Markets at Midday: Big four banks drive ASX 200 sharply higher, DigiCo and Infratil rally on data centre deals

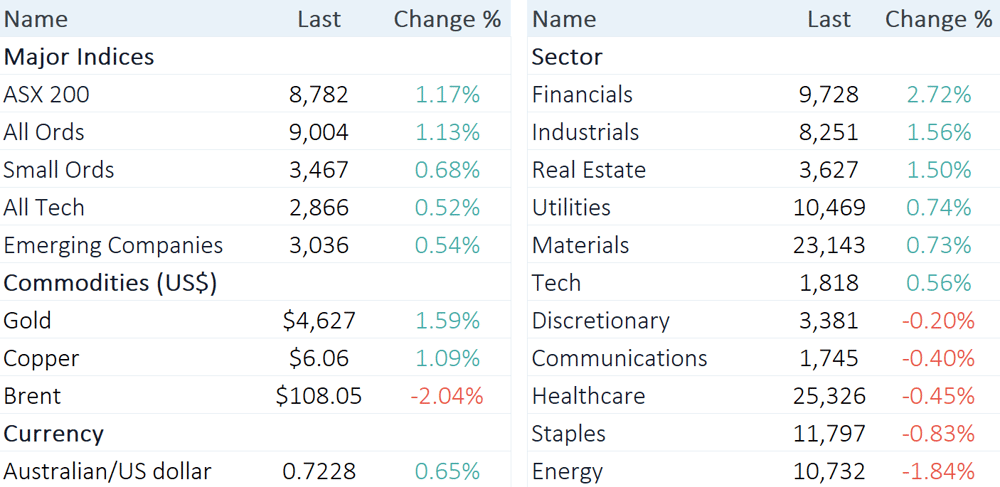

The S&P/ASX 200 is trading 101 pts higher (+1.17%) at noon.

Source: Market Index

The S&P/ASX 200 is trading 101 pts higher (+1.17%) at noon.

It feels like one of the strongest sessions in a long while, though a move that's largely driven by a massive rally for banks – with Westpac up 4.3%, NAB and ANZ both up ~3% and CBA trading 2.8% higher. The Aussie 10-year slipped 6 bps to 4.95% on Tuesday, with Real Estate stocks trading sharply higher today, to a fresh two-month high. On the flip side, consumer-facing sectors like Staples (-0.8%), Healthcare (-0.4%), Telcos (-0.40%) and Discretionary (0.2%) are trading lower.

On a side note, one of the more interesting bits of corporate commentary today comes from JB Hi-Fi CEO, Nick Wells: “As we enter the important end of financial year trading period, in the technology categories we are seeing significant supplier component related cost increases and stock availability shortages, along with heightened competitive activity."

Let’s dive in

Midday market summary

Today’s big story: Infratil and Digico deals

Two material data centre catalysts hit the market, with DigiCo announcing a US$750 million asset sale, and Infratil signing the largest data centre contract in Australian history.

In a nutshell:

DigiCo Infrastructure REIT (DGT): Announced the binding US$750m sale of its Chicago CHI1 facility at a ~5% premium to the Nov-24 purchase price, freeing ~$360m in net cash proceeds and dropping gearing from 36% to 17%. Capital is being redeployed into the 88MW SYD1 expansion, while DGT also plans to explore enhanced distributions and monetise the Los Angeles sites.

Infratil (IFT): CDC (49.7% owned by IFT) signed a 30-year, 555MW contract with a US investment grade customer, lifting total contracted capacity beyond 1GW. FY27 EBITDAF guidance unchanged at $680m-$720m but FY28 EBITDAF projected to surpass $1bn, with annualised contracted EBITDAF reaching ~$2bn once fully deployed post-FY28. No additional shareholder equity required to fund the new capacity, with FY27 capex (ex-land) stepping up to $3.8bn-$4.2bn.

We're seeing a very strong share price response, with DigiCo shares up 22.4% (now up 4.7% YTD), while Infratil is up 12.7% to fresh all-time highs.

Some food for thought:

DigiCo exercising some capital discipline here, offloading an asset at a decent premium while deleveraging its balance sheet and outlining plans for potential capital management

This sets a strong precedence for current assets, with management exploring options for its LAX1 and LAX2 projects, while continuing to build out its Kansas City, Dallas Fort Worth and Australian assets

Infratil noted the massive 555MW deal is "within CDC’s current growth plan and doesn’t require further shareholder equity." The development programme will be funded via existing cash, committed debt facilities and further debt/hybrid funding.

