News | Market Wraps

Evening Wrap: ASX 200 defies Trump-Fed spat as safe haven buying lifts Commonwealth Bank, supermarkets and gold

The S&P/ASX 200 closed 2.4 points lower, down 0.03%.

Mentioned

The S&P/ASX 200 closed 2.4 points lower, down 0.03%.

Aussie stocks hung tough today, largely shaking off sharp falls in US stocks on Monday as the Trump administration stepped up its rhetoric against Federal Reserve Chairman Jerome Powell.

Having said this, it was a very specific, very defensive rally from today's low, with investors opting mainly for the relative safety of the big banks ("Well at least I'll get a fully franked dividend yield while all this silliness plays out!"), the big supermarket operators ("Well we all still have to buy groceries!"), and don't forget the default "defensive go-tos" of gold stocks and Telstra (TLS) (+0.23%) – they too rose.

Commonwealth Bank of Australia (CBA) (+4.2%) led the banking rally, supported by Macquarie Group (MQG) (+0.6%), while Coles Group (COL) (+1.1%) and Woolworths (WOW) (+0.7%) led supermarkets.

In gold, Evolution Mining (EVN) (+4.8%), Black Cat Syndicate (BC8) (+7.0%), and Resolute Mining (RSG) (+8.6%) were the best – but there were so many more that did really, really well! 🥇

To make sense of all the above, I have detailed technical analysis on the Nasdaq Composite, S&P/ASX 200 and Gold in today's ChartWatch (but loads of other super interesting charts too!).

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key upcoming economic data in tonight's Evening Wrap.

Let's dive in!

Today in Review

Tue 22 Apr 25, 5:06pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 7,816.7 | -0.03% |

| All Ords | 8,013.7 | -0.10% |

| Small Ords | 2,965.1 | -0.71% |

| All Tech | 3,265.2 | -1.97% |

| Emerging Companies | 2,153.8 | -0.60% |

Currency | ||

| AUD/USD | 0.6428 | +0.19% |

US Futures | ||

| S&P 500 | 5,243.0 | +1.12% |

| Dow Jones | 38,694.0 | +0.95% |

| Nasdaq | 18,132.75 | +1.17% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Financials | 8,490.8 | +1.23% |

| Consumer Staples | 12,240.6 | +0.33% |

| Materials | 15,836.2 | +0.19% |

| Utilities | 8,934.9 | -0.25% |

| Communication Services | 1,678.1 | -0.63% |

| Consumer Discretionary | 3,771.5 | -0.76% |

| Real Estate | 3,479.8 | -0.97% |

| Industrials | 7,618.6 | -1.22% |

| Health Care | 38,880.3 | -1.35% |

| Energy | 6,820.9 | -1.91% |

| Information Technology | 2,200.9 | -2.26% |

Markets

%20intraday%20chart%2022%20April%202025.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 2.4 points lower at 7,816.7, 0.92% from its session low and just 0.07% from its high. Despite the bravado among the big-caps, in the broader-based S&P/ASX 300 (XKO) advancers lagged decliners notably – by a margin of 61 to 216.

At a press conference in the Oval Office early Friday morning our time, President Trump had this to say when questioned about his earlier comments that “the termination of Jerome Powell cannot come fast enough”:

“He’ll leave if I ask him to, he’ll be out of there. I don’t think he’s doing the job. He’s too late, always too late, or he’s too slow, and I’m not happy with him. I’ve let him know, and if I want him out, he’ll be out of there real fast, believe me.”

