ASX 200 Live Today - Tuesday, 28th April

The S&P/ASX 200 eyes a six day losing streak despite the S&P 500 and Nasdaq closing at fresh all-time highs. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, April 28. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

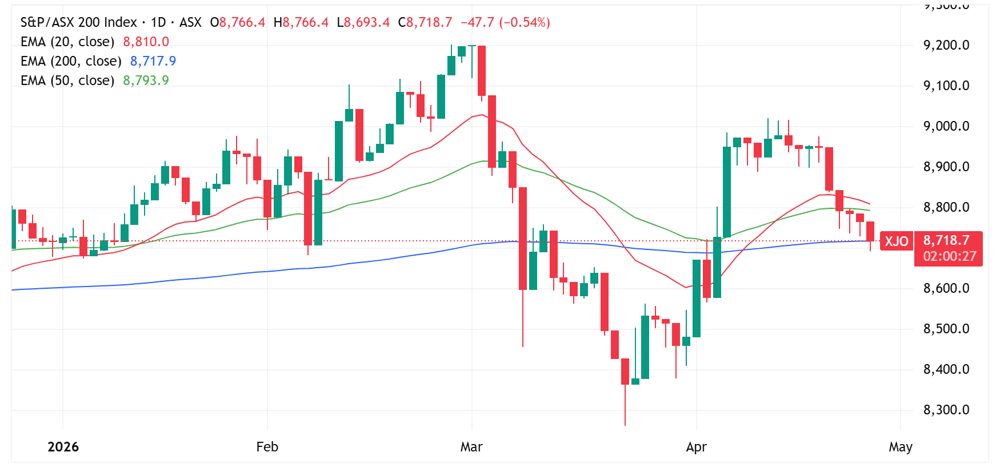

ASX 200 extends losing streak, tests 200-day

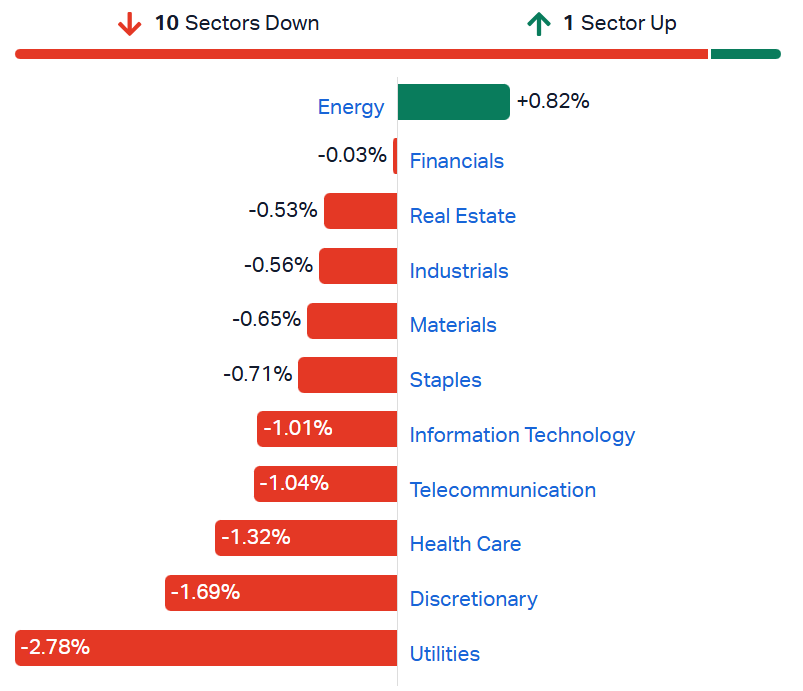

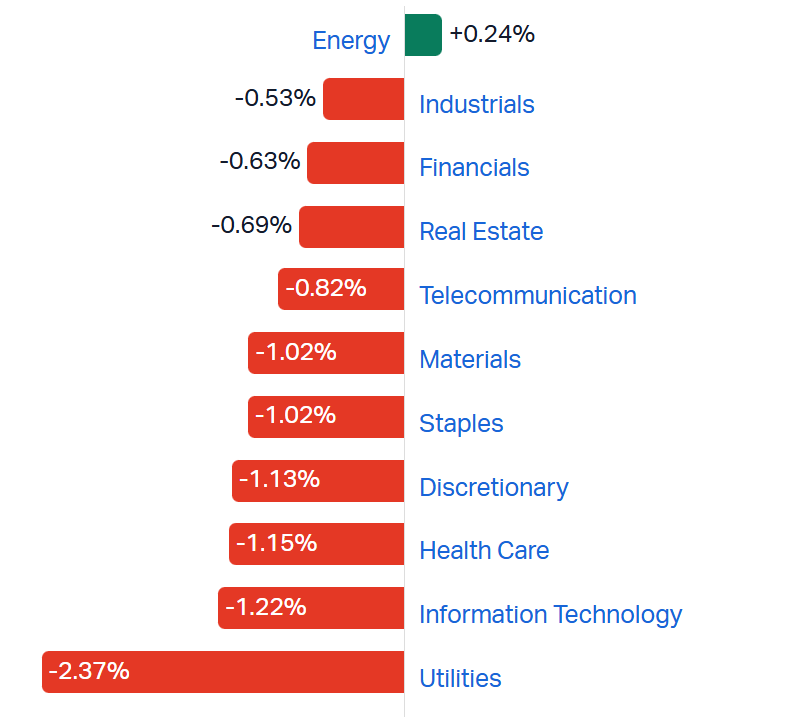

[2:05 pm] That's all for today! Another rough day for markets, with the ASX 200 down 0.54%, all sectors (except Energy) red and 121 constituents (60.5%) lower.

