ASX 200 Live Today - Tuesday, 20th January

The S&P/ASX 200 is set to slip on lower commodity prices and a weak US lead. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, January 20. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Be sure to refresh manually for the latest updates — and let us know how we can make it even better.

ASX 200 lower as banks and miners slip

[2:00 pm] ASX 200 currently down 0.54%, slightly off intraday lows of -0.70%. This largest reflects weakness from Materials (-1.22%) and Financials (-0.79%). Seeing a fairly broad pullback for miners, with most heavyweight names down 1-2%. Though an understandable pullback from record highs (XMJ was up almost 9% YTD).

Tech/growth is getting rather interesting, with Qoria (-18.9%) absolutely obliterated on a 2Q26 update. Hub24 reported a slightly above consensus quarterly FUA update, with the stock rally as much as 8.6% in early trade (currently up just 2.5%). It does seem like valuation is quite a focus point right now, especially when miners are printing cash.

Overall, the index is working its way through a bit of a pullback. It'll be interesting to see where the dust settles for Materials after the massive run up.

Boss Energy non-executive chair steps down

[1:55 pm] Boss Energy says non-executive chair Wyatt Buck plans to step down once a successor is appointed and will remain on the board to support continuity.

The company has begun recruitment and expects to finalise a new chair in the first half of 2026.Buck has served as chair for three years and joined the board in October 2020. The move is framed as an orderly succession following the recent leadership transition to CEO Matthew Dusci.

By Warren Masilamony

RBC's take on BHP

[1:47 pm] RBC analyst Kaan Peker says BHP delivered a mixed but operationally strong 2Q, with iron ore and copper volumes beating expectations, a strong copper price outcome, and an upgrade to FY26 copper guidance, supporting higher FY26 EBITDA and EPS.

Peker flagged Jansen as the key offsetting factor: "Stage 1 capex has been reset higher to US$8.4bn, about $1bn above RBCe. Alongside working-capital outflows, this pressures near-term FCF but balance sheet strength remains intact (with 1H met debt in-line with consensus)."

Xero lifts ASX Tech

[1:29 pm] The S&P/ASX All Technology Index is modestly higher in early afternoon trade, led by Xero which is up 3.9% on the back of the global launch of their new AI Analytics capabilities on their platform.

Ticker | Company | % Chg | Price |

|---|---|---|---|

XRO | Xero | 3.94% | $104.87 |

TNE | Technology One | 1.71% | $27.33 |

CDA | Codan | 1.01% | $37.34 |

MP1 | Megaport | 0.59% | $12.03 |

360 | Life360 | 0.22% | $27.10 |

By Warren Masilamony

ASX 200 Materials retreats after notching two straight record highs in the previous sessions

[12:58 pm] ASX 200 Materials Index down 1.29%, relatively broad-based weakness across iron ore, rare earths, nickel and lithium. Heavyweight BHP, Rio Tinto and Fortescue all down around 1%, which might reflect some follow through weakness from China's weak economic data dump on Monday.

Ticker | Company | % Chg | Price |

|---|---|---|---|

ORA | Orora | -7.33% | $2.09 |

LYC | Lynas Rare Earths | -5.10% | $15.45 |

BSL | Bluescope Steel | -2.77% | $30.76 |

ILU | Iluka Resources | -2.05% | $6.68 |

S32 | South32 | -2.01% | $4.14 |

BHP | Bhp Group | -1.52% | $48.01 |

CIA | Champion Iron | -1.48% | $6.34 |

NUF | Nufarm | -1.46% | $2.37 |

NIC | Nickel Industries | -1.41% | $0.91 |

PLS | Pls Group | -1.39% | $4.62 |

ZIM | Zimplats | -1.25% | $22.83 |

IGO | Igo | -1.23% | $8.80 |

MIN | Mineral Resources | -1.18% | $59.29 |

FMG | Fortescue | -1.14% | $22.14 |

RIO | Rio Tinto | -1.11% | $147.72 |

By Warren Masilamony

29Metals launches $150m capital raise

[11:25 am] Shares in 29Metals was halted this morning as the company is seeking to raise $150 million at 40 cents per share. This represents a sizeable 35.4% discount to its last closing price of 62 cents.

