ASX 200 Live Today - Tuesday, 26th May

The S&P/ASX 200 is set to rise as Iran peace hopes lifts European and Asian equities. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, May 26. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 lower, US-Iran escalation tempers peace deal expectations

[2:00 pm] The S&P/ASX 200 is currently down 0.39% as an uptick in oil and yields weighed on market sentiment.

US Central Command described the strikes as "defensive", targeting missile launch sites and boats attempting to lay mines, and stressed the ceasefire remains intact

Second major attack during the seven-week ceasefire, raising risk of escalation around the Strait of Hormuz, a key oil shipping chokepoint

Iranian state media reported blasts around Bandar Abbas (home to a military port and dual-use airport) but said the situation was "completely under control"

The above has driven a slight uptick in oil prices, with Brent up 1.5% to US$95.07 a barrel and the Aussie 10-year yield snapping four straight days of declines, currently up 4 bps to 4.91%.

That's all for today. Overall, there's a lot of optimism around a US-Iran deal, and that optimism continues to be tested. We've seen a meaningful pullback in oil and yields over the past 4-5 sessions, but none of it matters if a deal doesn't eventuate.

Shanxi coal mine incident tightens met coal supply

[1:32 pm] UBS sees the Shanxi mine disaster lifting met coal prices in the near-term.

Gas explosion at Liushenyu mine (22 May) killed 82 workers, triggering closure of 25 mines in Qinyuan (~26Mtpa) and 2-7 day halts at 109 underground met coal mines (122Mt, ~11% of China's domestic met coal output)

UBS forecasts met coal prices could rise US$15-20/t from current spot of US$240/t, with Shanxi sitting at the low-cost end of the global cost curve

Historical precedent points to a modest +3-5% price lift over 10-30 days post-incident, with May-timed events typically driving stronger and more persistent gains due to supportive restocking and industrial activity

CRN offers the highest leverage to met coal price moves, while WHC is flagged as a lower-risk, more liquid way to play the theme

Elevated met coal prices could compress steel mill margins and tighten low-grade iron ore discounts, a negative skew for FMG and MIN versus BHP and RIO

Flight Centre slips as guidance no reaffirmed at Investor Day

[1:30 pm] Flight Centre trading 3.1% lower ($9.96) as its Investor Day presentation this morning flagged accelerating headwinds in the leisure segment and no reaffirmed guidance commentary.

April leisure profit hit estimated at $10m, predominantly from refunds, with May and June (typically stronger leisure months) at risk of greater impact from ongoing volatility, cancellations and reduced forward bookings

Corporate business not significantly impacted, though management monitoring potential flow-on effects from higher airfares and macro factors, more likely to hit early FY27

Cost margin down to 9.2% after Q3, with discretionary spend halted, a support role freeze in place and capex prioritisation underway

Goodman Group Q3 earnings call highlights

[12:55 pm] Management reiterated FY26 guidance and pointed to a structurally constrained, AI-fuelled data centre and industrial pipeline as the key growth engine.

Operating EPS growth of at least 9% for FY26 reaffirmed, with potential upside from performance fees and revenue timing

Work in progress targeted at $18bn by June 2026, with data centre production run rate of 400-500MW per year over the next 12 months seen as sustainable

Total data centre development pipeline of ~6GW, implying a 10-11 year runway at current build pace, with stabilised assets expected to more than double their contribution to investment income over 2-3 years

Industrial pipeline targeting blended yields on cost in the high 7% to 8% range, with billion-dollar automated warehouses becoming a larger feature of the book

Over $10bn of retained earnings flagged to fund long-term asset holdings over the next 5 years, with data centres and industrial assets each expected to reach 50% of investment income longer term

Key risks remain power availability and capital scarcity, though rising barriers to entry (land, approvals, power, capital) are viewed as a competitive advantage

Company page: Goodman Group (GMG)

Taiwan overtakes India in stock market value

[12:52 pm] Taiwan's equity market has climbed to fifth largest globally, driven by TSMC's AI-fuelled rally, while India struggles with outflows and slowing earnings, Bloomberg reports.

