Markets at Midday: ASX 200 eyes four-day losing streak, Tech stocks pull back, Energy and Utilities higher

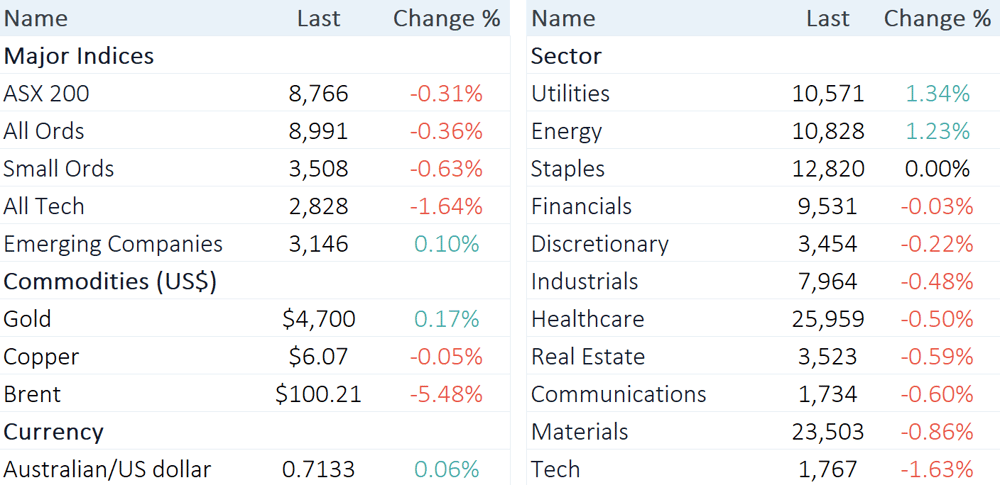

The S&P/ASX 200 continues to struggle, with only Energy and defensive sectors like Utilities and Staples trading higher today.

Source: Market Index

The S&P/ASX 200 is trading 25 pts lower, down 0.29% at noon.

Another heavy session for markets, with mainly defensives and energy stocks trading somewhat higher. We're now on a four-day skid, and fast approaching the key 200-day moving average. Tech stocks are pulling back after a strong run up, Materials are on the backfoot after a relatively soft overnight session for commodity prices, and sectors like Discretionary and Real Estate eye a three-day losing streak after some recent relief.

Let’s dive in

Midday market summary

Today’s big story: Quarterlies galore

A lot of quarterly results today, here are a few key takeaways:

Judo Capital: Reaffirmed its FY26 PBT guidance, but expects numbers to land at the lower end of $180-190m (which still implies ~40% year-on-year growth). They bulked up their cost of risk guidance to 70-75 bps of loans, from 60-65 bps, reflecting anticipated headwinds for customers in fuel-sensitive industries. Judo now joins NAB and Westpac in bumping up provisions.

Fortescue: Total Q3 iron ore production was up 7% year-on-year but down 3% quarter-on-quarter to 59.5 million tonnes. The main detractor from an otherwise solid result was Iron Bridge, where production was lowered to 9-10Mt (from 10-12Mt) due to cyclone-related disruptions. The market was also iffy about an approved US$680 million investment in green energy infrastructure. Fortescue shares are currently down 3.6%.

PLS Group: It was record setting quarter, with production up 12% quarter-on-quarter to 232.4kdmt, which also beat market expectations by 6%. PLS flexed its lithium leverage, as average realised prices surged 61% to US$1,867 a tonne, driving revenue 52% higher. PLS also stressed that diesel is a "small component" of the operating cost base under normal circumstances, representing 4-5% of total production cash costs in the March quarter

Sector moves: Tech on the backfoot

The S&P/ASX 200 Tech Index is down 1.6%, a second day of softness after a ~16% rally between 13-22 April. Today's weakness follows a 5.8% dip in the US-listed iShares Expanded Tech-Software ETF overnight. This ETF is widely used as a barometer for software stocks.

Two high-profile US tech stocks reported earnings overnight, with ServiceNow and IBM both broadly beating consensus expectations. The price action was volatile, with IBM down 8.2% (but off session lows of -11.9%) and ServiceNow down 17.7%.

The big question: Is this just a pullback after a strong run or are we headed back towards another round of "SaaScopolyse"?

