Oil price calamity! ASX 200 plunges, but amidst the carnage, Woodside, Santos and other ASX energy stocks are rising

Oil has surged above US$100, slamming the ASX. But energy stocks are rising. Here are the key ASX oil, LNG, and fuel names to watch.

Source: Shutterstock

Mentioned

KEY POINTS

- Oil prices have surged above US$100 per barrel as Middle East tensions threaten global supply — triggering one of the largest single-day spikes in the commodity in years.

- While the ASX 200 tumbles, energy stocks are gaining strength as investors rush into companies positioned to benefit from higher oil and LNG prices.

- We break down the major ASX energy players, their production exposure, and the latest broker ratings and price targets to see which stocks could benefit most.

Markets woke to a geopolitical shock this morning. Escalating tensions in the Middle East have sent energy markets into overdrive, with traders scrambling to price in the risk of supply disruptions across one of the world’s most critical oil-producing regions.

The reaction has been swift and brutal. Oil prices have surged and global equity markets have buckled as investors digest the implications of another major geopolitical flashpoint.

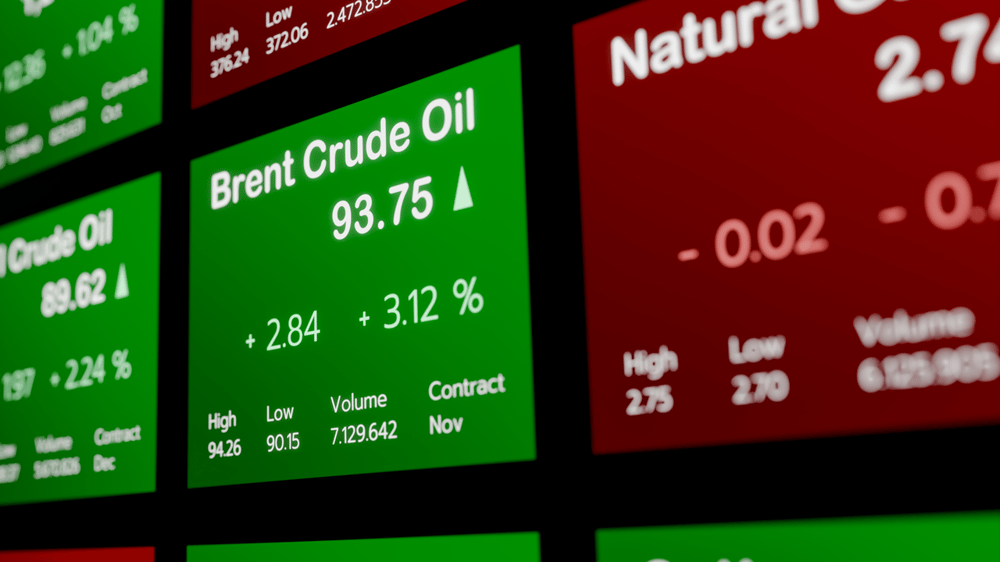

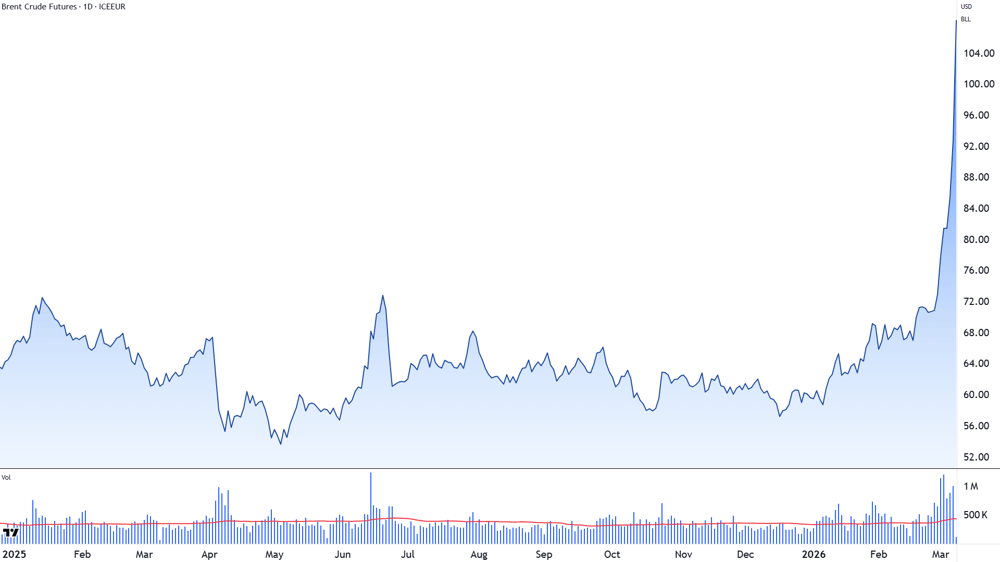

The Brent crude oil spot price has blasted through US$100 per barrel, briefly touching US$109 in early trade — its highest level since March 2022, when Russia’s invasion of Ukraine sent energy markets into turmoil. Moves of this magnitude are rare outside periods of major geopolitical stress, highlighting just how seriously the market is treating the latest developments.

Brent Crude Oil Futures chart since 1 Jan 2025

Against that backdrop, the ASX 200 has slumped roughly 4% in early trade, marking the benchmark’s biggest one-day drop since the chaotic period surrounding Donald Trump’s reciprocal tariff escalation last April, and before that, the darkest days of the COVID-19 market crash. Investors are rapidly rotating away from risk as higher energy costs threaten to squeeze global growth and corporate margins.

But amid the carnage, one corner of the market is shining brightly.