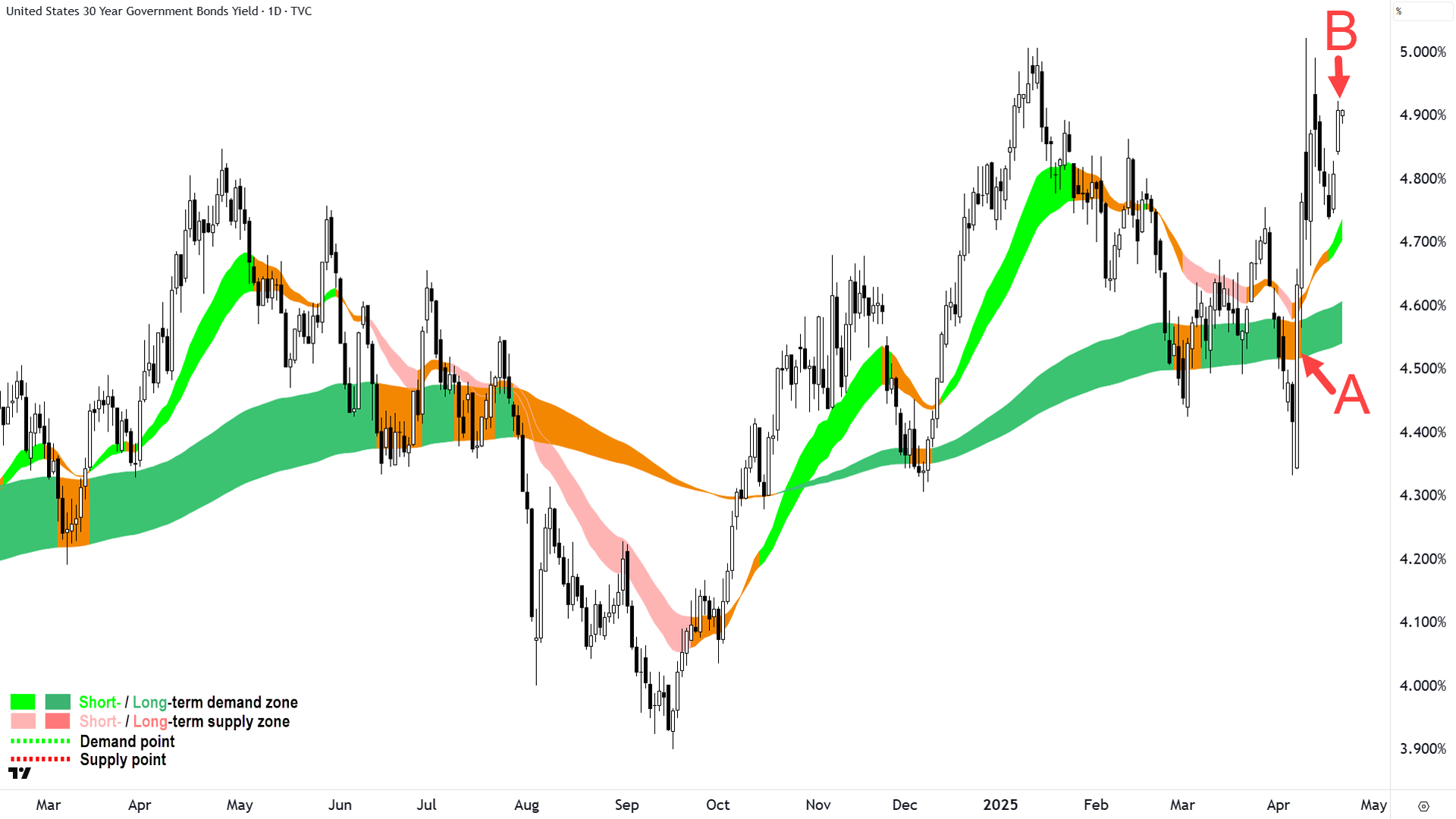

This newly stepped-up rhetoric against the Chairman of the Federal Reserve has reignited the selloff in the bond market ("B") – which, as you know, took a sudden turn for the worse following the President’s Liberation Day "reciprocal" tariffs announcement ("A").

US 30 Year T-Bond Yield (click here for full size image)

{kind=link}

The thought that a sitting US president could pressure the Federal Reserve into a monetary policy response undermines the entire modern economic system of independence between the monetary and fiscal arms of government. It's kind of a big deal.

So, the US bond market is under pressure again, and is even less "beautiful" than when President Trump performed his impressive April 7 about-face with respect to his "reciprocal" tariffs.

As we have discussed here several times over the last few weeks, the unpredictability emanating from the Oval Office is undermining confidence in US government debt at global risk-free reserve asset, and is arguably causing many US debt holders to reconsider their position and look for alternative risk-free-style assets.

%20ICE%20chart%2022%20April%202025.png)

US Dollar Index Futures (Front month, back-adjusted) ICE (click here for full size image)

{kind=link}

The yields on Chinese, UK, European (and even Australian!) government bonds have fallen - as investors have fled US bonds for calmer seas. The US dollar – King Dollar is tanking.

But another clear beneficiary in all of this is gold, it has powered ahead since our last chat here (full analysis on gold, as well as the usual Nasdaq and XJO updates can be found in ChartWatch below).

Weirdly, Aussie stocks didn't do too bad at all today and neither did the Australian dollar. Is the market thinking changing, are we a safe haven jurisdiction now? And why? 🤔

I suspect it may indeed have surprised many of you that Aussie stocks weren't belted like their US counterparts today. We also shrugged off corresponding US stocks' losses on Thursday – and that was ahead of a 4-day break at risk of any number of Trumpisms!

