News | Market Wraps

Evening Wrap: ASX 200 gains despite disturbing inflation report, gold and consumer stocks lead, uranium, lithium and coal stocks lag

The S&P/ASX 200 closed 47.3 points higher, up 0.57%.

Mentioned

The S&P/ASX 200 closed 47.3 points higher, up 0.57%.

Stocks go up and stocks go down. We know that bit. Generally, they tend to go up on good news and down on bad. So today was encouraging given Aussie stocks digested a rather nasty October inflation report – and still went up.

Having said that, there's plenty of news driving local stock prices at the moment, including the fallout from yesterday's announcement of the first round of President-elect Trump's new tariffs, as well as today's modest de-escalation of part of the conflict in the Middle East.

On the first point, US stocks largely shrugged off the tariff news, and on the second, lower crude oil prices and a smidge less uncertainty for markets generally meant we enjoyed a modest relief rally today.

Gold stocks bounced back, but consumer focussed, telecommunications and techonology, financial, and real estate stocks also prospered. Laggards? Not many, Energy stocks weren't great – particularly coal and uranium plays, and Healthcare ended with only a tiny gain.

Click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all of the key upcoming economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on the major ASX Sectors in today's ChartWatch.

Let's dive in!

Today in Review

Wed 27 Nov 24, 5:15pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,406.7 | +0.57% |

| All Ords | 8,659.6 | +0.55% |

| Small Ords | 3,179.8 | +0.68% |

| All Tech | 3,915.3 | +0.60% |

| Emerging Companies | 2,288.0 | +0.16% |

Currency | ||

| AUD/USD | 0.6473 | -0.03% |

US Futures | ||

| S&P 500 | 6,036.25 | -0.03% |

| Dow Jones | 44,969.0 | +0.04% |

| Nasdaq | 20,962.25 | -0.15% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Consumer Discretionary | 3,944.4 | +1.03% |

| Communication Services | 1,702.6 | +0.87% |

| Financials | 8,944.6 | +0.84% |

| Information Technology | 2,846.8 | +0.75% |

| Real Estate | 4,079.1 | +0.74% |

| Utilities | 9,056.8 | +0.72% |

| Industrials | 7,732.7 | +0.39% |

| Consumer Staples | 11,702.9 | +0.39% |

| Energy | 8,621.5 | +0.25% |

| Materials | 16,715.7 | +0.17% |

| Health Care | 45,197.7 | +0.02% |

Markets

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 47.3 points higher at 8,406.7, 0.57% from its session low and just 0.13% from its high. In the broader-based S&P/ASX 300 (XKO), advancers beat decliners by a tidy 184 to 90.

The Gold (XGD) (+2.0%) sub-index rebounded today on a modest rise in the gold price in Asia (but only a dead cat bounce in the US overnight versus Monday's big dip – see yesterday's ChartWatch for details).

A worse than expected October CPI report, that showed a worrying uptick in underlying inflation (to +3.5% p.a. from +3.2% p.a. in September), did little to sink consumer Consumer Discretionary (XDJ) (+1.0%), nor the rest of the market for that matter.

Interest rate sensitives / high-PE sectors like Communication Services (XTJ) (+0.87%) and Information Technology (XIJ) (+0.75%), and bond market proxies like Real Estate (XRE) (+0.75%) and Utilities (XUJ) (+0.72%), also did well. Financials (XFJ) (+0.84%) rebounded from yesterday's rout.

Most likely, investors are balancing that stronger than expected October inflation result against major external factors like Trump's tariffs, plus a welcome de-escalation of the conflict in the Middle East. The latter pushed the prices of key energy commodities lower on Tuesday, and this triggered weakness in several of our oil and gas, coal, and uranium stocks.

Materials (XMJ) (+0.17%) more generally also underperformed the benchmark S&P/ASX 200 today, as did the Health Care (XHJ) (+0.02%) sector, but both sectors (indeed all 11 major ASX sectors) still managed to scrape in with a gain.

