ASX 200 Live Today - Thursday, 12th February

The S&P/ASX 200 is set to open flat ahead of a very busy day for 1H26 results. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Thursday, February 12. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Be sure to refresh manually for the latest updates — and let us know how we can make it even better.

ASX 200 higher, soaring banks and miners offset tumbling tech and healthcare

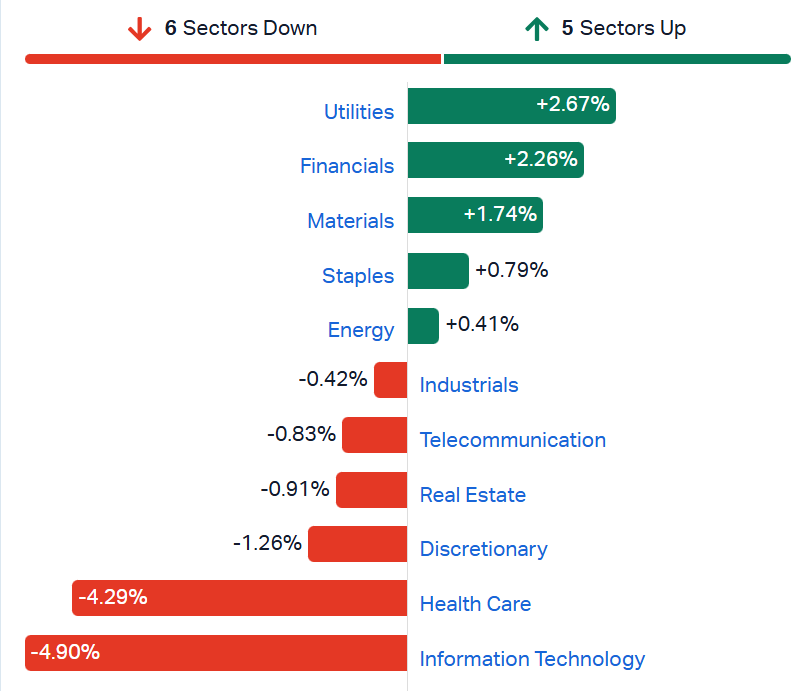

[2:10 pm] The ASX 200 has eased slightly off session highs, currently up 0.56%. Strength in Utilities (+3.3%), Financials (+2.6%) and Materials (+1.4%) has offset the sharp declines in the Tech (-5.4%) and Healthcare (-5.1%) sectors.

The volatility we're seeing reminds me of some of the commentary we're seeing on Wall Street: "Over the past month, SPX was up 0 bps while stocks on average moved almost 11%. McElligott points out that we’re seeing stunningly large, and highly divergent, moves across single-name equities and their volatility. But those moves are effectively offsetting each other at the index level, muting spot performance and suppressing index volatility via a classic “correlation crunch," Nomura analysts said in a note.

Anyway, the market seems to be in good stead as bank earnings (CBA yesterday) continue to top market expectations and commodity prices continue to hold up relatively well amid an uptick in volatility. It's interesting to see these banks eke out some decent beats, but re-rate quite aggressively (CBA up 12% in the last two sessions). On the flip side, tech continues to tumble into the abyss. The S&P/ASX 200 Tech Index is down 5.5% and ~0.4% away from last Friday's low. That's all for today, a very messy results day, with TPW, PME and AMP all selling off sharply despite results that may not necessary read that bad at face value. I'll catch you all tomorrow.

Tech gives back gains

[1:06 pm] The S&P/ASX 200 Tech index has given back almost all of its recent gains (6.2% bounce between 9-11 Feb), down 5.3% and on the cusp of undercutting last Friday's low.

AMP obliterated

[12:17 pm] AMP is trading sharply lower, down 28% after reporting a broadly weaker-than-expected result for 2025. While a few headline items were in-line, most business divisions missed analyst expectations.

Barrenjoey's first take: "AMP’s 2H25 result was in line at the headline, supported by lower tax. Revenue was below expectations across most divisions, with the outlook for revenue margins below expectations and likely to drive consensus downgrades to FY26 and outer years. Capital was not as strong as expected, so it is difficult to see what supports the share price today."

Northern Star earnings call highlights

[12:13 pm] Northern Star is trading ~5% higher following its 1H26 result, which was modestly ahead of market expectations. Cash flow was soft, reflecting ongoing investments into KCGM and Hemi. A few incremental bits of new info from the earnings call, including:

Final investment decision for the Hemi project is likely deferred to FY27 due to extended regulatory approvals, with first gold expected in FY30 at the earliest.

