News | Market Wraps

Evening Wrap: ASX 200 notches gain as uranium and critical minerals stocks boom on separate bullish developments

The S&P/ASX 200 closed 12.2 points higher, up 0.15%.

Mentioned

The S&P/ASX 200 closed 12.2 points higher, up 0.15%.

Uranium and rare earths got a major rocket under them today - with several stocks enjoying double-digit percentage gains 🚀.

For uranium, it was media reports that the White House will tonight be announcing an executive order aimed at accelerating nuclear reactor deployment. For rare earths and critical minerals stocks, it was likely an ultra bullish report from major broker Morgan Stanley.

These moves capped an otherwise quiet end to the trading week for the Aussie stock market, but one that could be pivotal in the context of the current rally - more on that in tonight's ChartWatch!

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key upcoming economic data in tonight's Evening Wrap.

Let's dive in!

Today in Review

Fri 23 May 25, 5:05pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,360.9 | +0.15% |

| All Ords | 8,586.7 | +0.18% |

| Small Ords | 3,188.2 | +0.42% |

| All Tech | 3,913.1 | +0.90% |

| Emerging Companies | 2,262.9 | +0.42% |

Currency | ||

| AUD/USD | 0.6412 | 0.00% |

US Futures | ||

| S&P 500 | 5,849.5 | -0.12% |

| Dow Jones | 41,896.0 | -0.07% |

| Nasdaq | 21,132.0 | -0.22% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Information Technology | 2,773.2 | +1.13% |

| Energy | 7,755.6 | +1.05% |

| Real Estate | 3,855.8 | +0.76% |

| Communication Services | 1,824.7 | +0.75% |

| Financials | 9,007.9 | +0.50% |

| Health Care | 41,779.8 | +0.05% |

| Consumer Staples | 12,422.5 | -0.22% |

| Consumer Discretionary | 4,045.6 | -0.24% |

| Industrials | 8,217.2 | -0.26% |

| Materials | 16,402.1 | -0.65% |

| Utilities | 9,326.0 | -0.97% |

Markets

%20intraday%20chart%2023%20May%202025.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 12.2 points higher at 8,360.9, roughly at its mid-point for the third-straight day running – 0.26% from its session low and 0.24% from its high. At least the market breadth improved today and avoided a third-straight session of 2:1 decliners to advancers, today it was 166 up versus 108 down in the broader-based S&P/ASX 300 (XKO).