Energy stocks are surging as the oil price spike transforms the sector’s earnings outlook almost instantly. For companies producing, refining, or exporting crude and petroleum products, every additional dollar in the oil price can translate directly into higher cash flow.

For investors willing to lean into the momentum, the ASX energy sector is suddenly back in the spotlight. So which stocks stand to benefit most from the oil price surge — and which ones are already priced for perfection?

To answer that question, we’ll walk through the major ASX-listed oil and downstream energy companies one by one, examining how each business is positioned to benefit from higher crude prices.

For each stock, we’ll review its core operations and the latest broker research from major investment banks, including consensus ratings and price targets to gauge whether analysts currently see them as buys, holds, or sells in the new oil-price environment.

The ASX stocks poised to cash in on crude’s calamity

The latest surge in oil prices is being driven by one simple factor: supply risk. Escalating conflict involving Iran has effectively shut down vessel transit through the Strait of Hormuz, one of the world’s most important oil shipping routes, forcing traders to rapidly reprice the probability of a prolonged disruption to global crude and LNG flows.

For investors, that means the spotlight swings firmly onto ASX-listed oil and gas producers and downstream refiners and retailers. In the list below, we’ve focused on companies already in production — those best positioned to capture the immediate upside from higher crude and LNG prices — rather than waiting years for projects to be developed. They are listed in order of market capitalisation, largest to smallest.

Woodside Energy (WDS)

Market Capitalisation: $58.5 billion

%20chart%20as%20at%209%20March%202026.png)

Woodside Energy (WDS) chart

Operations

Pluto LNG (Western Australia) — Woodside operates and holds 90% of Pluto LNG in the Pilbara. The project processes gas from the offshore Pluto and Xena fields into LNG, with additional domestic gas and trucked LNG supply.

North West Shelf Project (Western Australia) — Woodside is operator and has an aggregate interest of 33.33% across most of the joint ventures, with some interests differing by asset. The project is a major Pilbara-based LNG and domestic gas hub supplying both Australian and export markets.