Taiwan's market cap reached $4.95tn vs India's $4.92tn, placing it behind only the US, mainland China, Japan and Hong Kong

TSMC now accounts for ~42% of Taiwan's benchmark index, with shares up 49% year-to-date on AI demand

Regulatory tailwind: Taiwan lifted the single-stock cap for domestic funds from 10% to 25% (only TSMC qualifies), which JPMorgan estimates could draw over $6bn of inflows

India's benchmark is down 8% YTD, on track for its first annual decline in a decade, with global funds selling nearly $24bn of local equities

India's weight in the MSCI EM index has fallen to ~12% from 19% a year ago, hit by elevated valuations, a weaker rupee and limited AI exposure

Despite the market shift, India's $4.15tn economy still dwarfs Taiwan's $977bn GDP, leaving a structural disconnect between economic and equity market scale

Source: Bloomberg

Top ASX 200 gainers and losers at noon

[12:15 pm] Fisher & Paykel continues to hold onto its results-driven gains, industrial stocks like NRW, Develop Global and Genusplus catch a bid, while coal stocks experience a slight pullback after Monday's broad-based rally.

Ticker | Company | % Chg | Price |

|---|---|---|---|

FPH | Fisher & Paykel | 7.30% | $29.54 |

SGM | Sims | 3.52% | $24.97 |

LSF | L1 Long Short Fund | 3.08% | $4.35 |

CEN | Contact Energy | 2.86% | $7.90 |

NWH | NRW | 2.78% | $7.40 |

DVP | Develop Global | 2.74% | $6.01 |

GNP | Genusplus Group | 2.48% | $10.12 |

SRL | Sunrise Energy Metals | 1.99% | $15.39 |

VNT | Ventia Services Group | 1.79% | $6.26 |

AAI | Alcoa Corporation | 1.77% | $100.84 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

ASX | ASX | -11.90% | $51.81 |

ELV | Elevra Lithium | -8.19% | $12.67 |

PXA | Pexa Group | -6.66% | $10.72 |

TLX | Telix Pharmaceuticals | -6.33% | $12.58 |

IFT | Infratil | -5.67% | $12.32 |

WHC | Whitehaven Coal | -5.19% | $8.41 |

YAL | Yancoal Australia | -4.69% | $6.71 |

NHC | New Hope Corporation | -4.08% | $5.53 |

4DX | 4DMedical | -4.05% | $3.32 |

TWE | Treasury Wine Estates | -3.90% | $4.43 |

Mach7 Technologies CEO Thomas buys 200k shares

[12:13 pm] Mach7 Technologies CEO Teri Thomas has lodged an Appendix 3Y disclosing the on-market purchase of 200k shares. This represents a 57% increase in shareholding, to 550,000 shares. Mach7 shares are down 50% year-to-date.

Company page: Mach7 Technologies (M7T)

ASX 200 slips after a three-day winning streak

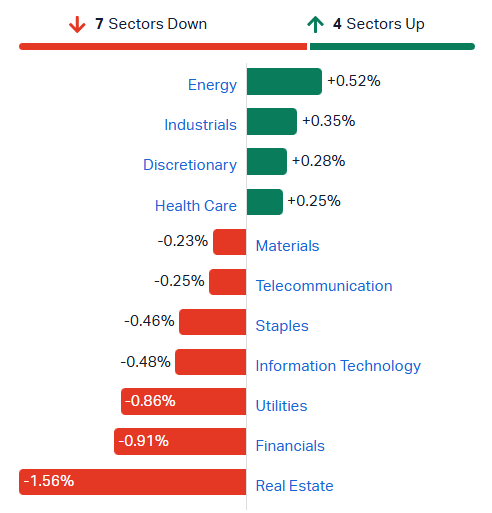

[11:22 am] A fairly soft day for markets, with the ASX 200 down 0.37%, though off session lows of (-0.73%). Breadth is fairly weak, with seven sectors red and 124 (62%) of constituents lower. The Big Four Banks are all down around 0.5%, Real Estate sector hit by a 3.5% dip for Goodman Group, while Utilities weighed by a pullback in energy/LNG prices.

S&P/ASX 200 sectors (Source: Market Index)

Kogan soars 15% on trading update

[11:08 am] Kogan is trading sharply higher after the company announced an upbeat trading update for the 10 months ended 30 April 2026.