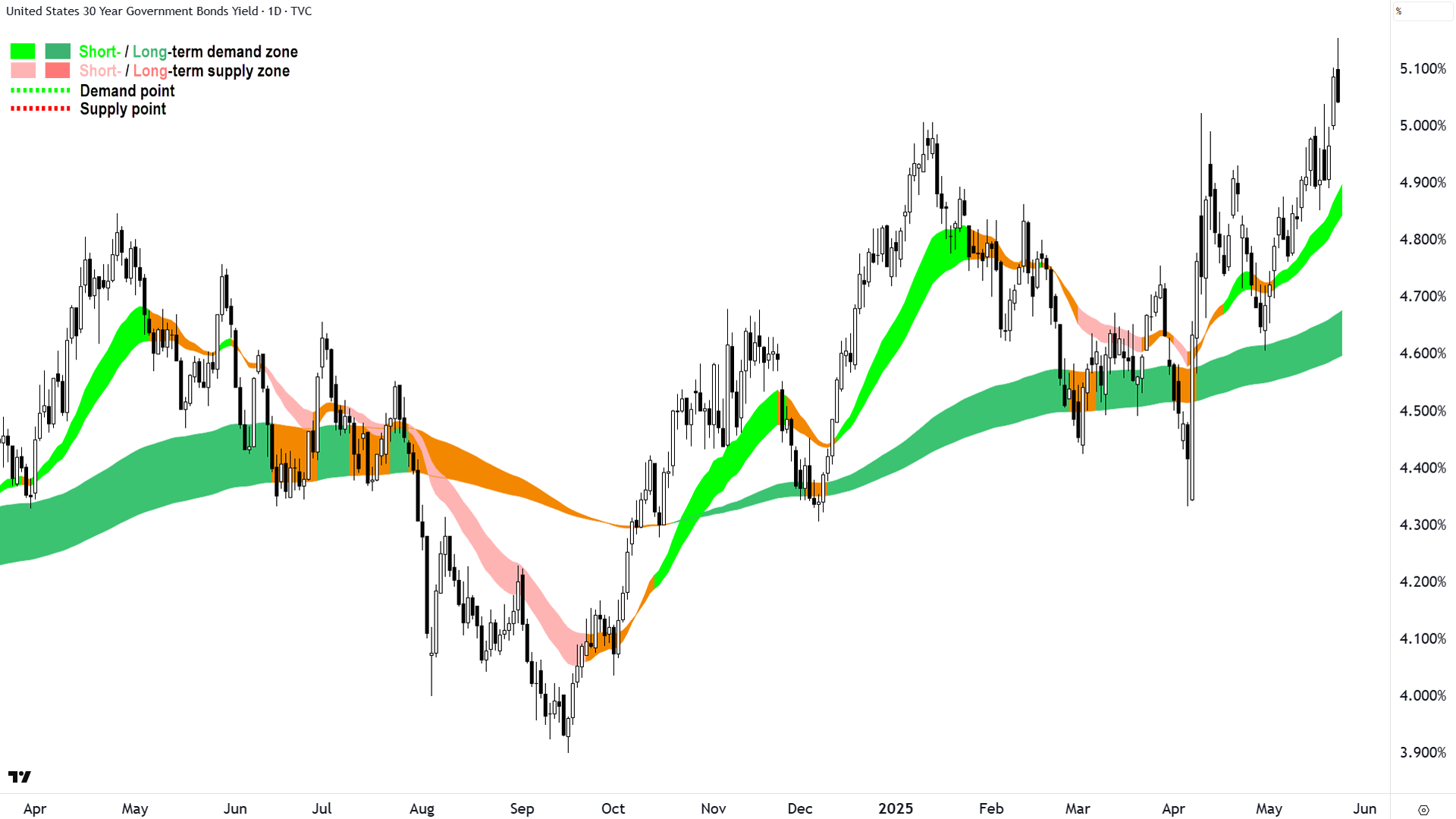

US long term risk-free yields stepped back from the ledge upon which they were standing by around halfway through Thursday's trading session in New York, which in theory is a positive for stocks, but interestingly didn't show up in stock prices. Still, this was enough to help bond-proxy Real Estate Investment Trusts (XPJ) (+1.2%) and long duration plays Communication Services (XTJ) (+0.75%) and Information Technology (XIJ) (+0.72%) to decent gains.

US 30 Year T-Bond Yield (click here for full size image)