Must read announcements

AGL Energy (AGL): Lifts lower end of FY26 guidance on strong operational performance

Atlas Arteria (ALX): Board rejects IFM takeover offer as too low and opportunistic

Infratil (IFT): Signs largest data centre contract in Australia's history at 555MW

Computershare (CPU): Reaffirms FY26 Management EPS, lifts margin income guidance

DigiCo Infrastructure REIT (DGT): Agrees US$750m sale of Chicago CHI1 to fund SYD1 expansion

JB Hi-Fi (JBH): Q3 sales growth maintained but Q4 outlook clouded by supplier cost pressure

Capital raisings

Alma Metals (ALM): $4m raise to accelerate Briggs Copper Project

BWP Trust (BWP): Capital deployment and equity raising

Decidr AI Industries (DAI): Successful completion of $15m placement

Nanollose (NC6): $1.58m raised through option conversions

Odessa Minerals (ODE): Successful $2.65m placement

Thinking out loud: Regis and Vault merger

The Regis Resources and Vault Minerals merger-of-equals has drawn a rather negative market reaction – Vault experienced a 3% gain on Tuesday but down 8.4% today and Regis is down ~14% over the last two days. Here are the key details and some food for thought:

Regis holders will own ~51% of the combined company and Vault holders with the remaining ~49%

Combined company to produce over 700koz gold per annum from five high-quality WA assets, positioning it as the 3rd largest primary ASX-listed gold producer

VAU trading at a modest premium to the implied offer price suggests low perceived regulatory or interloper risk, with the deal's all-scrip structure (no tax implications) and unanimous board support pointing to a clean path through

Analysts see the major appeal as scale creation, balance sheet strength and significant corporate tax benefits (>$500m in tax losses), though limited operational synergies given the geographic and operational footprint

Combined production base of ~750koz+ pa post-expansions, with combined FCF of ~$1.71bn implying EV/FCF of ~5.2x in 2026, falling to ~4.0-5.5x in FY28 at sustained ~A$6,300/oz gold prices, which some commentators argue looks cheap if bullish gold

Intraday winners and losers

Lithium, defence and banks are catching a rather aggressive bid, while investors dump Regis/Vault, uranium and energy stocks.

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

ELV | Elevra Lithium | 7.00% | $13.45 |

LTR | Liontown | 4.73% | $2.55 |

AMP | AMP | 3.86% | $1.53 |

DRO | Droneshield | 3.34% | $3.87 |

EOS | Electro Optic Systems | 3.23% | $10.22 |

DOW | Downer Edi | 3.15% | $8.02 |

NWH | NRW | 3.10% | $6.66 |

ASB | Austal | 2.94% | $4.20 |

WBC | Westpac | 2.73% | $39.34 |

IGO | IGO | 2.66% | $7.91 |

ANZ | ANZ Group | 2.47% | $37.10 |

LYC | Lynas Rare Earths | 2.45% | $19.26 |

Data as at 12:03 pm AEST, % change measures the move from today's open price

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

RRL | Regis Resources | -8.64% | $6.24 |

JBH | JB Hi-Fi | -5.87% | $73.34 |

VAU | Vault Minerals | -5.71% | $4.29 |

ALK | Alkane Resources | -4.88% | $1.42 |

A2M | A2 Milk Company | -4.87% | $6.44 |

DYL | Deep Yellow | -4.76% | $1.70 |

MFG | Magellan Financial Group | -4.73% | $9.16 |

YAL | Yancoal Australia | -3.75% | $7.07 |

PDN | Paladin Energy | -3.66% | $11.58 |

NHC | New Hope Corporation | -2.99% | $5.35 |

Data as at 12:03 pm AEST, % change measures the move from today's open price

Broker Moves

Computershare (CPU)

Upgraded to neutral from underperform at Bank of America; Price Target: $34.20 from $32.50

Flight Centre Travel Group (FLT)

Retained at outperform at CLSA; Price Target: $16.70

Retained at positive at E&P; Price Target: $19.14 from $19.66

Retained at overweight at Jarden; Price Target: $16.80 from $16.70

Retained at buy at Jefferies; Price Target: $15.00 from $17.50

Retained at buy at Morgans; Price Target: $14.55 from $18.05

Nine Entertainment Co. Holdings (NEC)

Upgraded to buy from overweight at Jarden; Price Target: $1.15 from $1.30

Sigma Healthcare (SIG)

Downgraded to accumulate from buy at Morgans; Price Target: $3.30 from $3.36

The Lottery Corporation (TLC)

Downgraded to equal-weight from overweight at Morgan Stanley; Price Target: $5.70

Universal Store Holdings (UNI)

Retained at buy at Bell Potter; Price Target: $9.30 from $10.50

Retained at overweight at Jarden; Price Target: $8.80 from $10.00

Retained at buy at Morgans; Price Target: $9.50 from $9.60

Retained at buy at UBS; Price Target: $9.00 from $9.50

Westpac Banking Corporation (WBC)

Retained at hold at CLSA; Price Target: $34.90 from $38.20

Downgraded to sell from underweight at Jarden; Price Target: $31.00 from $32.00

Retained at underweight at JPMorgan; Price Target: $35.90 from $37.30

Retained at neutral at UBS; Price Target: $40.00

Wisetech Global (WTC)

Retained at buy at Bell Potter; Price Target: $78.75

Retained at outperform at CLSA; Price Target: $116.00

Retained at buy at Jefferies; Price Target: $72.00

Retained at outperform at Macquarie; Price Target: $97.70