ASX 200 Live Today - Monday, 4th May

The S&P/ASX 200 set to slip, S&P 500 and Nasdaq hit record highs overnight while all other sectors struggled. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Monday, May 4. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 lower, back below the 200-day

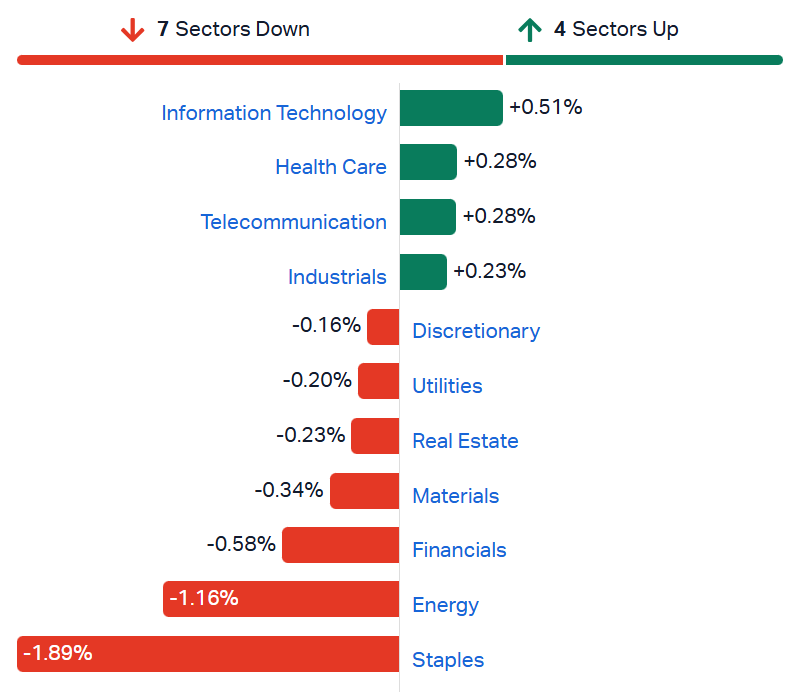

[2:15 pm] ASX 200 on the backfoot again, down 0.45% after a short-lived bounce on Friday. Fairly weak breadth today, with just 82 constituents (41%) higher and just three sectors in green (Tech, Healthcare and Telcos).

Today marks another day where corporate updates weighed on select sectors, including:

Endeavour's (-4.5%) soft Q3 trading update and A2 Milk (-9.6%) product recall weighed on the Staples sector

Accent Group's (-12.9%) 2H26 EBIT guidance downgrade (21% cut at the midpoint) may have provided a downbeat read through for the broader retail sector

NAB (-1.5%) 1H26 result was decent, though factors including competitive pressures, soaring credit impairments, deteriorating asset quality weighed on both the stock and broader banking sector

Energy stocks traded broadly lower, with Brent down ~4% in the last three sessions

While US equities continue to edge higher on the back of strong earnings, the updates we're getting locally aren't telling the same story. Before we wrap here, here are some interesting tidbits I've come across today:

While narrow market breadth can persist for months, it always resolves with a leadership rotation, according to Goldman Sachs. Since 1980, the median episode of narrow market breadth ... has been three months, but with the longest episode in the late 1990s lasting for more than two years. While narrow breadth can resolve via either "catch up" or "catch down," both outcomes are characterised by the underperformance of previous market leaders.

Tracy Shuchart from Ninja Trader says consensus is modeling Hormuz as an oil shock, but it's really an input-layer reset of the global manufacturing economy. Crude is just the loudest signal, while the slow repricing of chemicals, metals, and specialty inputs underneath every physical product is the more consequential transmission. Because each layer moves on its own timeline (oil in days, fertilizer in weeks, specialty chemicals in months, capital goods in quarters, sovereign wealth and reinsurance in years), the impact rolls through in waves rather than a single shock, making it harder to model than a typical commodity event.

The 1973 oil crisis (embargo imposed by Arab members of OPEC) began on 6-Oct-73 and lasted until March 1974. Equity markets experienced an initial selloff when the embargo was declared, but most of the weakness took place around six months after the embargo was lifted.

Stocks making 52-week highs

[1:23 pm] A very narrow list of ASX 200 stocks tagged a fresh 52-week high last week, including lithium (LTR, PLS MIN), companies that upgraded earnings (CDA), nickel (NIC), energy (KAR, ALD) and defensives (AZJ, APA).