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

OCL | Objective Corporation | -5.0% | $11.60 | -22.0% |

360 | Life360 | -4.7% | $20.74 | 2.6% |

BVS | Bravura Solutions | -4.5% | $2.11 | -7.5% |

TNE | Technology One | -3.5% | $28.73 | 0.6% |

DDR | Dicker Data | -3.1% | $8.92 | 5.1% |

WTC | Wisetech Global | -2.2% | $43.43 | -48.9% |

PME | Pro Medicus | -2.1% | $138.59 | -33.7% |

IRE | Iress | -2.1% | $6.93 | -11.7% |

SDR | Siteminder | -1.8% | $3.05 | -23.1% |

HSN | Hansen Technologies | -1.7% | $4.97 | 0.3% |

PPS | Praemium | -1.4% | $0.72 | -5.9% |

MAQ | Macquarie Technology Group | -1.4% | $70.68 | 24.0% |

XRO | Xero | -1.3% | $80.19 | -49.4% |

CAT | Catapult Sports | -1.2% | $3.19 | -18.2% |

AD8 | Audinate Group | -1.1% | $2.60 | -57.4% |

MP1 | Megaport | -0.9% | $8.74 | -16.9% |

CDA | Codan | -0.5% | $35.82 | 133.7% |

NXT | NextDC | 0.3% | $14.80 | 34.9% |

ELS | Elsight | 3.3% | $6.90 | 1603.7% |

WBT | Weebit Nano | 4.2% | $4.44 | 165.9% |

DGT | Digico Infrastructure REIT | 4.4% | $2.26 | -12.6% |

DTL | Data#3 | 4.7% | $7.93 | 7.2% |

Must read announcements

Fortescue (FMG): Q3 beats on shipments and costs, Iron Bridge guidance trimmed

Iress (IRE): Guides FY26 revenue to bottom of range on macro caution

Judo Capital (JDO): Q3 flags PBT at lower end, lifts credit risk guidance

Newmont (NEM): Q1 delivers record free cash flow on surging gold price

Pilbara Minerals (PLS): Q3 production beats on record quarter, guidance reaffirmed

Capital raisings

Australian Oil Company (AOK): $2m capital raising for Surat Basin exploration

Basin Energy (BSN): Strategic investors lead financing to advance exploration

NextDC (NXT): $750m wholesale notes successfully priced

Strata Minerals (SMX): Capital raise update

Temas Resources (TIO): closes $1.5m private placement

Thinking out loud: PMIs point to inflation

S&P Global has released PMIs for most major economies in the past two days. While manufacturing and services activity was generally positive, output prices are rising at multi-year highs. This is not a good look for near-term CPI data.

US: Average prices charged for goods and services rose in April at the fastest rate since July 2022 ... service sector selling price inflation also accelerated to reach a 45-month high.

UK: Input cost inflation continued to accelerate sharply and was the highest since November 2022. This was led by a rapid increase in raw material prices in the manufacturing sector. Service providers also experienced a surge in cost pressures, largely due to higher fuel prices.

Eurozone: Input costs increased at the fastest pace since the end of 2022. Rates of cost inflation quickened across both goods and services, but manufacturers registered the sharper rise. In turn, output price inflation hit a 37-month high. Selling prices increased particularly sharply in Germany, but stronger inflation was also seen in France and across the rest of the single currency bloc as a whole.

Australia: Cost inflation accelerated for a third consecutive month to its highest since August 2022, driven by fuel and shipping costs. Charge inflation hit a 3.5-year high as firms passed costs through

Japan: Input cost inflation hit its sharpest rate since January 2023, driven by staff, raw materials, fuel and energy costs linked to the Middle East and a weak yen. Output charge inflation hit a record high in data going back to late 2007.

Intraday winners and losers

The below tables observe the S&P/ASX 200 stocks with the largest increase/decrease from today's open price.