Sangomar (offshore Senegal) — Woodside is operator of Senegal’s first major oil project, with an 82% interest in the Sangomar exploitation area. The field, around 100 kilometres south of Dakar, produces oil from offshore reservoirs.

Production

Woodside reported record 2025 production of 198.8 million barrels of oil equivalent at the group level, supported by strong output from Sangomar and high reliability at its LNG assets.

Dividend yield

Based on Woodside Energy’s trailing 12-month dividend payout of $1.653 per share and its closing price of $30.75 on Friday 6 March, its dividend yield is 5.3% p.a.

Woodside Energy’s last two dividends were 100% franked.

Woodside Energy Broker Consensus

%20Broker%20Consensus%20as%20at%209%20March%202026.png)

Woodside Energy Broker Consensus

To obtain a stock’s Broker Consensus Rating, we assign a value of +1 to any rating better than HOLD/NEUTRAL/MARKETWEIGHT, a value of 0 for any rating equivalent to HOLD/NEUTRAL/MARKETWEIGHT, and a value of -1 to any rating worse than HOLD/NEUTRAL/MARKETWEIGHT.

We then take the average of all assigned rating values and assign a Broker Consensus Rating of BUY to values greater than +0.5, a rating of HOLD for values between -0.5 and +0.5, and a rating of SELL for values less than -0.5.

The Broker Consensus Target is simply the average of the target prices we have on file for each broker. Typically, brokers define their target prices as a 12-month forecast. Each target price is based on fundamental valuation assumptions.

Woodside Energy’s Broker Consensus Rating is +0.2, resulting in a Broker Consensus Rating of HOLD. Its Broker Consensus Target is $29.25. This suggests brokers collectively believe the stock is around 4.9% overvalued based upon its closing price on Friday 6 March of $30.75.

Santos (STO)

Market Capitalisation: $24.2 billion

%20chart%20as%20at%209%20March%202026.png)

Santos (STO) chart

Operations

Gladstone LNG (Queensland, Australia) — Santos is operator and holds a 30% interest in the coal seam gas-to-LNG export project on Curtis Island, supplied from the Bowen and Surat basins.

PNG LNG (Papua New Guinea) — Santos holds a 42.5% interest in the ExxonMobil-operated LNG project exporting gas to Asian markets.

Darwin LNG / Barossa (Northern Territory, Australia) — Santos is operator with roughly 50% ownership of the Barossa gas field, which will supply the Darwin LNG plant as the Bayu-Undan field declines.

Pikka Phase 1 (Alaska, USA) — Santos holds a 51% stake in the oil development on Alaska’s North Slope targeting first production in the mid-2020s.

Production

Santos reported full-year 2025 production of 87.7 million barrels of oil equivalent (mmboe), near the upper end of guidance.

Dividend yield

Based on Santos’ full-year dividend of $0.348 per share for 2025 and its closing price of $7.46 on Friday 6 March, its dividend yield is 4.6% p.a.

Santos’ last two dividends averaged 5% franking.

Santos Broker Consensus

%20Broker%20Consensus%20as%20at%209%20March%202026.png)

Santos Broker Consensus

Santos' Broker consensus rating is +0.8, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $7.75. This suggests brokers collectively believe the stock is around 3.9% undervalued based upon the closing price on Friday 6 March of $7.46.

Origin Energy (ORG)

Market Capitalisation: $20.6 billion

%20chart%20as%20at%209%20March%202026.png)

Origin Energy (ORG) chart

Operations

Australia Pacific LNG (Queensland, Australia) — Origin holds a 27.5% interest in the coal seam gas-to-LNG export project operated by ConocoPhillips. Gas is sourced from the Surat and Bowen basins and exported via the Curtis Island LNG facility near Gladstone.

Integrated energy business (Australia) — Origin also operates a large electricity and gas retail and power generation portfolio across Australia’s National Electricity Market.

Production

Origin Energy’s share of production from Australia Pacific LNG was approximately 69 petajoules of gas in FY2025, representing its primary upstream energy production exposure.

