ASX 200 Live Today - Friday, 8th May

The S&P/ASX 200 is set to tumble as oil prices clawed back losses and US CEOs flag a downbeat outlook for consumers.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Friday, May 8. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 tumbles, flat for the week

[1:00 pm] Closing shop a bit early today (having some data issues, hence none of the usual tables – need to painstakingly move some things around). A very heavy session, with the ASX 200 down 1.65% and now flat for the week. This isn't the kind of move you want to see coming off the recent skid/brief move below the 200-day. Weakness is very broad based, with all sectors red, and Utilities, Financials and Real Estate all down more than 2%. Breadth is unsurprisingly poor, with 150 constituents (75%) trading lower. Asian markets also opened somewhat soft, with the Hang Send down 1.26%, KOSPI down 1.06% but Nikkei up 0.44%. Brent is currently down 2.3% to US$100.94 a barrel and down ~7.7% week-to-date. The ASX 200 now marginally above the 200-day moving average, at a time where it looks increasingly fragile (from both a technical perspective, and the recent avalanche of downbeat corporate updates).

Chinese lithium futures edge higher

[11:26 am] A relatively weak day for local lithium stocks, though Chinese lithium futures are up 1.43% to 200,000 yuan a tonne, the highest since August 2023.

IGO (+1.4%) and MinRes (+0.1%) at the only two major names in positive territory, while PLS (-0.4%), Liontown (-1.0%) trade slightly lower.

Macquarie trading lower despite strong FY26 beat

[11:00 am] A very choppy morning for Macquarie, despite its FY26 result broadly beating market expectations.

Open: +0.96% ($244.20)

Session high: +3.15% ($249.49)

Session low: -3.3% ($233.84%)

Now: -0.98% ($239.50)

The key numbers from the result include:

Net profit up 30% to $4.85bn vs $4.42bn ests (10% beat)

EPS up 30% to $12.77 vs $11.60 ests (10% beat)

Full year dividend of $7.00 per share vs $7.32 ests (4% miss)

On-market share buyback concluded with $1.01bn acquired at an average $189.80, with no further purchases expected

While asset disposals drive substantial one-off gains, the company's underlying performance was also strong across its commodities, asset management and capital markets divisions. The dividend fell short of market expectations, which may imply some degree of capital preservation for strategic investments.

Top ASX 200 gainers

[10:30 am] Trading updates from Block and REA Group driving shares notably higher, while software stocks like TechnologyOne, Xero and Life360 also eking out some gains.

Top ASX 200 losers

[10:30 am] Tabcorp continues to tumble after yesterday's AUSTRAC investigation announcement, while uranium, defence and building/construction stocks also under pressure.