And ironically, as discussed above – he didn't disappoint – we got our headlines, and sufficiently risky ones at that. Yet the ASX held. Rock solid 💪.

So, have we then seen a sort of, Liberation Day for Aussie stocks? Um, too soon? 😁 Ok then, how about an Independence Day for Aussie stocks!?

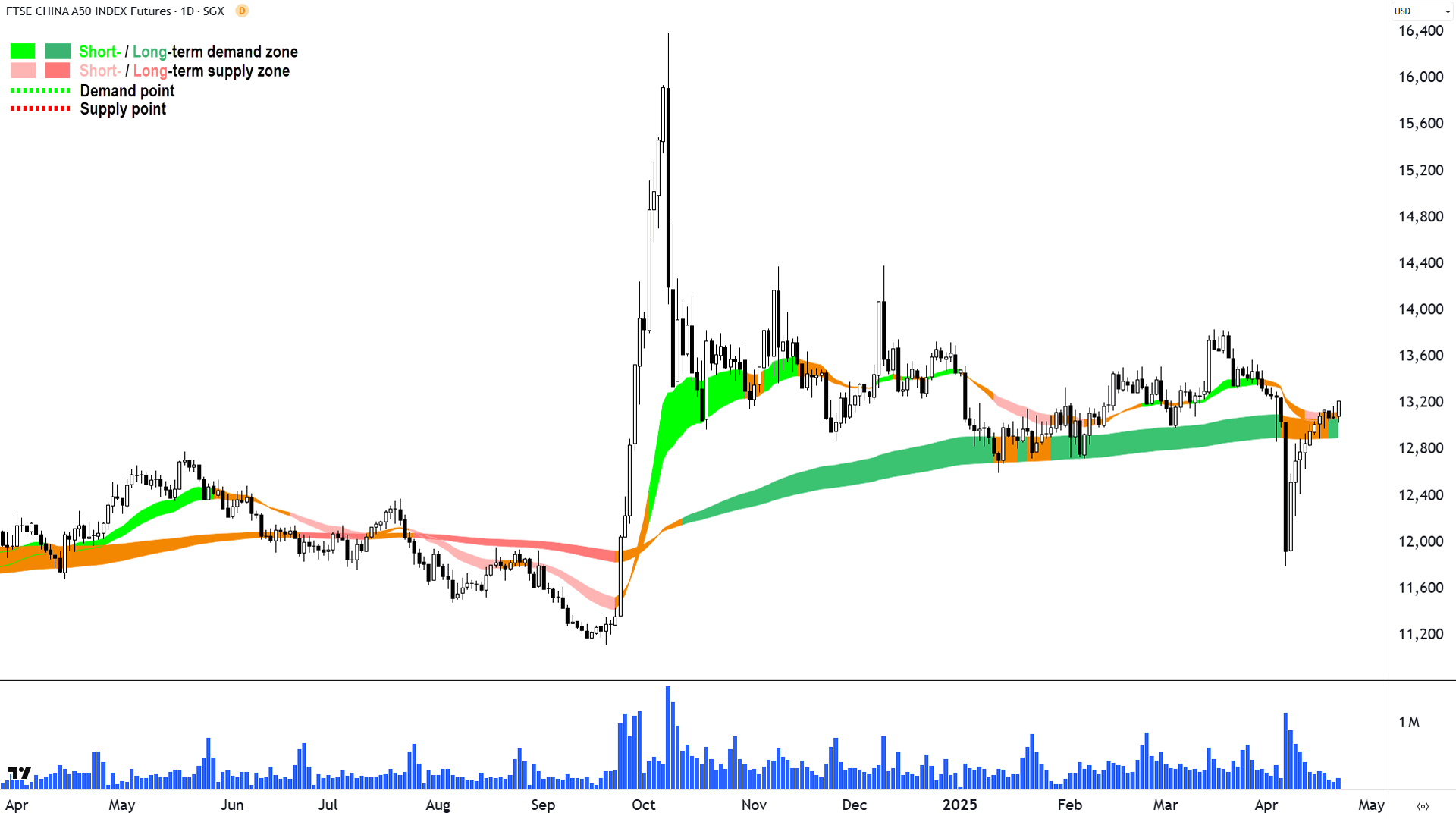

FTSE China A50 Index Futures (click here for full size image)

{kind=link}

Perhaps confirming the ASX is now hitching its wagon to "the other" major economic superpower, I note that Chinese stocks are also higher today...🧐

It seems you can have your headlines President Trump, we're betting on China now!