{kind=link}

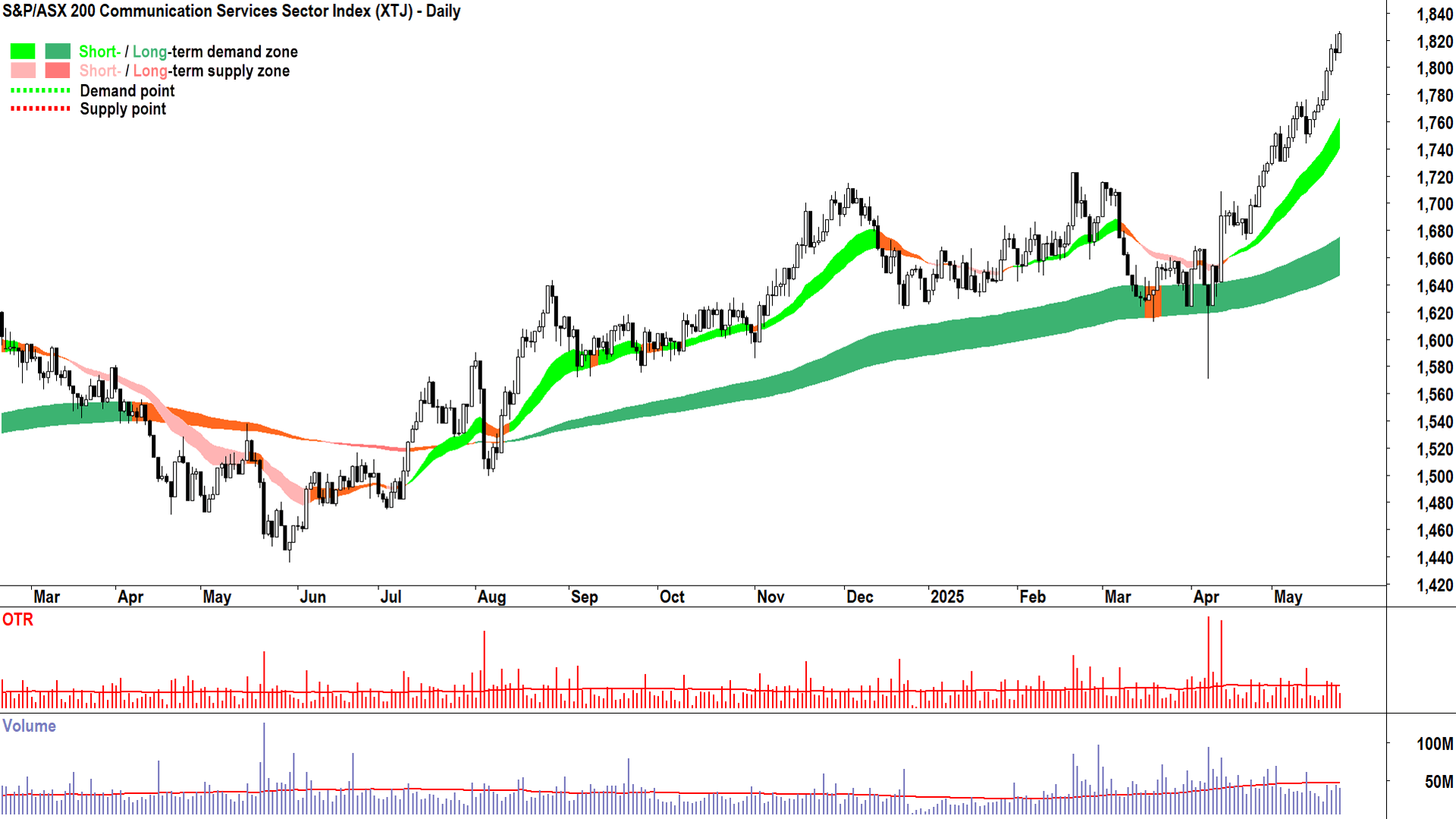

The XTJ is a bit on an interesting one. It's got a good mix of long duration in the form of growth stocks CAR Group (CAR) (1.3%) and REA Group (REA) (+0.46%), but also of plenty of utilities-style, old-fashioned telco and internet providers like Superloop (SLC) (+2.7%), Aussie Broadband (ABB) (+2.6%), Tuas (TUA) (+1.4%), and of course the grandaddy of defence – Teltra (TLS) (+0.85%).

You'll often here me refer to the chart below of the XTJ as "The Telstra Index" due to that stock's large weighting, and therefore its large influence on the XTJ's price. I note that Telstra has been a darling of ChartWatch ASX Scans for a long time now, but so too has been many of those other aforementioned names. It's perhaps no surprise then that the XTJ is hands down the best looking ASX sector index from a technical perspective.

%20sector%20index%20chart%2023%20May%202025.png)

Communication Services (XTJ) sector index chart (click here for full size image)

{kind=link}

Energy (XEJ) (+0.81%) also wasn't terrible today, but plenty of this was due to strength in the sector's uranium stocks. No good news on the uranium price in case you were wondering – it was down overnight – rather, it was likely spurred by media reports the White House will tonight be announcing an executive order aimed at accelerating nuclear reactor deployment.

Boss Energy (BOE) (+12.2%) led the pack, possibly because it also enjoyed a rating upgrade from JP Morgan to overweight from neutral, plus an increase in its price target by 5 cents to $4.05. Bannerman Energy (BMN) (+11.9%), Nexgen Energy (NXG) (+8.7%), and Deep Yellow (DYL) (+8.2%) also enjoyed strong gains.

Utilities (XUJ) (-1.3%) stocks were hardest hit, a little at odds with the bond-proxy narrative, but can I offer: Perhaps some money flowed from gas production and infrastructure companies like APA Group (APA) (-1.5%) and Origin Energy (ORG) (-1.1%) towards uranium plays? That's the great thing about narratives...a little bit of credibility goes a long way! 😁

Elsewhere, the Gold (XGD) sub-index (-0.49%) pulled back, and falls in the major iron ore miners BHP Group (BHP) (-0.73%), Fortescue (FMG) (-2.4%), and Rio Tinto (RIO) (-1.6%) dragged on the Resources (XJR) (-0.54%) sector.