Dividend yield

Based on Origin Energy’s trailing 12-month dividend payout of $0.60 per share and its closing price of $11.94 on Friday 6 March, its dividend yield is 3.7%.

Origin Energy’s last two dividends were 100% franked.

Origin Energy Broker Consensus

%20Broker%20Consensus%20as%20at%209%20March%202026.png)

Origin Energy Broker Consensus

Origin Energy’s Broker Consensus Rating is +0.33, resulting in a Broker Consensus Rating of HOLD. Its Broker Consensus Target is $12.35. This suggests brokers collectively believe the stock is around 3.5% undervalued based upon the closing price on Friday 6 March of $11.94.

Ampol (ALD)

Market Capitalisation: $7.4 billion

%20chart%20as%20at%209%20March%202026.png)

Ampol (ALD) chart

Operations

Lytton Refinery (Queensland, Australia) — Ampol owns and operates the Lytton oil refinery in Brisbane, one of Australia’s last remaining fuel refineries, producing petrol, diesel, jet fuel and other refined petroleum products.

Fuel supply and retail network (Australia and New Zealand) — Ampol operates a large fuel import, distribution and retail network, supplying transport fuels through a national network of service stations and commercial fuel customers.

Z Energy (New Zealand) — Ampol owns 100% of Z Energy, a leading fuel distributor and retailer supplying petrol, diesel and aviation fuels across New Zealand.

Production

Ampol’s Lytton refinery processes around 109,000 barrels of crude oil per day, producing refined transport fuels for the domestic market.

Dividend yield

Based on Ampol’s trailing 12-month dividend payout of $1.00 per share and its closing price of $30.96 on Friday 6 March, its dividend yield is 3.2%.

Ampol’s last two dividends were 100% franked.

Ampol Broker Consensus

%20Broker%20Consensus%20as%20at%209%20March%202026.png)

Ampol Broker Consensus

Ampol’s Broker Consensus Rating is +1.0, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $34.36. This suggests brokers collectively believe the stock is around 11.0% undervalued based upon the closing price on Friday 6 March of $30.96.

Viva Energy (VEA)

Market Capitalisation: $3.4 billion

%20chart%20as%20at%209%20March%202026.png)

Viva Energy (VEA) chart

Operations

Geelong Refinery (Victoria, Australia) — Viva Energy owns and operates the

Geelong oil refinery, Australia’s second remaining refinery, processing crude oil into petrol, diesel, jet fuel and other refined products for the domestic market.

Fuel supply and retail network (Australia) — Viva Energy imports, distributes and markets fuels across Australia through a national fuel distribution and retail network, including its long-term Shell-branded service station network.

Commercial fuels and aviation (Australia) — Viva Energy is a major supplier of aviation fuel and commercial fuels, servicing airports, transport operators and industrial customers across the country.

Production

Viva Energy’s Geelong refinery processes around 120,000 barrels of crude oil per day, supplying refined fuels primarily to the Australian market.

Dividend yield

Based on Viva Energy’s trailing 12-month dividend payout of $0.067 per share and its closing price of $2.10 on Friday 6 March, its dividend yield is 3.2%.

Viva Energy’s last two dividends were 100% franked.

Viva Energy Broker Consensus

%20Broker%20Consensus%20as%20at%209%20March%202026.png)

Viva Energy Broker Consensus

Viva Energy’s Broker Consensus rating is +0.57, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $2.27. This suggests brokers collectively believe the stock is around 8.0% undervalued based upon the closing price on Friday 6 March of $2.10.

Beach Energy (BPT)

Market Capitalisation: $2.6 billion

%20chart%20as%20at%209%20March%202026.png)

Beach Energy (BPT) chart

Operations

Western Flank oil fields (Cooper Basin, Australia) — Beach holds a 100% interest in several producing oil fields across the South Australian Cooper Basin, which form a key source of the company’s oil production.