ChartWatch

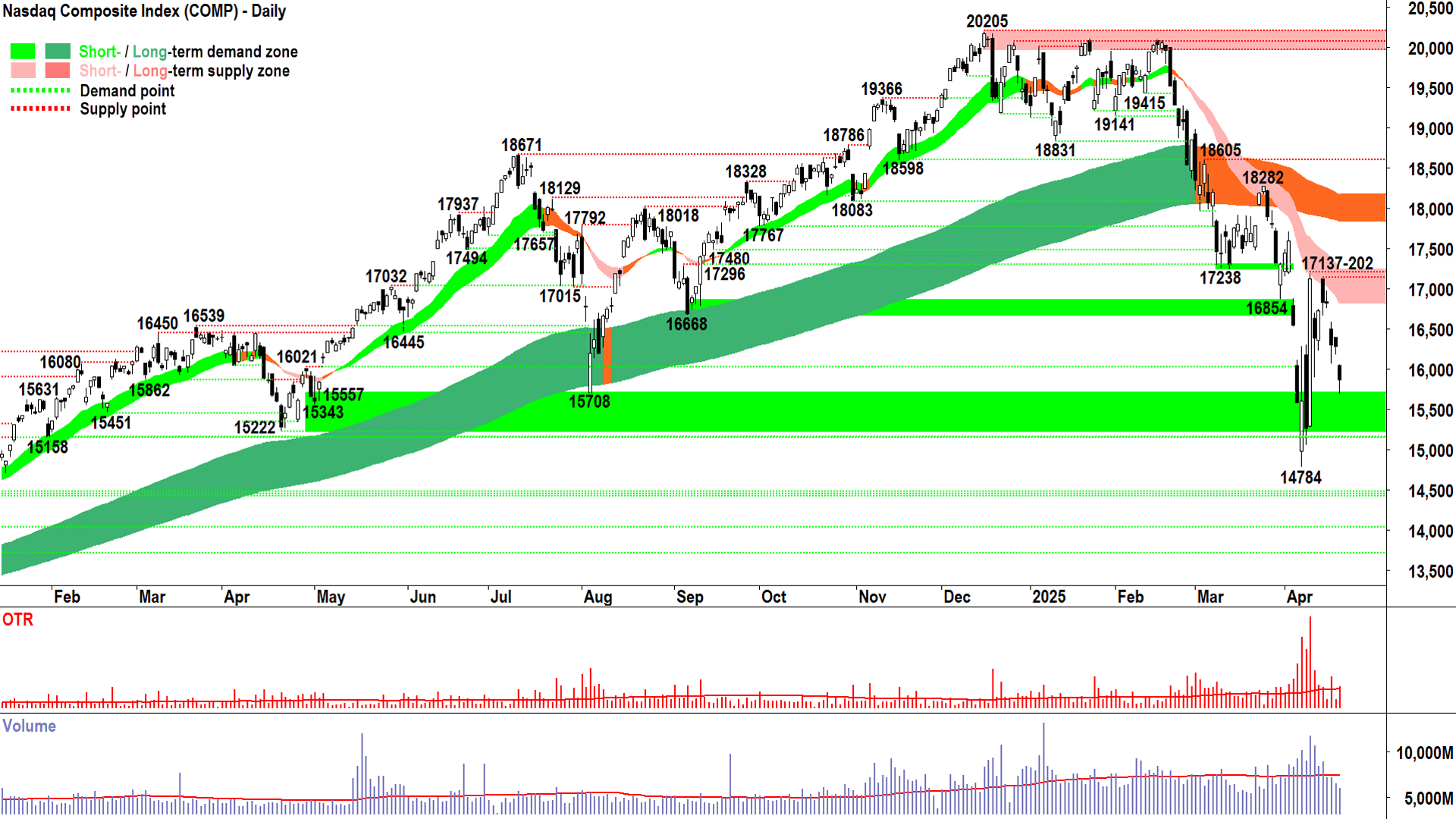

NASDAQ Composite Index

An interesting chart (click here for full size image)

{kind=link}

Not a great deal has change since our last update in terms of guiding our understanding of what’s happening within the demand-supply environment for US stocks (because headlines and Trump-isms aside, please tell me what else actually matters!? 🤔).

We have two more candles to interpret, but neither is inconsistent with our prevailing assumption that the supply-side remains in control of price in the short and long term.

The demand-side isn’t completely absent from proceedings, however, as can be seen in Monday’s downward pointing shadow. The buy the dippers are still lurking – even if they aren’t powerful enough to shift the dial a great deal by the end of the session.