Ticker | Company | Close | Sector | 1 Week | 1 Year |

|---|---|---|---|---|---|

Liontown | $2.64 | Materials | 17.9% | 412.6% | |

PLS Group | $6.14 | Materials | 6.4% | 317.7% | |

Mineral Resources | $66.70 | Materials | 12.4% | 227.8% | |

Codan | $43.33 | Technology | 21.6% | 166.3% | |

Predictive Discovery | $0.91 | Materials | -4.7% | 149.3% | |

Tabcorp Holdings | $1.17 | Discretionary | 5.0% | 86.4% | |

Nickel Industries | $1.07 | Materials | 7.0% | 79.0% | |

Karoon Energy | $2.17 | Energy | -3.1% | 52.8% | |

Ampol | $35.82 | Energy | 4.7% | 43.6% | |

Aurizon Holdings | $4.27 | Industrials | 2.2% | 42.3% | |

APA Group | $10.50 | Utilities | 3.8% | 25.6% |

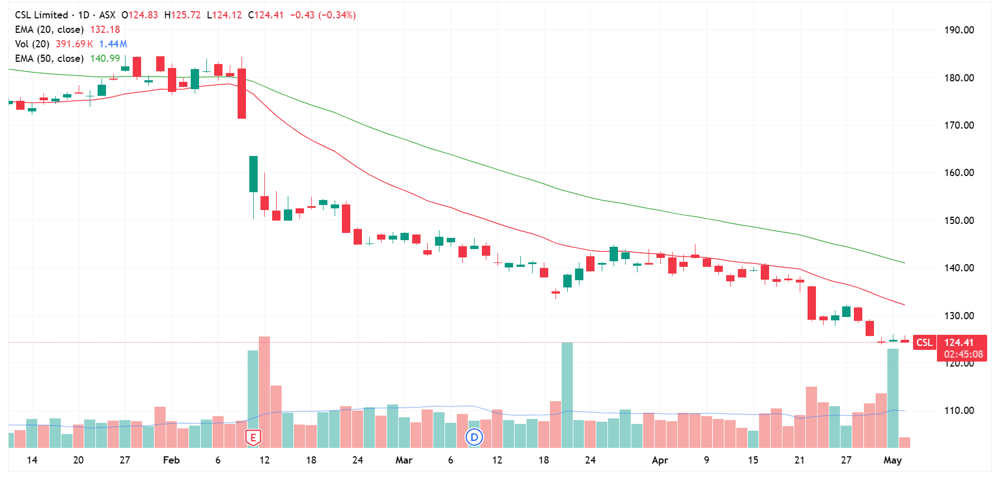

CSL check in: Still grinding lower

[1:22 pm] It's been almost three months since CSL's half-year result (11-Feb), where the stock fell 4.6% to a near eight-year low of $163.44. Fast forward to today, and the stock has fallen a further 24% since the result to trade at its lowest level since March 2017.

CSL daily price chart (Source: TradingView)

Accent Group sold to oblivion

[1:06 pm] If you looked at the price chart, you'd say this is one of those companies headed towards administration.

Shares in Accent Group tumbled 12% today after downgrading its second-half EBIT guidance to $23-28 million from prior expectations of $30-35 million (~21% cut at the midpoint). Management cited:

"The Company advises that trading to the end of March was in line with its prior guidance and expectations. However, following the escalation in geopolitical tensions in late March, which contributed to higher fuel prices and a significant deterioration in consumer confidence, both sales and gross margin were adversely impacted during April. As a result of the changes in macroeconomic conditions, and the Company's expectation that these conditions are unlikely to abate in the short term, the Company has updated its trading outlook for May and June based on recent trade."

The stock is now down 42% year-to-date and down 71% in the last twelve months, trading at record lows.

RBA poised for third straight hike on Tuesday

[12:19 pm] The RBA is set to entrench its hawkish outlier status with a third consecutive rate rise on Tuesday, even as global peers hold steady to assess fallout from the Iran conflict.

Economists overwhelmingly expect the RBA to hike rates to 4.35%, fully unwinding last year's cuts

Q1 inflation held well above the 2-3% target band, driven in part by Middle East fuel supply disruptions, with pass-through now spreading to building products, takeaway food, freight, airfares, plastics, fertilisers, detergents and paints

Domestic data remains solid, with total credit up 8.1% y/y in March (housing investor loans up 9.6%, business credit up ~10%), unemployment near 4.3%, household spending holding up

The March decision was a narrow 5-4 split vote, and CBA's Belinda Allen flags the May call feels "more precarious"

Economist views diverge after tomorrow's decision: CBA expects a prolonged hold, AMP/Barclays/Goldman/Citi see one more hike, Westpac's Luci Ellis sees two more hikes taking the cash rate to a near 18-year high of 4.85%

