrating the sell the rally switch has been flicked).

8353 is the next major point of supply versus the short term trend ribbon (kicking in around 7890) is now the key zone of demand.

A close above, test, and then hold of the long term trend ribbon will confirm a new long term uptrend phase has begun. Potentially not long to go now…

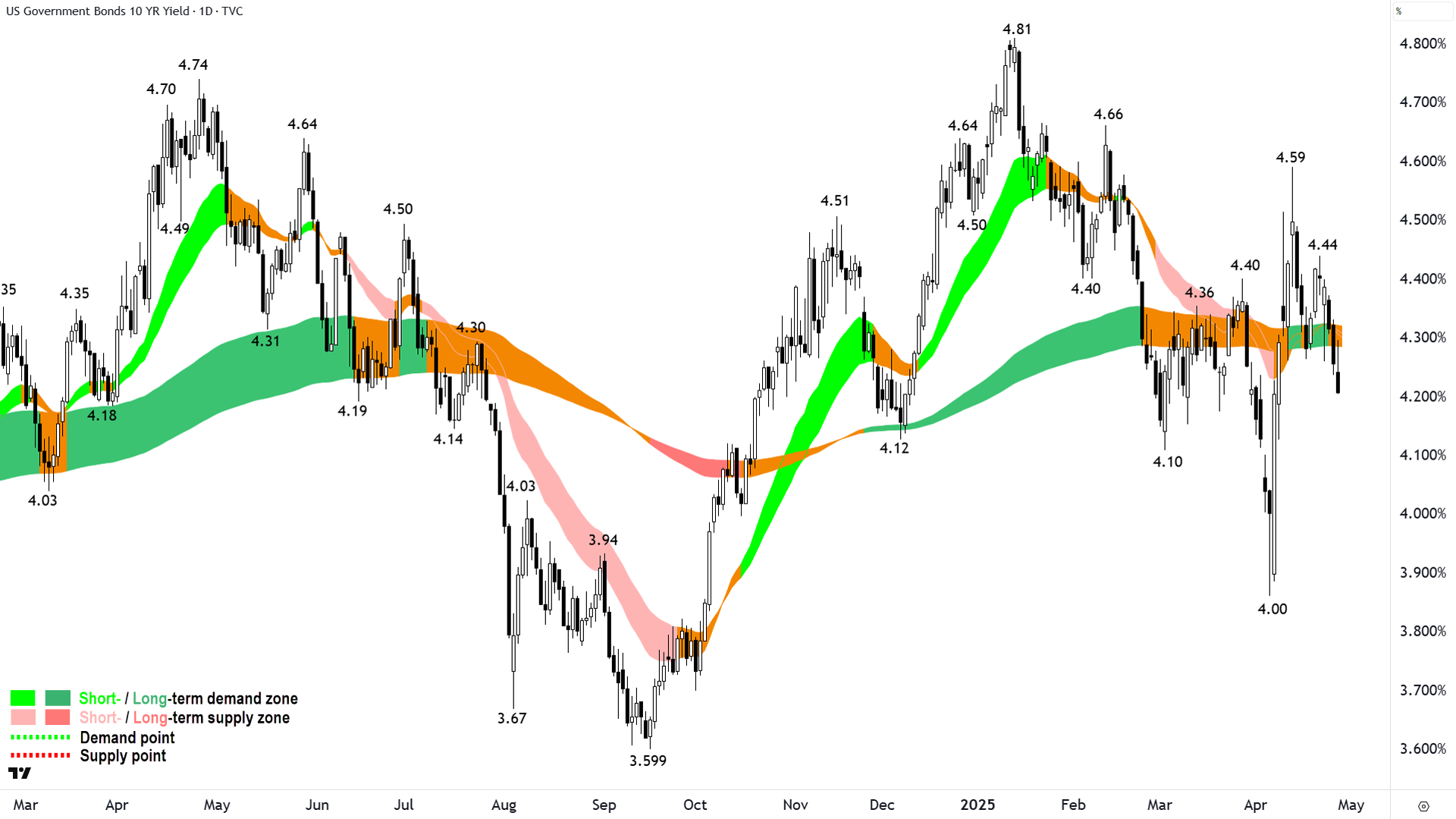

US 10 Year T-Bond Yield

Just keep an eye on this one...👀 (click here for full size image)

{kind=link}

Just keep an eye on this one. Yes, US risk-free yields fell last night – consistent with the narrative that the US bond market is stepping back from the ledge...improvement of the global view that US treasuries remain the global risk-free asset of choice, etc.