In our last update on Thursday, you heard me use the term “fighting retreat” to describe Wednesday’s candle. Monday’s candle is much the same. Together they lead me to believe we’re in more of an equilibrium phase than an all-out excess supply phase…although arguing shades of supply-side control in the present market is probably a bit irrelevant!

You know the drill. If we get another substantial demand-side showing in the green zone between 15222-15708 – as in some really convincing demand-side candles (i.e., white bodies and or downward pointing shadows – big ones), on some above average volume – then there’s a solid chance that 14784 can hold and the Comp can work its way out of the current bear market.

Without those, or if instead we see some really convincing opposite candles (i.e., black bodies and or upward pointing shadows – big ones), then it’s more likely we’ll see the demand at 14784 consumed, making way for the next leg down in this bear market.

More broadly speaking, the short term trend ribbon is the key barrier to the upside. Below it, there’s really very little reason for optimism.

This is all a bit moot when you consider that a clearly defined risk management methodology that dictates portfolio risk as per the strength of the trend in a benchmark index would have put you in a majority cash position over a month ago.

I know I labour this point a bit – but I want to contrast the ho-hum attitude of this analysis against the click-bait headlines trying to make you emotional about your portfolios everywhere else!

S&P/ASX 200 (XJO)

%20chart%2022%20April%202025.png)

An interesting chart (click here for full size image)

{kind=link}

Talk about your fighting retreat! 💪💪💪

Tack Thursday’s candle onto today’s candle and it says a great deal about the inherent strength Aussie stocks are showing in the face of adversity (or in the face of absurdity – if you prefer 😁).

Our recent price action doesn’t add up with the Comp’s – but it doesn’t have to.

As technical analysts we must assume every single market participant – that is, everyone on both the demand and supply-sides – is aware of every risk facing Aussie stocks right now, and has priced those risks and acted accordingly.

This is the warm and cosy blanket I wrap myself in each night before I fall asleep and dream of candlesticks! 😴

The market knows all, and that’s all I need to know.

So, what’s happening on the XJO isn’t a mistake. It’s not ignoring the building risks in the US. It’s valid, and we should allow it to shape our view on who’s in control of the price in the chart above.

The XJO’s rally from 7169 is credible. It’s consistent with major swing lows set in previous corrections. It is, however, still only the beginning of a credible reversal – so confirmation is required. E.g.:

A close above the short term trend ribbon

Subsequent test and hold of the short term trend ribbon

Short term trend ribbon turns up

Continued predominance of demand-side candles

A higher trough to 7169 being set (as high as possible to indicate growing demand-side control)

There’s no point looking any further out than that. There’s also no point making any big calls here. We appear to be doing our own thing. There does appear to be credible demand-side participation.

But we’re not out of the woods ⚠️!

So, let’s see how the next few candles fall…but with a greater helping of optimism here than compared to the Comp.