The stock rallied as much as 20% in early trade, currently up 15.1% to $3.96. The strong one-day gain has lifted the stock back into positive year-to-date territory (+9.5%), and flat over the last twelve months.

Key numbers from the update include:

Group gross sales up 13.2% to $875.6m, with Kogan.com up 18.2%

Group revenue up 6.0% to $433.7m, with Kogan.com up 18.1%

Group gross profit up 11.1% to $177.9m, with gross margin up 1.9pp to 41.0%

Group adjusted EBITDA up 17.4% to $37.5m

Group adjusted EBITDA margin of 8.6%, at the upper end of FY26 guidance, with Kogan.com standalone margin of 11.5%

Analysts' take on Charter Hall

[11:02 am] Charter Hall delivered its third FY26 earnings upgrade on Monday, lifting guidance by 3% toward the upper end of consensus. This was driven by record equity capital raising and strong funds management momentum, with the stock up 6.7% on the day.

JPMorgan upgraded to Neutral from Underweight, target retained at $21.00. The third earnings upgrade confirms a strong track record of delivering on guidance, with record equity inflows positioning FY27 for earnings acceleration as deployment activity flows through.

UBS retained Buy, raised target from $24.50 to $24.75. Earnings forecasts lifted for FY27 onward on accelerating institutional and retail flows, with strong growth justifying current valuation and an attractive entry point on a growth-adjusted basis versus 10-year averages.

Jarden retained Neutral, raised target from $22.59 to $22.79. Capital raising and deployment velocity have reached unprecedented levels, though FY26 outperformance scope is limited with FY27 growth set to come from the annualised impact of current deployments, offsetting risks from moderating transaction activity.

Fisher & Paykel FY26 earnings call highlights

[11:00 am] Here are some interesting bits from the FPH earnings call.

FY27 guidance assumes hospital consumables and OSA masks growth similar to FY26, but hardware growth may be flat or decline after two strong years of US Airvo 3 and 950 system demand

FY27 gross margin to face net ~50bps headwind from tariffs and Middle East surcharges (70bps US tariff drag, 45bps raw materials, 25bps freight), offset by 50bps from continuous improvement initiatives

Anesthesia products growing more than 40% and now exceeding 10% of new applications revenue, penetrating slightly faster than high flow respiratory products did historically

Long-term gross margin target of 65% within two to three years if current conditions persist, with 67-68% achievable under favourable FX, supported by 100-150bps annual improvement from business initiatives

Company page: Fisher & Paykel Healthcare (FPH)

ASX tumbles on capex and expense blowout

[10:21 am] Shares in the exchange operator opened 3.8% lower this morning, now down 10.0% to $52.88. The company lifted its FY27 capex and cost expectations, while announcing the divestment of its 49% interest in Sympli.

FY26 reaffirmed: Revenue $1.03bn vs $1.24bn ests (17% miss), capex $170-180m vs $177.4m ests (in-line)

FY27 capex guided to $180-200m vs prior $160-180m and $174m ests (10% above)

FY27 total expenses growth guided at +18-21% y/y

FY28 capex guided at $170-190m

Dividend payout ratio of 75-85% of underlying NPAT reaffirmed, though ASX expects to pay at the bottom end of the range for at least the next two dividends

To divest 49% interest in Sympli to ATI Group for a nominal amount, resulting in an after-tax loss of ~$12m recognised as a significant item in FY26 results

This is a pretty ugly outcome considering the latest UBS modelling (30-Apr) expected FY27 expense growth of just 10%.

Company page: ASX Limited (ASX)

Top ASX 200 gainers

[10:15 am] Fisher & Paykel trading notably higher off the back of its FY26 results, a few odd industrial names like Mercury, Fletcher, GenusPlus also edging higher in early trade.