ChartWatch

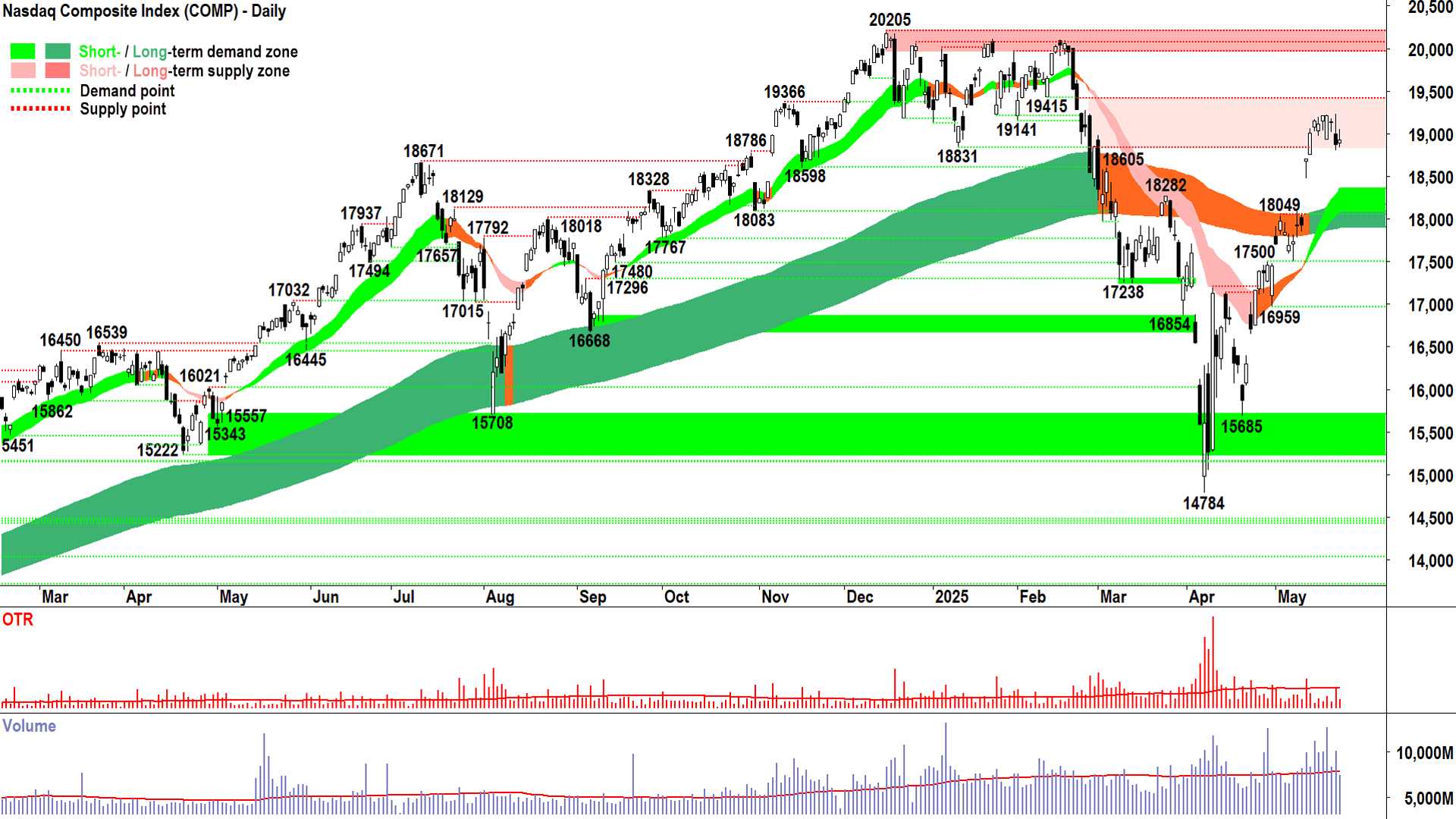

NASDAQ Composite Index

A good day? We know better! 🧐(click here for full size image)

{kind=link}

On the face of it, an up-day on the Comp on Thursday…most investors probably thought it was a good day.