S&P/ASX 200 sectors (Source: Market Index)

The index has managed a small bounce off lows of (0.83%), currently trading right on the 200-day.

S&P/ASX 200 daily chart (Source: TradingView)

On a side note, some interesting comments from Goldman Sachs on software stocks: "We expect the debate around AI disruption, and therefore uncertainty about many companies' terminal value, will persist for at least several quarters. The threat of disruption will likely represent a persistent overhang until the later stages of AI adoption. In the meantime, disproving this disruption narrative is challenging. For investors to have confidence in the long-term impact of AI, it will require more evidence of where AI is impacting earnings, which could take several quarters if not years."

A rough day for retailers

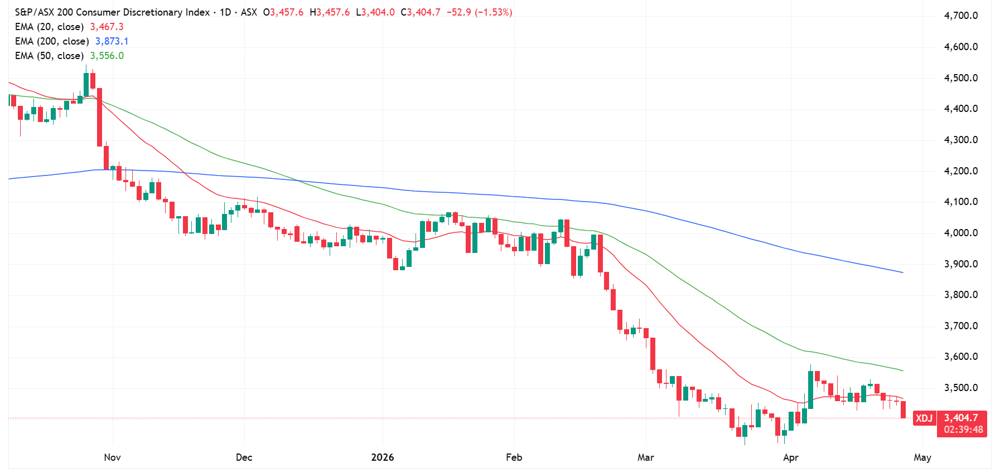

[1:24 pm] The S&P/ASX 200 Discretionary Index is down 1.5% today and within 2% of the recent 23 March low. Some relatively broad weakness today, including Wesfarmers (-1.4%), Aristocrat Leisure (-1.7%), The Lottery Corp (-0.5%) and Light & Wonder (+2.7%). JB Hi-Fi is the only bright spot, reversing early declines and currently up 2.2%.

The index's largest constituent, Wesfarmers, is on the cusp of making a fresh 52-week low.

S&P/ASX 200 Discretionary Index daily chart (Source: TradingView)

CATL raises $5bn in Hong Kong placement at bottom of range

[1:16 pm] The world's largest battery maker priced its Hong Kong share placement at a 7% discount, with softer-than-expected demand partly attributed to recent shareholder sell-downs.

CATL priced 60.98m shares at HK$628.20, the bottom of the HK$628.20-HK$651.80 marketed range, with the stock falling as much as 9.2% on the day of pricing

The wider-than-usual discount (vs. 3.8-5.1% in recent CATL-related transactions) reflects investor caution around the company raising capital opportunistically given its already sizable balance sheet

Proceeds will fund global capacity expansion, zero-carbon business development, R&D, and general working capital

CATL's Hong Kong shares have rallied 139% since their debut less than a year ago

Source: Bloomberg

What's catching a bid today?

[1:15 pm] The below table observes the S&P/ASX 200 stocks with the largest gains from today's open price.

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

ELV | Elevra Lithium | 5.88% | $13.78 |

ILU | Iluka Resources | 3.78% | $7.83 |

GGP | Greatland Resources | 2.54% | $14.14 |

JBH | JB Hi-Fi | 2.45% | $77.33 |

HUB | Hub24 | 2.23% | $85.33 |

L1G | L1 Group | 2.16% | $1.18 |

DYL | Deep Yellow | 2.07% | $1.97 |

TAH | Tabcorp | 2.00% | $1.12 |

IGO | IGO | 1.83% | $7.51 |

CDA | Codan | 1.60% | $36.14 |

Nickel Industries refinances bank debt

[1:11 pm] Nickel Industries has replaced its existing bank loans with a new US$450 million unsecured syndicated facility, extending its debt maturity profile to mid-2030.

Interest rate is SOFR plus a margin starting at 3.50% for the first six months, then stepping down to as low as 2.25% if net debt/EBITDA falls below 2.0x, incentivising deleveraging

Quarterly amortisation of 5.875% per instalment begins six months post-close, with a final bullet repayment on 30 June 2030 — the schedule is designed to provide cash flow flexibility as the Excelsior Nickel Cobalt HPAL (ENC) project ramps up

Post-refinancing net debt sits at approximately US$994m, comprising US$800m in senior unsecured notes (due October 2030), the new US$450m facility, and US$256m in cash

Company page: Nickel Industries (NIC)

UBS upgrades lithium price forecasts on tighter supply-demand outlook

[12:25 pm] UBS raises its lithium price deck by up to 47% near-term, driven by stronger EV and energy storage demand alongside constrained supply, flagging structural deficits emerging from 2030.

