How to Buy Shares for a Child

A Guide to Building a "Starter" Portfolio

Updated: 10 August 2022

Disclaimer

It’s imperative that you speak to your stockbroker or accountant prior to investing on behalf of a minor. Tax implications can be significant and everyone’s situation is different.

Many Australian investors would like to start a share portfolio for their child or grandchild to help them along the road to financial security.

The intention is to hold for the long-term, compound all returns, and have a modest nest egg to give the beneficiary on their 18th birthday or significant milestone.

When done correctly, exposure to the stock market can be an excellent long-term investment for a child because it combines two very important factors of successful investment:

- Compounding of dividends

- Time

As time is on the kid’s side, the amount of capital required can be as little as a few thousand dollars.

"Compound interest is the eighth wonder of the world.

He who understands it, earns it ... he who doesn't ... pays it."

- Albert Einstein

What’s the Goal?

The goal should be to generate a capital return close to the overall stock market while reinvesting dividends back into the portfolio.

Although the Australian share market has been volatile recently, it’s important to look at the long-term picture.

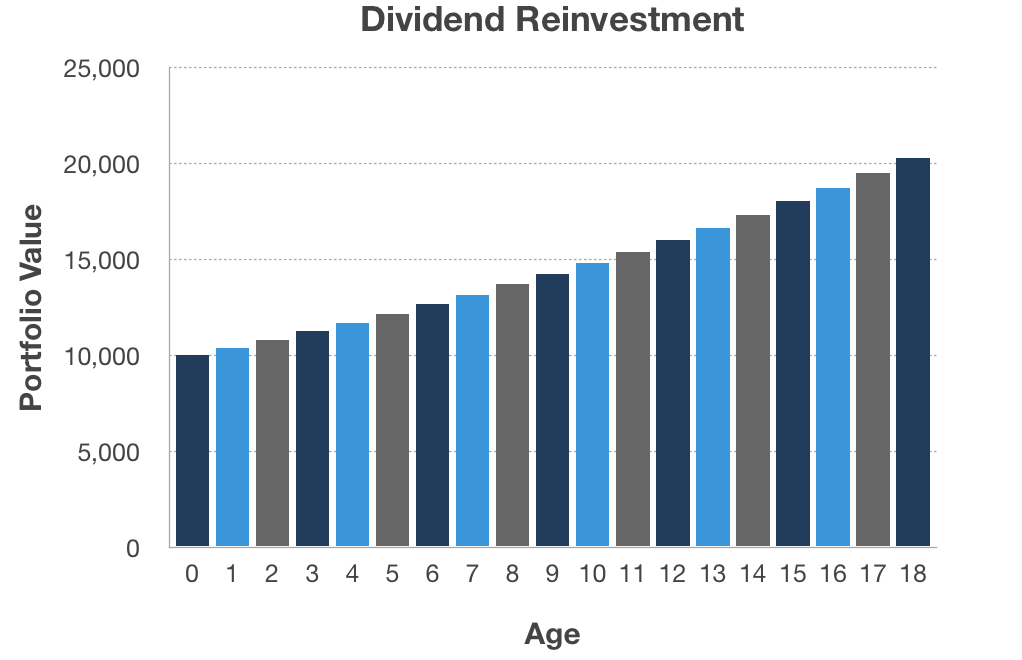

Since 1900, the Australian share market has had 99 positive years and returned an average of 13.2% annually (including dividends).

$10,000 with 4% dividends will double over 18 years

$10,000 with 4% dividends will double over 18 yearsIf the child starts developing an interest in their investment, they can be encouraged to provide input (with the adult's guidance) into the portfolio's constituents.

Pocket money can be added to the share portfolio over time and valuable lessons in the basics of investment can be taught.

Setting up the Account

Minors can’t personally buy and sell shares, so to avoid the need for a formal trust the most common (and easiest) approach is to create an account in the name of an adult (e.g. parent) with the shares held in trust for the child.

When completing the paperwork, you place the minor’s name in the account designation. E.g.

By law, you are the legal owner of the shares but the minor is the beneficiary.

A Cash Management account (i.e. bank account) in the same name should also be created and linked to the share trading account. This usually comes standard with most broking accounts so there’s no need to organise it prior to opening the trading account.

Place the starting capital into the bank account and then you are ready to invest.

Shares to Buy for Kids

Most “gift” portfolios are relatively small (i.e. under $20,000) so building a diversified portfolio of individual stocks is not practical. Although it can be done, purchasing enough companies to get adequate diversification would incur significant brokerage costs (crippling the return of the small portfolio) and increase the time spent managing the portfolio.

A popular option to solve the diversification dilemma is to use an Exchange Traded Fund (ETF) that provides exposure to a broad market index (e.g. S&P/ASX 200). Investors can buy and sell ETFs through their stockbroker just like ordinary ASX shares and view prices online at anytime using their ticker codes.

Three of the biggest companies in Australia that offer Listed Funds are:

- SPDR

- Vanguard Investments

- BetaShares

Market Index has a page that lists all ASX listed ETFs grouped by region and sector.

One ETF to rule them all

Australia's largest ETF is Vanugaurd's Australian Shares (VAS). It contains Australia's 300 largest ASX listed companies, is rebalance regularly, and provides diversification to ~73%Aug 22 of Australia's equity market (by market capitalisation).

Transferring Ownership to the Child

When the minor turn 18, you can transfer ownership of all shares to the child and they will legally own the shares in their name. You relinquish all rights to the portfolio and lose control over the trading.

A “Change of Ownership” form is required and under most circumstances the adult will not incur capital gains tax because there was no change in beneficiary.

If the shares are Issuer Sponsored, you must use a form provided by the Share Registry. If the shares are held on HIN, you must use a form provided by your stockbroker. See this post for an explanation of SRN and HIN.

Tax Implications

A tax return will need to be completed for the child if they have earned more than $416 or are entitled to a refund of franking credits. The laws are complex and different for a minor (to prevent parents funnelling their income to children and avoiding their tax obligations) so an accountant should be consulted. This is especially the case when the adult wishes to purchase a large parcel of shares for the child as any profits above the $416 threshold will attract a high tax rate.

It's also extremely important that the adult does not use the portfolio or dividends for their own purposes in any way. The Australian Taxation Office (ATO) may see "cross-usage" as proof that the adult is actually the beneficial owner.

FAQs

Can I simply “gift” a parcel of shares to my kids?

Yes, but you will probably incur Capital Gains Tax (CGT) on any profits as there is a change in beneficial ownership. You will need to complete an “Off-Market Transfer Form” with your broker (or Share Registry if held on SRN) and these typically cost $50 - $100.

Does a child who owns shares need to lodge a tax return?

Yes, if the child earns more than $416 or is entitled to a refund of franking credits. - ATO Link

Can I use any dividends for personal income?

No, the ATO will most likely then consider you as the true owner causing CGT issues on the transfer.