Ticker | Company | % Chg | Price |

|---|---|---|---|

Tabcorp Holdings | -7.96% | $0.81 | |

Mesoblast | -3.83% | $2.01 | |

Electro Optic Systems | -3.67% | $9.19 | |

Westpac | -3.56% | $37.94 | |

Nexgen Energy | -3.45% | $17.05 | |

Paladin Energy | -3.36% | $12.51 | |

Droneshield | -3.32% | $3.64 | |

James Hardie Industries | -3.16% | $28.16 | |

NRW Holdings | -2.80% | $6.94 | |

Guzman Y Gomez | -2.75% | $18.07 |

ASX 200 gives back gains

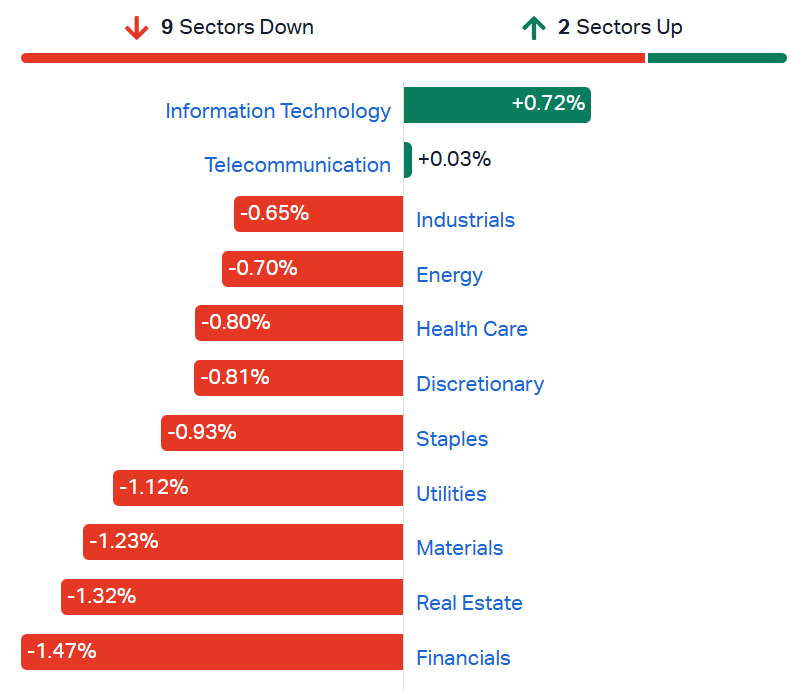

[10:13 am] ASX 200 down 1.26% in early trade, cancelling out Thursday's gains. Though the index is still up ~0.9% in the last three sessions. Rather heavy declines across the board, with Utilities, Materials, Real Estate and Financials sectors all down more than 1%.

S&P/ASX 200 sectors (Source: Market Index)

SKS Technologies wins $22m retail HQ contract, tender pipeline more than doubles

[9:33 am] SKS Technologies has secured a $22 million contract from Buildcorp to deliver an integrated electrical technology solution for a major retailer's new Melbourne Docklands headquarters, with the broader tender pipeline showing strong momentum.

The company also noted:

Order book now sits at $355m total, with ~$270m of work extending beyond the traditional 12-month horizon into 2H27

Tender pipeline up almost 120% since February 2026, from $572.3m to $1.25bn

Data centre tenders make up just over $1bn of the total pipeline, up from $423.6m in February

SKS might be one of the strongest trending stocks out there, up 76% in the past month, 87% year-to-date and 313% in the last twelve months.

Company page: SKS Technologies Group (SKS)

QBE reaffirms FY26 outlook with solid Q1 trading update

[9:31 am] QBE has reiterated its FY26 guidance after a solid first quarter, with premium growth ahead of medium-term targets and catastrophe costs running well below allowance.

1Q26 GWP growth of 11% year-on-year (7% constant currency)

Group premium rate increases of ~2% in-line with expectations

Net cost of catastrophe claims of ~$300m for the four months to April, well below the $517m 1H26 catastrophe allowance, despite multiple Australian events and Northern Hemisphere storms

Direct underwriting impact from Middle East conflict not material to date at ~$60m in net claims

Investment income of ~$500m in the four months to April, with core fixed income yield up to 4.1% from 3.7% at FY25

FY26 guidance reiterated: Mid-single-digit GWP growth (constant currency) and combined operating ratio of ~92.5%

Company page: QBE Insurance (QBE)

Macquarie FY26 profit beats with record second half

[9:29 am] Macquarie delivered a 30% lift in FY26 profit driven by a record second half, with all four operating groups posting double-digit growth and CGM benefiting from a meter business divestment.

Net profit up 30% to $4.85bn vs $4.42bn ests (10% beat)

2H26 net profit soared 93% half-on-half to $3.19bn

EPS up 30% to $12.77 vs $11.60 ests (10% beat)

Full year dividend of $7.00 per share vs $7.32 ests (4% miss)

Commodities and Global Markets contribution up 49% to $4.22bn driven by gain on sale of OnStream meters platform and higher commodities risk management income

Macquarie Capital up 43% to $1.49bn

Macquarie Asset Management up 27% to $2.60bn on higher performance fees

Banking and Financial Services up 17% to $1.61bn

On-market share buyback concluded with $1.01bn acquired at an average $189.80, with no further purchases expected

Company page: Macquarie Group (MQG)

Perseus Mining appoints Wade Bickley as COO

[9:21 am] Perseus Mining has appointed Wade Bickley as Chief Operating Officer effective 1 June 2026, joining from Appian Capital Base Metals where he held the same role. Bickley brings over 25 years of industry experience across gold and base metals operations in Australia, West Africa and Southern Africa.