We know better. Hey – it wasn’t a terrible day, but that upward pointing shadow tells us the supply-side continues to flex its muscles into higher prices and liquidity.

= Sell the rally

= The opposite of healthy, demand-control driven price action.

The other big issue for me comes not from Thursday’s candle in isolation, but when one considers it in conjunction with Wednesday’s far better defined supply-side dominated showing.

Consider that at the top of Thursday’s candle, i.e., the height of yesterday’s demand-side optimism – prices had barely tipped halfway back up Wednesday’s range.

So, we proceed with caution, noting that the strong rally from 14784 is experiencing an influx of modestly motivated supply. Enough to halt the demand-side’s advance and cause prices to at least move sideways.

Excess Demand + Supply = Equilibrium. Makes sense.

Of course, if Supply grows / Demand subsides enough…we could flip to Supply > Demand = P ⬇️.

If that’s the case (and I’d say based on the last two candles it’s now better than 50-50 to happen), then I’d expect plenty of latent demand in the system at the short term uptrend ribbon, currently kicking in around 18350.

Hey, it’s also possible the demand-side wipes the floor with this pesky little supply-side showing and rams the price back towards Wednesday’s now crucial high / credible point of supply at 19242.

I still believe that a move like that will completely nullify the supply-side (i.e., they’ll realise they’re better served by hanging on for more) and facilitate a test of 20205.

With overall trends and price action still extremely demand-side oriented, I suspect it’s just a question of whether we get a pullback to the short term trend ribbon before that occurs.