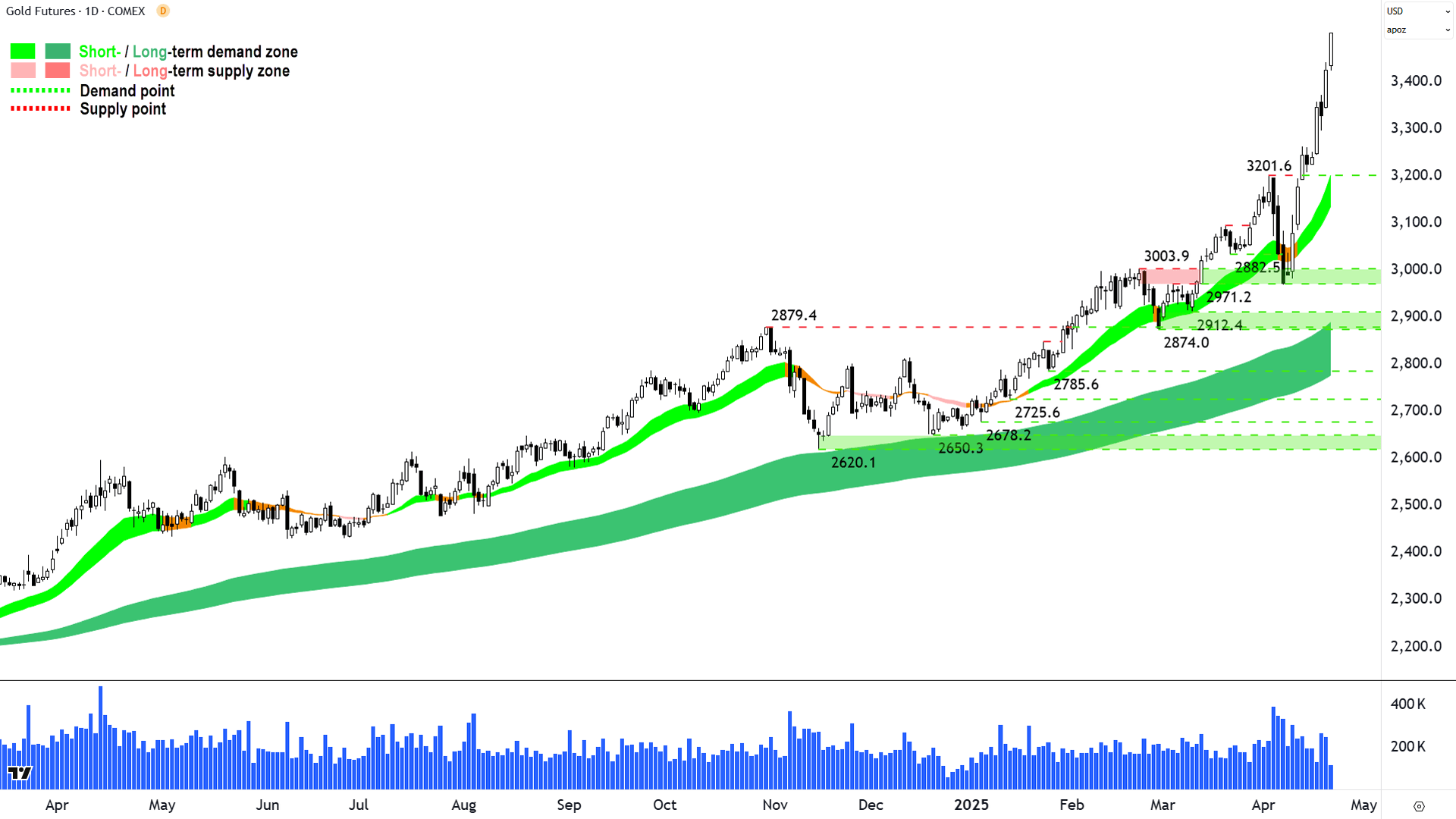

Gold Futures (Front month, back-adjusted) COMEX

%20COMEX%20chart%2022%20April%202025.png)

An interesting chart (click here for full size image)

{kind=link}

In the Wrap, we noted how the US bond markets loss is gold's gain. How long can this relationship last, and therefore gold keep powering? 🚀🤔

That's the million dollar question, and you know I don't do prognostications – this is not a cop out – it's just pointless to try to predict the future because nobody can.

The fact of the matter is: Gold's rally will last as long as it does. Our job is not to worry about it coming to its inevitable end (no rally goes on forever!).

Our job is to the monitor the price action and candles on both charts (US bonds and Gold) and watch for the typical fingerprints of supply-side control in the gold price.

Which clearly aren't in abundance, looking at the chart above!

So, much like I've said with respect to the gold chart for about 18-months now...I see no reason to doubt the prevailing short and long term uptrends.

Economy

Today

There weren't any major data releases in our time zone today

Later this week

Wednesday

07:00 AUS Flash Purchasing Managers Index (PMI) April

Manufacturing PMI: 52.1 previous

Services PMI: 51.6 previous

21:45 USA Flash Purchasing Managers Index (PMI) April

Manufacturing PMI: 49.0 forecast vs 50.2 previous

Services PMI: 52.8 forecast vs 54.4 previous

22:00 USA New Home Sales March (682,000 forecast vs 676,000 in February)

Thursday

20:30 USA Core Durable Goods Orders March (+0.3% m/m forecast vs +0.7% m/m in February)

22:00 USA Existing Home Sales March (4.14 million forecast vs 4.26 million in February)

Friday

All day AUS ANZAC Day Public Holiday

Latest News

Interesting Movers

Trading higher

+23.9% Challenger Gold (CEL) – No news, general strength across the broader Gold sector today, rise is consistent with prevailing short term uptrend and long term trend is transitioning from down to up 🔎📈

+19.2% St Barbara (SBM) – No news, general strength across the broader Gold sector today.

+18.5% Native Mineral Resources (NMR) – RC drilling returns high-grade, shallow gold mineralisation, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends 🔎📈

+15.4% Koonenberry Gold (KNB) – No news, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+11.1% MTM Critical Metals (MTM) – No news, general strength across the broader Rare Earths & Critical Minerals sector today, rise is consistent with prevailing short and long term uptrends, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

+9.5% Tivan (TVN) – No news, general strength across the broader Critical Minerals sector today, rise is consistent with prevailing short and long term uptrends 🔎📈

+9.3% Iperionx (IPX) – No news, general strength across the broader Critical Minerals sector today.