Spodumene price forecasts upgraded up to 23% near-term and 17% long-term to US$1,400/t SC6.0

Demand outlook lifted to a 15% two-year CAGR for EV sales, above the UBS autos team's prior 12% assumption, supported by the energy shock improving EV total cost of ownership economics and surging energy storage system (ESS) demand

China battery signals are encouraging: March EV battery sales were up 31% year-on-year to 114.5GWh, and ESS battery sales surged 115% year-on-year to 60.3GWh

Supply growth of ~596kt is modelled from 2025-2027, falling just short of ~623kt in incremental demand over the same period, pointing to a tight but manageable balance near-term

Near-term supply trimmed following IGO's output guidance downgrade for Greenbushes, with broader supply response is expected to be tempered by macro uncertainty, input cost disruptions, and elevated price volatility keeping producers cautious on committing to restarts or new production

Australian fuel margins look elevated but unsustainable

[11:28 am] UBS prefers Ampol (ALD) over Viva Energy (VEA) as crack spreads widen, but cautions against capitalising margins until conditions normalise.

Regional crack spreads are averaging ~US$42/bbl this quarter, up ~US$19/bbl quarter-on-quarter, though crude premia are expected to pressure margins

Petrol margins are tracking at ~A$20.3c/L year-to-date (vs. ~A$17.0c/L in 2025), while diesel margins have softened to ~A$10.0c/L in April vs. ~A$18.2c/L for full-year 2025

Fuel stock cover as of 18 April sits at 44 days for gasoline, 33 days for diesel, and 30 days for kerosene, which Morgan Stanley flags potential demand management scenarios from July 2026 when including inbound cargoes

New car sales fell 1.4% in 1Q26 vs. prior corresponding period, with petrol-powered vehicles declining sharply (36% share, down 18%), while EVs surged 92% to 12% share and hybrids rose 9% to 24% share — a structural headwind for fuel volumes over time

Lithium stocks trend higher

[11:26 am] PLS Group is currently trading at fresh all-time highs despite Chinese lithium carbonate prices falling 1.6% to 178,800 yuan a tonne this morning.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

EUR | European Lithium | 52.6% | $0.44 | 690.9% |

DLI | Delta Lithium | 6.4% | $0.25 | 42.9% |

PMT | Pmet Resources | 6.0% | $0.62 | 123.6% |

LTR | Liontown | 3.3% | $2.36 | 320.5% |

MIN | Mineral Resources | 2.9% | $60.74 | 231.9% |

IGO | IGO | 2.9% | $7.53 | 107.4% |

PLS | PLS Group | 2.7% | $6.09 | 307.4% |

VUL | Vulcan Energy Resources | 1.6% | $3.86 | -1.8% |

GL1 | Global Lithium Resources | 0.9% | $0.58 | 259.4% |

CXO | Core Lithium | 0.6% | $0.33 | 347.9% |

INR | Ioneer | 0.0% | $0.14 | 3.7% |

AGY | Argosy Minerals | -1.3% | $0.08 | 305.3% |

WR1 | Winsome Resources | -3.1% | $0.48 | 143.6% |

PAT | Patriot Resources | -4.0% | $0.12 | 90.5% |

Gold stocks mostly lower

[11:23 am] A fairly heavy session for gold stocks, with most names down 2-3%. Newmont pulling back after a 6.7% rally on Monday, Pantoro weighed by a downbeat quarterly update and Resolute down 12% in the last two sessions amid unrest in parts of Mali.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

PNR | Pantoro Gold | -7.9% | $3.51 | 23.2% |

RSG | Resolute Mining | -4.5% | $1.23 | 162.1% |

NEM | Newmont | -3.1% | $161.06 | 90.5% |

NST | Northern Star Resources | -2.6% | $21.57 | 1.4% |

CYL | Catalyst Metals | -2.5% | $6.13 | -6.0% |

VAU | Vault Minerals | -2.2% | $4.69 | 63.8% |

BGL | Bellevue Gold | -2.1% | $1.63 | 81.6% |

RRL | Regis Resources | -2.1% | $7.26 | 60.9% |

MEK | Meeka Metals | -2.1% | $0.14 | -8.4% |

BC8 | Black Cat Syndicate | -2.0% | $1.21 | 21.7% |

EMR | Emerald Resources | -1.9% | $6.25 | 56.6% |

RMS | Ramelius Resources | -1.9% | $3.67 | 46.2% |

EVN | Evolution Mining | -1.6% | $12.87 | 61.6% |

WGX | Westgold Resources | -1.6% | $6.07 | 100.3% |

ALK | Alkane Resources | -1.6% | $1.56 | 102.6% |

GMD | Genesis Minerals | -1.4% | $6.33 | 64.4% |

PRU | Perseus Mining | -0.8% | $5.55 | 71.1% |

CMM | Capricorn Metals | -0.8% | $11.36 | 26.1% |

OBM | Ora Banda Mining | -0.3% | $1.54 | 46.2% |

SBM | St. Barbara | 1.1% | $0.67 | 134.0% |

AMI | Aurelia Metals | 1.9% | $0.27 | -10.0% |

IperionX scales titanium production amid surging US defence demand

[10:42 am] IperionX outlined an aggressive production ramp-up at its Virginia facility, underpinned by strong government backing and accelerating customer demand across defence and advanced manufacturing. This investor presentation was marked as non-price sensitive, though the stock is trading 8.2% higher this morning.