Source: Bloomberg

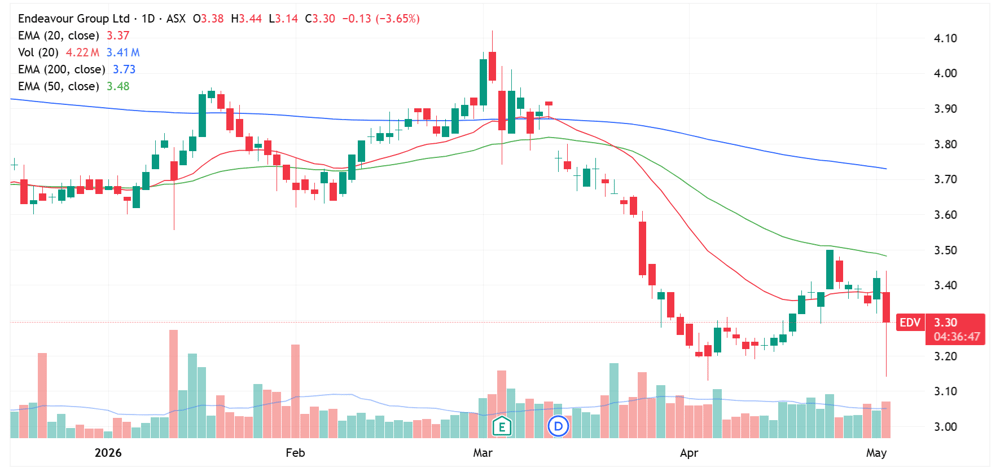

Endeavour back near record lows

[11:26 am] A very volatile morning for Endeavour Group, after the company reported a relatively soft Q3 trading update. The stock opened 1.1% lower, sold off as much as 8.1% to a fresh record low of $3.14 and currently down 4.0% to $3.28.

The key numbers we noted earlier include:

Q3 FY26 sales growth of 2.9% for Retail and 3.7% for Hotels (boosted by Easter timing falling in Q3 this year vs. Q4 in pcp)

FY26 half-to-date sales growth (16-week vs. 16-week, both including Easter and ANZAC Day) of 0.7% for Retail and 3.7% for Hotels as at week 43

Hotels momentum softened in March, with March-April growth of just 1.5% vs. pcp despite a record ANZAC Day, reflecting weakness across food, bar, gaming and accommodation

Retail continues to gain market share in a challenging environment, with strength in Dan Murphy's and BWS over Easter offsetting subdued demand outside key events

Group proactively building up to $400m of additional inventory vs. pcp to buffer against Middle East-related supply disruption, temporarily impacting leverage via short-term debt facilities

Marks a slowdown from the 'first seven weeks of 2H26' update at the Feb half year result, which noted 1.3% sale growth for retail and 4.5% for Hotels.

Endeavour daily price chart (Source: TradingView)

Asia April PMIs: Middle East war drives record cost surges and supply chain strain

[11:24 am] South Korea, Taiwan and Japan all delivered stronger headline manufacturing PMIs in April, but the strength was largely driven by stockpiling activity ahead of further price rises and supply disruption from the Middle East conflict, with cost pressures hitting multi-year or all-time highs.

South Korea:

Headline PMI rose to 53.6 in April from 52.6 in March, the strongest reading since February 2022

Input price inflation and output charge inflation both hit record highs in the 22-year series history, driven by surging raw material prices (particularly oil and fuel), supply shortages and delivery delays

New orders growth at highest since February 2022 and production growth steepest in 20 months, partly reflecting client efforts to build safety stocks

Supplier delivery times deteriorated to the greatest extent since June 2022; stocks of finished goods fell at the fastest pace in 2026 so far

Business confidence slipped to a five-month low on uncertainty over the length of the conflict

Taiwan:

Headline PMI jumped to 55.3 in April from 53.3 in March, the strongest since December 2021 and a fifth consecutive month of expansion

Input costs rose at the steepest pace since May 2021 and one of the fastest on record (22-year series), driven by oil prices and widespread supplier price hikes

Supplier performance deteriorated at the greatest extent since the pandemic, with lead times the longest in just over four years

Business confidence slipped to a three-month low despite optimism around AI-related demand

Japan:

Headline PMI rose to 55.1 in April from 51.6 in March, the strongest reading since January 2022

Production expanded at the fastest pace since February 2014, with new order growth at the quickest since January 2022

Supply chain performance deteriorated at the steepest rate in 15 years (worst since the Tohoku earthquake aftermath in April 2011)

Input cost inflation hit a 3.5-year high (steepest since October 2022) on raw materials, oil and transport, output charge inflation also at the fastest since late 2022

Analysts' take on Qantas

[11:00 am] Qantas announced further capacity reductions last Friday, in response to sustained fuel cost pressure and Middle East supply disruption, redeploying aircraft from domestic to higher-yielding European routes while reaffirming FY earnings guidance.

JPMorgan retained Overweight, target unchanged at $10.30. European routes are becoming a profit centre as Middle East alternatives disappear, with rational domestic competition and medium-term upside from Loyalty and Sunrise strategies.

RBC Capital Markets retained Outperform, lowered target from $10.75 to $10.25. Network settings retain flexibility for further pricing adjustment, with extended Perth-Rome flights generating improved spreads, though earnings revisions are offset by valuation impact from capacity changes.

Analysts' take on Coles

[11:00 am] Coles delivered a Q3 result last Friday that beat expectations on supermarket LFL growth of 3.6%, with disciplined cost management offsetting inflationary pressures and supporting reaffirmed FY earnings guidance, though liquor sales deteriorated sharply (-5% y/y) amid big-box format challenges.