KCGM mill expansion commissioning is scheduled for early FY27, with production guidance of 750,000–800,000 ounces and high-grade ore prioritised during ramp-up.

Strong mining performance at KCGM in H1, with record tonnage moved and robust high-grade stockpiles, supports confidence in H2 cash flows and a dividend payout above the policy midpoint.

No immediate plans to pre-deliver against the hedge book, maintaining flexibility while free cash flow improves.

Portfolio rationalisation continues, with focus on organic growth and operational efficiency rather than acquisitions, and updated FY 2027 production guidance will be provided once schedules and stockpiles are confirmed.

Analysts mixed on Computershare

[12:10 pm] Computereshare suffered a 3.1% dip on Wednesday, despite opening 6.2% higher. The company reported a 1H26 result that was modestly ahead of consensus, as well as a slight upgrade to its FY26 guidance.

Morgan Stanley upgraded to equal-weight, raised target from $32.10 to $32.40. EPS growth improving (~6.7% FY26), strong revenue in Issuer Services and Corporate Trust, elevated costs investment-driven, earnings quality expected to improve as restructuring costs roll off.

JPMorgan upgraded to overweight, raised target from $35.50 to $36.50. FY26 EPS beat with solid operating momentum, margin income resilient, tokenisation risks modest, share price weakness considered overdone.

Goldman Sachs maintained buy, lowered target from $40 to $38. NPAT ahead of consensus due to stronger revenue and lower interest expense, elevated expenses from tech and growth reinvestment, caution on normalisation of transactional revenues, tokenisation a key risk.

ASX 200 within 0.3% of all-time highs

[12:02 pm] ASX 200 up 0.60% and pushing session highs. Banks have continued to rally for a second session, with CBA up 3.8% (now up 10.9% since Wednesday) and ANZ soaring 7.2% off the back of its 1Q26 update. Miners also trading broadly higher, with the S&P/ASX 200 Materials Index within 0.1% of its 30-Jan all-time high.

ASX 200 sector performance (Source: Market Index)

CBA remains sell-rated, analysts reluctantly lift target prices

[11:14 am] CBA rallied 6.8% on Wednesday after its 1H26 result topped market expectations, including a ~5% NPAT beat, strong lending growth and low loan losses. Analysts remain broadly sell-rated due to valuation, but nudged target prices slightly higher.

Morgan Stanley maintained underweight, raised target from $131.00 to $140.00. Strong franchise performance lifted earnings confidence, deposit mix shifts are a key swing factor, higher rates provided margin support, but valuation rebound seen as unjustified.

Goldman Sachs maintained sell, raised target from $134.00 to $137.85. Revenue strength drove earnings beat, cost growth limited operating leverage, macro tailwinds expected to moderate, prefer peers for stronger profit growth.

UBS maintained sell, raised target from $125.00 to $130.00. Transaction deposit growth widened retail moat, mortgage momentum supported income outlook, technology investment to pressure expenses, valuation viewed as stretched despite upgrades.

Analysts slash CSL target prices

[11:11 am] CSL's first-half FY26 result on Wednesday was broadly weaker-than-expected, with Behring a clear drag on the Group. Management reaffirmed FY26 guidance, but analysts viewed this as requiring a big second half uplift. The stock managed to close just 4.6% lower vs. an initial 12% selloff. Here's what analysts are thinking:

Morgan Stanley retained overweight, lowered target from $242.00 to $215.00. Guidance seen as achievable with strong cost discipline, Behring recovery critical, valuation supportive despite near-term risks.

RBC Capital Markets downgraded to sector perform, lowered target from $230.00 to $176.00. Result missed key metrics, doubts over FY guidance delivery, CEO transition seen as stock overhang, medium-term growth targets at risk.

UBS retained buy, lowered target from $275.00 to $235.00. Interim leadership restored some confidence, H2 sales acceleration viewed cautiously, cost reductions provide earnings buffer, margin recovery slower than previously assumed.

Origin beats profit, upgrades Energy Markets outlook

[10:30 am] A solid earnings beat was driven by Energy Markets, with guidance nudged higher and capex lifted slightly on batteries. ORG jumped 7.5% at the open to $11.63.

Revenue of $7.99bn vs $8.18bn ests (2.3% miss)

Underlying NPAT of $593m vs $551.3m ests (7.6% beat).