The proceeds will be used for:

Working capital adjusted for the impact of Xantho Extended seismicity

Supports ongoing investment in Gossan Valley

Progression of Capricorn Copper towards restart, including a Restart Definitive Feasibility Study

Drilling of exploration targets across the portfolio

In parallel, the company announced its 2025 production report, with most numbers tracking slightly below guidance.

Copper: 22kt vs 22–25 kt guidance (-6% at the midpoint)

Zinc: 35kt vs 35–40kt guidance (-7%)

Gold: 15koz vs 15–20 koz guidance (-14%)

Silver: 746koz vs 700–900 koz guidance (-7%)

Site Costs: $388 m vs 370–400 m guidance (+1%)

Total Capital: $124 m vs 121–158 m guidance (-11%)

For 2026, the company guided to (vs. Macquarie ests):

Copper: 22–24kt vs 22.3kt ests (+3% at the midpoint)

Zinc: 40–50kt vs 57.2kt ests (-21%)

Gold: 12–20koz vs 21.6koz ests (-26%)

Silver: 600–800koz vs 848koz ests (-17%)

ASX 200 lower as miners and banks weigh

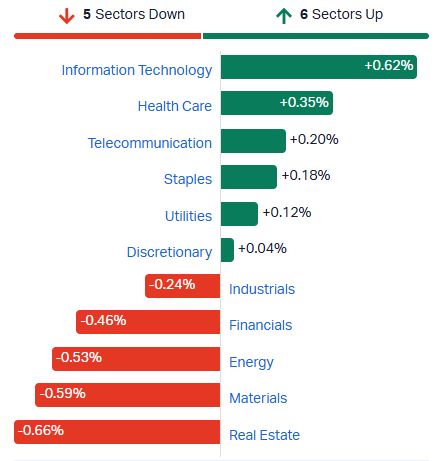

[10:36 am] ASX 200 down for a second straight session, largely reflecting weakness from miners and banks.

S&P/ASX 200 Materials Index experiencing a bit of broad softness (ex-gold), with notable decliners including Lynas (-4.3%), PLS Group (-2.4%), South32 (-1.3%) and slight declines from Fortescue and Rio Tinto

Financials down for a second day, with the Big Four banks all down around 0.5-0.8%

Tech stocks slightly higher after closing at the lowest since 7-Apr-25 on Monday

ASX 200 sector performance (Source: TradingView)

Qoria, ARB Corp nosedive

[10:25 am] Qoria (-20.4%) and ARB Corp (-9.1%) both down massively this morning.

Qoria's Q2 update read relatively well at face value, the company also reaffirmed its FY26 guidance ($145 million in revenue, 20% ARR growth, 20% adjusted EBITDA margin, and positive free cash flow). I guess this goes to show that the only thing that props up a richly valued tech stock is a line of willing buyers (and this is what happens when they disappear). Qoria reported a Q2 exit ARR of $149 million, so you could argue it is looking relatively cheap as it now trades closer to 3x ARR.

No surprises with the ARB selloff, with the company pre-announcing a 1H26 profit before tax of ~$58 million vs. Macquarie expectations of $63 million (7.9% miss).

BHP Q2 production beat, lifts Jansen Stage 1 capex

[10:13 am] BHP’s Jansen Stage 1 project remains on track for ~4.15Mtpa output despite higher capital costs, while Q2 production beats expectations across key commodities and FY26 guidance points to modest upgrades in copper and energy coal.

Total investment for Jansen Stage 1 revised up to $8.4bn from prior range of $7.0–7.4bn, reflecting updated cost pressures since initial $5.7bn approval in 2021.