Ticker | Company | % Chg | Price |

|---|---|---|---|

FPH | Fisher & Paykel | 6.65% | $29.36 |

MCY | Mercury Nz | 3.79% | $5.75 |

FBU | Fletcher Building | 1.95% | $2.61 |

LSF | L1 Long Short Fund | 1.90% | $4.30 |

DVP | Develop Global | 1.88% | $5.96 |

GNP | Genusplus Group | 1.67% | $10.04 |

MEZ | Meridian Energy | 1.59% | $4.81 |

EVT | EVT | 1.42% | $12.17 |

AIA | Auckland International Airport | 1.41% | $6.85 |

APE | Eagers Automotive | 1.37% | $22.17 |

Top ASX 200 losers

[10:15 am] The exchange operator is trading sharply lower after lifting its FY27 capex guidance from $160-180 million to $180-200 million, data centre names like Infratil and Goodman Group also under pressure off the back of earnings/updates this morning.

Ticker | Company | % Chg | Price |

|---|---|---|---|

ASX | ASX | -7.60% | $54.34 |

PXA | Pexa Group | -4.36% | $10.98 |

IFT | Infratil | -3.83% | $12.56 |

GMG | Goodman Group | -3.03% | $29.14 |

CGF | Challenger | -2.78% | $9.09 |

ELV | Elevra Lithium | -2.68% | $13.43 |

PDI | Predictive Discovery | -2.47% | $0.71 |

TLX | Telix Pharmaceuticals | -2.38% | $13.11 |

MI6 | Minerals 260 | -2.33% | $0.84 |

ZIP | Zip | -2.00% | $2.21 |

Flight Centre flags FY26 leisure hit from Middle East tensions

[9:45 am] Flight Centre's Investor Day says Middle East volatility is weighing heavily on Q4 leisure performance after a strong nine-month run.

April leisure profit hit estimated at $10m, predominantly from refunds, with May and June (typically stronger leisure months) at risk of greater impact from ongoing volatility, cancellations and reduced forward bookings

Corporate business not significantly impacted, though management monitoring potential flow-on effects from higher airfares and macro factors, more likely to hit early FY27

Cost margin down to 9.2% after Q3, with discretionary spend halted, a support role freeze in place and capex prioritisation underway

Management leaning into short-to-mid-haul international and domestic promotion to grow share, while leveraging supplier relationships for preferential pricing and capacity

Flight Centre had already updated the market on 5 May, where management reaffirmed FY26 underlying profit before tax guidance. However, today's commentary regarding the key May-June leisure trading period may draw some criticism. Flight Centre shares are down 31% year-to-date and trading near August 2020 levels.

Company page: Flight Centre (FLT)

Goodman Group reaffirms FY26 guidance in Q3 update

[9:41 am] Goodman Group has delivered a solid Q3 operational update with portfolio metrics steady and FY26 earnings guidance reaffirmed.

Like-for-like net property income up 4.1% year-on-year

Occupancy of 95.7% with WALE of 4.9 years

Total property portfolio of $87.1bn

Work in progress of $14.5bn

FY26 operating EPS guidance reaffirmed at 9% growth year-on-year

Management commentary: "Hyperscale capex is accelerating, with our metropolitan portfolio positioned at the centre of cloud and AI demand, and the shift towards low-latency dependant AI inferencing. Supply remains constrained by grid capacity, water availability, site complexity and capital intensity."

It's worth noting that Goodman Group has a strong track record of upgrading its full-year guidance during the year, so it is interesting to see guidance reaffirmed at 9% growth while consensus is sitting at 10%.

Company page: Goodman Group (GMG)

NRW Holdings subsidiary Fredon secures ~$120m in new contracts

[9:40 am] NRW Holdings' wholly owned subsidiary Fredon has secured a suite of electrical and communications contracts across Victoria and WA.

Additional $69m electrical package on an existing Lend Lease data centre project in Victoria, taking Fredon's total contract value for the site to ~$155m with completion planned for August 2027

$26m electrical and communications package for the Bunbury Hospital Redevelopment in WA, commencing April 2026 with completion expected around April 2028

$16m electrical, ICT and security package for the University of WA Nedlands Student Accommodation project in partnership with Lendlease, completion planned for June 2027

$10m electrical and security package for the 609 Wellington St Purpose Built Student Accommodation project in Perth CBD, completion scheduled for June 2027

Company page: NRW Holdings (NWH)

BHP shelves Pilbara decarbonisation plans, leaked documents reveal

[9:31 am Exclusively leaked internal documents to Four Corners and Guardian Australia show BHP has quietly delayed major renewable energy and electric vehicle projects in the Pilbara despite public climate commitments, with no clear pathway to net zero post-2030.