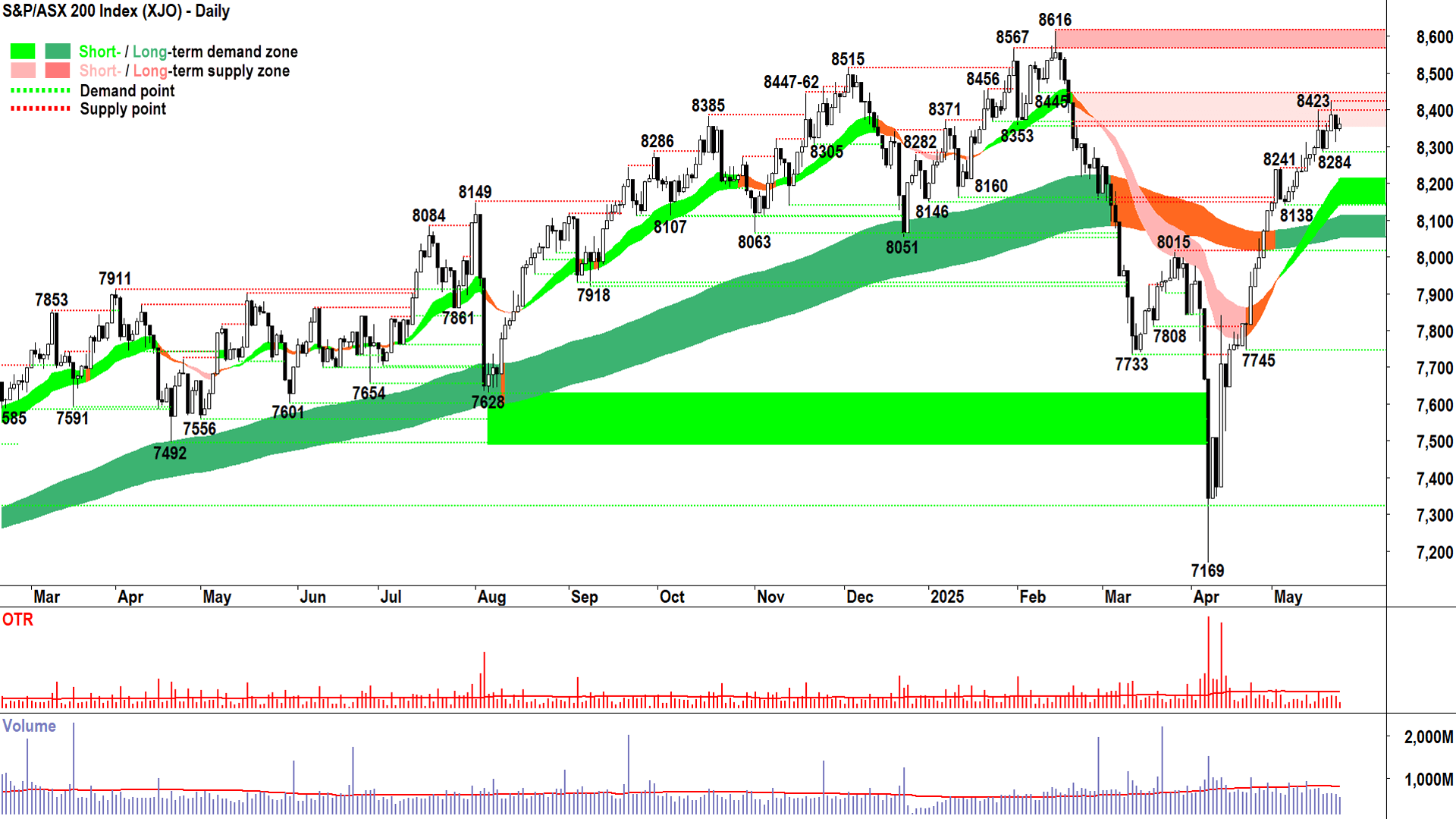

S&P/ASX 200 (XJO)

%20chart%2023%20May%202025.png)

It’s a slowing. It’s far from a reversing... (click here for full size image)

{kind=link}

Given it’s Friday afternoon, I could really could just go “ditto” here and save both of us some trouble.

Do you really need me to pad out an explanation of today’s measly little candle, which is basically just a copy-cat performance of the Comp’s?

That stuff I wrote above about an influx of pesky supply halting a price advance caused by the prevailing demand-side controlled market is very accurate here, too.

It’s a slowing. It’s far from a reversing.

The odds continue to lie in favour of the prevailing trends (up), price action (rising peaks and rising troughs), and (I still want to say) predominance of demand-side candles (pervasive excess demand).

I will change my tune and call it something more sinister when and if any of the above warrant it. Today’s just not that day.

8284-short term trend ribbon is demand. The short term trend is intact until the XJO closes below that zone. Supply is getting pretty thick now just under 8445.

Economy

Today

There weren't any major data releases in our time zone today

Later this week

Saturday

00:00 New Home Sales April (696,000 forecast vs 724,000 in March)

Latest News

Interesting Movers

Trading higher

+15.3% Silex Systems (SLX) – No news, general strength across the broader Uranium sector today.

+14.8% Trigg Minerals (TMG) – No news, general strength across the broader Rare Earths & Critical Minerals sector today, rise is consistent with prevailing short term and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+13.1% MTM Critical Metals (MTM) – Production-Scale FJH Unit Validated for Commercial Rollout, general strength across the broader Rare Earths & Critical Minerals sector today, also a positive note from Morgan Stanley on rare earths and other critical metals demand may have helped this and many other critical minerals stocks.

+12.1% Boss Energy (BOE) – No news, general strength across the broader Uranium sector today, plus JP Morgan upgrade to overweight from neutral, rise is consistent with prevailing short term uptrend and long term trend is transitioning from down to up, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+11.9% Bannerman Energy (BMN) – No news, general strength across the broader Uranium sector today.

+10.8% Mayne Pharma Group (MYX) – No news, today's move is consistent with recent volatility.

+10.2% Novonix (NVX) – U.S. to Place Up to 721% Tariffs on Chinese Graphite, general strength across the broader Critical Minerals sector today.

+10.1% Austin Engineering (ANG) – Change in substantial holding from Thorney International.

+10.0% Dateline Resources (DTR) – Inproving Scoping Study Economics, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+9.8% Chalice Mining (CHN) – No news, general strength across the broader Rare Earths & Critical Minerals sector today.

+8.8% Lotus Resources (LOT) – No news, general strength across the broader Uranium sector today.

+8.7% Nexgen Energy (NXG) – No news, general strength across the broader Uranium sector today.

+8.3% Deep Yellow (DYL) – No news, general strength across the broader Uranium sector today.

+8.2% BetaShares Global Uranium ETF (URNM) – No news, general strength across the broader Uranium sector today, uranium miners ETF.