I have a full wrap of strongest versus weakest sectors for you in ChartWatch below.

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

WEB Travel (WEB) | $4.80 | +$0.57 | +13.5% | +19.4% | -17.4% |

Qoria (QOR) | $0.465 | +$0.05 | +12.0% | +10.7% | +106.7% |

Brainchip (BRN) | $0.265 | +$0.025 | +10.4% | +15.2% | +43.2% |

PYC Therapeutics (PYC) | $2.00 | +$0.13 | +7.0% | +14.3% | +162.8% |

Life360 (360) | $24.70 | +$1.45 | +6.2% | +10.9% | +224.6% |

Ora Banda Mining (OBM) | $0.700 | +$0.035 | +5.3% | -24.7% | +268.4% |

Aussie Broadband (ABB) | $3.75 | +$0.17 | +4.7% | -0.3% | -0.3% |

Chalice Mining (CHN) | $1.390 | +$0.06 | +4.5% | -25.1% | -10.3% |

Ampol (ALD) | $29.64 | +$1.24 | +4.4% | +4.7% | -11.7% |

Lendlease Group (LLC) | $7.11 | +$0.27 | +3.9% | +5.2% | +10.2% |

Polynovo (PNV) | $2.14 | +$0.08 | +3.9% | +2.4% | +58.5% |

Catapult Group International (CAT) | $3.51 | +$0.13 | +3.8% | +43.3% | +209.3% |

Tabcorp (TAH) | $0.540 | +$0.02 | +3.8% | +12.5% | -27.0% |

Domino's Pizza Enterprises (DMP) | $32.55 | +$1.2 | +3.8% | -9.1% | -37.4% |

Genesis Minerals (GMD) | $2.52 | +$0.09 | +3.7% | +2.0% | +48.7% |

Clarity Pharmaceuticals (CU6) | $5.95 | +$0.2 | +3.5% | -17.0% | +350.5% |

TPG Telecom (TPG) | $4.50 | +$0.15 | +3.4% | -0.9% | -3.4% |

Premier Investments (PMV) | $35.23 | +$1.14 | +3.3% | +3.8% | +49.2% |

The A2 Milk Company (A2M) | $5.71 | +$0.18 | +3.3% | -2.1% | +45.3% |

Mesoblast (MSB) | $1.760 | +$0.055 | +3.2% | +29.4% | +370.0% |

AUB Group (AUB) | $32.08 | +$1. | +3.2% | +0.6% | +15.8% |

Spark New Zealand (SPK) | $2.68 | +$0.08 | +3.1% | -1.1% | -42.6% |

Jumbo Interactive (JIN) | $14.13 | +$0.41 | +3.0% | +8.9% | +4.1% |

Lovisa (LOV) | $28.47 | +$0.79 | +2.9% | -1.6% | +55.7% |

Nuix (NXL) | $6.34 | +$0.17 | +2.8% | -12.2% | +296.3% |

Today's strongest performing ASX stocks

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Vulcan Energy Resources (VUL) | $7.40 | -$0.74 | -9.1% | +38.8% | +226.0% |

WA1 Resources (WA1) | $16.05 | -$0.94 | -5.5% | +16.6% | +95.3% |

Pinnacle Investment Management Group (PNI) | $23.16 | -$1.24 | -5.1% | +18.9% | +159.9% |