+8.6% Resolute Mining (RSG) – 2024 Sustainability Report, general strength across the broader Gold sector today.

+8.4% Antipa Minerals (AZY) – No news, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+7.8% Brainchip (BRN) – No news, still likely benefiting from Trump's looming semiconductor review.

+7.8% Alkane Resources (ALK) – No news, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+7.0% Black Cat Syndicate (BC8) – No news, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+6.9% Adriatic Metals (ADT) – No news, general strength across the broader Precious Metals sector today.

+6.9% Aurelia Metals (AMI) – No news, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+6.6% West African Resources (WAF) – No news, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.2% Pantoro (PNR) – No news, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.2% Southern Cross Gold (SX2) – No news, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.1% Kingsgate Consolidated (KCN) – No news, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

+4.8% Evolution Mining (EVN) – No news, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+4.8% Gorilla Gold Mines (GG8) – No news, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+4.5% Austal (ASB) – No news, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+4.2% Commonwealth Bank of Australia (CBA) – No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+3.8% Regis Resources (RRL) – No news, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+3.4% Global X Physical Gold ETF (GOL) – No news, general strength across the broader Gold sector today, Gold ETF, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+3.4% De Grey Mining (DEG) – Court approves Scheme and Change in substantial holding (potentially a reduction in short seller interest), general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

Trading lower

-19.2% Meteoric Resources (MEI) – No news, pulled back in the wake of recent sharp rally.

-12.5% Paladin Energy (PDN) – No news, general weakness across the broader Uranium sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-12.5% EBR Systems (EBR) – No news, fall is consistent with prevailing short term downtrend and falling peaks and falling troughs 🔎📉

-12.0% Bannerman Energy (BMN) – No news, general weakness across the broader Uranium sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-11.0% Australian Strategic Materials (ASM) – Pulled back in the wake of recent sharp rally.

-10.9% Silex Systems (SLX) – General weakness across the broader Uranium sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-9.7% Lotus Resources (LOT) – General weakness across the broader Uranium sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-9.0% Zip Co. (ZIP) – Change in substantial holding (possibly an increase in short seller interest), fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-8.2% Deep Yellow (DYL) – March 2025 Quarterly Activities Report and Appendix 5B March 2025 Quarterly Cashflow, general weakness across the broader Uranium sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-7.8% Boss Energy (BOE) – No news, general weakness across the broader Uranium sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-7.1% Bellevue Gold (BGL) – Near-term hedge book close out, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-6.4% Cettire (CTT) – No news, fall is consistent with prevailing short and long term downtrends, one of the most Featured (highest conviction) stocks in ChartWatch ASX Scans Downtrends list 🔎📉

-6.4% Coronado Global Resources (CRN) – No news, general weakness across the broader Energy sector today, fall is consistent with prevailing short and long term downtrends, one of the most Featured (highest conviction) stocks in ChartWatch ASX Scans Downtrends list 🔎📉

-6.3% Polynovo (PNV) – No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-6.2% Nextdc (NXT) – No news, general weakness across the broader Information Technology sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.9% Regal Partners (RPL) – No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.4% Block (XYZ) – No news, general weakness across the broader Industrials sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.4% Nexgen Energy (NXG) – No news, general weakness across the broader Uranium sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.0% Clarity Pharmaceuticals (CU6) – No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.9% Nickel Industries (NIC) – No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.7% Liontown Resources (LTR) – No news, general weakness across the broader Lithium sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.5% IGO (IGO) – No news, general weakness across the broader Lithium sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

Broker Moves

Amcor (AMC)

Retained at buy at Citi; Price Target: $19.00

AMP (AMP)

Upgraded to buy from negative at Citi; Price Target: $1.300 from $1.600

Upgraded to buy from negative at Goldman Sachs; Price Target: $1.400 from $1.540

BHP Group (BHP)

Retained at buy at Citi; Price Target: $45.00

Retained at outperform at Macquarie; Price Target: $42.00

Retained at add at Morgans; Price Target: $48.70 from $48.10

Retained at accumulate at Ord Minnett; Price Target: $42.00

Bank of Queensland (BOQ)

Retained at sell at Citi; Price Target: $6.00

Car Group (CAR)

Retained at add at Morgans; Price Target: $40.70 from $41.40

Challenger (CGF)

Retained at buy at Bell Potter; Price Target: $7.80

Retained at buy at Citi; Price Target: $7.55 from $6.70

Retained at add at Morgans; Price Target: $7.51 from $6.93

Retained at buy at Ord Minnett; Price Target: $8.00

Computershare (CPU)