Interim dividend 30cps vs 30cps ests (in-line)

Energy Markets EBITDA of $860m vs $805m ests (6.8% beat)

Integrated Gas EBITDA of $798m vs $817m ests (2.3% miss).

Octopus Energy loss widened to $89m vs year ago $24m

Outlook was tightened at the midpoint, including:

Energy Markets FY26 underlying EBITDA guidance lifted to $1,550-1,750m, midpoint $1,650m, up 6.5% vs prior midpoint $1,550m.

Australia Pacific LNG production reaffirmed at 645-680 PJ.

Total Origin capex guidance lifted to $900-1,100m, midpoint $1,000m, up 5.3% vs prior midpoint $950m.

By Warren Masilamony | Company page: ASX (ORG)

Top ASX 200 gainers and losers

[10:30 am] Lot of results-driven movers, with Origin and Orora higher, and AMP and Pro Medicus sold to oblivion.

Viva Leisure’s H1 profit surges as buyback returns

[10:20 am] VVA H1 results beat consensus estimates on revenue and profit, while FY26 guidance is framed as minimums and management is leaning into capital management.

Revenue up 18% to $116.5m vs $115.8m ests (0.6% beat)

Net profit attributable to members up 168% to $5.23m vs $3.8m ests (38% beat)

FY26 guidance: underlying NPAT >$16m, revenue >$237m vs $238.3m ests (floor 0.5% below), statutory EBITDA >$111m vs $112m ests (floor 0.9% below), underlying EBITDA >$53m

Viva Leisure plans to recommence an on-market buyback of up to 10% of shares

By Warren Masilamony | Company page: ASX (VVA)

ASX beats on revenue, dividend trimmed

[10:14 am] Strong trading activity lifted half year earnings, but regulatory costs and higher spend squeezed margins and dragged the interim dividend lower.

Markets revenue up 14% as average daily on market trading value rose to $6.9bn (+23% y/y), while clearing and settlement each grew 22% on higher traded value and retail activity.

EBITDA up 8% to $370.4m

Total expenses up 20% to $264.3m

Australian Securities and Investments Commission inquiry costs of $17.3m plus higher cloud, licensing and program spen

Underlying NPAT up 4% to $263.6m, with net interest income down 7% to $40.2m

Lower earnings on cash balances after Reserve Bank of Australia cash rate cuts partly offset by higher collateral income on participant balances.

Interim DPS down 8.5% to 101.8 cents

Capex of $83.1m in H1, including $49.5m on CHESS

FY26 capex guidance reaffirmed at $170-180m and FY27 at $160-180m, while medium-term underlying ROE target remains 12.5-14.0%.

By Warren Masilamony | Company page: ASX (ASX)

Lendlease CEO to step down in August 2026

[9:40 am] Lendlease announced that CEO Tony Lombardo will resign following FY26 results, after five years leading the Group.

Tony Lombardo to step down as CEO in August 2026 and relocate to South-East Asia for a new career opportunity

Lombardo has led Lendlease for 18 years, including five as Group CEO, overseeing the Group’s refreshed strategy

Board states FY27 is an inflection point and the transition provides an opportunity for new leadership to execute the next phase of the strategy

Board has engaged an international executive search firm to appoint a new Group CEO and will provide updates in due course

Company page: Lendlease Group (LLC)

AMP 1H26 earnings mixed

[9:39 am] AMP delivered its full-year results, noting growth across key divisions, supported by cost control and AUM expansion. I've used consensus for most in-items, and Macquarie's estimates for division earnings (Macquarie's forecasts sit a little above consensus).

Revenue down 1% to $1.29bn vs $1.30bn ests (in-line)

Underlying NPAT up 20.8% to $285m vs $284.6m ests (in-line)

Statutory NPAT down 11% to $133m vs $211m ests, reflecting legacy legal settlements and business simplification

Platforms underlying NPAT up 9% to $106m vs. Macquarie ests of $121m (12% miss)

Super & Investments underlying NPAT up 15% to $62m vs. Macquarie ests of $71m (12% miss)

Group AUM up 9% to $161.7bn vs $158.4bn ests (2.0% beat)

Total 2025 dividend of 4cps, in line with guidance

The results looks like a miss vs. a few specific broker notes (Macquarie and Citi).

Company page: AMP (AMP)

Pro Medicus profits surge on 4DMedical investment

[9:28 am] Pro Medicus delivered a massive profit uplift, though the gains were largely attributed to it's investment in 4DMedical.