Waitsia Gas Project (Perth Basin, Western Australia) — Beach holds a 50% interest in the Waitsia gas field and Stage 2 development, alongside operator Mitsui E&P Australia. Gas from Waitsia is processed at the Waitsia Gas Plant and supplied to the domestic market.

Otway Basin gas assets (Victoria and South Australia) — Beach operates and holds significant interests in multiple offshore and onshore gas fields, supplying gas to the Australian east coast market.

Production

Beach Energy reported FY2025 production of approximately 20.2 million barrels of oil equivalent at the group level across its Cooper, Otway and Perth Basin assets.

Dividend yield

Based on Beach Energy’s trailing 12-month dividend payout of $0.07 per share and its closing price of $1.15 on Friday 6 March, its dividend yield is 6.1%.

Beach Energy’s last two dividends were 100% franked.

Beach Energy Broker Consensus

%20Broker%20Consensus%20as%20at%209%20March%202026.png)

Beach Energy (BPT) Broker Consensus

Beach Energy’s Broker Consensus rating is -0.38, resulting in a Broker Consensus Rating of HOLD. Its Broker Consensus Target is $1.11. This suggests brokers collectively believe the stock is around 3.1% overvalued based upon the closing price on Friday 6 March of $1.15.

Karoon Energy (KAR)

Market Capitalisation: $1.4 billion

%20chart%20as%20at%209%20March%202026.png)

Karoon Energy (KAR) chart

Operations

Baúna Oil Field (Santos Basin, Brazil) — Karoon holds a 100% interest in the Baúna offshore oil project, located around 210 kilometres off the coast of Brazil. Production is processed via the FPSO Cidade de Itajaí, with crude exported to international markets.

Patola Field (Santos Basin, Brazil) — Karoon holds a 100% interest in the Patola oil field, a subsea tie-back development that produces via the Baúna infrastructure.

Neon Project (Brazil) — Karoon holds a 100% interest in the Neon offshore oil discovery in the Santos Basin, which is currently being assessed as a potential future development.

Production

Karoon Energy reported 2025 production of approximately 9.8 million barrels of oil equivalent, reflecting output primarily from the Baúna and Patola fields in Brazil.

Dividend yield

Karoon Energy does not currently pay a dividend, with cash flows largely reinvested into development and exploration activities.

Karoon Energy Broker Consensus

%20Broker%20Consensus%20as%20at%209%20March%202026.png)

Karoon Energy Broker Consensus

Karoon Energy’s Broker Consensus Rating is +0.50, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $1.99. This suggests brokers collectively believe the stock is around 9.5% undervalued based upon the closing price on Friday 6 March of $1.815.

Amplitude Energy (AEL)

Market Capitalisation: $786 million

%20chart%20as%20at%209%20March%202026.png)

Amplitude Energy (ALD) chart

Operations

Sole Gas Project (Gippsland Basin, Australia) — Amplitude Energy holds a 100% interest in the Sole offshore gas field, located in the Gippsland Basin offshore Victoria. Gas is processed at the Orbost Gas Processing Plant and supplied into the east coast domestic gas market.

East Coast gas portfolio (Australia) — The company also holds interests across several offshore Gippsland Basin exploration and appraisal permits, targeting future domestic gas supply opportunities.

Production

Amplitude Energy reported FY2025 production of approximately 9.0 petajoules of gas, sourced primarily from the Sole gas field supplying the east coast market.

Dividend yield

Amplitude Energy does not currently pay a dividend, with cash flows focused on supporting operations and balance sheet strength.

Amplitude Energy Broker Consensus

%20Broker%20Consensus%20as%20at%209%20March%202026.png)

Amplitude Energy Broker Consensus

Amplitude Energy’s Broker Consensus Rating is +0.75, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $3.26. This suggests brokers collectively believe the stock is around 24.3% undervalued based upon the closing price on Friday 6 March of $2.62.