But there will come a point where a decline in this chart won't be cheered by markets – but rather it will begin to set off alarm bells again 🚨.

A rapid / steep decline here, punctuated by long black candles would likely indicate that traders are now assessing a substantial negative impact to the US economy as a result of President Trump's trade policies implemented so far. Basically, that a US recession is inevitable – if not already started – and lower official rates will be required to stem the damage.

We're not there yet – a gradual decline here is A-OK. But just keep an eye out. There's all sorts of talk about shortages of goods on US retailers shelves already, shipping getting cancelled between the US and China, and of bankruptcies among various transport companies. Possibly just bearish chatter as bears like to spread!

But we can rest assured – as always – the bond market will tell us what's what! 💪

Economy

Today

There weren't any major data releases in our time zone today

Later this week

Tuesday

22:00 USA JOLTS Job Openings March (7.48 million forecast vs 7.57 million previous)

22:00 USA Conference Board Consumer Confidence April (87.4 forecast to 92.9 previous)

Wednesday

09:30 Consumer Price Index (CPI) March Quarter (+0.8% q/q and +2.3% p.a. forecast vs +0.2% q/q and +2.4% p.a. previous)

09:30 Consumer Price Index (CPI) Trimmed Mean March Quarter (+0.6% q/q and +2.8% p.a. forecast vs +0.5% q/q and +3.2% p.a. previous)

09:30 CHN Manufacturing & Non-Manufacturing Purchasing Managers Index (PMI) April

Manufacturing: 49.8 forecast vs 50.5 in March

Non-Manufacturing: 50.7 forecast vs 51.2 in March

20:15 USA Advance GDP March y/y (+0.4% p.a. vs +2.4% p.a.)

22:00 USA Core Personal Consumption Expenditures (PCE) Price Index March (+0.1% m/m and +2.6% p.a. vs +0.4% m/m and +2.8% p.a. in February)

Personal Income m/m: +0.4% forecast vs +0.% in February

Personal Spending m/m: +0.6% forecast vs +0.4% in February

Thursday

ALL DAY CHN May Day Bank Holiday

TBA JPN Bank of Japan (BOJ) Policy Rate, Monetary Policy Statement, Outlook Report & Press Conference

22:00 USA ISM Manufacturing PMI April (48.0 forecast vs 49.0 in March)

Friday

ALL DAY CHN May Day Bank Holiday

09:30 Retail Sales m/m March (+0.4% forecast and +0.2% in February)

20:30 Non-Farm Employment Data April

Employment Change m/m: +129,000 forecast vs +228,000 in March

Average Hourly Earnings m/m: +0.3% forecast vs +0.3% in March

Unemployment Rate: 4.2% forecast vs 4.2% in March

Saturday

ALL DAY AUS Parliamentary Elections (forecast 🤔???)

Latest News

Interesting Movers

Trading higher

+14.3% Boss Energy (BOE) – March Quarterly Activities Report, general strength across the broader Uranium sector today, (but probably at least some impact from the recent recovery in the uranium price as per reported in ChartWatch since last week!).

+13.3% Develop Global (DVP) – No news since 28-Apr Quarterly Activities Report, also retained at buy by Bell Potter and Canaccord Genuity today (see Broker Moves for more details).

+13.1% Mineral Resources (MIN) – Quarterly Activity Report - Q3 FY25, general strength across the broader Lithium sector today, (hmmm...how much was short covering and how much was positional buying – and does it matter!? 🤔).

+12.1% Lotus Resources (LOT) – No news, general strength across the broader Uranium sector today, (ditto likely positive impact from improving uranium price).

+11.9% Bannerman Energy (BMN) – No news, general strength across the broader Uranium sector today, (ditto likely positive impact from improving uranium price).

+11.7% Deep Yellow (DYL) – No news, general strength across the broader Uranium sector today, (ditto likely positive impact from improving uranium price).

+8.9% Nexgen Energy (NXG) – No news, general strength across the broader Uranium sector today, (ditto likely positive impact from improving uranium price).

+8.7% Silex Systems (SLX) – No news, general strength across the broader Uranium sector today, (ditto likely positive impact from improving uranium price).