Revenue up 28.4% to $124.8m vs $128.6m ests (3% miss)

Underlying profit before tax up 29.7% to $90.7m, unclear if comparable to Macquarie pre-tax profit (Jan-26) ests of $101.8m

Underlying EBIT margins up 100 bps to 73%

Reported net profit after tax up 230.9% to $171.2m

This includes unrealised gains of $149.1m from the company's $10m hybrid debt and equity investment in 4DMedical

Cash and cash equivalents up 5.3% to $221.8m

Interim dividend of 32 cps vs. Macquarie ests of 35 cps (8.5% miss)

Management commentary: Pipeline remains very strong across all market segments with many leads coming from the company's attendance at the RSNA conference in the US with RSNA 2025 being the most successful for the company to date.

Company page: Pro Medicus (PME)

Breville 1H26 EBIT in line with plan

[9:20 am] Breville delivered record first half revenue and EBIT growth, supported by geographic expansion, new product development, and tariff mitigation strategies.

Revenue up 11% to $1.10bn vs $1.11bn ests (1% miss)

EBIT up slightly to $145.8m vs $144.3m ests (1% beat)

NPAT up 2% to $98.2m vs $97.9m ests (0.3% beat)

Interim dividend up 5.6% to 19 cps vs. Morgans ests of 18 cps (5.5% beat)

US gross profit 80% manufactured outside China, with tariff impacts managed through diversification, pricing, and distribution mix

New product development and coffee segment drove double-digit revenue growth, with expansion into Mexico, China, Middle East, and Korea

Breville guided to a slight year-on-year EBIT increase for FY26, which is relatively in-line with consensus for ~0.1% growth.

Company page: Breville Group (BRG)

Temple & Webster 1H26 revenue growth accelerates

[9:15 am] Temple & Webster delivered strong half-year results with revenue up 20% and EBITDA in-line with guidance, supported by strategic growth initiatives.

Revenue up 20% to $375.9m vs $370.2m ests (1.5% beat)

EBITDA ex-items up 28% to $15.9m vs $15.3m ests (4% beat)

Margin 4.0% within FY26 guidance of 3–5%

Though slight miss vs. Morgan Stanley ests of 4.1%

Free cash flow $23m, cash balance $161m with no debt and $7.5m deployed in on-market share buy-back

A few operational metrics of interest:

Active customers up 14% to ~1.4m

Revenue per active customer stable at $472

Repeat customers now 62% of total orders; conversion rate up to 3.2%

Sales of exclusive products up 9% to 49% of total revenue (H1 FY25: 45%)

New Zealand revenue over $1m in four months post launch (~3,000 orders)

TPW noted 1-Jan to 9-Feb revenues up 20% year-on-year (so slight acceleration from previous 1-Jul to 20-Nov growth of 18%). Also reaffirmed FY26 guidance of 3-5% EBITDA margins.

TPW shares have been smashed in recent months, down 55% since late-October to the lowest since Nov-24.

Company page: Temple & Webster Group (TPW)

Northern Star 1H26 profit rises on higher gold prices

[9:10 am] Northern Star delivered strong half-year results driven by higher realised gold prices and maintained a solid balance sheet.

Revenue up 19% to $3.41bn vs $3.35bn ests (2% beat)

Average realised gold price up 31% to US$4,670/oz

Gold sales down 9% to 729koz

Underlying NPAT up 49% to $760m vs. $692m ests (10% beat)

Cash earnings of $1.10bn, in line with guidance of $1.06–1.11bn

Cost of sales increased 9% to $2.18bn due to higher mining activity, inflation, maintenance, depreciation, and royalties.

Interim dividend unchanged at 25 cps

Net cash position $293m, including cash and bullion $1.18bn

FY26 guidance reaffirmed, including gold sales of 1.60–1.70Moz and AISC A$2,600–2,800/oz

Overall, a fairly lackluster result from Northern Star (cash flows from operating activities fell 17.8% to $1.03 billion). Though not surprising given the volume of production and cost downgrades over the past 12 months. The company has a lot of work cut out for it amid its KCGM mill expansion and Hemi development.

Company page: Northern Star Resources (NST)

Insurance Australia 1H26 profit down, buy-back announced

[9:00 am] IAG posted lower half-year profits but maintained strong underlying margins and plans a share buy-back.