First production schedule reverted to mid-CY27

Stage 1 is 75% complete and expected to deliver ~4.15Mtpa, with underlying EBITDA margins ~63–64%, IRR 7.9–9.1%, and payback of 11–15 years.

Jansen Stage 2 construction progressing, BHP will update capex estimates in Q4 FY26, with long-term potential for 16–17Mtpa ultimate production.

Q2 FY26 production report vs consensus:

WAIO (100% basis) up 5% year-on-year to 76.3Mt vs 74.4Mt (2.6% beat)

Copper down 4% to 490.5kt vs 483.8kt (1.4% beat)

Metallurgical coal down 3% to 4.3Mt vs 4.5Mt (4.4% miss)

Energy coal up 25% to 4.6Mt vs 3.8Mt (21.1% beat)

FY26 guidance:

Iron ore 258–269Mt, unchanged

Energy coal 14–16Mt, upper half of prior guidance

Steelmaking coal 18–20Mt, unchanged

Copper 1,900–2,000kt vs prior 1,800–2,000kt

Company page: BHP Group (BHP)

ARB set to tumble

[10:02 am] ARB has reported unaudited numbers for 1H26, with profit before tax of approximately $58 million, representing a 16.3% year-on-year decline and 7.9% below UBS expectations of $63 million.

Edit: Typo here. It was UBS estimates of $63m, not Macquarie.

The announcement noted: "As advised at the Company’s AGM, the two key contributors to the decline in profit in 1H FY2026 were: lower gross margins driven by the weaker Australian dollar compared with the Thai baht and lower factory overhead recoveries as inventory levels materially increased in the prior comparable period."

Company page: ARB Corp (ARB)

AMP names Blair Vernon as CEO as Alexis George prepares to retire

[9:50 am] Blair Vernon will succeed Alexis George as AMP’s Group CEO on 30 March 2026.

Blair Vernon, AMP’s current CFO, brings over 30 years of experience in financial services across Australia and New Zealand, including previous leadership roles as CEO/MD of New Zealand Wealth Management and Acting CEO of AMP Australia.

Vernon led AMP’s transformation and simplification program, including the divestment of AMP Capital assets, and has been Group CFO since July 2023.

CEO contract: $1.4 million salary, short-term incentive up to 125% of salary, long-term incentive target of 100% of salary, six-month termination notice, 12-month post-employment restraint.

Alexis George will retire from executive roles on 30 March 2026 but remain available for handover and support, with all incentives treated per existing contract terms.

Company page: AMP (AMP)

Hub24 delivers record inflows in 2Q26

[9:45 am] Hub24 delivered a strong December quarter funds under administration update, with record inflows and still-solid growth rates.

Platform FUA up 5% quarter-on-quarter and 29% year-on-year to $127.9bn

Platform FUA growth driven by record net inflows of $5.6bn

Record half-year net inflows of $10.7bn

Total FUA up 26% year-on-year to $152.3bn

Hub24 platform ranked first for quarterly and annual net inflows

Commenced development of myhub leveraging Hub24 Group capabilities to address productivity challenges for advice practices

To add some perspective, Macquarie (28-Nov-25) was expecting 1H26 FUA of $128.2bn, with first-half inflows of $10.2bn.

Company page: Hub24 (HUB)

Qoria delivers record Q2 revenue

[9:38 am] Qoria delivered record ARR growth in a typically slow quarter, surpassing US$100 million in ARR and building a robust K12 pipeline for FY26.

Q2 exit ARR of $149 million after FX adjustments, up 19% year-on-year

Cash receipts for 1H26 up 20% year-on-year $79.1 million

Free cash flow up 46% to $8.9 million.

Qustodio ARR is growing at an annualised rate of 34%, with the weighted K12 pipeline up 29% to $13.6 million and an unweighted pipeline of $39.5 million.

FY26 guidance reaffirmed: $145 million in revenue, 20% ARR growth, 20% adjusted EBITDA margin, and positive free cash flow.