+8.6% Botanix Pharmaceuticals (BOT) – No news, rise is consistent with prevailing long term uptrend 🔎📈

+8.5% Paladin Energy (PDN) – No news, general strength across the broader Uranium sector today, (ditto likely positive impact from improving uranium price).

+8.3% Alkane Resources (ALK) – March Quarterly Activities Report, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+7.1% Adriatic Metals (ADT) – No news 🤔.

+6.9% Meeka Metals (MEK) – No news since 28-Apr March 2025 Quarterly Activities Report and March 2025 Quarterly Cashflow Report.

+6.8% Weebit Nano (WBT) – No news, general strength across the broader Information Technology sector today.

+6.8% Droneshield (DRO) – No news, rise is consistent with prevailing short term uptrend and long term trend is transitioning from down to up, a recent regular in ChartWatch ASX Scans Uptrends list 🔎

Trading lower

-12.9% 29METALS (29M) – March 2025 Quarterly Report - Investor Presentation, fall is consistent with prevailing short and long term downtrends, one of the most Featured (highest conviction) stocks in ChartWatch ASX Scans Downtrends list 🔎📉

-4.7% Northern Star Resources (NST) – March 2025 Quarterly Activities Report.

-4.0% Auckland International Airport (AIA) – AIA releases long-term blueprint for the future.

-2.8% Catalyst Metals (CYL) – Quarterly activities report.

-2.3% BetaShares Australian Strong Bear ETF (BBO) – No news, short ASX equities ETF.

-1.8% Brainchip (BRN) – Appendix 4C and Quarterly Activities Report.

Broker Moves

29METALS (29M)

Retained at equal-weight at Morgan Stanley; Price Target: $0.130

Aeris Resources (AIS)

Retained at outperform at Macquarie; Price Target: $0.280

Retained at hold at Ord Minnett; Price Target: $0.250 from $0.280

ALS (ALQ)

Retained at neutral at Jarden; Price Target: $14.50 from $14.40

Retained at buy at Jefferies; Price Target: $18.80 from $17.70

Retained at overweight at JP Morgan; Price Target: $17.20 from $16.50

Retained at outperform at Macquarie; Price Target: $17.30 from $16.25

Retained at accumulate at Ord Minnett; Price Target: $17.25 from $16.05

Retained at buy at UBS; Price Target: $18.70 from $17.50

Amcor (AMC)

Upgraded at equal-weight at Morgan Stanley; Price Target: $20.31 from $16.00

Retained at neutral at UBS; Price Target: $16.90

AMP (AMP)

Retained at hold at Ord Minnett; Price Target: $1.520

ANZ Group (ANZ)

Retained at equal-weight at Morgan Stanley; Price Target: $29.30

Abacus Storage King (ASK)

Retained at buy at Citi; Price Target: $1.400

ASX (ASX)

Retained at neutral at Macquarie; Price Target: $65.00

Adveritas (AV1)

Retained at buy at Bell Potter; Price Target: $0.140 from $0.120

Bapcor (BAP)

Retained at neutral at Citi; Price Target: $5.64

Retained at outperform at CLSA; Price Target: $5.65

Retained at buy at Jefferies; Price Target: $5.90

Retained at outperform at Macquarie; Price Target: $5.85

Retained at hold at Ord Minnett; Price Target: $5.30

Biome Australia (BIO)

Retained at buy at Bell Potter; Price Target: $0.850

Bubs Australia (BUB)

Retained at hold at Bell Potter; Price Target: $0.145 from $0.155

Brambles (BXB)

Retained at neutral at Citi; Price Target: $20.15

Retained at outperform at CLSA; Price Target: $22.30

Retained at positive at E&P; Price Target: $22.07 from $22.27

Retained at hold at Jefferies; Price Target: $17.93 from $17.75

Retained at outperform at Macquarie; Price Target: $21.85

Retained at overweight at Morgan Stanley; Price Target: $22.00

Retained at hold at Morgans; Price Target: $19.75 from $20.50

Retained at buy at Ord Minnett; Price Target: $24.90 from $23.80

Retained at buy at UBS; Price Target: $23.00 from $22.80

Commonwealth Bank of Australia (CBA)

Retained at underweight at Morgan Stanley; Price Target: $128.00

Collins Foods (CKF)

Retained at neutral at Macquarie; Price Target: $8.20

Coles Group (COL)