Silex Systems (SLX) | $5.71 | -$0.25 | -4.2% | +15.1% | +70.4% |

Weebit Nano (WBT) | $2.67 | -$0.1 | -3.6% | +38.7% | -23.9% |

Yancoal Australia (YAL) | $6.19 | -$0.21 | -3.3% | -6.8% | +23.6% |

Fleetpartners Group (FPR) | $3.15 | -$0.1 | -3.1% | +3.6% | +15.4% |

Boss Energy (BOE) | $2.84 | -$0.09 | -3.1% | -17.0% | -34.3% |

Bluescope Steel (BSL) | $21.76 | -$0.67 | -3.0% | +3.2% | +7.7% |

MA Financial Group (MAF) | $6.26 | -$0.19 | -2.9% | -2.2% | +21.8% |

Graincorp (GNC) | $7.69 | -$0.22 | -2.8% | -15.4% | +2.5% |

Zip Co. (ZIP) | $3.26 | -$0.09 | -2.7% | +4.5% | +769.3% |

Bravura Solutions (BVS) | $1.540 | -$0.035 | -2.2% | +2.0% | +106.7% |

GQG Partners (GQG) | $2.24 | -$0.05 | -2.2% | -18.5% | +60.0% |

Whitehaven Coal (WHC) | $6.56 | -$0.14 | -2.1% | -5.7% | -9.9% |

James Hardie Industries (JHX) | $56.40 | -$1.2 | -2.1% | +10.0% | +20.5% |

Nufarm (NUF) | $3.87 | -$0.08 | -2.0% | +1.8% | -17.0% |

Gentrack Group (GTK) | $11.81 | -$0.23 | -1.9% | +29.2% | +154.5% |

Rpmglobal (RUL) | $3.10 | -$0.06 | -1.9% | +5.1% | +102.6% |

Sims (SGM) | $12.94 | -$0.24 | -1.8% | +0.5% | -5.6% |

Credit Corp Group (CCP) | $17.77 | -$0.31 | -1.7% | +3.0% | +39.9% |

Pilbara Minerals (PLS) | $2.43 | -$0.04 | -1.6% | -14.7% | -33.2% |

Qantas Airways (QAN) | $8.80 | -$0.14 | -1.6% | +8.2% | +67.3% |

Paladin Energy (PDN) | $8.17 | -$0.13 | -1.6% | -17.1% | -19.1% |

Arcadium Lithium (LTM) | $8.04 | -$0.11 | -1.4% | -3.1% | 0% |

Today's weakest ASX stocks

ChartWatch

S&P/ASX 200 (XJO)

