Three reasons lithium prices are surging and the ASX stocks poised to prosper

Lithium is moving again. Prices are up, confidence is building, and capital is flooding back. Is this the start of the next boom?

Source: Market Index via ChatGPT

Mentioned

KEY POINTS

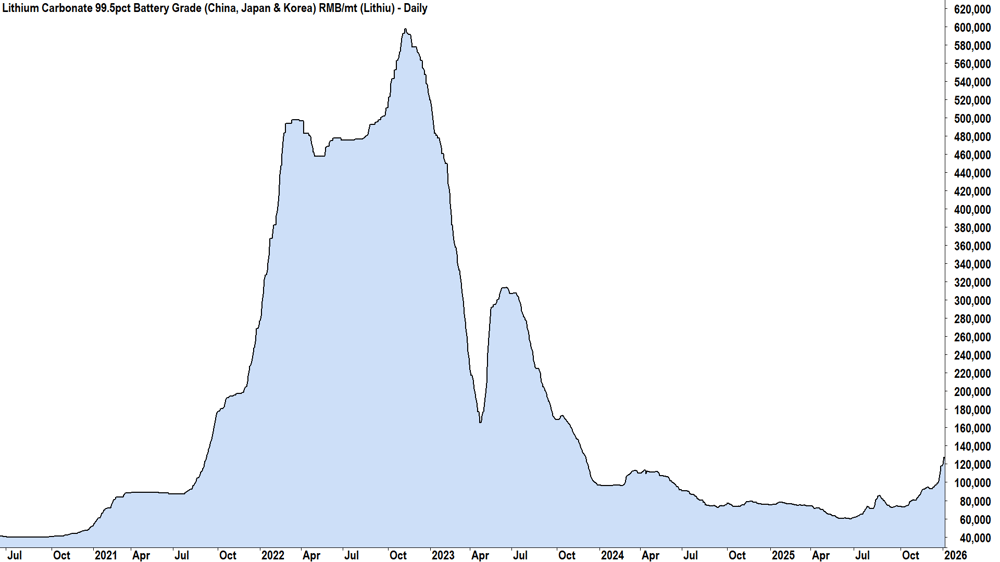

- After a brutal three-year bear market that crushed prices by nearly 90%, lithium has turned — with benchmark prices now more than doubling off the lows.

- Producers, developers and explorers across the ASX lithium space are surging as confidence returns and investors scramble for exposure to the next cycle.

- This article breaks down why sentiment has flipped towards lithium, and which ASX-listed lithium stocks stand to benefit most if the rally continues.

Commodity markets are rarely linear. They move in cycles: a period of tight supply and rising prices sparks a rush of investment; new capacity eventually hits the market with a lag; the resulting glut crushes prices; and the industry goes dormant again — until demand (often from a new end-market) quietly forces the next reset. Lithium has lived this textbook “boom–bust–boom?” pattern in fast-forward since 2020.

The last boom was brutal and brief. As electric vehicles (EVs) surged and supply chains strained, lithium prices ripped higher into 2022 — only to roll over as supply responded and downstream buyers de-stocked. What followed was a withering, three-year bear market in which key benchmark prices were slashed by roughly ninety per cent from their highs. Mines were mothballed, expansion plans were deferred, and “survival mode” became the industry’s default posture.

And then — almost imperceptibly at first — the tone changed. After bottoming in mid-2025, benchmark lithium prices have since more than doubled, helped by stronger-than-expected demand from battery storage and a shift in sentiment around supply discipline.

Lithium carbonate price chart

Is this just a bear-market bounce, or the opening act of the next lithium cycle? That’s the investor’s dilemma: get in late for the bounce, but early with respect to the upcoming up-cycle — or late in what could turn out to be just a bounce in a secular bear market.

In this article I’ll tackle that question head-on. First, I’ll lay out three reasons the lithium price is turning — backed by broker research and on-the-ground channel checks. Then, I’ll run the ruler over the major ASX-listed lithium names poised to prosper if prices keep climbing.

3 REASONS LITHIUM PRICES HAVE TURNED

1) Burgeoning demand from BESS is reshaping the lithium market

The first and most structural driver of lithium’s recovery is on the demand side of the equation: the rapid acceleration of battery energy storage systems (BESS). What was once a rounding error in lithium demand behind EVs is now becoming a structurally important end-market — one that is less cyclical than its counterpart and far less sensitive to short-term price volatility. That shift matters enormously at the margin.