Jarden downgraded to Neutral from Overweight, raised target from $21.60 to $22.60. Ssees consistent food performance and market share gains from Aldi/independents, but moves to the sidelines on valuation with more near-term upside seen in Woolworths.

UBS retained Buy, raised target from $25.00 to $25.50. Supermarket cost savings and value offerings underpin guidance, while liquor faces significant operating deleverage with big-box warehouse wind-down likely.

JPMorgan retained Overweight, raised target from $23.50 to $24.00. Inflation expected to accelerate sales growth to mid-5% from Q2, with stable earnings outlook despite ongoing margin pressure and probable warehouse store closures.

ASX 200 lower on Staples, Banks and Resources

[10:33 am] ASX 200 down 0.46% in early trade after snapping an eight-day losing streak last Friday. Staples notably lower, largely reflecting a ~13% selloff for A2 Milk and 7% dip for Endeavour Group, Energy stocks slip on softening oil prices and Financials weighed by NAB's (-2.7%) 1H26 result.

S&P/ASX 200 sectors (Source: Market Index)

Overall, more weakness despite Friday's bounce, with corporate updates continuing to weigh on the market. Endeavour's Q3 and NAB's 1H26 results were the two notable drivers of today's weakness.

Top ASX 200 gainers

[10:24 am] Life360 is trading sharply higher after US software stocks bounce overnight, Cochlear is on a three-day win streak (but still down 40.5% since its FY26 guidance downgrade on 21-Apr) and a few gold stocks are also catching a bid.

Ticker | Company | % Chg | Price |

|---|---|---|---|

360 | Life360 | 6.15% | $21.23 |

SRL | Sunrise Energy Metals | 3.96% | $12.48 |

COH | Cochlear | 2.31% | $101.05 |

GGP | Greatland Resources | 2.07% | $13.78 |

ALQ | ALS | 2.06% | $21.80 |

GLF | Gemlife Communities Group | 1.94% | $4.74 |

TAH | Tabcorp | 1.72% | $1.19 |

DYL | Deep Yellow | 1.65% | $1.85 |

PDI | Predictive Discovery | 1.65% | $0.93 |

DOW | Downer | 1.62% | $7.54 |

Top ASX 200 losers

[10:24 am] A2 Milk is trading sharply lower after a issuing a product recall for its US-label Platinum infant formula, Endeavour sold off after issuing a weak Q3 update, while a broad mix of resource-related stocks are also under pressure.

Ticker | Company | % Chg | Price |

|---|---|---|---|

A2M | A2 Milk Company | -12.52% | $6.36 |

EDV | Endeavour Group | -6.14% | $3.21 |

LOV | Lovisa | -3.28% | $23.27 |

BOQ | Bank Of Queensland | -2.78% | $6.47 |

ARU | Arafura Rare Earths | -2.78% | $0.35 |

LYC | Lynas Rare Earths | -2.25% | $18.71 |

CSC | Capstone Copper Corp | -2.15% | $11.61 |

LTR | Liontown | -2.08% | $2.59 |

AAI | Alcoa Corporation | -2.05% | $87.78 |

WTC | Wisetech Global | -1.92% | $42.89 |

a2 Milk recalls small volume of US-label a2 Platinum infant formula

[10:12 am] a2 Milk Company has voluntarily recalled three batches of US-label a2 Platinum infant formula due to detection of cereulide, with the recall isolated to a discontinued US product line and no expected impact on financial results.

Recall covers three batches totalling 63,078 tins, with an estimated 16,428 tins sold to consumers

Total US infant formula sales account for ~0.1% of the Company's total sales revenue in 1H26, recall is not expected to impact financial results

Product was manufactured by Synlait Milk and sold only in the US through a2MC's website, Amazon and Meijer stores as part of Operation Fly Formula

Importation rights had already expired on 31 December 2025 and the Product had been discontinued and removed from sale prior to the recall

Recall initiated after cereulide was detected following MPI's 15 April 2026 industry update applied retrospectively to NZ infant formula manufacturers

No confirmed incidents of infant illness or harm reported to the Company

All a2 Platinum product sold outside the US (Australia, NZ, South Korea, Vietnam and cross-border into China) is unaffected as it has a different formulation and relevant ingredient

A2 shares dipped as much as 18.9% this morning, currently down 13.2% to $6.31.