NPAT down 35.1% to $505m

GWP up 6% to $8.93bn vs $9.11bn ests (2% miss)

Underlying insurance margin 15.1% vs 14.9% ests (20 bp beat)

Interim dividend unchanged at 12 cps

Company to launch on-market buy-back of up to $200m

Guides FY26 GWP growth in high single digits vs. prior guidance of at least 10%

FY26 reported insurance profit expected $1.55–1.75bn (margin 14–16%)

Company page: Insurance Australia Group (IAG)

ANZ Q1 cash profit beats estimates

[8:57 am] ANZ delivered strong quarterly results, driven by cost reduction, revenue growth and improved return on equity.

Cash Profit of $1.94bn vs $1.80bn ests (8% beat)

Cash profit up 17% on 2H25 quarterly average (ex-significant items)

CET1 ratio up 12 bps to 12.15% at 31 December 2025

Cost-to-income ratio fell below 50% as expense reductions and productivity initiatives drove efficiency gains.

ANZ gained 1.3% on Wednesday, largely off the back of CBA's better-than-expected first-half FY26 result.

Company page: ANZ Group (ANZ)

Nickel prices surge as Indonesia cuts output

[8:55 am] Indonesia’s production quotas tighten supply, sending nickel prices higher and reshaping global markets.

LME nickel rose 2% to $17,835 a tonne, extending a rally of over 20% since mid-December amid speculative buying and geopolitical tensions.

Indonesia set national nickel ore quotas at 260–270m tonnes for 2026, down from the 379m tonnes targeted in 2025.

PT Weda Bay Nickel’s quota cut to 12m tonnes from 42m tonnes in 2025 will constrain output despite previous expansion plans; the company is seeking revisions.

Tighter Indonesian supply follows a two-year global nickel surplus that had depressed prices and forced closures in Australia and New Caledonia.

The Sprott Nickel Miners ETF rallied 7.6% overnight, so a very strong lead in for local nickel names like Nickel Industries (NIC), Centaurus (CTM), Nico Resources (NC1) and more.

US budget deficit set to rise, debt hits record levels

[8:50 am] Congressional Budget Office (CBO) projects widening deficits and growing federal debt over the next decade, with tariffs and interest costs shaping fiscal outlook.

2026 budget deficit projected at $1.9tn, up 8% from Jan-25 estimate

Federal debt held by the public expected to reach 101% of GDP this year and 120% by 2036.

Deficit growth driven by $4.7tn from the 2025 Reconciliation Act and $0.5tn from immigration measures, partially offset by $3tn reduction from tariffs.

Interest spending to rise to 3.3% of GDP in 2026 and 4.6% by 2036, accounting for roughly 20% of federal spending.

Customs duties expected to hit $418bn (1.3% of GDP) in 2026, exceeding corporate income tax receipts for the first time since 1934, though US businesses absorb 30% of import price rises, consumers the rest.

Trade deficit forecast to narrow from 2.7% of GDP in 2025 to 1.6% in 2036, while the US dollar is expected to weaken nearly 10% over the decade.

Pershing Square builds sizable Meta stake on AI optimism

[8:49 am] Bill Ackman’s fund sees Meta as undervalued, betting on long-term upside from AI despite market fears over spending.

Pershing Square’s Meta position equals 10% of fund capital as of end-2025, added in Q4 2025 alongside Amazon and Hertz stakes.

Meta shares down 16% over 12 months amid concerns over AI investment, with projected AI capex of $115bn–$135bn in 2026.

Meta trades at 22x forward earnings, cheaper than Alphabet, Apple and Nvidia, highlighting potential for growth from AI initiatives.

Pershing believes market underestimates Meta’s long-term AI upside and sees the current share price as a deeply discounted valuation.

Pershing outperformed the S&P 500 in 2025, with NAV up 20.9% vs. the index’s 17% return.

Source: CNBC

US jobs rebound in January

[8:46 am] January payrolls surprised to the upside, suggesting the US labour market is stabilising after a weak 2025.

Payrolls rose 130,000 in January vs. 65,000 ests, marking the largest monthly gain in over a year.

Unemployment fell to 4.3% vs. 4.4% ests, while average hourly earnings increased 0.4% MoM vs. 0.3% ests.

Health care led job growth, with construction and professional/business services also adding roles; manufacturing gained for the first time in over a year.

Annual revisions showed job gains in 2025 averaged just 15,000 per month, down from the previously reported 49,000 pace.