Appointment comes as Perseus ramps up underground operations at Yaouré and progresses Nyanzaga toward production, described by management as one of Africa's most significant new gold development projects

Company page: Perseus Mining (PRU)

REA Group Q3 misses on revenue and EBITDA, but lowers cost guidance

[9:20 am] REA Group's Q3 result came in below market expectations on revenue and EBITDA, though strong April listings, lowered cost guidance and double-digit residential revenue growth painted a more constructive outlook.

Revenue up 6% to $398m vs $411.6m ests (3% miss)

Operating EBITDA (ex-associates) up 11% to $220m vs $231.0m ests (5% miss)

Operating expenses up 1% to $178m

Residential revenue up 12%, driven by Buy yield growth of 14% and national Buy listing volumes returning to growth at +1%

April listing volumes up 19% YoY (Melbourne +20%, Sydney +25%) reflecting easier comparables

FY26 guidance: Operating cost growth lowered to low to mid single-digit for the group and mid to high single-digit for Australia, positive operating jaws expected, residential Buy yield growth of ~13% maintained, along with the 1-3% decline in national residential Buy listing volumes

Q3 was a little weak but FY26 guidance reaffirmed on all fronts (plus lowered cost growth guidance).

REA been trading pretty much sideways since its 1H26 result on 6 February. On this day, the stock closed 7.8% lower after opening down as much as 17%.

Company page: REA Group (REA)

News Corp Q3 beats on Dow Jones, REA Group strength

[9:13 am] News Corp delivered a Q3 beat across revenue, EBITDA and EPS, with Digital Real Estate Services, Dow Jones and Book Publishing all driving growth, alongside management flagging recent AI content licensing deals. NYSE-listed shares up 1.0% in after hours.

Revenue up 9% to $2.19bn vs $2.11bn ests (4% beat), including an $88m positive FX impact

Adj EPS of $0.21 vs $0.19 ests (11% beat)

Dow Jones revenue up 8% to $619m, with Risk & Compliance up 19%, Dow Jones Energy up 12% and digital advertising up 13%

REA Group revenue up 20% to $325m on FX tailwinds and continued strong Australian residential performance

Move (Realtor.com) revenue up 10% to $148m

Book Publishing revenue up 8% to $555m

CEO flagged recent Meta AI content deal complementing the existing OpenAI partnership, with further deals in discussion expected to lift revenue and profitability

Company page: News Corporation (NWS)

Block beats Q1, raises full year guidance on AI-driven productivity gains

[9:09 am] Block delivered Q1 beats across the board and lifted its FY26 outlook, with management highlighting AI tools driving significant productivity and quality improvements internally. NYSE-listed Block shares are up 8.0% after hours.

Revenue up to $6.06bn vs $6.04bn ests (in line)

Adj EPS of $0.85 vs $0.68 ests (25% beat)

Gross profit up 27% to $2.91bn vs $2.80bn ests (4% beat)

Square GPV up 13% year-on-year, with US GPV up 8.2% and international up 35%

Cash App Consumer Lending origination volume up 82%, with Borrow originations up 175%

FY26 guidance upgraded:

Gross profit of $12.33bn vs. $12.22bn ests and prior $12.20bn

Adj operating income of $3.34bn (27% margin, up 60% YoY) vs $3.26bn ests

Adj EPS of $3.85 (up 62% YoY) vs $3.67 ests and prior $3.66

AI commentary: Production code changes per engineer up over 2.5x since January, incident rates down over 70% YoY, with Builderbot now autonomously executing 15% of production code changes

NY Fed survey shows consumer inflation expectations tick higher

[9:03 am] The April NY Fed Survey of Consumer Expectations showed near-term inflation expectations rising while longer-term views held steady, with labour market sentiment largely stable.