+8.0% EBR Systems (EBR) – No news since 22-May EBR Capital Raising Presentation.

+6.7% Paladin Energy (PDN) – No news, general strength across the broader Uranium sector today.

Trading lower

-18.5% Coronado Global Resources (CRN) – No news, fall is consistent with prevailing short and long term downtrends, one of the most Featured (highest conviction) stocks in ChartWatch ASX Scans Downtrends list 🔎📉

-8.0% Warriedar Resources (WA8) – No news, general weakness across the broader Gold sector today.

-6.4% Cettire (CTT) – No news, fall is consistent with prevailing short and long term downtrends, one of the most Featured (highest conviction) stocks in ChartWatch ASX Scans Downtrends list 🔎📉

-6.1% Nufarm (NUF) – Continued negative response to 21-May Half Yearly Report, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.5% Duratec (DUR) – REVISED GUIDANCE FOR FY25 AND BUSINESS UPDATE.

-5.3% Botanix Pharmaceuticals (BOT) – Director Update.

-4.6% Antipa Minerals (AZY) – Notice of Release from Voluntary Escrow, general weakness across the broader Gold sector today.

-4.4% Catalyst Metals (CYL) – Investor Presentation - May 2025, general weakness across the broader Gold sector today.

Broker Moves

Australian Agricultural Company (AAC)

Retained at buy at Bell Potter; Price Target: $1.900 from $1.950

Ampol (ALD)

Retained at buy at Goldman Sachs; Price Target: $31.80

ALS (ALQ)

Downgraded to underweight from neutral at Jarden; Price Target: $15.00 from $14.50

ANZ Group (ANZ)

Retained at equal-weight at Morgan Stanley; Price Target: $26.50

ARB Corporation (ARB)

Retained at buy at Ord Minnett; Price Target: $37.00 from $45.00

Bapcor (BAP)

Retained at neutral at Citi; Price Target: $5.43

Betmakers Technology Group (BET)

Retained at speculative buy at Ord Minnett; Price Target: $0.210 from $0.180

Boss Energy (BOE)

Upgraded to overweight from neutral at JP Morgan; Price Target: $4.05 from $4.00

Bluescope Steel (BSL)

Retained at buy at Goldman Sachs; Price Target: $28.70

Catapult Group International (CAT)

Retained at positive at E&P; Price Target: $5.31 from $4.53

Retained at buy at Jefferies; Price Target: $5.60 from $4.60

Cromwell Property Group (CMW)

Upgraded to overweight from neutral at JP Morgan; Price Target: $0.450

Dalrymple Bay Infrastructure/Notes (DBI)

Retained at add at Morgans; Price Target: $4.35

Dexus Industria Reit. (DXI)

Retained at hold at Morgans; Price Target: $2.65 from $2.60

EQ Resources (EQR)

Retained at add at Morgans; Price Target: $0.100 from $0.130

Fortescue (FMG)

Retained at hold at Bell Potter; Price Target: $15.87 from $16.79

Retained at hold at CLSA; Price Target: $15.50 from $16.00

Retained at neutral at Goldman Sachs; Price Target: $15.60

Retained at neutral at Macquarie; Price Target: $15.00

Retained at overweight at Morgan Stanley; Price Target: $16.50

Retained at buy at Ord Minnett; Price Target: $20.00

Retained at outperform at RBC Capital Markets; Price Target: $20.00

Fisher & Paykel Healthcare Corporation (FPH)

Downgraded to hold from buy at Jefferies; Price Target: NZ$39.40

HMC Capital (HMC)

Retained at equal-weight at Morgan Stanley; Price Target: $6.30

Insurance Australia Group (IAG)

Retained at buy at Citi; Price Target: $10.00

Retained at neutral at Goldman Sachs; Price Target: $8.30

Downgraded to neutral from outperform at Macquarie; Price Target: $8.70 from $8.50

Retained at neutral at UBS; Price Target: $9.30

Iluka Resources (ILU)

Upgraded to overweight from equal-weight at Morgan Stanley; Price Target: $4.65 from $3.50

Lynas Rare Earths (LYC)

Upgraded to overweight from underweight at Morgan Stanley; Price Target: $10.00 from $7.10

Medibank Private (MPL)