BHP has allocated no funding to major Pilbara renewable projects until 2031, with diesel trucks locked in at two WA mines until the late 2030s and potentially to 2041

$400m Jimblebar solar farm approved by the board in June 2023 was halted shortly after due to "cash prioritisation requirements", with the replacement $1.3bn solar/wind/battery project also shelved

WA iron ore operations account for ~30% of BHP's global emissions, but are forecast to cut emissions by just 1% by 2030

Company's gas-fired power plant is being expanded while the renewables pipeline is deferred

Source: ABC

Santos lays out tier-1 strategy and capital framework at Investor Day

[9:25 am] Santos has outlined its strategy and financial framework focused on tier-1 basins, growing free cash flow and a sharper capital allocation policy targeting shareholder returns.

Barossa at 75% of planned 2026 production rates, targeting plateau production mid-2026 with unit production cost less than $7/boe

Pikka phase 1 in Alaska producing intermittently during final commissioning, with continuous production imminent and plateau production of ~80,000 bopd (gross) targeted in 3Q26 at unit production cost less than $8/boe

New capital allocation framework targets disciplined growth within a $45-50/bbl breakeven and return of at least 60% of free cash flow to shareholders

Once Barossa and Pikka are at plateau, every $10/bbl above free cash flow breakeven generates an expected $550-600m in annual free cash flow

Targeting ~$2.5bn net debt reduction by 2030 to reach the lower end of the 15-25% gearing range, cutting annual interest by ~$150m

Upstream investment to be prioritised in Moomba Central fields and deprioritised across the broader Cooper Basin, targeting cumulative capex reduction of ~$300m from 2027-2030 and $150m in annual savings thereafter

Company page: Santos (STO)

Atlas Arteria board unanimously rejects IFM takeover bid

[9:22 am] Atlas Arteria's independent directors have unanimously recommended securityholders reject IFM's $4.75 cash offer, with the independent expert concluding the bid is neither fair nor reasonable.

IFM offer was $4.75 cash per share, with potential step-up to $5.10 if relevant interest reaches 45% or more before close

$4.75 represents a premium of less than 10% to the last closing price prior to the offer, with the bidder having paid more than $5.10 for a non-controlling interest as recently as September 2025

Independent expert Kroll Australia's control valuation range of $5.39 to $6.20 per security, materially above the offer

Offer is highly conditional with 13 separate categories of conditions including waiver of the OTPP Put Option, with no certainty the $5.10 step-up will be triggered

Board flagged potential value-realisation pathways including a possible Chicago Skyway divestment and other asset sales, with proceeds anticipated to be returned to securityholders

Company page: Atlas Arteria (ALX)

Kogan delivers 10-month update, EBITDA margin at upper end of FY26 guidance

[9:21 am] Kogan.com has reported solid sales and earnings growth for the 10 months to 30 April, with Kogan.com driving group performance and Mighty Ape's turnaround accelerating.

Group gross sales up 13.2% to $875.6m, with Kogan.com up 18.2%

Group revenue up 6.0% to $433.7m, with Kogan.com up 18.1%

Group gross profit up 11.1% to $177.9m, with gross margin up 1.9pp to 41.0%

Group adjusted EBITDA up 17.4% to $37.5m

Group adjusted EBITDA margin of 8.6%, at the upper end of FY26 guidance, with Kogan.com standalone margin of 11.5%

Group active customers up 4% to 3.5m, with Kogan.com active customers up 9%

Kogan shares have held up relatively well compared to some discretionary and eCommerce peers. The stock is down 6.2% year-to-date and down 15% in the last twelve months.

Company page: Kogan.com (KGN)

Greatland secures final environmental approvals for Havieron

[9:19 am] Greatland Resources has received Western Australian state environmental approval for Havieron, completing the primary permitting required for development.