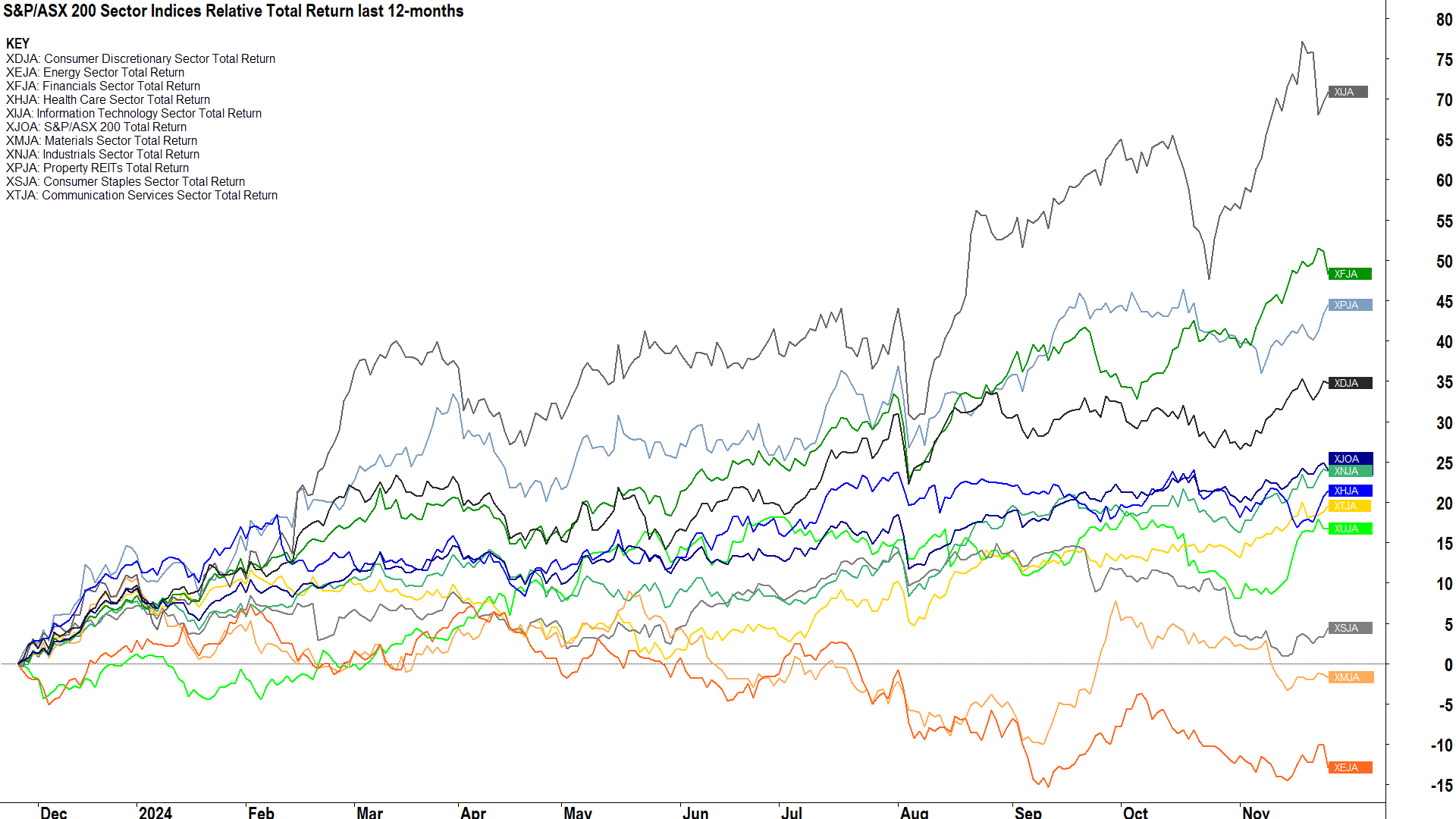

S&P-ASX 200 Sector Indices Relative Total Return last 12-months (click here for full size image)

{kind=link}

I ran this chart in my article on 4 of the ASX's most highflying tech stocks today. If you're interested in technical analysis, or just want a different view on how to interpret strong charts - then it's a must read.

What strikes me the most in the chart above, is it really does torpedo the investing concept of buy and hold. Or as I like to call it, buy, hold, hope and pray. That is, hope and pray that the stocks you're holding end up being the ones that don't tank over the next 12 months!

Within any stock market, especially our own, there are always going to be stocks and sectors that are outperforming in the present micro and macroeconomic environment – and those that aren't.

Your job as an investor, is to try and do your best to ensure that you hold as many of the winners as possible and dump or avoid as many of the losers as possible. Either you pay someone to do this for you, or you take on the responsibility yourself.

But for me, buying a bunch of stocks on Day 1 and holding on in hope that by Day 365 they're the best performers, is simply not an option.

With this in mind, let's do a super-quick run through the charts of the 11 major ASX sectors plus the Gold sub-index. I've put them into 3 groups: Demand-side Control, Equilibrium, and Supply-side Control.

Demand-side Control Group

Demand-side control group

5 very strong charts here. Perhaps financials and tech are showing a recent supply-side candle or two, but in neither case do I believe the well-established and strong short and long term uptrends shouldn't be trusted. As you peruse these groups, it will become clear to you the sectors the big fund managers are favouring and those that are being shunned.

You know me – I am a trend follower, not a prognosticator. I have no idea which sectors will fall into the demand-equilibrium-and-supply-side groups 365 days from now. Nor do I really care. I will follow the trends as they stand today, comforted by the fact that when the fingerprints of supply do eventually take a grip – I'll know exactly how to act.

Equilibrium Group

Equilibrium group

Gold is a relatively new entrant to this group – and despite today's bounce – thoroughly deserves to be here. Property is the closest to making the leap up to the Demand-side Control cohort, whilst Health Care and Utilities look very much stuck in the middle.

Supply-side Control Group

Supply-side control group

For those of you who have kept the faith in Energy and Resources (remember the "pray" part of the buy, hold, hope and pray technique?), looking at the charts above – you've no doubt been disappointed. These charts have been in decline for some time now, so this means you've had plenty of heads-up to act!