The rhetoric from the major investment banks towards lithium has turned increasingly positive through the back half of last year (after a collectively bearish prior 12 months). Here's a sample of their latest research reports on the lithium and energy storage industries:

UBS

UBS argues the lithium market is approaching a genuine inflection point driven by storage demand that could trigger a “third upcycle” in the commodity [1]. The bank notes a “BESS tipping point” is looming as grid-scale storage emerges as a decisive new pillar of demand rather than a supplementary one. Following a recent trip to China by several of the bank’s analysts, UBS noted that “all” industry contacts believed lithium markets were trending into deficit by around the second half of this year [2].

Canaccord Genuity

Canaccord notes it’s increasingly clear that the lithium market is approaching a structural deficit. In its recent research note “Lithium | Upgrading BESStimates”, the broker states that following its latest supply–demand model update, it now expects the market to be balanced by this year and in deficit from next year, driven by stronger-than-expected demand growth — particularly from BESS. Canaccord forecasts lithium demand rising by around 15% to ~1.5 million tonnes (Mt) lithium carbonate equivalent ("LCE") by the end of 2026, with growth split roughly 60% BESS and 40% EVs, materially tightening the market versus prior expectations [3].

Macquarie

Macquarie also taps energy storage demand as the critical upside surprise factor in 2026, noting stronger demand than expected in 2025, supported by rising overseas orders and improving project economics. While warning higher prices should ultimately incentivise supply responses, the bank suggests the current phase reflects a genuine rebalancing, with pricing firming ahead of visible deficits as the market anticipates tighter conditions [4].

Morgan Stanley

Morgan Stanley sees battery energy storage demand as a durable, multi-year tailwind for lithium rather than a short-lived surge. The bank notes that strong BESS demand is likely to persist into 2026, with shipments running well ahead of installations as the market scales. Morgan Stanley highlights that growth is being underpinned by AI-driven electricity demand, accelerating renewable energy build-out, and policy changes in China that support healthy BESS project internal rates of return. While the bank cautions that risks remain, it argues that any lithium upcycle is likely to be more gradual than past demand shocks, reflecting the industry’s greater maturity and broader demand base — suggesting a more sustained tightening phase rather than a speculative spike [5].

Together, these insights suggest lithium’s rebound is being underwritten by a broader, more durable demand base — one that did not exist in previous cycles.

2) The race to the bottom is ending as China pushes back against destructive competition

The next key driver of lithium’s recovery sits on the supply side of the equation: the curtailment of value-destructive competition. One of the defining features of lithium’s brutal bear market — particularly in China — was a debilitating race to the bottom, where marginal producers continued operating even as prices collapsed across lithium minerals, downstream products and battery systems. That behaviour kept supply elevated, delayed the market’s natural clearing process, and pushed prices well below incentive levels. Increasingly, broker research suggests this dynamic is changing — not by accident, but by official design.

RBC Capital Markets

In its recent research note “ASX Lithium: China Lithium Royalty Reform Confirms Anti-Involution Shift, Lifting Domestic Cost Floor”, the bank argues that royalty reforms enacted in mid-2025 “institutionalise a higher domestic cost base,” effectively embedding a structural lithium price floor. RBC estimates the change lifts China’s marginal lithium production costs by CNY1,000-1,500 per tonne LCE, which it notes is sufficient to wipe out most cash margins at high-cost lepidolite operations. Critically, RBC frames this as “practical enforcement of the anti-involution policy for the lithium sector,” favouring disciplined, integrated producers over volume-at-any-cost supply growth [6].

Macquarie

Macquarie adds colour from the downstream angle. In its recent research note “Critical Minerals Chronicle – Lithium”, the bank notes that China’s Ministry of Industry and Information Technology recently convened major BESS players where “anti-involution” was directly discussed, suggesting regulatory tolerance for price-led margin repair rather than forced cost absorption. Macquarie argues this shift supports near-term pricing resilience and marks a departure from the behaviour that defined the downturn [4].