WA Minister for the Environment granted Part IV approval on 25 May 2026, following Commonwealth EPBC Act approval received 24 April 2026

Final Investment Decision targeted in the current June 2026 quarter

Tendering for critical path project packages and early works already underway, including boxcut tunnel installation, underground development and blind bore construction preparation

Steady-state production guidance of ~270koz gold per annum at lowest quartile costs, with an initial mine life of 17 years

Company page: Greatland Resources (GGP)

Silver Mines acquires strategic land package adjacent to Bowdens Silver

[9:18 am] Silver Mines has acquired a strategic parcel of freehold land and water entitlements next to its flagship Bowdens Silver Project for $12.5 million cash.

Acquisition consideration of $12.5m in cash, with $1.76m already paid, funded from existing cash reserves

Post-completion Silver Mines will own ~3,345 hectares of freehold land, covering the entire Bowdens Silver Project licence area plus a substantial buffer

Strategic benefits include enhanced project water security, biodiversity offset opportunities, employee housing and infrastructure flexibility, while supporting ongoing grazing and cropping

Bowdens Definitive Feasibility Study remains on track for completion around mid-year

Company page: Silver Mines (SVL)

Treasury Wine Estates brings forward CFO retirement

[9:16 am] Treasury Wine Estates has brought forward the retirement of its Chief Financial and Strategy Officer Stuart Boxer, with an interim appointment in place.

Stuart Boxer's retirement brought forward to 30 June from 30 September

Deputy CFO Justin Pipito to assume the Chief Financial and Strategy Officer role on an interim basis from 1 June

External and internal search for permanent CFO progressing well

Company page: Treasury Wine Estates (TWE)

Viva Leisure upgrades FY26 NPAT guidance, reaffirms revenue and EBITDA

[9:14 am] Viva Leisure has upgraded its FY26 NPAT guidance on stronger margins and accelerating contribution from its technology division, while reaffirming revenue and EBITDA.

FY26 underlying NPAT now expected to exceed $17m vs prior >$16m

FY26 statutory NPAT now expected to exceed $12m vs prior >$11.5m, representing growth of more than 130% on FY25's $5.2m

Technology, Payments, Licensing & Retail (TPLR) division tracking ~30% year-on-year

Total network membership of ~680k, up ~9.5% on FY25 closing of 620,902, with corporate clubs at portfolio utilisation of ~80%, the highest in company history

Net leverage of 1.90x vs covenant of 2.50x, with on-market share buyback continuing

Over 100 committed franchise and corporate locations still to open, with ~30 expected to open in 1H27, supporting growth re-acceleration

Company page: Viva Leisure (VVA)

MinRes and Ganfeng sanction $490m Mt Marion expansion

[9:13 am] Mineral Resources and JV partner Ganfeng have made final investment decision on a flotation plant and underground development at Mt Marion, with payback flagged at under one year at current spot prices.

Total capex of $490m on a 100% basis across FY27 and FY28, split between flotation plant ($240m), underground pre-production development ($220m) and non-processing infrastructure ($30m)

Payback of less than one year at current spot spodumene price of ~US$2,700/t SC6

Installed capacity to increase 20% from ~500ktpa SC6 to 600ktpa SC6, with plant recovery improving towards 70% and the lower-grade SC3.5 product removed to deliver a single SC5 product

Mine life extended via access to additional resources below the existing open pit, with underground ore set to supplement up to 40% of processing feed from FY28

Construction targeted to commence Q1 FY27 with commissioning and ramp-up in 2H FY28, minimal disruption to existing operations expected

Company page: Mineral Resources (MIN)

Fisher & Paykel Healthcare delivers strong FY26 result, FY27 guidance slightly soft on revenue

[9:10 am] Fisher & Paykel Healthcare reported double-digit revenue and profit growth, beating its own NPAT guidance, though FY27 revenue guidance came in below consensus.

Revenue up 14% to NZ$2.31bn vs NZ$2.30bn ests (in line)

Hospital revenue up 18% to NZ$1.51bn

Consumables up 16% despite subdued seasonal respiratory illness activity

Homecare revenue up 8% to NZ$802.7m, with OSA masks up 7%

Gross margin up 80bps to 63.7% vs 63.1% ests, absorbing ~90bps headwind from US tariffs on NZ-sourced hospital products

NPAT up 24% to NZ$468.5m vs guidance of NZ$450-470m and NZ$467.6m ests (in line),

Total dividend up 22% to 52.0cps

FY27 guidance: Revenue NZ$2.45-2.57bn vs NZ$2.56bn ests (2% miss at midpoint), NPAT NZ$500-550m vs NZ$538.8m ests (3% miss at midpoint), including 50bps net GM headwind from US tariffs and Middle East conflict

NZX-listed Fisher & Paykel shares are up 9.9% this morning.