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

ELV | Elevra Lithium | 12.12% | $12.17 |

XRO | Xero | 3.43% | $79.86 |

ZIP | Zip Co | 2.86% | $2.52 |

PME | Pro Medicus | 2.64% | $138.48 |

COH | Cochlear | 2.15% | $98.34 |

DRO | Droneshield | 2.05% | $3.73 |

EDV | Endeavour Group | 1.92% | $3.46 |

IMD | Imdex | 1.75% | $4.07 |

ALD | Ampol | 1.58% | $34.13 |

ALQ | ALS | 1.55% | $21.24 |

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

EVT | EVT | -8.47% | $12.54 |

4DX | 4DMedical | -4.42% | $4.97 |

REG | Regis Healthcare | -4.14% | $6.71 |

SDF | Steadfast Group | -3.88% | $4.21 |

HUB | Hub24 | -3.87% | $82.53 |

ALK | Alkane Resources | -3.86% | $1.62 |

NWL | Netwealth Group | -3.80% | $24.18 |

FMG | Fortescue | -3.53% | $20.20 |

APE | Eagers Automotive | -3.20% | $23.27 |

VAU | Vault Minerals | -3.04% | $4.79 |

Broker moves

Bank of Queensland (BOQ)

Upgraded to accumulate from hold at Morgans; Price Target: $7.39

Cobre (CBE)

Initiated at speculative buy at Canaccord Genuity; Price Target: $0.25

Data3 (DTL)

Upgraded to buy from outperform at Taylor Collison; Price Target: $8.50 from $7.00

Elevra Lithium (ELV)

Retained at buy at Canaccord Genuity; Price Target: $16.50

Insurance Australia Group (IAG)

Retained at outperform at Macquarie; Price Target: $9.00

Mirvac Group (MGR)

Retained at hold at CLSA; Price Target: $1.80 from $2.13

Retained at overweight at Jarden; Price Target: $2.24

Medibank Private (MPL)

Retained at neutral at Macquarie; Price Target: $4.80

NIB Holdings (NHF)

Retained at underperform at Macquarie; Price Target: $6.10

News Corporation (NWS)

Downgraded to overweight from buy at Jarden; Price Target: $46.30 from $46.80

Perseus Mining (PRU)

Retained at overweight at Barrenjoey; Price Target: $6.85 from $6.70

Retained at buy at Canaccord Genuity; Price Target: $8.80

Retained at buy at Euroz Hartleys; Price Target: $6.85 from $6.60

Retained at overweight at JPMorgan; Price Target: $7.40

Retained at outperform at Macquarie; Price Target: $6.50

QBE Insurance Group (QBE)

Retained at neutral at Macquarie; Price Target: $25.10

Reece (REH)

Downgraded to hold from accumulate at Morgans; Price Target: $14.10 from $17.70

Regis Resources (RRL)

Upgraded to buy from hold at Argonaut Securities; Price Target: $10.50 from $8.30

Retained at buy at Canaccord Genuity; Price Target: $8.70 from $8.85

Retained at neutral at JPMorgan; Price Target: $7.00

Retained at outperform at RBC Capital Markets; Price Target: $11.10 from $11.00

Reliance Worldwide Corporation (RWC)

Upgraded to overweight from neutral at JPMorgan; Price Target: $3.65 from $3.75

South32 (S32)

Retained at buy at Jefferies; Price Target: $5.25 from $5.20

Retained at overweight at JPMorgan; Price Target: $5.10 from $5.00

Retained at outperform at RBC Capital Markets; Price Target: $4.70

Steadfast Group (SDF)

Retained at outperform at Macquarie; Price Target: $4.80

Sandfire Resources (SFR)

Downgraded to hold from buy at Argonaut Securities; Price Target: $18.50 from $19.00

Retained at overweight at JPMorgan; Price Target: $19.70 from $19.40

Upgraded to accumulate from hold at Morgans; Price Target: $20.40

Stockland (SGP)

Downgraded to neutral from buy at Bank of America; Price Target: $4.40 from $6.50

Santos (STO)

Retained at outperform at CLSA; Price Target: $10.40 from $10.30

Retained at overweight at Jarden; Price Target: $8.80 from $8.85

Retained at accumulate at Ord Minnett; Price Target: $7.90

Retained at outperform at RBC Capital Markets; Price Target: $8.50

Retained at buy at UBS; Price Target: $8.80 from $8.70

Suncorp Group (SUN)

Retained at outperform at Macquarie; Price Target: $18.70

Markets at Midday is in a pilot phase –