UBS

UBS reaches a similar conclusion from a policy and industry-behaviour perspective, highlighting China’s push toward a “unified national market” and anti-involution agenda, explicitly aimed at curbing cut-throat competition across critical minerals. UBS notes that falling inventories and improving pricing conditions are consistent with this shift, and reports that industry contacts increasingly see supply discipline — rather than aggressive price-led volume growth — as the new operating norm [2].

Taken together, these signals suggest the era of indiscriminate price-cutting is fading — a crucial precondition for any sustained lithium recovery.

3) Belief the bottom is in — and the next cycle has begun

The final key driver of lithium’s recovery acts on both the demand and supply sides of the equation: growing belief that the bottom is in. Commodity bottoms are rarely called with confidence at the time. Investors are conditioned to avoid catching falling knives, and lithium’s three-year collapse only reinforced that instinct.

But markets don’t wait for consensus. Once prices stop making new lows and begin rising persistently, psychology shifts. Confidence grows with every failed sell-off, positive news starts to reinforce improving price action, and eventually the two most powerful forces in markets return: fear of missing out (“FOMO”) and holding on for upside (“HOFU”).

Rising prices attract new capital chasing the next big trend, while simultaneously encouraging those already invested to withhold supply in the expectation of higher prices ahead. Plenty of demand, scarce supply — the original recipe for a bull market!

Macquarie

Macquarie’s work suggests sentiment towards lithium is now firmly in a more positive phase. It notes that both lithium prices and ASX lithium stocks have begun to firm ahead of visible deficits, reflecting a market that is anticipating tighter conditions rather than reacting to them. Macquarie highlights falling inventories, strengthening Chinese prices, and broad share-price appreciation across lithium names as evidence that sentiment has turned and investors are repositioning for the next phase of the cycle [4].

Canaccord Genuity

Canaccord frames the same shift through a forward-looking lens. It argues that the recent pricing momentum and auction outcomes are “confirmation of the improving outlook for the sector” and explicitly states that it expects this to continue supporting equities in the near to mid-term. Canaccord also warns that once confidence returns, pricing can overshoot in the near term as downstream players and investors race to secure exposure before supply responds [3].

UBS

UBS reinforces the behavioural angle, noting falling inventories and emerging restocking, while reporting that contacts increasingly see the market transitioning away from surplus conditions [2].

Together, these signals suggest lithium is no longer trading like a broken market — but like one in the early stages of a new cycle. Rising prices are drawing in capital, capital sustains momentum, and belief becomes self-fulfilling. That doesn’t guarantee a straight line higher — but it does suggest the market is no longer debating oblivion; it’s beginning to price opportunity.

ASX LITHIUM STOCKS IN FOCUS

If lithium’s rebound proves durable, the winners won’t be evenly distributed. Producers with scale and operating leverage typically respond first: cash flow improves immediately, balance sheets de-risk, and expansion optionality re-emerges. That frames PLS Group (PLS), Mineral Resources (MIN) and IGO (IGO) — names with meaningful exposure to spodumene pricing and downstream contracting.

Next come the “newer” producers and restart candidates: Liontown Resources (LTR) as it ramps Kathleen Valley, and Core Lithium (CXO) as the market weighs restart economics. Then there’s a deep bench of developers and explorers — brines and hard-rock — where a higher price deck can be the difference between a stalled DFS and a credible FID pathway*: Vulcan Energy Resources (VUL), Galan (GLN), Lake (LKE), Ioneer (INR), Argosy (AGY), plus the hard-rock exploration/development cohort led by Develop Global (DVP), Elevra Lithium (ELV), PMET Resources (PMT), Wildcat Resources (WC8), Global Lithium Resources (GL1) and Winsome Resources (WR1).

Below I’ve profiled each name — ordered by market capitalisation — to clarify who is best positioned if lithium prices keep rising (all data as at ASX close 6 January 2026).

PLS Group (ASX: PLS)

%20price%20chart%206%20Jan%202025.png)

Last price: $4.84

Market cap: $15.6 billion

Operations / geography: Pilgangoora Lithium Operation (spodumene, Western Australia).

Type: Producer

FY25 production: Pilbara reported 755kt of spodumene concentrate production in FY25. Production guidance for FY26 is 820-870kt at a cost of A$560-600/t.