Company page: Fisher & Paykel Healthcare (FPH)

Infratil delivers FY26 earnings growth, flags strong FY27 outlook

[9:02 am] Infratil reported solid FY26 results driven by data centres and renewables, with FY27 guidance materially ahead of consensus on AI-led infrastructure demand.

Operating revenue of NZ$3.49bn vs NZ$3.39bn ests (3% beat)

Proportionate operational EBITDAF up 11% to NZ$989m vs NZ$997.7m ests (in-line)

Net parent surplus of NZ$550m (FY25: loss of NZ$295m)

Proportionate capex up 17% to NZ$2.7bn, total asset value up 13% to NZ$20.6bn

Full year dividend of 20.9cps

FY27 guidance: Proportionate EBITDAF NZ$1.30-1.40bn, unclear if comparable to NZ$1.09bn ests, indicates ~21% year-on-year growth, with capex of NZ$3.8-4.4bn

CDC forecasts EBITDAF to grow more than 150% to over A$1bn by FY28, while Longroad Energy EBITDAF up 170% to US$121m and targeting US$1bn run-rate by CY29-30

Over NZ$600m of assets divested in FY26 with potential for another ~NZ$1bn in medium term, including a sale process underway for Qscan

NZX-listed Infratil shares are down 3.0% this morning.

Company page: Infratil (IFT)

Zimplats responds to Zimbabwe critical minerals classification

[9:01 am] Zimplats has acknowledged the Zimbabwean government's new policy framework classifying PGMs as critical minerals, with further details pending.

Zimbabwean government announced on 22 May classifying PGMs and other minerals as critical minerals under a new policy framework

Zimplats is engaging with authorities to understand the full implications, with further details from the government expected in due course

Company flagged its position as one of the largest contributors to the Zimbabwean economy via FX generation, employment, infrastructure and fiscal contributions

Key uncertainty for investors is whether the new framework introduces additional royalties, export restrictions or beneficiation requirements that could weigh on margins

Company page: Zimplats (ZIM)

Strike Energy chair Poynton sells 4.3m shares

[8:58 am] Outgoing chair John Poynton has lodged an Appendix 3Y disclosing the sale of 4.3 million Strike Energy shares at 12.2 cents a piece. This cuts his beneficial shareholding by 27% to 11.9 million shares.

Company page: Strike Energy (STX)

UBS holds steady on silver, sees muted upside

[8:56 am] UBS maintains a stable US$80/oz forecast across all tenors, with elevated prices weighing on demand and the risk/reward looking unappealing for long positions.

Silver forecasts unchanged at US$80/oz through to Jun-27

2026 market deficit narrowed to 60-70m oz (from 300m oz previously), with risk demand could prove even less resilient

Silver up over 140% over the past year, with elevated prices eroding demand in jewellery, silverware and photovoltaics

ETF holdings down over 67Moz YTD to around 794Moz, with overall investment demand expected at 300Moz this year vs nearly 440Moz last year

Unlike gold, silver lacks central bank buying support and is likely to lag, though high correlation with gold and a weaker USD should provide underlying support

UBS lifts copper forecasts on widening supply deficit

[8:54 am] UBS reiterates a constructive copper view, with persistent supply tightness expected to underpin prices through 2027.

Forecasts copper at US$14,000/mt by Sep-26 and introduces new Jun-27 target of US$15,500/mt

LME copper briefly exceeded US$14,000/mt in May, with spot at US$13,497/mt as of 22 May

2026 market deficit estimated at 520,000mt, widening from 203,000mt in 2025, driven by sulphuric acid export restrictions in China, tight scrap and concentrate supply, and Freeport's Grasberg delay to early 2028

2026 benchmark TCRCs collapsed to $0/mt (from around $25/mt in 2025) with spot below -$100/mt, reflecting fierce smelter competition for concentrate

Global copper demand forecast to grow 2.8% in 2026 on grid investment, EV adoption and data centre buildout, while refined supply growth projected at just 1.7%

Prefers long copper positions, viewing pullbacks toward US$12,800-13,000/mt as attractive entry points and favouring volatility-selling strategies to the downside

Yardeni's "FEMO" thesis: Rally driven by earnings, not hype

[8:52 am] Yardeni Research argues the market's surge since March is rational, powered by upgraded earnings rather than speculative FOMO.