Looking forward, I'll let you decide whether the trends, price action, and candles are pointing to greater or lesser supply-side control in these charts. If in doubt about how my technical model works, check the Primer.

Staples is showing some signs of life, and whilst a gargantuan effort is still required to neutralise the long term downtrend, it is the closest of the three to moving up into the Equilibrium group.

Economy

Today

AUS Consumer Price Index (CPI) October

Headline: +2.1% p.a. vs +2.1% p.a. in September

Trimmed Mean: +3.5% p.a. vs +3.2% in September

Ignore the headline, it was skewed by government electricity bill credits (-35.6% p.a. change)

Only the trimmed mean matters and it went substantially in the wrong direction / remains stubbornly above the RBA's 2-3% target range

Food and beverages +3.3% p.a. (steady but Fruit and Vegetables +8.5% p.a.), Rents +6.7% p.a. (up from 6.6% p.a.), and Insurance +6.3% p.a. (up from +6.1% p.a.) still places Aussies are getting gouged with price increases going to be firmly on RBA's radar

Market response will be to push further out timing for first rate cut, was slated as June 2025 prior to this data.

(FYI, our Kiwi cousins enjoyed a 0.50% cut today to take their RBNZ official cash rate to 4.25% - now below the RBA's 4.35%)

Later this week

Thursday

00:30 USA Preliminary Gross Domestic Product (GDP) September Quarter (+2.8% p.a. forecast vs +2.8% p.a. previous)

00:30 USA Core Durable Goods Orders October (+0.2% m/m forecast vs +0.5% m/m in September)

02:00 USA Core Personal Consumption Expenditures (PCE) Price Index October (+0.3% m/m and +2.8% p.a. forecast vs +0.3% m/m and +2.7% p.a. in September)

06:00 FOMC Minutes from its November meeting

19:55 AUD RBA Gov Bullock Speaks

Friday

00:00 JPN Tokyo Core CPI November (+2.0% p.a. forecast vs +1.8% p.a. in October)

All Day USA Thanksgiving Public Holiday

Saturday

12:30 CHN Manufacturing and Non-Manufacturing (Services) Purchasing Managers Index (PMI) November (Manufacturing: 50.3 forecast vs 50.1 in October; Services: 50.2 forecast vs 50.2 in October)

Latest News

Interesting Movers

Trading higher

+13.5% WEB Travel Group (WEB) - Appendix 4D and Half-Year Financial Report, 1H25 Investor Presentation, and Capital management initiatives

+12.0% Qoria (QOR) - No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Daily Scans Uptrends list 🔎📈

+10.6% Paradigm Biopharmaceuticals (PAR) - No news, continued positive response to Response to ASX Price Query and 2024 Chairman Address and AGM Presentation

+10.4% Brainchip (BRN) - No news

+9.0% EML Payments (EML) - No news, continued positive response to yesterday's EML 2.0 Strategy Plan Investor Presentation & Trading Update, upgraded to outperform from sector perform at RBC Capital Markets and price target increased to $1.20 from $0.90

+7.0% PYC Therapeutics (PYC) - PYC to Progress Kidney Drug Candidate Into Human Trials, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Daily Scans Uptrends list 🔎📈

+6.2% Life360 (360) - No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Daily Scans Uptrends list 🔎📈

+5.3% Ora Banda Mining (OBM) - No news, generally stronger ASX gold sector today, prices steadied modestly overnight, small gain in Asian trade

+5.0% Kingsgate Consolidated (KCN) - 2024 Annual General Meeting Presentation, ditto generally strong ASX gold sector today

Trading lower

-21.8% Novonix (NVX) - The price finally went up, so that means a capital raise…at a near-40% discount. Insto's only mind you. Masterful. See Successful Completion of Institutional Placement.

-9.1% Vulcan Energy Resources (VUL) - Vulcan announces Board appointments and committee changes, pullback after recent strong rally.