Why it matters in an upcycle: Scale + operating leverage. When pricing firms, margin expands quickly; when pricing is weak, PLS can still protect volumes and balance sheet. The key variable is the durability of the rebound — and how quickly contract/auction outcomes feed through realised pricing.

Mineral Resources (ASX: MIN)

%20price%20chart%206%20Jan%202025.png)

Last price: $57.77

Market cap: $11.4 billion

Operations / geography: Integrated mining/services group with lithium exposure via Wodgina and Mt Marion hubs (spodumene, Western Australia).

Type: Producer (lithium, iron ore)

FY25 production (lithium): MIN reported 508kt of spodumene concentrate production in FY25. Production guidance for FY26 at Mt Marion is 160-180kt at a cost of A$820-890/t and at Wodgina is 220-240kt at a cost of A$730-800/t. MIN is holding around 450ktpa (pre-POSCO deal completion) of offline spodumene production capacity.

Why it matters in an upcycle: MIN offers leveraged lithium exposure but with diversification (iron ore/mining services) that can cushion volatility. In rising lithium prices, the market tends to re-rate the lithium optionality — especially if costs are under control and shipments track guidance.

IGO (ASX: IGO)

%20price%20chart%206%20Jan%202025.png)

Last price: $8.73

Market cap: $6.6 billion

Operations / geography: Battery-materials exposure via Greenbushes (spodumene, Western Australia) and downstream processing interests; Australia-centric portfolio that also includes nickel.

Type: Producer / investor (material exposure through ownership interests)

FY25 production: IGO reported 1,479kt of spodumene concentrate production in FY25. Production guidance for FY26 at Greenbushes is 1,500-1,650kt spodumene concentrate at a cost of A$310-360/t and at Kwinana Refinery is 9-11kt lithium hydroxide at a conversion cost of A$16k-20k.

Why it matters in an upcycle: IGO offers lithium price sensitivity with a different risk profile to pure-play miners — more exposure to asset performance, governance and downstream outcomes, not just mine-site execution.

Vulcan Energy Resources (ASX: VUL)

%20price%20chart%206%20Jan%202025.png)

Last price: $4.89

Market cap: $2.3 billion

Operations / geography: Lionheart Project (integrated geothermal energy and lithium extraction, Germany).

Type: Developer

Stage: FID for Phase 1 taken in December 2025. Construction commencing early 2026 with production targeted to commence 2028. When producing, VUL's costs are estimated to sit in the lowest cost quartile among global producers.

Why it matters in an upcycle: VUL offers differentiated exposure to lithium via European-sourced, zero-carbon lithium production, positioning it as a strategic supplier to EU automakers seeking greener battery materials. In a rising lithium price environment, VUL’s leverage comes not just from price, but from jurisdictional scarcity, ESG credentials, and downstream strategic value.

Liontown (ASX: LTR)

%20price%20chart%206%20Jan%202025.png)

Last price: $1.94

Market cap: $5.7 billion

Operations / geography: Kathleen Valley (spodumene, Western Australia).

Type: Producer / ramp-up

FY25 production: LTR reported 294kt of spodumene concentrate production in FY25. FY26 guidance is 365-450kt (SC5.2) at a cost of A$1,060-1,295/t. Full production is expected to be 2,800kt per annum by FY27.

Why it matters in an upcycle: The market will reward consistent ramp-up execution. Higher spot/benchmark pricing can also improve liquidity and offtake optionality — particularly relevant given evolving customer/financing arrangements.

Develop Global (ASX: DVP)

%20price%20chart%206%20Jan%202025.png)

Last price: $4.97

Market cap: $1.6 billion

Operations / geography: Australian resources developer with lithium exposure through development assets (portfolio includes base-metals focus alongside lithium optionality).

Type: Developer

Stage: Typical DFS/FID pathway depending on project; focus is on funding certainty, permitting, and build schedules.

Why it matters in an upcycle: Developers benefit disproportionately when the forward price deck improves: funding conversations get easier, offtake terms improve, and the market starts paying for “optionality” again. Project-specific milestones will drive re-rating.