Powder production capacity targeted to reach 200 metric tons per annum (mtpa) by end of 2026, up from 50mt in Q1, with an ambition to expand 7x by 2027 to become the world's largest titanium metal powder producer

$41m in obligated government funding yet to be received, providing near-term runway through 2026. Definitive feasibility study for the Titan project, funded by the Department of War, due for completion and release in Q2 2026.

Customer engagement accelerating across defence, automotive, consumer electronics and robotics, with new product launches expected across 2026 and 2027.

Multiple new government and commercial contracts anticipated as production milestones are achieved over the next 6 to 18 months.

Global titanium supply chain heavily exposed to China and Russia, and surging US defence spending and reshoring policy creating structural demand for domestic supply

Company page: IperionX (IPX)

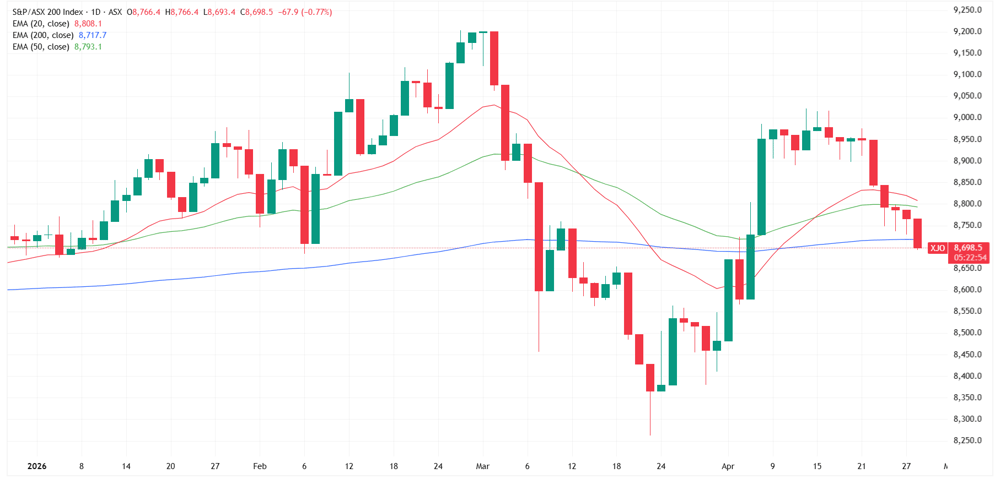

ASX 200 slips below the 200-day moving average

[10:38 am] ASX 200 has slipped below the key 200-day, highlighting deteriorating market internals and fading participation.

ASX 200 daily chart (Source: TradingView)

ASX 200 lower, most sectors red

[10:33 am] A rather ugly open for the ASX 200, currently down 0.68% and on track for a sixth straight day of declines. Breadth is weak, with all sectors except Energy trading lower, and 141 constituents (70.5%) down in early trade. Utilities weighed by continued selling on Origin (-4.5%) after yesterday's downbeat quarterly, Discretionary now on a five-day losing streak after a small relief rally earlier this month, Healthcare stocks making fresh 8-year lows and broad softness for most other defensives/cyclicals.

S&P/ASX 200 sectors (Source: Market Index)

Origin Energy sharply lower

[10:29 am] Origin Energy was aggressively sold down after a flattish open, currently down 3.8%. The company reported its Q3 update on Monday, which triggered a 5.0% selloff.

UBS trimmed its price target this morning, following a soft Octopus Energy EBITDA guidance cut, though the broker sees the long-term value thesis as unchanged.

APLNG March quarter production volumes in line, though soft domestic gas prices from surplus short-term supply dragged sales revenue marginally lower.

Key negative was a downgrade to FY26 Octopus Energy EBITDA guidance (from $0-$150m to -$70m to $30m), implying a ~$70m cut to consensus at the new midpoint

Driven by accelerated wind-down of the UK Government's Energy Company Obligation (ECO) scheme by December 2026, leaving some costs unrecoverable

UBS flags the EBITDA cut as a near-term headwind but not a value impairment, pointing to strong high-margin international customer growth at Octopus (+440k in the December quarter rising to +460k in the March quarter) as the dominant long-term value driver

UBS cuts FY26 EPS forecasts by 9% and FY27 EPS by 18% (latter reflecting oil swap and FX forward hedge settlement payments of $190m in FY27 and $18m in FY28)

Price target trimmed to $14.10 from $14.30

Company page: Origin Energy (ORG)

Top ASX 200 gainers

[10:08 am] Reliance Worldwide gapped up ~8% after reaffirming its FY26 guidance, while Lynas finally bounces after falling ~18% in the last two weeks. Lithium stocks also continue to trend higher, uranium stocks bounce after broad weakness on Monday and Whitehaven higher on a relatively in-line quarterly production report.

Ticker | Company | % Chg | Price |

|---|---|---|---|

RWC | Reliance Worldwide | 7.89% | $3.28 |

LYC | Lynas Rare Earths | 4.15% | $18.83 |

WHC | Whitehaven Coal | 3.90% | $8.00 |

ELV | Elevra Lithium | 3.88% | $13.38 |

LIN | Lindian Resources | 2.29% | $0.90 |

PDN | Paladin Energy | 2.22% | $12.44 |

LTR | Liontown | 2.19% | $2.33 |

ILU | Iluka Resources | 2.00% | $7.65 |

MIN | Mineral Resources | 1.98% | $60.18 |

IGO | IGO | 1.91% | $7.46 |

Top ASX 200 losers

[10:08 am] Gold stocks are trading broadly lower after gold prices slipped 0.58% overnight, with most names down 2-3%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

RSG | Resolute Mining | -6.59% | $1.21 |

GGP | Greatland Resources | -3.74% | $13.64 |

ALK | Alkane Resources | -3.47% | $1.53 |

NEM | Newmont | -3.08% | $161.04 |

WAF | West African Resources | -2.97% | $3.11 |

WGX | Westgold Resources | -2.76% | $6.00 |

VAU | Vault Minerals | -2.71% | $4.66 |

EMR | Emerald Resources | -2.67% | $6.20 |

NST | Northern Star Resources | -2.57% | $21.57 |

EOS | Electro Optic Systems | -2.54% | $9.98 |

Quick question for our readers

[10:07 am] We’re looking to better understand the investors who read the Market Index Live Blog each day. To do that, we’ll be running a quick daily poll – just one simple question – to learn more about how you invest, trade, and navigate the markets.