Company page: a2 Milk Company (A2M)

Navigator Global Investments to acquire $195m alternatives portfolio

[10:09 am] NGI is acquiring a portfolio of net revenue share interests in 17 alternative asset managers from Stable for US$195 million (~A$270.4m), funded by a $145 million capital raise

Acquiring net revenue share interests in 17 alternative asset managers from funds managed by and clients of Stable

Funded by a $145m fully underwritten entitlement offer plus $136m of NGI scrip

Entitlement offer priced at 1 for 8.13 at $2.40 per share or a 3.2% discount to last close

All eligible NGI directors intend to participate

Expected to deliver low double-digit EPS accretion and improve key profitability metrics; completion expected in early FY27

FY26 adjusted EBITDA guided to $100m-$104m

Company page: Navigator Global Investments (NGI)

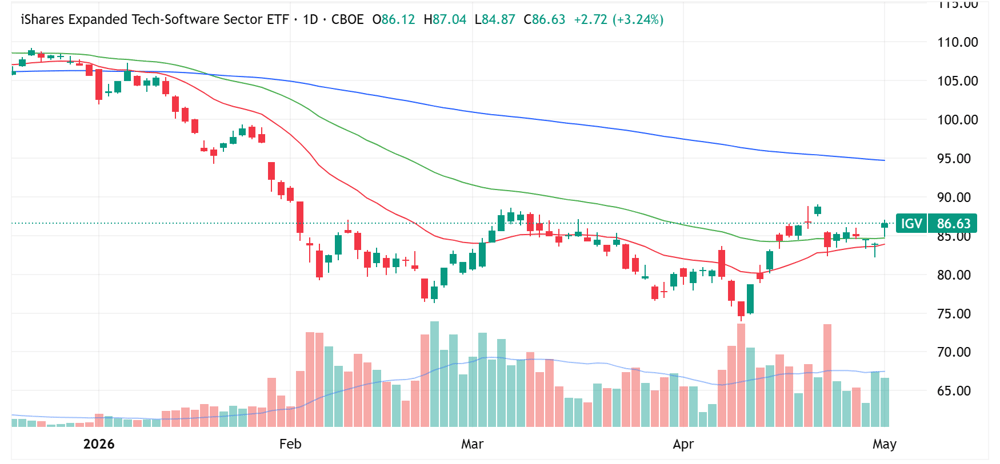

Software stocks bounce

[9:56 am] Local software stocks have a strong lead after the NYSE-listed iShares Expanded-Tech software ETF snapped a three-day losing streak last Friday, up 3.2%. Notable US-listed gainers include Microstrategy (+7.0%), Datadog (+6.3%), Shopify (+5.4%) and Salesforce (+4.1%).

iShares Expanded-Tech Software ETF daily chart (Source: TradingView)

GR Engineering wins $57m Beetaloo O&M contract

[9:50 am] GR Engineering's subsidiary GRPS has secured a five-year operations and maintenance contract for the Sturt Plateau Compression Facility in the Beetaloo Basin, with an option to extend.

Estimated contract value of $57m over five years, with an option to extend by a further three years

Awarded by SPCF Co, an entity owned 50% by Tamboran Resources (TBN) and 50% by Daly Waters Infrastructure, LP

GRPS will be responsible for operation of the facility including regulatory compliance, production performance, maintenance, asset integrity management and HSE compliance

Company page: GR Engineering Services (GNG)

Accent Group cuts H2 EBIT guidance, flags ASIC investigation

[9:31 am] Accent Group has materially downgraded 2H26 EBIT guidance and disclosed an ASIC investigation into trading in its securities.

2H26 EBIT guidance of $23m-$28m, down from prior $30m-$35m (~21% downgrade at the midpoint)

Includes ~$2m of restructuring costs from April to June FY26 as part of a new cost-out program

FY26 EBIT guidance of $79.5m-$84.5m vs. UBS ests of $91.9m (10.7% miss at the midpoint)

Trading update for first 18 weeks of H2: Total owned sales up 7.1% year-on-year but LFL sales down 1%

Continuing business gross margin of 54.2%, down 80 bps year-on-year

ASIC investigation: Company has received notices requiring it to provide reasonable assistance (including production of documents) regarding suspected contraventions of the Corporations Act in relation to trading in its securities between 23 May 2025 and 10 June 2025

Accent guided to 2H26 EBIT of $30-35 million at its 1H26 result on 25 February, which suggests a rather material deterioration in the consumer landscape. The prior guidance assumed flat LFL sales (which is now negative 1% for the first 18 weeks) and flat gross margins (which is currently down 80 bps year-on-year).

Accent shares are down 34% year-to-date and down 67% in the last twelve months.

Company page: Accent Group (AX1)

Viva Energy flags six-week Geelong Refinery RCCU restart

[9:23 am] Viva Energy expects to restart its Residue Catalytic Cracking Unit and associated units during June following the 15 April fire, with production returning to over 90% of capacity.

Repairs to impacted units necessary to restart the RCCU expected to take approximately six weeks, subject to further inspection

Production to increase to over 90% of capacity following the RCCU restart

While the RCCU is offline, the Geelong Refinery is producing diesel and jet fuel at ~80% of capacity and petrol at ~60%

Sufficient fuel stocks held to cover reduced production with normal customer supply expected to be maintained

Company page: Viva Energy Group (VEA)

Chrysos Corporation hits record sample volumes, signs five new leases

[9:21 am] Chrysos delivered back-to-back monthly records of over one million assay samples processed and tracking at the upper end of FY26 guidance.