Elevra Lithium (ASX: ELV)

%20price%20chart%206%20Jan%202025.png)

Last price: $8.02

Market cap: ~$1.36 billion

Operations / geography: Elevra was formed through the merger of Piedmont Lithium and Sayona Mining. Lithium exposure includes spodumene producing assets in North America (Canada: 60% stake in the Moblan Lithium Project; USA: 100% North American Lithium). It also owns or has stakes in development projects in the USA and Ghana.

Type: Producer / developer

FY25 production: ELV reported 205kt of spodumene concentrate production in FY25. FY26 guidance is 195-210kt (SC5.3) at a cost of A$1,175-1,275/t. Full production is expected to be 315kt per annum (SC5.4), but the company has not yet put a timeframe on when this might be achieved.

Why it matters in an upcycle: When lithium prices rise, producers tend to react quickly — particularly those with net cash / minimal debt and demonstrable unit-cost momentum (reported cost reductions and/or clearly articulated cost-down pathways).

PMET Resources (ASX: PMT)

%20price%20chart%206%20Jan%202025.png)

Last price: $0.635

Market cap: $346 million

Operations / geography: Shaakichiuwaanaan Project (spodumene, Canada).

Type: Explorer

Stage: Drilling / resource delineation (exploration-driven, with studies to follow as resource confidence grows).

Why it matters in an upcycle: In higher price regimes, the market pays more for scale potential and favourable jurisdiction — and PMET offers both. Explorers with credible resources upgrade potential can re-rate sharply on drilling results.

Core Lithium (ASX: CXO)

%20price%20chart%206%20Jan%202025.png)

Last price: $0.295

Market cap: $784 million

Operations / geography: Finniss Lithium Operation (spodumene, Northern Territory).

Type: Producer / restart candidate (Finiss was placed on care and maintenance due to low lithium prices in mid-2024).

FY25 production: CXO completed and released a restart study in May 2025 outlining options to reposition Finniss as a lower-cost, longer-life operation with potential underground mining development and enhanced processing. The company has not made a FID to restart production but recent filings suggest it is “rapidly advancing” towards one as the site remains in a fully compliant and restart ready state. There is no publicly stated target year for when full production will resume. Restart execution remains contingent on market conditions, funding, and board approval.

Why it matters in an upcycle: CXO is a classic option on a rising lithium price — if prices rise enough to justify sustained operations, the stock can re-rate quickly as it will likely get its product to market long before those in the exploration and development phases. If not, dilution / financing risk stays front-of-mind as mine restarts typically require substantial amounts of capital.

Ioneer (ASX: INR)

%20price%20chart%206%20Jan%202025.png)

Last price: $0.215

Market cap: $575 million

Operations / geography: Rhyolite Ridge lithium-boron project (spodumene, USA).

Type: Developer

Stage: Permitting / financing / development pathway.

Why it matters in an upcycle: A stronger lithium price can support financing momentum; INR also carries “jurisdiction premium” potential if strategic capital partners emerge — the US strategic-supply narrative is a meaningful valuation lever.

Wildcat Resources (ASX: WC8)

%20price%20chart%206%20Jan%202025.png)

Last price: $0.38

Market cap: $514 million

Operations / geography: Tabba Tabba Project (flagship) and Bolt Cutter Project (spodumene, Western Australia)

Type: Explorer / developer

Stage: Drilling-led (value driven by discovery, resource definition) but claims to be “progressing well” towards a DFS at Tabba Tabba which has a MRE* of 74.1Mt at 1.0% Li2O3 using a 0.45% cut-off.

Why it matters in an upcycle: Explorers with momentum often attract capital faster when commodity prices improve — especially those with substantial in-ground resources.

Galan Lithium (ASX: GLN)

%20price%20chart%206%20Jan%202025.png)

Last price: $0.350

Market cap: $402 million

Operations / geography: Hombre Muerto West (HMW) Project (brine, Argentina).

Type: Developer

Stage: HMW is permitted with a short path to production (H1 2026), with mining and global sales permits for Phases 1 and 2. Production up to 21ktpa LCE in Phase 2.

Why it matters in an upcycle: Brine projects live and die by flow sheet confidence and capex realism. If lithium pricing strengthens, the market becomes more forgiving on funding risk and more receptive to brine optionality — provided execution risk is clearly managed. HMW is a global top 10 lithium asset by mineral resources.