It’ll take a few seconds to answer, and over time it helps us shape the content and coverage that matters most to you.

Elsight's Halo platform granted US Blue List status

[9:55 am] A meaningful credentialing milestone for Elsight as it secures direct access to a rapidly scaling US defence drone procurement pipeline, arriving just as the Pentagon prepares its largest drone budget in a generation.

Halo connectivity platform has been included on the US Department of War's DCMA Blue List, a directory of NDAA-compliant unmanned aircraft systems and components

Inclusion enables US military units to procure Halo directly through the DCMA acquisition marketplace, bypassing traditional multi-year acquisition cycles

US FY27 Department of War budget request totals ~US$1.5tn (a 42% increase), with ~US$75bn earmarked for drone and counter-drone capabilities, representing a tripling vs FY26 levels

Company page: Elsight (ELS)

Beach Energy Q3 production falls short, FY26 guidance revised lower

[9:50 am] A challenging quarter for Beach with weather disruptions across the Cooper Basin and Western Flank, alongside cyclone-related shut-ins, forcing a downgrade to its FY26 production outlook despite a strong ramp-up at Waitsia.

Production up 7% quarter-on-quarter to 4.8MMboe vs ests 5.1MMboe (6% miss)

Sales volume of 5.3MMboe vs ests 5.6MMboe (5% miss)

Sales revenue of $419m vs ests $444.5m (6% miss)

Capex of $126m vs ests $166m (24% beat)

FY26 production guidance lowered to 19.4-20.3MMboe (prior 19.7-22.0MMboe), reflecting NWS and Waitsia cyclone shut-ins, compressor interruptions and Cooper Basin weather delays

This represents a 4.8% downgrade at the midpoint

Perth Basin production up 174% with the final two gas compressors commissioned at Waitsia, while Otway Basin was down 9% on lower customer nominations and Western Flank down 8% on a severe rain event

Company page: Beach Energy (BPT)

Whitehaven Coal Q3 ROM production broadly in line

[9:46 am] Whitehaven Coal reported Q3 Managed ROM production in-line with market expectations, noting that FY26 production is tracking to the upper half of guidance and unit costs around the midpoint.

Managed ROM production of 9.50Mt vs ests 9.54Mt (in line), down 14% vs. Q2 reflecting seasonality and a strong prior quarter

Beats: Maules Creek production of 3.4Mt vs ests 2.98Mt (14% beat), Daunia 1.5Mt vs ests 1.33Mt (13% beat), Gunnedah 1.0Mt vs ests 0.85Mt (18% beat).

Misses:Narrabri 1.0Mt vs ests 1.43Mt (30% miss) and Blackwater 2.6Mt vs ests 3.18Mt (18% miss).

Managed saleable coal production of 8.38Mt vs ests 7.16Mt (17% beat), with total managed coal sales up 14% to 8.64Mt vs quarter-ago 7.60Mt.

FY26 ROM production and coal sales tracking firmly in the upper half of the 37.0-41.0Mt guidance range, with unit costs around the midpoint of A$130-145/t and capex tracking to the low end of A$340-440m

Net debt reduced to A$0.6bn (Dec: A$0.7bn) before the US$500m second deferred BMA payment on 2-Apr-26

Diesel exposure flagged as a Q4 cost headwind, with every A$1/L increase in diesel price adding ~A$10-11/t to unit costs on an annualised basis.

Company page: Whitehaven Coal (WHC)

Greatland Resources beats on AISC, eyes upper end of FY26 production guidance

[9:43 am] Greatland Resources delivered a strong Q3, with costs beating market expectations, alongside a record quarterly cash build. A fairly surprising outcome given most mining quarterlies have flagged upside risks to full-year cost guidances due to ongoing fuel supply concerns.

Q3 AISC of $2,056/oz vs ests $2,286/oz (10% beat)

Q3 operating cashflow up 12% to $453m vs quarter-ago $406m

Q3 gold production of 83koz and gold sales of 98koz, both pre-reported

Closing cash up to $1,208m (DecQ: $948m), debt free

FY26 production guided to around or slightly above the upper end of the 260-310koz range, with AISC trending towards the lower end of $2,400-$2,800/oz

Telfer Mineral Resource Estimate grew 4.8Moz (+150%) to 8.0Moz Au at a discovery cost of $5/oz, lifting Group MRE to 14.9Moz Au and 645kt Cu, supporting a multi-decade growth profile

Company page: Greatland Resources (GGP)

Aurelia Metals lifts FY26 gold guidance on stronger Q3 output

[9:40 am] Aurelia Metals reported stronger-than-expected Q3 with gold production, leading to an upgrade to FY26 guidance, alongside a balance sheet refinancing.