Year-ahead inflation expectations rose to 3.6% from 3.4% in March, while 3-year and 5-year expectations were unchanged at 3.1% and 3.0% respectively

Median year-ahead gas price growth expectations dropped sharply to 5.1% from 9.4% (which had been the highest since March 2022 amid Iran war energy disruptions)

Year-ahead earnings growth expectations rose to 2.7% from 2.4%; mean unemployment expectations ticked up to 43.9% from 43.5% (highest since April 2025)

Perceived probability of losing one's job over the next year edged up to 14.6% from 14.4%, while probability of finding a job if unemployed rose marginally to 46.0% from 45.9%

China consumer spending picks up over Labor Day

[9:00 am] Chinese consumer spending accelerated over the Labor Day holiday, though economists warn it's not enough to signal a genuine turnaround given softer underlying activity.

Consumer sales up 14.3% YoY over the five-day break based on VAT invoices, slightly faster than the 13.7% gain over Lunar New Year

March retail sales up just 1.7%, the latest in a string of sub-2% readings, with government scaling back consumer goods trade-in subsidies this year

Inter-regional trips up just 3.5% over the break, well below the 4.3% Lunar New Year gain and less than half last year's rate

Bloomberg Economics notes broader high-frequency April data showed weak activity, with oil shocks from Iran war weighing on production

Source: Bloomberg

US strikes Iranian ports as Hormuz tensions escalate

[8:58 am] US forces struck Iran's Qeshm Port, Bandar Abbas and a naval checkpoint after Iranian attacks on US warships, though officials insist the ceasefire remains intact.

US Central Command confirmed self-defense strikes after Iran launched missiles, drones and small boats at USS Truxtun, USS Rafael Peralta and USS Mason transiting the Strait of Hormuz

Strikes targeted missile/drone launch sites, command and control locations, and ISR nodes

CENTCOM said it "does not seek escalation"

Trump says the ceasefire remains in effect, with Washington still awaiting Iran's response to its proposal to reopen Hormuz

Comes two days after Iran fired 15 ballistic and cruise missiles at the UAE's Fujairah Port, sparking anger among Gulf countries

McDonald's beats but flags worsening low-income consumer pressure

[8:57 am] McDonald's beat Q1 expectations on stronger US ticket spending, though management warned the consumer environment may be getting worse as gas prices weigh on low-income diners.

Revenue up 9% to $6.52bn vs $6.47bn ests (1% beat)

Adj EPS of $2.83 vs $2.74 ests (3% beat)

Global same-store sales up 3.8% vs 3.7% ests, with US comps up 3.9% driven by higher average check

CEO flagged elevated gas prices from Iran war disproportionately hitting low-income consumers, with the environment "certainly not improving and may be getting a little bit worse"

Q2 expected to decelerate as company laps tough Minecraft tie-in comparison; considering selling weaker-margin company-owned US restaurants (less than 5% of US footprint) to franchisees

Whirlpool CEO warns of "recession-level industry decline"

[8:55 am] The consumer resilience theme was under pressure today, with several companies flagging inflation headwinds and trade downs. Whirlpool CEO Marc Bitzer warned of a "recession-level" industry decline in North America, with consumer demand falling to levels not seen since the 2008 financial crisis.

Here are some of the key quotes from the earnings call.

"Consumer sentiment has dropped to its lowest level in 50 years. The consumer sentiment was already on a very low level by any historical standard, the war in Iran amplified consumer concerns about the cost of living."

"While our view is that consumer sentiment is unsustainably low and should rebound from here, these events clearly pressured our industry and particularly discretionary demand."

"The US appliance industry demand declined 7.4% in the first quarter, with March being down 10%. This level of industry decline is similar to what we have observed during the global financial crisis and even higher than during other recessionary periods."

"Keep in mind that we’re operating in an environment where duress replacement demand drives more than 60% of the industry, and this part of the demand is relatively stable. This gives you a sense about how dramatic the impact on discretionary demand was."