Participation rate rose to 62.5%, part-time work for economic reasons dropped, and long-term unemployment fell, signalling improving labour market confidence.

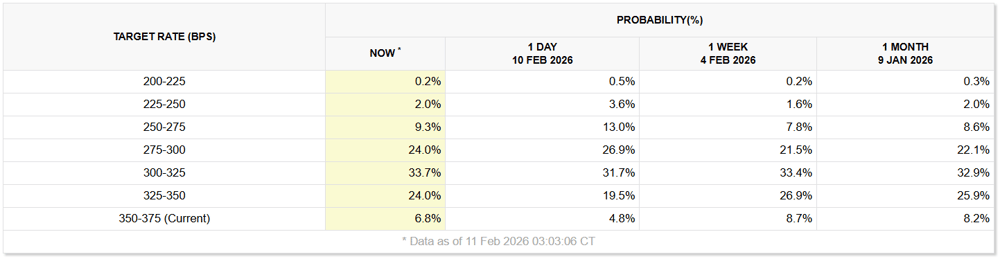

The solid jobs data drove US bond yields slightly higher, while rate cut expectations slipped (e.g. likelihood of three 25 bp rate cuts by year end now 24.0% vs. 26.9% a day ago).

Year-end Fed interest rate expectations | Source: CME Fedwatch Tool

Software stocks continued to tank overnight

[8:43 am] Contrary to many analysts and CEOs that say the software selloff is overdone, the sector sector continued to tumble overnight.

The iShares Expanded Tech-Software ETF dipped 2.5% after a three-day bounce, but still ~4% away from recent lows. Though the largest US-listed software names recorded greater declines, including #1 SAP (-4.5%), #2 Salesforce (-4.3%), #3 Shopify (-7.9%), #4 Uber (-3.3%) and #5 Intuit (-5.1%).

iShares Expanded Tech-Software ETF daily chart (Source: TradingView)

Analysts say software sell-off overdone as AI fears overshoot

[8:39 am] JPMorgan says the collapse in software stocks is pricing in unrealistic near-term AI disruption, creating scope for a tactical rebound as positioning and sentiment reset.

Extreme price action and a “positioning flush” leave risk skewed to a rebound as investors have become overly bearish on AI’s impact on SaaS business models.

Sell-off has been indiscriminate, hitting names with AI partnerships and proprietary data the same as those without, suggesting fear-driven rather than fundamentals-led moves.

Enterprise software remains buffered by high switching costs and multi-year contracts, limiting near-term displacement from new AI tools.

Fourth-quarter reporting across software has been broadly positive, with analysts forecasting 16.8% earnings growth for 2026, inconsistent with current pessimism.

Source: Bloomberg

CME targets first rare earth futures

[8:38 am] CME is planning the world’s first rare earths futures contract to create a hedging market outside China and unlock financing for Western supply chains, according to Reuters.

CME is designing a futures contract for neodymium and praseodymium (NdPr), the key magnet materials used in EV motors, wind turbines and defence systems.

China controls about 90% of processed rare earth material, with NdPr pricing currently set via Chinese exchanges and price agencies, leaving Western projects exposed to volatility.

NdPr prices have rallied about 41% year-to-date after falling roughly 50% in the 15 months to May 2023.

Lack of hedging tools has constrained financing for non-China mines and processors, while a futures market would also let EV and industrial users hedge magnet input costs.

Source: Reuters

Equal-weight S&P 500 at all-time highs

[8:35 am] Very interesting to see the Equal-weight S&P 500 (+0.18%) mark a fourth straight all-time high overnight, outperforming the cap-weighted index by 19 bps. The Equal-weight S&P 500 is now up 5.8% year-to-date, far outperforming the S&P 500 (+0.92%). The US market continues to show signs of a broadening rally, notable resources overnight and more signs of a defensive rotation.

Good morning!

[8:26 am] ASX 200 futures are up 3 pts (+0.03%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks slightly lower, with the S&P 500 (-0.01%), Dow (-0.13%) and Nasdaq (-0.16%) all closing around the midpoint of today's trading range

Breadth was still very solid, with the Equal-weight S&P 500 (+0.18%) closing at a fourth straight all-time high, buoyed by strength in resources and defensives

US nonfarm payrolls increased 130,000 last month, almost double market expectations

The busiest results day yet, with AMP, Breville, Insurance Australia, Origin and more due to report

To catch up on all overnight developments, check out today's Morning Wrap.