-7.4% Galan Lithium (GLN) - No news, generally tough day (week, month, year?) for ASX lithium stocks, fall is consistent with prevailing short and long term downtrends 🔎📈

-5.5% WA1 Resources (WA1) - No news, consistent with recent share price volatility (has rallied strongly last few days)

-5.1% Pinnacle Investment Management Group (PNI) - Share Purchase Plan

-4.2% Silex Systems (SLX) - GLE Acquires Paducah, KY Property for the PLEF, but also generally tough day for ASX lithium stocks (could do the week and few months jibe here also)

-4.1% Lotus Resources (LOT) - No news, ditto uranium, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Daily Scans Downtrends list 🔎📈

-3.6% Weebit Nano (WBT) - 2024 AGM Chair Address and CEO Presentation

-3.3% Yancoal Australia (YAL) - No news, continued uncertainty over whether acquisition of Anglo American's QLD coal assets will proceed, but generally tough day for ASX coal stocks, likely due to falling coking and thermal coal prices

-3.1% Boss Energy (BOE) - No news, ditto uranium, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Daily Scans Downtrends list 🔎📈

Broker Notes

Australian Clinical Labs (ACL)

Retained at buy at Citi; Price Target: $3.60

Air New Zealand (AIZ)

Retained at outperform at Macquarie; Price Target: $0.79 from $0.69

ARB Corporation (ARB)

Retained at buy at Citi; Price Target: $50.00

Aroa Biosurgery (ARX)

Retained at buy at Bell Potter; Price Target: $0.90

Retained at add at Morgans; Price Target: $1.05

ASX (ASX)

Retained at neutral at Citi; Price Target: $62.30

Retained at hold at CLSA; Price Target: $61.90 from $61.50

Retained at neutral at Jarden; Price Target: $62.25

Retained at neutral at JP Morgan; Price Target: $60.00

Retained at equal-weight at Morgan Stanley; Price Target: $58.00

Retained at sell at UBS; Price Target: $64.15 from $57.00

Brickworks (BKW)

Retained at neutral at Macquarie; Price Target: $27.70 from $27.40

Retained at accumulate at Ord Minnett; Price Target: $31.00

Brazilian Rare Earths (BRE)

Retained at buy at Ord Minnett; Price Target: $5.50 from $7.00

Brightstar Resources (BTR)

Retained at buy at Canaccord Genuity; Price Target: $0.06

Capitol Health (CAJ)

Retained at hold at Bell Potter; Price Target: $0.33

Centuria Office Reit (COF)

Retained at hold at Bell Potter; Price Target: $1.25

Endeavour Group (EDV)

Retained at neutral at Citi; Price Target: $4.89

EML Payments (EML)

Upgraded to outperform from sector perform at RBC Capital Markets; Price Target: $1.20 from $0.90

Eroad (ERD)

Retained at buy at Shaw and Partners; Price Target: $1.40 from $1.50

Gentrack Group (GTK)

Retained at buy at Bell Potter; Price Target: $13.90 from $11.50

Retained at overweight at Morgan Stanley; Price Target: $13.50 from $18.20

Retained at buy at Shaw and Partners; Price Target: $11.80 from $10.00

Healius (HLS)

Retained at buy at Citi; Price Target: $1.05

Hub24 (HUB)

Retained at neutral at Citi; Price Target: $56.70

Harvey Norman (HVN)

Retained at buy at Citi; Price Target: $5.50

IVE Group (IGL)

Retained at buy at Bell Potter; Price Target: $2.70

Monash IVF Group (MVF)

Retained at buy at Bell Potter; Price Target: $1.85

Newmont Corporation (NEM)

Retained at outperform at Macquarie; Price Target: $82.00

Nobleoak Life (NOL)

Retained at buy at Shaw and Partners; Price Target: $2.85

Netwealth Group (NWL)

Retained at neutral at Citi; Price Target: $27.00

Qantas Airways (QAN)