Q3 gold production up 11% to 13.0koz, with copper flat at 0.6kt, zinc down 4% to 6.9kt and lead flat at 4.3kt

FY26 gold guidance lifted to 45-50koz (prior 35-45koz), reflecting prioritisation of higher value gold ore at Peak (18.7% upgrade at the midpoint)

FY26 copper guidance reduced to 2.5-3.0kt (prior 3.0-4.0kt) and growth capital lowered to $45-60m (prior $60-70m)

New $150m senior secured financing commitment executed with Citi, Credeq and HSBC, releasing ~$38m of restricted cash and taking proforma cash to over $130m

Company page: Aurelia Metals (AMI)

Reliance Worldwide reaffirms FY26 outlook amid tariff and Middle East updates

[9:35 am] Reliance Worldwide has confirmed its FY26 trading outlook, with the net cost impact from US tariffs expected at the lower end of guidance and no material impact anticipated from the war in Iran.

FY26 net cost impact from US tariffs expected at the lower end of the previously indicated $25-30m range

FY27 net cost impact unchanged at $5-7m based on current tariff rates, excluding any potential tariff refund

US Supreme Court struck down IEEPA-based tariffs on 20-Feb, with a federal refund portal opening on 20-Apr, RWC has lodged a refund claim with recoverable amounts yet to be verified

No direct exposure to the war in Iran or Strait of Hormuz closure, with higher oil-driven resin, logistics and energy costs being offset through price increases, though prolongation may impact FY27

Reliance suffered an 9% selloff on the day of its 1H26 result on 17-Feb and fell a further ~16% over the next month. The stock is currently hovering around three year lows and down 24.5% year-to-date.

Reliance Worldwide daily price chart (Source: TradingView) | Company page: Reliance Worldwide (RWC)

Resolute confirms Syama operations unaffected by Mali unrest

[9:30 am] Resolute Mining provided an operational update following coordinated jihadist and separatist attacks across Mali over the weekend.

Syama operation in southern Mali's Sikasso Region (~30km from the Côte d'Ivoire border) continues to operate without interruption, with no impact to personnel safety, supply chains or production.

Coordinated weekend attacks targeted several regions, with militants seizing several and military bases. Mali's defence minister Sadio Camara and military intelligence chief Modibo Koné were both killed

Resolute shares tumbled 8.1% on Monday, vs. the All Ords Gold Index which finished 1.6% higher.

Company page: Resolute Mining (RSG)

Pantoro misses Q3 production and cost expectations

[9:26 am] Pantoro Gold reported a Q3 production miss against market expectations, though reaffirmed its full-year guidance.

Q3 production down 19% quarter-on-quarter to 17.8koz vs ests of 22.0koz (19% miss)

"As outlined on 9 March, operations during the Quarter were hampered by wet weather and low cloud during February and March which impacted flights in and out of site, open pit mining and ore haulage activities."

AISC of $3,204/oz vs ests of $2,752/oz (16% higher than ests)

Cash and equivalents of $237.3m

FY26 guidance maintained at 86-92koz, with management flagging the company is on track to deliver into that range by year-end

Buy-back program announced 23 February 2026, with 1.32m shares purchased at an average $3.50 during March

Company page: Pantoro Gold (PNR)

Carnarvon progresses Bedout drilling ahead

[9:24 am] Carnarvon Energy provided a quarterly update covering Dorado, Bedout exploration progress and a strong balance sheet position.

Cash of $98m at quarter-end with no debt, plus a US$90m future development cost carry on Dorado, and a 19.9% stake in Strike Energy

Bedout JV (Carnarvon 10-20%, operated by Santos) progressing the multi-well Environmental Plan, long-lead procurement and offshore drilling rig tender, with well commencement targeted for 1H27

Dorado (Carnarvon 10%, Santos 80%) Phase 1 liquids concept based on a single wellhead platform supporting up to 12 wells tied back to an FPSO, with potential future tiebacks from Pavo. Drilling activity in the region expected to resume 1H27 alongside renewed development work as Santos evaluates further Bedout resources

On-market share Buy-Back of up to 10% of issued capital reinstated on 14 February 2026, funded from existing cash and running for 12 months unless completed or terminated earlier

Carnarvon has a pretty interesting value proposition, given its ~$187 million market cap vs. $98 million cash position, 19.9% stake in Strike Energy (~$82m) and US$90m (~A$125m) cost carry from Santos. You've effectively got a company trading at zero EV.

Company page: Carnarvon Energy (CVN)

Lindian secures domestic sulphuric acid supply ahead of China export ban

[9:17 am] Lindian Resources has confirmed an existing sulphuric acid supply arrangement, positioning the company favourably ahead of China's near-total ban on sulphuric acid exports from 1-May-26.

Supply agreement is with Stepnogorsk Sulphuric Acid Plant (SSAP), a state-backed producer within Kazakhstan's sovereign wealth fund

SSAP currently produces ~180,000tpa with capacity expanding to ~360,000tpa, with sulphuric acid pricing in Kazakhstan estimated at US$100-130 per tonne, below typical Western market pricing

China's export ban is expected to remove ~4.65Mt of sulphuric acid supply from global markets, likely tightening availability and pressuring prices in import-dependent regions including Chile, Indonesia, Africa and the Middle East

Domestic supply access may reduce exposure to global price volatility and supply disruption, supporting Lindian's downstream strategy and potential cost advantage versus import-reliant peers

Company page: Lindian Resources (LIN)

Ora Banda Mining names John Richards as Chair-elect

[9:13 am] Ora Banda Mining has announced that Chair Peter Mansell intends to retire at the close of the 2026 AGM, with John Richards appointed as Chair-elect.