Processed over one million samples in March 2026 (a new fleet record), followed by a second consecutive month above one million in April

19 new PhotonAssay lease agreements signed YTD, including five since the last update

Two further ALS agreements (sixteen units now within that partnership), with four of the recent ALS deals entering new regions

ALS (ticker ALQ) is one of the world's largest commercial laboratory businesses, with Chrysos signing two more lease agreements with them

FY26 guidance unchanged with revenue tracking at the upper end of $80m-$90m and EBITDA at the upper end of $20m-$27m

Company page: Chrysos Corporation (C79)

Inghams appoints Grant Douglas as new CFO

[9:16 am] Inghams has appointed Grant Douglas as Chief Financial Officer from October 2026, with current CFO Gary Mallett stepping down after seven years.

Douglas joins from Brickworks where he was most recently CFO, having held senior finance roles including a three-year stint as EVP Finance for Brickworks North America

Prior to Brickworks (joined 2011), Douglas spent 14 years in Deloitte's Audit & Assurance practice. He is a Chartered Accountant and GAICD

CEO Ed Alexander said Douglas' track record in listed environments and disciplined capital allocation will be critical as Inghams sharpens focus on earnings quality, consistency and returns

Company page: Inghams Group (ING)

Endeavour Group Q3: Retail growth holds up, Hotels softening

[9:12 am] Endeavour delivered Q3 sales growth across both segments boosted by Easter sales, but underlying momentum is moderating amid cost-of-living pressures, with management flagging Middle East conflict supply chain costs and a new $100 million cost-out program.

Q3 FY26 sales growth of 2.9% for Retail and 3.7% for Hotels (boosted by Easter timing falling in Q3 this year vs. Q4 in pcp)

FY26 half-to-date sales growth (16-week vs. 16-week, both including Easter and ANZAC Day) of 0.7% for Retail and 3.7% for Hotels as at week 43

Hotels momentum softened in March, with March-April growth of just 1.5% vs. pcp despite a record ANZAC Day, reflecting weakness across food, bar, gaming and accommodation

Retail continues to gain market share in a challenging environment, with strength in Dan Murphy's and BWS over Easter offsetting subdued demand outside key events

Group proactively building up to $400m of additional inventory vs. pcp to buffer against Middle East-related supply disruption, temporarily impacting leverage via short-term debt facilities

Additional fuel and freight costs in FY26 estimated at $6-$8m, primarily impacting Retail gross margin

Three-year cost reduction program targeting $100m of savings in FY27 from store cost optimisation, labour efficiencies, centralised administration, procurement and support office headcount

Endeavour reported a challenged 1H26 result on 4 March, which drove the stock 3.5% lower on the day and a further ~16% lower by 7 April. The stock has since bounced ~6.8% from April lows. The 1H26 result noted sales growth for the first seven weeks of 2H26 at 1.3% for retail and 4.5% for hotels, suggesting a slight deceleration compared to half-to-date sales growth.

Company page: Endeavour Group (EDV)

Nuix confirms John Ruthven as permanent CEO

[9:07 am] Nuix has appointed John Ruthven as Chief Executive Officer and Managing Director effective 4 May 2026, transitioning him from the Interim CEO role he has held since November 2025.

Ruthven was appointed Interim CEO on 27 October 2025 for a period of up to 12 months, with effect from 3 November 2025

The Board completed a comprehensive global search before determining Ruthven was the preferred candidate based on his performance, skill set and knowledge of the Company

Chair Robert Mactier said the Board was unanimous in the selection and pointed to Ruthven's strategic and considered approach during the interim period

Ruthven said the past six months had strengthened his conviction in Nuix's purpose, technology differentiation and people as foundations for a growth story

Company page: Nuix (NXL)

NAB 1H26 results

[9:04 am] NAB delivered underlying earnings momentum supported by business banking strength, but a $949 million software capitalisation policy change masked the headline result.

Revenue up 3.1% (ex-Markets & Treasury up 1.8%)

Cash earnings (ex-items) up 2.3% half-on-half to $3.58bn vs. $3.34bn ests (7.1% beat)

Statutory net profit of $2.75bn

Net Interest Margin up 3 bps to 1.81% vs 1.79% ests (2 bp beat)

NIM was stable as deposit replicating portfolio gains and lower deposit costs offset lending competition

Expenses up 26.2% (down 0.5% ex-LNI), with higher personnel and technology costs offset by productivity benefits and lower remediation

Australian business lending up 5.6% with market share gains in SME and total business lending

Forward-looking collective provisions increased $300m, lifting CP/CRWA ratio to 1.35% on Middle East-related uncertainty

1H26 DRP to include a 1.5% discount and be partially underwritten, raising ~$1.8bn and supporting a pro forma CET1 of 12.05% at March 2026

Interim dividend flat year-on-year at 85 cps, in-line with ests

Company page: National Australia Bank (NAB)

Bullish vs. bearish focus points

[8:46 am] Here's snapshot of what's driving markets as Q1 US earnings season wraps up against a backdrop of Middle East tensions and AI capex debates.