Retained at outperform at Macquarie; Price Target: $22.00

Domino's Pizza Enterprises (DMP)

Retained at neutral at Macquarie; Price Target: $30.50

Develop Global (DVP)

Retained at buy at Bell Potter; Price Target: $4.00

Retained at buy at Canaccord Genuity; Price Target: $5.05 from $4.80

Endeavour Group (EDV)

Retained at neutral at Macquarie; Price Target: $4.10

Fletcher Building (FBU)

Retained at underperform at Macquarie; Price Target: NZ$1.95

Frontier Digital Ventures (FDV)

Retained at buy at Bell Potter; Price Target: $0.540 from $0.520

Flight Centre Travel Group (FLT)

Retained at buy at Citi; Price Target: $16.10 from $18.45

Retained at hold at Jefferies; Price Target: $14.00 from $17.00

Retained at overweight at JP Morgan; Price Target: $17.00 from $19.00

Retained at overweight at Morgan Stanley; Price Target: $16.60

Retained at add at Morgans; Price Target: $16.70 from $19.80

Retained at buy at Ord Minnett; Price Target: $17.61 from $22.54

Retained at buy at UBS; Price Target: $20.00

Retained at overweight at Wilsons; Price Target: $19.00 from $21.40

Gold Road Resources (GOR)

Retained at hold at Argonaut Securities; Price Target: $3.60 from $3.30

Downgraded to hold from buy at Bell Potter; Price Target: $3.25 from $3.20

Retained at buy at Canaccord Genuity; Price Target: $3.45 from $3.35

Retained at hold at Ord Minnett; Price Target: $3.35 from $3.00

Retained at sector perform at RBC Capital Markets; Price Target: $2.70 from $2.60

Retained at buy at UBS; Price Target: $3.55

Hansen Technologies (HSN)

Retained at buy at Shaw and Partners; Price Target: $7.30 from $7.20

Harvey Norman (HVN)

Retained at outperform at Macquarie; Price Target: $5.50

Imdex (IMD)

Retained at neutral at UBS; Price Target: $3.00 from $2.95

Inghams Group (ING)

Retained at outperform at Macquarie; Price Target: $3.50

JB HI-FI (JBH)

Retained at outperform at Macquarie; Price Target: $111.00

Liontown Resources (LTR)

Retained at neutral at Goldman Sachs; Price Target: $0.630 from $0.640

Retained at hold at Morgans; Price Target: $0.520 from $0.490

Retained at neutral at UBS; Price Target: $0.650

Lynas Rare Earths (LYC)

Retained at sell at Bell Potter; Price Target: $6.25 from $6.50

Retained at buy at Canaccord Genuity; Price Target: $8.80 from $8.20

Retained at sell at Citi; Price Target: $5.50

Retained at neutral at Goldman Sachs; Price Target: $7.20 from $7.10

Retained at hold at Jefferies; Price Target: $8.00 from $7.00

Retained at underweight at JP Morgan; Price Target: $5.30 from $5.10

Retained at neutral at Macquarie; Price Target: $8.00 from $7.30

Retained at underweight at Morgan Stanley; Price Target: $7.00

Retained at hold at Ord Minnett; Price Target: $8.70 from $7.80

Metro Mining (MMI)

Retained at buy at Shaw and Partners; Price Target: $0.170

Mitchell Services (MSV)

Retained at buy at Morgans; Price Target: $0.450 from $0.500

Metcash (MTS)

Retained at neutral at Macquarie; Price Target: $3.30

Monash IVF Group (MVF)

Retained at buy at Bell Potter; Price Target: $1.250 from $1.690

National Australia Bank (NAB)

Retained at equal-weight at Morgan Stanley; Price Target: $34.80

Newmont Corporation (NEM)

Retained at buy at Goldman Sachs; Price Target: $93.40 from $95.50

Retained at buy at Ord Minnett; Price Target: $97.00 from $95.00

Nextdc (NXT)

Retained at buy at Citi; Price Target: $18.70

Origin Energy (ORG)

Retained at buy at Citi; Price Target: $11.50

Pantoro (PNR)

Downgraded to hold from buy at Argonaut Securities; Price Target: $3.00 from $3.80