Retained at Morgan Stanley; Price Target: $4.50

Nick Scali (NCK)

Initiated at buy at Jefferies; Price Target: $21.00

NIB (NHF)

Retained at Morgan Stanley; Price Target: $6.65

Nufarm (NUF)

Downgraded to hold from add at Morgans; Price Target: $2.78 from $4.53

Ramsay Health Care (RHC)

Retained at equal-weight at Morgan Stanley; Price Target: $37.40 from $37.20

Rio Tinto (RIO)

Retained at buy at Ord Minnett; Price Target: $126.00 from $125.00

Reliance Worldwide Corporation (RWC)

Retained at buy at Citi; Price Target: $5.25

Sandfire Resources (SFR)

Retained at underweight at Morgan Stanley; Price Target: $6.75

Sims (SGM)

Retained at sell at Goldman Sachs; Price Target: $12.00

Shape Australia Corporation (SHA)

Initiated at buy at Shaw and Partners; Price Target: $5.00

Sunstone Metals (STM)

Retained at buy at Shaw and Partners; Price Target: $0.032

Syrah Resources (SYR)

Retained at equal-weight at Morgan Stanley; Price Target: $0.400 from $0.220

Viva Energy Group (VEA)

Retained at buy at Goldman Sachs; Price Target: $3.00

Ventia Services Group (VNT)

Retained at outperform at Macquarie; Price Target: $5.00 from $4.50

Wesfarmers (WES)

Retained at sell at Citi; Price Target: $60.00 from $61.00

Retained at buy at Goldman Sachs; Price Target: $87.30 from $80.40

Retained at underweight at Jarden; Price Target: $73.10 from $67.50

Retained at hold at Jefferies; Price Target: $74.00 from $75.00

Retained at neutral at Macquarie; Price Target: $80.00 from $75.00

Retained at underweight at Morgan Stanley; Price Target: $66.70

Retained at neutral at UBS; Price Target: $82.00 from $78.00

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| LKY | Locksley Resources Ltd | $0.049 | +48.49% |

| RPG | Raptis Group Ltd | $0.025 | +38.89% |

| CCE | Carnegie Clean Energy Ltd | $0.059 | +37.21% |

| JNS | Janus Electric Holdings Ltd | $0.295 | +34.09% |

| REC | Recharge Metals Ltd | $0.019 | +26.67% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| ENX | Enegex Ltd | $0.013 | -18.75% |

| REZ | Resources & Energy Group Ltd | $0.013 | -18.75% |

| CRN | Coronado Global Resources Inc | $0.11 | -18.52% |

| JGH | Jade Gas Holdings Ltd | $0.028 | -17.65% |

| EXL | Elixinol Wellness Ltd | $0.015 | -16.67% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| RPG | Raptis Group Ltd | $0.025 | +38.89% |

| CCE | Carnegie Clean Energy Ltd | $0.059 | +37.21% |

| JNS | Janus Electric Holdings Ltd | $0.295 | +34.09% |

| OM1 | Omnia Metals Group Ltd | $0.011 | +22.22% |

| HOR | Horseshoe Metals Ltd | $0.022 | +15.79% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| CRN | Coronado Global Resources Inc | $0.11 | -18.52% |

| EXL | Elixinol Wellness Ltd | $0.015 | -16.67% |

| AVG | Australian Vintage Ltd | $0.075 | -12.79% |

| AVD | Avada Group Ltd | $0.22 | -10.20% |

| GPR | Geopacific Resources Ltd | $0.018 | -10.00% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| CRN | Coronado Global Resources Inc | $0.11 | -18.52% |

| EXL | Elixinol Wellness Ltd | $0.015 | -16.67% |

| AVG | Australian Vintage Ltd | $0.075 | -12.79% |

| AVD | Avada Group Ltd | $0.22 | -10.20% |

| GPR | Geopacific Resources Ltd | $0.018 | -10.00% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| AVH | Avita Medical Inc | $2.04 | -0.49% |

| NWSLV | News Corporation | $41.40 | 0.00% |

| CRN | Coronado Global Resources Inc | $0.11 | -18.52% |

| AOF | Australian Unity Office Fund | $0.48 | 0.00% |

| NFNG | Nufarm Finance (NZ) Ltd | $85.00 | +0.01% |