Retained at overweight at Morgan Stanley; Price Target: $10.50

Downgraded to neutral from buy at UBS; Price Target: $9.00 from $8.60

QBE Insurance Group (QBE)

Retained at buy at Citi; Price Target: $19.30

Retained at outperform at Macquarie; Price Target: $20.80

Retained at buy at UBS; Price Target: $21.50 from $20.50

Regis Healthcare (REG)

Retained at outperform at Macquarie; Price Target: $7.25 from $6.50

Ramsay Health Care (RHC)

Retained at neutral at Citi; Price Target: $42.00

Retained at neutral at Macquarie; Price Target: $42.75 from $45.75

Scentre Group (SCG)

Retained at overweight at Morgan Stanley; Price Target: $4.35

Sonic Healthcare (SHL)

Retained at hold at Citi; Price Target: $27.00

Smartpay (SMP)

Retained at buy at Shaw and Partners; Price Target: $1.10 from $1.20

The Lottery Corporation (TLC)

Upgraded to buy from hold at Jefferies; Price Target: $5.80 from $5.09

WEB Travel Group (WEB)

Retained at neutral at Citi; Price Target: $5.55

Retained at buy at UBS; Price Target: $5.60

Webjet (WJL)

Retained at buy at Goldman Sachs; Price Target: $1.10 from $1.05

Upgraded to buy from hold at Jefferies; Price Target: $1.10 from $0.95

Retained at overweight at JP Morgan; Price Target: $1.10 from $1.20

Retained at add at Morgans; Price Target: $1.05 from $0.95

Initiated at buy at Ord Minnett; Price Target: $1.32

Retained at outperform at RBC Capital Markets; Price Target: $1.30

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| SOM | Somnomed Ltd | $0.395 | +46.30% |

| G50 | G50 Corp Ltd | $0.20 | +37.93% |

| NAG | Nagambie Resources Ltd | $0.023 | +35.29% |

| ILA | Island Pharmaceuticals Ltd | $0.215 | +30.30% |

| BXN | Bioxyne Ltd | $0.018 | +28.57% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| AIV | Activex Ltd | $0.011 | -31.25% |

| CCX | City Chic Collective Ltd | $0.099 | -26.67% |

| BDG | Black Dragon Gold Corp | $0.039 | -22.00% |

| NVX | Novonix Ltd | $0.755 | -21.76% |

| IVXDB | Invion Ltd | $0.12 | -20.00% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| ILA | Island Pharmaceuticals Ltd | $0.215 | +30.30% |

| OCC | Orthocell Ltd | $0.805 | +25.78% |

| IGNDA | Ignite Ltd | $0.405 | +22.73% |

| IMR | Imricor Medical Systems Inc | $1.07 | +21.59% |

| PHO | Phosco Ltd | $0.079 | +12.86% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| IVXDB | Invion Ltd | $0.12 | -20.00% |

| BKT | Black Rock Mining Ltd | $0.037 | -19.57% |

| CSS | Clean Seas Seafood Ltd | $0.15 | -18.92% |

| DM1 | Desert Metals Ltd | $0.018 | -18.18% |

| NOR | Norwood Systems Ltd | $0.028 | -15.15% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| EP1 | E&P Financial Group Ltd | $0.51 | +3.03% |

| NDIA | Global X India Nifty 50 ETF | $76.94 | +0.05% |

| SMLL | Betashares Aust Small Companies Select Fund (Managed Fund) | $3.67 | +0.27% |

| GLPR | Ishares Ftse GBL Property Ex Aus (Aud Hedged) ETF | $28.10 | +0.25% |

| AN3PI | Australia and New Zealand Banking Group Ltd | $104.90 | +0.50% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| MQGPF | Macquarie Group Ltd | $105.30 | -0.17% |

| RSG | Resolute Mining Ltd | $0.395 | +1.28% |

| SMP | Smartpay Holdings Ltd | $0.535 | -4.46% |

| IPG | Ipd Group Ltd | $3.91 | +4.27% |

| EGL | Environmental Group Ltd (the) | $0.275 | +1.85% |