Downgraded to hold from buy at Bell Potter; Price Target: $2.30 from $2.40

Retained at buy at Canaccord Genuity; Price Target: $3.82 from $3.91

Upgraded to buy from hold at Moelis Australia; Price Target: $3.27 from $3.06

Retained at buy at Ord Minnett; Price Target: $3.05 from $3.00

Perseus Mining (PRU)

Retained at buy at Canaccord Genuity; Price Target: $5.00

Retained at neutral at Citi; Price Target: $3.50 from $3.60

Retained at outperform at Macquarie; Price Target: $3.80 from $3.85

PYC Therapeutics (PYC)

Retained at buy at Ord Minnett; Price Target: $4.00

Qoria (QOR)

Retained at buy at Ord Minnett; Price Target: $0.560 from $0.580

Resmed Inc (RMD)

Retained at buy at Goldman Sachs; Price Target: $49.30 from $46.90

Sigma Healthcare (SIG)

Retained at underperform at Macquarie; Price Target: $2.70

Santana Minerals (SMI)

Retained at buy at Shaw and Partners; Price Target: $1.360

Strike Energy (STX)

Retained at buy at Bell Potter; Price Target: $0.240 from $0.250

Retained at buy at Goldman Sachs; Price Target: $0.250

Retained at neutral at Macquarie; Price Target: $0.190 from $0.220

Super Retail Group (SUL)

Retained at neutral at Macquarie; Price Target: $15.40

Sayona Mining (SYA)

Retained at outperform at Macquarie; Price Target: $0.040

Telix Pharmaceuticals (TLX)

Retained at buy at Bell Potter; Price Target: $34.00 from $36.00

Retained at buy at UBS; Price Target: $36.00

Treasury Wine Estates (TWE)

Retained at outperform at Macquarie; Price Target: $11.70

Westpac Banking Corporation (WBC)

Retained at underweight at Morgan Stanley; Price Target: $29.20

Woodside Energy Group (WDS)

Retained at neutral at Citi; Price Target: $21.50

Wesfarmers (WES)

Retained at neutral at Macquarie; Price Target: $75.00

Woolworths Group (WOW)

Retained at outperform at Macquarie; Price Target: $30.80

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| DY6 | DY6 Metals Ltd | $0.165 | +292.86% |

| CML | Connected Minerals Ltd | $0.16 | +45.46% |

| ADN | Andromeda Metals Ltd | $0.014 | +40.00% |

| NYM | Narryer Metals Ltd | $0.042 | +35.48% |

| EL8 | Elevate Uranium Ltd | $0.29 | +31.82% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| HCF | H&G High Conviction Ltd | $0.055 | -84.29% |

| AOF | Australian Unity Office Fund | $0.48 | -45.76% |

| SMX | Strata Minerals Ltd | $0.017 | -43.33% |

| IVT | Inventis Ltd | $0.016 | -33.33% |

| REY | REY Resources Ltd | $0.027 | -28.95% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| OMX | Orange Minerals NL | $0.038 | +18.75% |

| TKM | Trek Metals Ltd | $0.069 | +9.52% |

| NMR | Native Mineral Resources Holdings Ltd | $0.18 | +9.09% |

| ZEO | Zeotech Ltd | $0.09 | +8.43% |

| ALK | Alkane Resources Ltd | $0.845 | +8.33% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| HCF | H&G High Conviction Ltd | $0.055 | -84.29% |

| AOF | Australian Unity Office Fund | $0.48 | -45.76% |

| SMX | Strata Minerals Ltd | $0.017 | -43.33% |

| IVT | Inventis Ltd | $0.016 | -33.33% |

| REY | REY Resources Ltd | $0.027 | -28.95% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| IHD | Ishares S&P/ASX DIV Opportunities Esg Screened ETF | $14.45 | +1.12% |

| OBL | Omni Bridgeway Ltd | $1.51 | +4.50% |

| BILL | Ishares Core Cash ETF | $100.75 | +0.01% |

| GLDN | Ishares Physical Gold ETF | $41.20 | +0.51% |

| MTO | Motorcycle Holdings Ltd | $2.23 | +2.77% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| NWSLV | News Corporation | $41.80 | 0.00% |

| CRN | Coronado Global Resources Inc | $0.225 | +2.27% |

| AOF | Australian Unity Office Fund | $0.48 | -45.76% |

| PIQ | Proteomics International Laboratories Ltd | $0.37 | -2.63% |

| CTT | Cettire Ltd | $0.465 | -1.06% |