Qoria joins a long list of tech stocks that have been smashed in recent months, it's down 48% from its 21-Oct-25 record high and trading at the lowest since July. Today's quarterly suggests the fundamentals and growth rates remain the same, though the market seems no longer willing to pay a premium valuation for most software names.

Company page: Qoria (QOR)

Origin Energy extends Eraring operations to strengthen NSW power security

[9:32 am] Origin Energy will keep Eraring Power Station running until 2029 to support NSW electricity reliability while staying on track with emissions targets.

Extend operation of all four Eraring Power Station units from 19-Aug-27 to 30-Apr-29, supporting NSW system security.

No further major maintenance overhauls are planned before the plant’s retirement in April 2029.

The extension is not expected to impact Origin’s 2030 emissions reduction targets or its net zero by 2050 ambition.

The Eraring site will remain a key part of the National Electricity Market beyond 2029.

The Eraring Battery, partially operational since late 2025, will reach full capacity in Q1 2027 with 700MW / 3,160MWh, providing about 4.5 hours of storage for NSW.

Company page: Origin Energy (ORG)

Bellevue Gold confirms Q2 production

[9:26 am] Bellevue Gold delivered Q2 production of 32koz with realised pricing offsetting slightly higher costs.

Gold sales of 31,905oz were marginally below consensus while AISC of A$2,989/oz came in slightly above A$2,914 consensus, but the company reiterated confidence in second half cost reductions and remains on track to meet FY26 production and cost guidance.

Company page: Bellevue Gold (BGL)

Northern Star lifts FY26 cost guidance

[9:25 am] Northern Star has bumped its FY26 AISC guidance to A$2,600-2,800/oz vs. prior A$2,300-2,700/oz.

This represents an 8% increase at the midpoint

AISC revision driven predominately by lower gold sales and higher royalties from elevated gold prices

Sustaining capex guidance of A$750m remains unchanged

It was just three weeks ago that Northern Star downgraded its FY26 gold sales guidance to 1,600-1,700koz vs. prior 1,700-1,850koz (7% downgrade at the midpoint). The company said this downgrade reflected a number of isolated negative events in late December, including a primary crusher failure at KCGM, longer-than-expected recovery at Yandal and lower mined grades at Pogo.

On the day of the gold sales downgrade (2-Jan), Northern Star shares dipped 8.6% (down as much as 11.4% intraday).

Company page: Northern Star (NST)

Yancoal Q4 2025 quarterly report

[9:20 am] Yancoal delivered a record performance in the December quarter and bumped its cash position to $2.13 billion (vs. market cap of $7.2bn). Here are some of the key numbers from the quarterly report:

Q4 attributable saleable coal production up 7% year-on-year to 10.4Mt

2025 attributable saleable coal production up 5% to 38.6Mt vs. guidance of 35-39Mt

2025 operational guidance remains unchanged at $89-97 a tonne and $750-900m capex (to report towards the bottom end of the range)

Q4 average realised price up 6% quarter-on-quarter but down 16% year-on-year to A$148 a tonne

Cash balance up 18.3% quarter-on-quarter to $2.13 billion

Management commentary: "Our strengthening financial position enables us to consider dividends and contemplate value adding growth opportunities. We look forward to providing further capital management commentary when we release our 2025 Financial Results."

Company page: Yancoal (YAL)