John Richards appointed as a Non-Executive Director with effect from 1-May-26, and is anticipated to assume the role of Chair following the November 2026 AGM

Richards is currently Non-Executive Chair of Sandfire Resources and Lead Independent Non-Executive Director of Sheffield Resources, bringing relevant copper and mineral sands sector experience.

Peter Mansell will retire from the board at the close of the 2026 AGM.

Mansell has been on the OBM board since 2018, and indirectly owns 2.5m shares in the company

Company page: Ora Banda Mining (OBM)

Critical Metals enters LoI to acquire European Lithium

[9:11 am] Critical Metals Corp (CRML) has signed a letter of intent to acquire all outstanding shares of European Lithium in an all-stock transaction valued at around US$835 million.

European Lithium shareholders to receive 0.035 Critical Metals shares for each European Lithium share held, based on the unaffected closing price on 22-Apr-26

CRML shares closed at $14.43 overnight, which implies a 50.5 cent offer price (vs. EUR last close of 28.5 cents)

Transaction structured via two interdependent Schemes of Arrangement covering European Lithium's shares and listed options, with unlisted ZEPOs cancelled or exchanged for economically equivalent CRML securities

Conditional on European Lithium holding a net cash and liquid assets balance of at least A$330m, alongside binding documentation, shareholder, regulatory and court approvals, and satisfactory due diligence

European Lithium has agreed to an exclusivity period, with the length undisclosed

The interesting thing here is that there was a window of opportunity to buy European Lithium before it went into trading halt. The AFR broke the story at 3:07 pm AEST on Thursday, driving the share price ~11% higher shortly after and closing the day up 16.3% to 28.5 cents. This window could've been used to buy the stock, though you'd have been flying blind on the actual takeover details.

Company page: European Lithium (EUR)

Fortescue close to long-term iron ore deal with CMRG

[9:05 am] Fortescue is reportedly nearing a long-term supply agreement with China Mineral Resources Group, following BHP's recent settlement that ended a months-long standoff.

A long-term settlement with CMRG is expected to be finalised in the coming months, according to Bloomberg

BHP confirmed last week it had concluded its own iron ore sales negotiations with CMRG, prompting traders and investors to look for further settlements across the sector

Fortescue executives travelled to China and met with CMRG earlier in the week, but said it is too early to specify the future negotiation routine post-deal

Pricing benchmarks have been a key sticking point, with Fortescue having shifted to an average of China's Mysteel index and the Argus Iron Ore Index, while its higher-grade Iron Bridge concentrate is priced against the Platts 65% index

Company page: Fortescue (FMG)

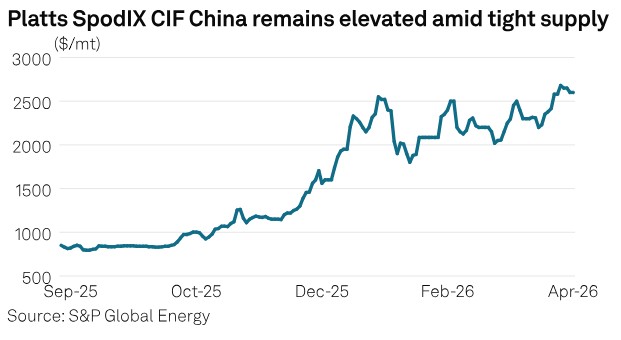

China lithium prices hit two-year high

[8:56 am] Tightening raw material supply and stronger downstream demand have pushed China's lithium spot and futures prices to multi-year highs, according to S&P Global.

Battery grade lithium carbonate assessed up 1.43% day on day to Yuan 177,500/mt (US$25,974/mt) DDP China on April 27 per Platts, the highest level since September 2023.

Most actively traded lithium carbonate contract on the Guangzhou Futures Exchange up 1.7% to Yuan 180,560/mt (US$26,459/mt), the fourth straight session of gains.

Mali driving the bid, with the country supplying 206,057mt of spodumene to China in Q1 2026 (9.3% of imports), and a sharp escalation in armed conflict since April 25 amplifying supply-side concerns despite no reported disruption to the Goulamina (Ganfeng 65%) or Bougouni (Hainan Mining) mines.

Multiple supply pressures stacking up, including Zimbabwe's export ban on lithium concentrate in place since late February, license-related shutdown risks at lepidolite mines in Jiangxi, and a downward revision to output guidance from IGO. Spodumene (SpodIX CIF China, 6% lithium oxide basis) up US$290/mt since the Zimbabwe ban began, last assessed at US$2,640/mt.

Downstream demand in China continues to strengthen amid a seasonal peak, compounding the squeeze on already tight raw material inventories.

Source: S&P Global

BoJ expected to hold as Iran war complicates rate path

[8:48 am] The Bank of Japan is widely expected to keep rates unchanged at 0.75% at 1:00 pm AEST on Tuesday, with focus shifting to Governor Kazuo Ueda's communication on the yen and the path of further hikes.

Markets are pricing just a ~7% chance of a hike, down sharply from weeks ago

The yen was hovering ~159.5, near levels that prompted intervention in 2024, with Finance Minister Satsuki Katayama flagging round-the-clock contact with US counterparts on speculative moves

March inflation accelerated for the first time in five months and service producer prices rose 1.25% m/m, the largest non-tax-driven increase in around 36 years, supporting a hawkish stance

Iran proposes Hormuz reopening, defers nuclear talks

[8:45 am] Iran has handed the US a new proposal via Pakistani mediators to reopen the Strait of Hormuz and extend the ceasefire, with nuclear negotiations postponed until after the US blockade is lifted, though Washington has signalled scepticism.