Whirlpool slashes guidance, suspends dividend as Iran war hits demand

[8:50 am] Whirlpool cut its full-year EPS outlook by roughly half and suspended its dividend after the Iran war triggered a recession-level collapse in US appliance demand. The stock fell 11.9%, now down 42% year-to-date and trading at the lowest since December 2011

Revenue down 9.6% to $3.27bn vs $3.51bn ests (7% miss)

Adj EPS of ($0.56) vs $0.62 ests

Ongoing EBIT margin of 1.3%, down 4.6 pts year-on-year

MDA North America sales down 7.5% to $2.24bn, with segment EBIT collapsing 96% to $6m from $149m

FY26 adj EPS guided to $3.00-$3.50 vs. $4.73 ests (31% miss) and prior outlook of ~$6.23

Dividend suspended to prioritise paying down over $900m in debt

April list price hike of 10% with further 4% hike scheduled for July, plus $150m+ in structural cost reductions

Source: Yahoo Finance

Shake Shack tumbles 28% as Q1 revenue misses on beef costs and weather

[8:48 am] Not a high-profile name but certainly an interesting read through for the consumer and retail complex. Shake Shack shares posted its biggest decline on record after Q1 revenue missed on rising beef costs and weather disruptions, with management holding prices steady despite cost pressures.

Revenue up 14.3% to $366.7m vs $370.8m ests (1% miss)

Adj EPS of zero vs $0.12 ests

Same-Shack sales up 4.6%, roughly in line with expectations

Adjusted EBITDA down 9.3% to $37.0m, with company lowering bottom end of FY EBITDA guidance while maintaining revenue outlook

Beef costs climbed "low-teens percentages" but no price increases were passed on, with marketing and tech expenses also weighing on profits

Source: Bloomberg

Oil price volatility to continue amid Iran uncertainty says Citi

[8:47 am] Citigroup's commodities head says oil prices will keep swinging wildly until clarity emerges on a US-Iran deal.

Brent has swung from as high as US$115.30 to US$96 a barrel this week as traders weigh peace prospects against renewed hostilities

Citi's Max Layton says Iran's regime "can last under blockade for years," not just months, suggesting prolonged supply risk

Physical crude market has a "decent buffer" of ~700-800m barrels built up over the prior 12 months, though being eaten through aggressively

Citi last month raised its baseline Brent forecast by US$15 to US$110 and pushed back its base case for Hormuz reopening to end of May

Loading delays at a key Omani terminal in April have upended schedules and may delay deliveries to buyers already starved of Middle Eastern supply

Source: Bloomberg

US equities lower as semis pull back and Iran tensions resurface

[8:45 am] US stocks ended Thursday off worst levels, with a sharp reversal in risk appetite driven by a semiconductor pullback and renewed geopolitical concerns.

S&P 500 down 0.4% with 9 of 11 sectors declining (led by Materials and Energy), Nasdaq 100 down 0.1%, reversing back-to-back record closes

Semis/memory under pressure following a big run amid froth concerns, while software was a rotational beneficiary supported by well received earnings from Fortinet (+18%) and Datadog (+31.3%)

Q1 earnings season tracking strong with ~85% of S&P 500 reported, blended growth rate just under 28%, beat rate just under 85%, and earnings positively surprising by ~19%

Iran risks perked back up late afternoon on claims UAE jets bombed Iranian targets and reports of exchange of fire in Strait of Hormuz, with Iran reportedly able to withstand a Hormuz blockade for months

Trump's 10% global tariffs declared unlawful by a federal trade court, adding another setback to the administration's economic agenda

Good morning!

[8:32 am] ASX 200 futures are down 152 pts (-1.73%) as of 8:30 am AEST.

The overnight session in a nutshell:

Major US benchmarks finished lower as US strikes on Iranian ports and military sites late session unsettled risk sentiment, pulling indexes off intraday record highs

Rough session for AI/speculative growth and memory names with semiconductors finally taking a breather after a weeks-long rally

Whirlpool CEO flagged "recession-level" industry decline from the Iran war and slashed FY26 EPS guidance roughly in half, while Shake Shack plunged 29% on a Q1 miss, highlighting growing strain on the US consumer