Bullish:

Q1 S&P 500 earnings growth rate ended the week at ~27% vs. the 12.6% at the start of earnings season

Big Tech delivered on the AI compute demand narrative with combined 2026 capex of >$700bn across Amazon, Google, Meta and Microsoft, cloud backlog nearly doubling at Google Cloud and up ~50% at AWS, plus cloud margin expansion

AI infrastructure plays rallied on data centre power dynamics, with Caterpillar, Quanta, Carrier, nVent, WESCO, Generac and Trane all posting big gains

Consumer resilience reinforced by Visa (growth across all spend bands, no signs of lower-spend weakening) and Mastercard (healthy spending despite geopolitical risks)

Minimal Middle East impact on earnings with affected companies (raw materials, supply chain, freight) highlighting mitigation measures supporting the pricing power/peak margin theme

Macro data held up: April ISM manufacturing expanded for a fourth straight month, initial claims at decades-low, Q1 final private domestic demand up 2.5%, real PCE up 2.1% year-on-year through March

Favourable May seasonality after the strongest April since November 2020, JPMorgan noted S&P 500 has averaged ~1.5% gains in May with positive returns 90% of the time over the past decade

Bearish

Brent crude still hovering >US$105 a barrel, a four-year high, with the Strait of Hormuz effectively closed and reports Trump told aides to prepare for an extended blockade of Iran

Energy inventory drawdowns intensifying: US exports hit a record 6.44m bpd driving a 6.2m barrel draw, gasoline inventories down for an 11th straight week

AI capex ROI concerns hit Meta (expected revenue deceleration plus $10bn capex guide raise to $125-145bn) and Microsoft ($190bn capex guide) post-results

AI monetisation worries flared on a report OpenAI missed internal weekly user and revenue targets, driving sharp selloffs in SoftBank and Oracle

Travel-leveraged names including Booking, Royal Caribbean and Hilton flagged Middle East headwinds alongside the airline jet fuel hit

Hawkish hold from the Fed with three dissents over the easing bias, Powell flagged complications looking through an energy shock given inflation has been above target for years and the Fed is already looking through tariffs

Technical backdrop weakening as CTAs flipped from buyers ($80bn over the past month, now long $44bn) to small sellers per Goldman, May historically the largest month for equity fund and ETF outflows

Q1 S&P 500 earnings tracking well ahead of expectations

[8:43 am] The latest data from FactSet shows Q1 S&P 500 earnings growth running at more than double the rate expected, with beat rates well-above historical averages.

Blended Q1 EPS growth rate of 27.1% vs. 13.2% expected at the end of the quarter

63% of S&P 500 companies have reported, with 84% beating EPS ests (vs. five year average of 78%)

Aggregate EPS surprise of 20.7% above ests, well ahead of the five-year average of 7.3%

US manufacturing strong but input price pressures intensify

[8:42 am] US April activity expanded at the fastest pace since 2022, but the war with Iran is driving sharp increases in input costs and inflation risk.

April ISM Manufacturing 52.7 vs. 53.2 ests

New orders expanded for a fourth straight month, rising to 54.1 from 53.5

ISM Prices Paid index jumped to 84.6 from 78.3, up 25.6 points over three months and the highest since April 2022

Employment index fell to 46.4 from 48.7, remaining in contraction

Exxon and Chevron beat expectations despite war hedging hits

[8:40 am] Both majors saw profits fall sharply year-on-year despite oil prices surging ~57%, with timing-related hedging losses masking underlying strength.

Exxon 1Q26:

Adjusted EPS of $1.16 vs. $1.00 ests (16% beat)

Revenue up to $85.14bn vs. $82.18bn ests (4% beat)

Net income down 45% to $4.2bn ($1.00 EPS) from $7.7bn ($1.76 EPS) a year ago, hit by a ~$4bn timing effect on hedges plus a $700m hit on closed hedges

Production segment profit down 15% to $5.74bn

CEO Darren Woods said ~15% of Exxon's production is impacted by the war, Middle East output to fall 750,000 bpd in Q2 if the Strait of Hormuz remains closed all quarter

Chevron 1Q26:

Adjusted EPS of $1.41 vs. 95c ests (48% beat, biggest beat since October 2020)

Revenue of $48.61bn vs. $52.1bn ests (7% miss)

Net income down 36% to $2.2bn ($1.11 EPS) from $3.5bn ($2.00 EPS), booked a $2.9bn charge on financial hedges

Production up 15% to ~3.9m bpd; segment profit up 4% to $3.9bn

Spirit Airlines shuts down after bailout collapses

[8:39 am] The pioneering ultra-low-cost carrier became the first major US airline in 25 years to fail, after creditors rejected a Trump administration rescue package.