Retained at equal-weight at Morgan Stanley; Price Target: $34.70 from $36.60

Cygnus Metals (CY5)

Retained at buy at Canaccord Genuity; Price Target: $0.300

Genesis Minerals (GMD)

Retained at hold at Bell Potter; Price Target: $4.45 from $3.75

Downgraded to hold from accumulate at Ord Minnett; Price Target: $4.15 from $3.75

James Hardie Industries (JHX)

Retained at negative at Citi; Price Target: $56.00

Karoon Energy (KAR)

Retained at add at Morgans; Price Target: $2.25 from $2.40

Macquarie Group (MQG)

Retained at sell at Citi; Price Target: $177.00

Retained at negative at UBS; Price Target: $235.00

Monash IVF Group (MVF)

Upgraded to buy from hold at Ord Minnett; Price Target: $1.100 from $1.250

Pilbara Minerals (PLS)

Retained at buy at Bell Potter; Price Target: $2.00

Retained at buy at Canaccord Genuity; Price Target: $2.70

Retained at buy at Citi; Price Target: $1.600 from $1.650

Retained at outperform at Macquarie; Price Target: $2.40

Retained at add at Morgans; Price Target: $2.30 from $2.40

REA Group (REA)

Retained at hold at Morgans; Price Target: $248.00

Region Group (RGN)

Retained at buy at Citi; Price Target: $2.40

South32 (S32)

Retained at buy at Citi; Price Target: $4.00

Retained at outperform at Macquarie; Price Target: $4.50

Retained at buy at Ord Minnett; Price Target: $4.20 from $4.30

Seek (SEK)

Retained at add at Morgans; Price Target: $27.20

Santos (STO)

Retained at outperform at Macquarie; Price Target: $8.50 from $8.60

Retained at buy at Ord Minnett; Price Target: $8.20

Transurban Group (TCL)

Retained at negative at Citi; Price Target: $14.00 from $13.80

Retained at hold at Morgans; Price Target: $12.65 from $12.64

Downgraded to negative from buy at UBS; Price Target: $14.60 from $14.85

West African Resources (WAF)

Retained at buy at Canaccord Genuity; Price Target: $4.55 from $4.50

Retained at outperform at Macquarie; Price Target: $2.80 from $2.70

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| SMM | Somerset Minerals Ltd | $0.012 | +33.33% |

| PFT | Pure Foods Tasmania Ltd | $0.022 | +29.41% |

| ASE | Astute Metals NL | $0.027 | +28.57% |

| CEL | Challenger Gold Ltd | $0.088 | +23.94% |

| EME | Energy Metals Ltd | $0.085 | +21.43% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| SRL | Sunrise Energy Metals Ltd | $0.44 | -38.03% |

| VMM | Viridis Mining and Minerals Ltd | $0.285 | -19.72% |

| MEI | Meteoric Resources NL | $0.105 | -19.23% |

| HE8 | Helios Energy Ltd | $0.013 | -18.75% |

| EPX | Ep&T Global Ltd | $0.029 | -17.14% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| CEL | Challenger Gold Ltd | $0.088 | +23.94% |

| NMR | Native Mineral Resources Holdings Ltd | $0.16 | +18.52% |

| KNB | Koonenberry Gold Ltd | $0.075 | +15.39% |

| MVL | Marvel Gold Ltd | $0.015 | +15.39% |

| AGD | Austral Gold Ltd | $0.07 | +12.90% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| IBX | Imagion Biosystems Ltd | $0.012 | -14.29% |

| MIO | Macarthur Minerals Ltd | $0.024 | -14.29% |

| BMM | Bayan Mining and Minerals Ltd | $0.031 | -13.89% |

| BMN | Bannerman Energy Ltd | $1.755 | -12.03% |

| SRJ | SRJ Technologies Group Plc | $0.022 | -12.00% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| BILL | Ishares Core Cash ETF | $100.64 | -0.01% |

| GLDN | Ishares Physical Gold ETF | $43.29 | +3.37% |

| GXLD | Global X Gold Bullion ETF | $54.24 | +3.28% |

| AYUPA | Australian Unity Ltd | $82.25 | 0.00% |

| AMI | Aurelia Metals Ltd | $0.31 | +6.90% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| WLE | Wam Leaders Ltd | $1.145 | -0.87% |

| NXL | NUIX Ltd | $2.27 | -2.99% |

| FLT | Flight Centre Travel Group Ltd | $11.74 | -4.09% |

| APX | Appen Ltd | $0.775 | -3.13% |

| RDY | Readytech Holdings Ltd | $2.20 | +0.46% |