S&P 500 up 9.2% YTD through Friday, with forward earnings up 14.4% and forward P/E down 4.6%, suggesting the rally is being driven by fundamentals rather than multiple expansion

Coins the term "FEMO" (Fabulous Earnings Momentum) to describe analyst upgrades backed by hard data and company guidance, contrasting it with hope-and-hype-driven FOMO

Forward P/E of 21.1x not viewed as irrationally valued absent a recession, which Yardeni does not foresee

Introduces "Buzz Lightyear Theory" arguing data is a fourth factor of production alongside land, labour and capital, with unlimited supply supporting structurally higher productivity

Pushes back on bubble narratives around AI exuberance, noting multiples have actually compressed despite the rally

Oil prices tumble, yields dip

[8:48 am] Brent settled 10.1% lower overnight to US$93.63 a barrel, the lowest since 17 April.

Brent crude daily price chart (Source: TradingView)

The easing oil price backdrop has pulled global bond yields sharply lower, with the German 10-year down 10 bps overnight to 2.93% and now down 25 bps in the last four sessions.

German government 10-year bond yield (Source: TradingView)

The Aussie 10-year has also down 23 bps in the last four sessions to 4.87%, the lowest since 10 March.

Australia government 10-year bond yield (Source: TradingView)

The Fed is now more likely to hold by year-end, with the likelihood of a 25 bp cut falling to 39.5% vs. 42.5% a day ago.

Source: CME Fedwatch Tool

Trump pushes Saudi Arabia and Qatar to recognise Israel as part of Iran deal

[8:41 am] Trump is tying expansion of the Abraham Accords to any Iran peace agreement, raising the diplomatic stakes around the emerging deal.

Trump said it should be "mandatory" that Saudi Arabia, Qatar, Pakistan, Turkey, Egypt and Jordan join the Abraham Accords alongside any Iran deal, warning non-signatories should be excluded from the agreement

Iran talks described as "proceeding nicely", with the interim deal expected to extend the ceasefire by around two months, lift the US naval blockade of Iranian ports and reopen the Strait of Hormuz

Key sticking points remain unresolved, including free passage through Hormuz (Iran wants to charge vessels for "navigation services"), the pace of unfreezing Iranian funds, and Israel's demand to preserve military freedom of action across all fronts including Lebanon

US is demanding Iran hand over ~400kg of highly-enriched uranium and cease enrichment for around 20 years in any follow-on nuclear deal, terms that face pushback from Tehran

Source: Bloomberg

European stocks hit two-month high on Iran peace hopes

[8:36 am] European equities rallied alongside Asian peers as easing Middle East tensions sent oil tumbling and lifted risk sentiment globally.

US market closed in observance of Memorial Day, UK market also shut for Spring Bank Holiday

STOXX 600 closed up 1% and within 1% of February's record high, recovering all losses since the Middle East conflict began

Brent tumbled ~10% to US$93 a barrel after Trump said a framework to reopen the Strait of Hormuz had been "largely negotiated" with Iran

Banks led gains (~2%) on the STOXX, while airlines rallied on lower fuel costs

European tech sector up over 25% this quarter, with ASML +1.5% and Schneider Electric +3.1% on continued AI enthusiasm

Japan's Nikkei topped 65,000 for the first time, with its three-day gain of 8.95% the steepest in over six years

Good morning!

[8:30 am] ASX 200 futures are up 24 pts (+0.27%).

The overnight session in a nutshell:

US markets closed for Memorial Day, but US futures higher after Trump said negotiations with Iran over an interim deal is “proceeding nicely”

Europe’s STOXX 600 rallied 1% to close within an arms reach of all-time highs, Nikkei 225 and Taiex both closed at record levels

Brent down 10.1% to US$93.63 a barrel, a near five-week low