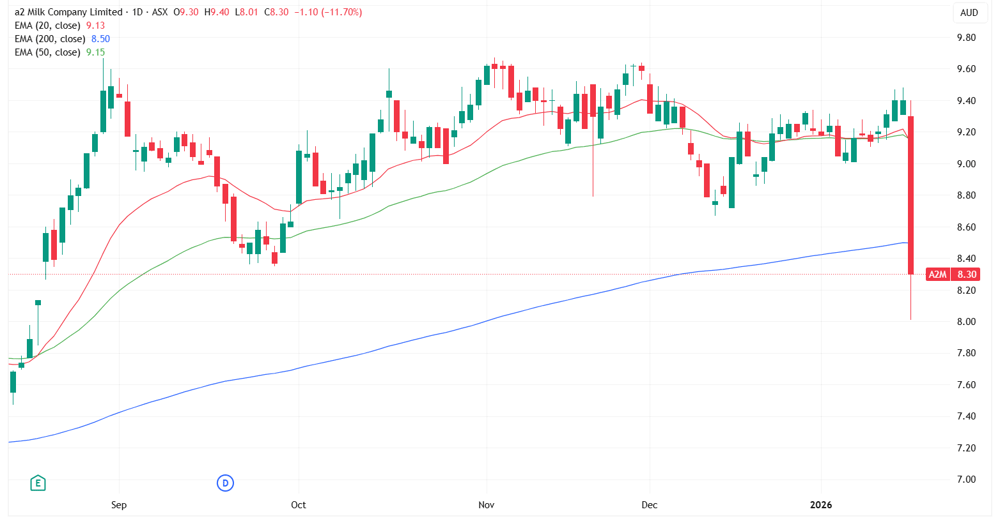

A2 dipped on China data

[9:07 am] A2 Milk abruptly sold off around 1:00 pm AEST on Monday, which was exactly when the Chinese economic data was released. The stock finished the session down 11.7% ($8.30) to the lowest since 19 August 2025.

A2 Milk daily price chart (Source: TradingView)

The selloff appears somewhat of an overreaction, as A2 upgraded its FY26 guidance just two months ago on 20 November 2025.

FY26 revenue growth of 10-13% vs. prior high single digits

NPAT to be slightly up on FY25 vs. prior 'similar' guidance

Intention to declare a special NZ$300m dividend, subject to regulatory approvals being received for two existing Pokeno China label registrations

Analysts were broadly positive on the guidance upgrade, including:

Macquarie retained Outperform, raised target from $8.70 to $9.50, citing an improved revenue outlook driven by broad-based category strength, strong execution across geographies and confidence in Pokeno tracking to plan, with the special dividend still linked to regulatory milestones.

UBS retained Neutral, raised target from $10.55 to $11.10, pointing to strong early FY26 trading across all product lines, continued momentum in English Label brands and lower-than-expected Pokeno manufacturing losses, with valuation now reflecting medium-term earnings potential.

China GDP and economic data recap

[8:59 am] Big economic data dump from China on Monday, which drove a downward intraday move for iron ore miners (FMG -1.8%) and sharp selloff for A2 Milk (-11.7%).

Here are some of the key takeaways from the GDP print:

GDP growth slowed to 4.5% year-on-year in the December quarter, the weakest since the pandemic

2025 full year real growth of 5% masked nominal growth of just 4%, pointing to a third year of deflation

Industrial output rose a strong 5.9%, supported by resilient exports, while retail sales lagged at 3.7% as households remained constrained by housing stress, jobs uncertainty and falling prices

Fixed asset investment excluding rural households fell 3.8%, the first annual contraction in decades, reflecting tighter controls on local government debt and efforts to curb excess capacity

Property remains the key drag, with investment down 17.2%, faster price declines and ongoing double digit falls in new housing starts despite some easing in the pace of contraction.

Demographic pressures intensified, with the lowest birth rate since 1949 and a shrinking working age population adding to long term fiscal and growth challenges

China crosses a new line in Taiwan airspace

[8:55 am] Beijing’s first confirmed military drone incursion into Taiwanese airspace signals a calibrated escalation in pressure on Taipei.

A Chinese reconnaissance drone entered Taiwanese airspace over Pratas Island for about four minutes, operating above the reach of air defence systems before departing after radio warnings.

This marks the first acknowledged military drone penetration, raising the baseline of China’s grey zone tactics compared with earlier civilian drone incidents.

The move comes amid heightened military activity, including recent PLA live fire drills following an $11 billion US arms package for Taiwan.