US Secretary of State Marco Rubio cast Iranian control of the strait as unacceptable, rejecting any system involving Iranian permission or tolls on international shipping

Crude pared gains and Asian equities extended advances on the Axios report

Political pressure is building on Trump from rising US gas prices and strained European ties, with German Chancellor Friedrich Merz publicly stating the US is being "humiliated" by Iran's leadership

Goldman lifts Brent forecasts on Hormuz shock

[8:44 am] Goldman Sachs raised oil price targets as the prolonged Strait of Hormuz closure drives record inventory draws, while Morgan Stanley held its more bullish view.

Goldman lifted Q4 Brent forecast up 13% to US$90 a barrel (from US$80), now nearly US$30 higher than pre-Hormuz shock levels. New Q2 and Q3 calls sit at US$100 and US$93 respectively

14.5m barrels a day of Persian Gulf crude production losses are driving global inventory draws at a record 11 to 12m barrels a day pace in April, which Goldman flagged as unsustainable and could force sharper demand destruction if the shock persists

Goldman now expects Gulf exports to normalise by end-June (pushed back from mid-May prior), with a 9.6m barrels a day market deficit this quarter vs a surplus a year ago

Morgan Stanley left Brent forecasts unchanged at US$110 in Q2, US$100 in Q3 and US$90 in Q4, noting Persian Gulf oil exports slumped 14.2m barrels a day while global stockpiles dropped 4.8m barrels a day as weaker demand absorbed part of the shortfall

Source: Bloomberg

Microsoft and OpenAI end exclusivity pact

[8:42 am] The two companies revised their landmark partnership, freeing OpenAI to sell its models through rival cloud providers.

Microsoft loses exclusive right to sell OpenAI models on its cloud, opening the door for OpenAI to strike distribution deals with AWS and other hyperscalers, in exchange Microsoft no longer pays a revenue share on OpenAI products it resells

Microsoft remains OpenAI's "primary cloud provider" with new OpenAI products available first on Azure, preserving a key competitive hook for the Azure franchise

Revenue share paid by OpenAI to Microsoft on its own product sales will be capped (level undisclosed), with payments now running through 2030 regardless of whether OpenAI reaches AGI, removing a key uncertainty from the prior deal where payments would have stopped at AGI

Microsoft retains its 27% ownership stake in OpenAI from last year's for-profit restructuring, locking in long-dated economic exposure to the startup

Positioning reset after CTA buying spree

[8:37 am] Analysts offer diverging takes on US equity positioning following recent systematic flows.

Goldman Sachs flagged $170bn of CTA purchases this month have pushed positioning back to neutral, with an estimated $25bn of pension rebalancing flows hitting US equities into month-end, the largest on record outside quarterly expirations

Hedge funds actively de-grossing into record market levels per Goldman, with positioning falling from the 100th percentile a few weeks ago to the 3rd percentile on a one-year lookback. Long/short US fund gross leverage dropped nearly 5 points last week, the largest move since September 2025

JPMorgan sees hedge fund exposure in the 34th percentile on a 12-month basis but 78th percentile on a longer-term view, with the US TPM indicator at the 70th percentile suggesting crowded tactical positioning across CTAs and retail ETFs

BofA more constructive, noting aggregate systematic positioning remains around $200bn below YTD highs despite $55bn added last week, with $40-50bn of further CTA demand expected in a flat-to-up tape (though unlikely to return to max-long levels)

Buybacks a near-term tailwind, with Goldman flagging a record US$422bn of authorisations announced through mid-April and the blackout window reopening in coming weeks

Big Tech earnings week kicks off with AI demand in focus

[8:36 am] Hyperscalers Amazon, Alphabet, Microsoft and Meta report Wednesday after the bell, with Apple to follow Thursday, as investors scrutinise AI capex returns and cloud growth.

UBS noted GPU and CPU demand inflecting at an unprecedented pace, but the bar has been raised for AWS and Google Cloud in particular

KeyBanc flagged upward bias on capex into 2027 after AWS disclosed chip revenue over $20bn (up triple digits y/y), though argued AWS momentum reinforces attractive returns on capex

Microsoft views mixed, with Guggenheim warning of downside risk on Azure given a high bar of around 38% growth, while Piper Sandler is positive on Copilot improvements and the ability to monetise both OpenAI and Anthropic growth

Meta capex a concern, with BMO questioning monetisation of $132bn in 2026 capex absent a clear near-term revenue opportunity, though Guggenheim argued AI investments are already driving high-return opportunities

Apple likely to benefit from an AI-driven upgrade cycle, but previews expect little new on AI strategy with WWDC set for early June

Good morning!

[8:28 am] ASX 200 futures are down 61 pts (-0.69%) as of 8:30 am AEST.

The overnight session in a nutshell:

S&P 500 (+0.12%) and Nasdaq (+0.20%) eked out another fresh all-time high, largely driven by Mag-7 strength

Dow (-0.13%) and Equal-weight S&P 500 (-0.12%) struggled for upside amid weakness from Staples, Real Estate, Discretionary, Healthcare and Materials

Nvidia (+4.0%) recorded a second straight all-time high, now up 31% since 30-Mar, though iShares Semiconductor ETF (-1.3%) snapped a historic 18-day win streak

Iran offers deal to US to reopen Strait and defer nuclear negotiations, Rubio says offer is not acceptable