Lake Resources (ASX: LKE)

%20price%20chart%206%20Jan%202025.png)

Last price: $0.15

Market cap: $345 million

Operations / geography: Kachi Project (brine, Argentina).

Type: Developer

Stage: Studies (DFS and FEED* completed) / permitting / strategic partnering with the goal of reaching a FID. DFS proposes 8.2Mt LCE Measured & Indicated resource.

Why it matters in an upcycle: Project structure and technology approach are key swing factors for LKE. It is leveraged to sentiment on brines and funding appetite. In stronger lithium markets, credible partners and clearer pathways to construction tend to drive the re-rating.

Argosy Minerals (ASX: AGY)

%20price%20chart%206%20Jan%202025.png)

Last price: $0.125

Market cap: $193 million

Operations / geography: Rincon Lithium Project 77.5% (brine, Argentina)

Type: Developer / early production optionality

Stage: Progressing 12ktpa LCE project development engineering and feasibility works toward achieving a construction-ready stage. Working towards a FID.

Why it matters in an upcycle: Project milestones and partner interest matter more than near-term lithium spot moves for late-stage developers. Having said that, rising prices tend to pull capital back toward the “next wave” of producers — because any improvement in realised price assumptions can materially change NPV math and funding feasibility.

Global Lithium Resources (ASX: GL1)

%20price%20chart%206%20Jan%202025.png)

Last price: $0.645

Market cap: $169 million

Operations / geography: Manna Lithium Project (spodumene, Western Australia).

Type: Explorer / developer

Stage: Drilling / optimised DFS delivered, progressing toward a FID some time this year. Manna has a MRE of 51.6Mt at 1% Li2O3 using a 0.4% cut-off.

Why it matters in an upcycle: GL1’s leverage is primarily to market risk appetite and tangible project de-risking.

Winsome Resources (ASX: WR1)

%20price%20chart%206%20Jan%202025.png)

Last price: $0.510

Market cap: $124 million

Operations / geography: Adina Lithium Project (spodumene, Canada)

Type: Explorer

Stage: Drilling / resource growth. Scoping Study completed in 2024, with typical pathway required from here: PFS / DFS → permitting / partnering → FID).

Why it matters in an upcycle: In stronger lithium markets, investors tend to pay up for jurisdiction (North America) + scale potential; WR1’s catalyst set is exploration results and credible project progression.

CONCLUSION — INVARIABLY, “THIS TIME” IS NEVER DIFFERENT!

In markets, price is often the cleanest signal we have. When prices are rising steadily, there is usually a reason — and when multiple, coherent narratives emerge to explain that rise, the signal tends to strengthen rather than weaken. Lithium’s recent resurgence ticks both boxes, at least for now.

History also offers a cautionary reminder: the most reliable cure for high prices is higher prices, as capital floods in and supply inevitably responds. The lithium industry is far better placed in this fledgling upswing to do exactly that than it was in past early-cycle rallies, when capital constraints and execution bottlenecks limited its response.

Bulls will argue “this time is different” — that even with greater supply-side capacity, demand growth has finally reached critical mass, threatening a sustained, perhaps runaway, expansion. My experience suggests the sensible approach is simpler: make hay while the sun is shining but never become so wedded to a persuasive narrative that you stop listening to the market.

Nobody wants to be left holding the bag when the trend turns — and lithium has shown us how quickly, and brutally, that can happen.

References:

[1] UBS — Australian Resources Gearing up for more, 12 December 2025

[2] UBS — Mining Strategy | On the Road: China trip feedback, 21 November 2025.

[3] Canaccord Genuity — Lithium | Upgrading BESStimates, 19 November 2025.

[4] Macquarie — Critical Minerals Chronicle MIIT clearing the way for higher lithium prices, 1 December 2025.

[5] Morgan Stanley — DataDig: (Li)ft Off?, 8 December 2025.

[6] RBC Capital Markets — China Lithium: Anti-Involution, Royalties and the End of Uneconomic Supply, 12 November 2025

* DFS = Definitive Feasibility Study; FID = Final Investment Decision; MRE = Mineral Resource Estimate; FEED = Front-end engineering design. Read this article on the stages of mining project development for more information.