China framed the flight as lawful training, reinforcing its strategy of normalising provocative actions while avoiding direct confrontation.

Source: Bloomberg

Greenland standoff hardens US–Europe fault lines

[8:51 am] Washington is escalating its Greenland push with tariffs and security rhetoric, deepening strains with Europe and raising the risk of economic and political retaliation.

The US is moving beyond rhetoric, imposing a 10% tariff on goods from eight European countries from February 1, rising to 25% in June, signalling a willingness to use trade pressure to force concessions.

Bessent framed Europe as strategically weak, dismissing EU threats to unwind a tariff deal and arguing the US is deliberately leveraging emergency powers and security dominance.

Europe’s response is sharpening, with French President Macron urging activation of the EU’s anti coercion instrument, marking a potential shift from diplomacy to formal retaliation.

The rationale from Washington centres on Arctic competition, missile defence ambitions and Europe’s past energy dependence on Russia, tying Greenland to broader US security and industrial strategy.

Source: Bloomberg

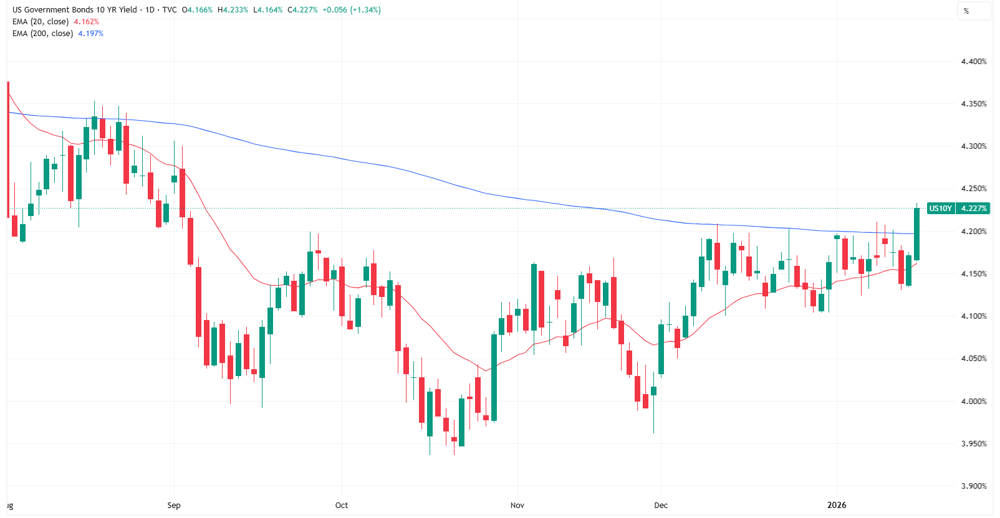

US 10-year yields hit four month high

[8:49 am] US 10-year yield up 5 bps overnight to 4.22%, trading at the highest level since 3-Sep-25 and now above the 200-day moving average for the first time since last August.

US 10-year yield daily chart (Source: TradingView)

Trump’s trade threats over Greenland raise the risk Europe rebalances away from US assets, with implications for the dollar, euro and global markets.

Europe is the US’s largest external financier, holding about $8 trillion in US bonds and equities, almost double the rest of the world combined, making any shift in allocations market moving.

Deutsche Bank argues geopolitical strain is undermining Europe’s willingness to keep underwriting US deficits, increasing the risk of dollar rebalancing.

The euro’s initial dip looks fragile, with tariffs potentially accelerating European political cohesion and limiting sustained downside for the currency.

Early market signals were mixed, with the euro rebounding 0.2 percent on the day while US and European equity futures fell, pointing to rising cross asset uncertainty.

A quiet overnight session

[8:45 am] Edit: I did not realise the US market was closed.

Good morning!

[8:34 am] ASX 200 futures are down 32pts (-0.36%) as of 8:30 am AEDT.

To catch up on all overnight developments, check out today's Morning Wrap.