Spirit ceased operations 3 am ET on 2 May, putting 17,000 workers out of a job (14,000 employees plus contractors)

US eighth-largest carrier with ~9,000 flights and 1.8m seats scheduled in May, representing 2% of domestic US flights

Already in its second bankruptcy (most recent filing August 2025), had reached a creditor deal in February before the 28 February Iran war sent jet fuel prices surging 57%

$500m government bailout proposal collapsed after creditors balked at terms giving the government control of most Spirit shares

Removal of Spirit capacity expected to push fares higher industry-wide, four major carriers (United, American, Delta, Southwest) now control ~80% of US flights

Berkshire Hathaway Q1 26: Cash hoard hits record $397bn

[8:38 am] Greg Abel's first annual meeting as CEO stressed continuity, with Berkshire's cash pile near $400bn signalling a lack of attractive investment opportunities.

Operating earnings up 18% to $11.35bn vs. $11.56bn ests (2% miss)

Net income doubled to $10.1bn

Cash hoard hit a record $397.4bn

Buffett told CNBC he does not see the ideal investing environment, saying "we've never had people in a more gambling mood than now"

Abel said Berkshire will not "do AI for the sake of AI" and ruled out breaking up or divesting subsidiaries, saying "we are a conglomerate but we are an efficient conglomerate"

Abel deflected questions on a single Munger-style adviser, pointing instead to a leadership team including Ajit Jain (insurance), Katie Farmer (BNSF) and Adam Johnson (consumer/NetJets)

OPEC+ lifts June output by 188,000 bpd in first meeting without UAE

[8:35 am] The cartel's seven remaining major producers approved a smaller hike than May as the UAE's 1 May exit reshapes the group.

June production increase of 188,000 bpd vs. May's 206,000 bpd hike (May figure excludes UAE share)

Seven participating countries: Saudi Arabia, Russia, Iraq, Kuwait, Kazakhstan, Algeria and Oman

UAE was OPEC's third-largest producer in February behind Saudi Arabia and Iraq before exiting after nearly six decades

Brent down 1.48% to US$109.21 overnight on Iran peace proposal hopes

Trump weighs Iran proposal as Strait of Hormuz remains closed

[8:34 am] Iran has formally proposed reopening the strait before resolving nuclear talks, but Trump signalled the offer is unlikely to be acceptable.

Iran's 14-point proposal includes US troop withdrawal from surrounding areas, lifting the blockade, releasing frozen assets, compensation and ending the war

Trump said he could restart strikes if Iran "misbehaves" and is not satisfied with the latest proposal

Q1 earnings strength broadens beyond Big Tech

[8:32 am] S&P 500 miss rates are at their lowest since 2021, with strength extending well past the technology sector.

S&P 500 ex-tech posting sharpest positive earnings surprises since Q4 2024, per Seaport Research

Info tech EPS growth ~50% vs. broad index 30%

Russell 2000 up 13% YTD vs. S&P 500 up 5.6%, with small caps benefiting disproportionately from domestic US strength

KBW Bank Index up 10% in April (biggest monthly gain since Nov 2024) as big US banks notched their most profitable quarter ever, though JPMorgan's Dimon warned a credit downturn could be worse than expected

Energy sector tumbled in April despite Exxon and Chevron beating ests (both up >25% YTD)

Consumer discretionary up 12% in April with Amazon +27%, Starbucks +18%, DR Horton +12%

Source: Bloomberg

AI trade divergence in Big Tech earnings

[8:31 am] Investors are sharply differentiating between AI winners and losers despite broadly strong Magnificent Seven results.

Alphabet shares jumped ~10% (up 23% YTD, best in Mag 7) on Google Cloud strength, while Meta tumbled ~8% on capex concerns funded increasingly by debt, creating a $566bn market cap divergence in a single day

Mag 7 (ex-Nvidia) on pace for Q1 earnings growth of 57% vs. 18% ests at start of season, well ahead of the rest of the S&P 500's ~16% growth

Microsoft guided to 2026 capex of $190bn, sending shares down ~4% and making it the worst Mag 7 performer YTD (down 14%)

Apple forecast current quarter revenue growth of up to 17%, well above ests, sending shares up 3.3% Friday

Nvidia down 8.4% over four sessions amid concerns its AI chip dominance is slipping, with Alphabet's TPUs, Amazon's homegrown chips ($20bn+ revenue run rate) and Qualcomm's data centre chips gaining traction

Good morning!

[8:16 am] ASX 200 futures are down 23 pts (-0.26%) as of 8:30 am AEST.

The overnight session in a nutshell:

S&P 500 (+0.29%) and Nasdaq (+0.89%) both closed at all-time highs, largely buoyed by tech stocks including Micron (+4.8%), Apple (+3.3%) and Tesla (+2.4%)

Nine out of eleven S&P 500 sectors finished lower amid weak breadth, US-Iran stalemate

Brent slipped 1.4% but still up 9.3% last week