ASX 200 Live Today - Monday, 25th May

The S&P/ASX 200 is trading higher on Monday amid relatively broad gains spanning miners, REITs, tech, retailers and industrials.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Monday, May 25. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 higher,

[2:15 pm] That's a wrap. The ASX 200 is currently up 0.39% and on track to record a third straight day of gains.

Materials (+1.92%) lifting the market higher, now up 5.8% in the last three sessions. A broad uplift across the mining complex today, with the All Ords Gold index up 4.4%, most mid-to-large copper names up 2-3%, Lynas up 1.7%, South32 up 1.9% and most uranium names up 2-4%. Heavyweights BHP and Rio Tinto also up 1-1.5%

Tech (+0.73%) has traded pretty much flat in the previous four sessions, now catching a slight bit of upside

Telcos (-1.26%) sharply lower, largely reflecting from CAR Group (-4.1%) and Seek (-5.3%)

Energy (-1.9%) is unsurprisingly weak, with Brent currently down 8.8% to US$95 a barrel

Overall, an encouraging start to the week amid lower bond yields, oil prices and a softer US dollar. Though still no major breakthrough in US-Iran peace talks. I don't think any of us would be surprised to wake up to oil prices 10% higher or lower from here. The situation remains fluid, but for now it's offering local equities a bit of a bounce.

Coal stocks extend gains

[1:50 pm] Coal stocks are still making fresh intraday highs as markets digest the news of a fatal mine explosion in China's coal-belt region of Shanxi.

Dalian coking coal futures surged as much as 8% with spillover buying across iron ore and steel contracts, while Shanxi Lu'an Environmental Energy gained as much as 9.2% and Jinneng Holding Shanxi Coal Industry as much as 7.4%

Deadliest mine accident in China since 2009, with President Xi Jinping and Premier Li Qiang vowing "a rigorous and thorough investigation" and "severe penalties in accordance with laws and regulations"

Two thermal coal mines in Shanxi's Qinyuan county with combined annual capacity of 1.8m tons have halted operations, with major hubs in Shaanxi, Inner Mongolia and Henan also launching inspections

Ticker | Company | % Chg | Price |

|---|---|---|---|

CRN | Coronado Global | 20.93% | $0.26 |

WHC | Whitehaven Coal | 10.54% | $9.02 |

YAL | Yancoal Australia | 8.78% | $7.13 |

SMR | Stanmore Resources | 7.85% | $2.61 |

NHC | New Hope | 4.82% | $5.77 |

TER | Terracom | 4.48% | $0.07 |

Indonesia to roll out centralised commodity export agency

[1:10 pm] Indonesia is moving ahead with the rollout of its new centralised commodity export agency Danantara Sumberdaya, with updates due in the coming weeks as the government takes direct control of palm oil, thermal coal and nickel exports.

Initial transition period from 1 June will require exporters to report sales of strategic commodities to Danantara Sumberdaya, with the entity later taking control of export contracts, shipping and payments

Palm oil, thermal coal and some nickel products are the first commodities targeted, all markets where Indonesia dominates global supply

President Prabowo cited up to $150bn in annual losses from "leaks" such as under-invoicing as justification, against total state revenue last year of just under $160bn

Sweeping changes have unnerved investors concerned Indonesia is drifting from its market-friendly and fiscally disciplined approach, with Moody's flagging higher risks for miners

Source: Bloomberg

Australian yields hit 10-week low

[1:10 pm] US-Iran peace talk hopes and a sharp pullback in oil prices has dragged the Aussie 10-year yield to the lowest since 10 March. The 10-year is on track to record four straight days of declines, down 22 bps to 4.88%.

Australia government 10-year bond yield (Source: TradingView)

Airlines rally on oil price weakness

[12:28 pm] Qantas (+4.9%) and Virgin (+6.5%) are both trading notably higher on the back of a sharp pullback in oil prices. Both stocks have been relatively rangebound for the past ~2 months, today's gains have pushed both stocks towards the upper end of their recent trading ranges.

Qantas daily price chart (Source: TradingView)

Adore Beauty bounces off record lows

[12:24 pm] Adore Beauty is bouncing off record lows after a trading update this morning showed solid YTD revenue growth despite cost-of-living pressures and increased promotional activity.

FY26 revenue (first 47 weeks to 24 May) up 7.4% to $193.4m vs pcp

Year-to-date new customer acquisition up 13.9% vs pcp

H2 FY26 gross margin expected in line with prior year at 34.5%

FY26 full year underlying EBITDA expected at ~$4.0m (~2.0% of revenue)

FY27 revenue growth target of at least 10%, with underlying EBITDA guidance of $9-13m, implying a more than 2x lift on FY26

Three new Adore Beauty stores opened in 2H26 (Kotara, Parramatta, Robina), taking total network to 20 stores (14 Adore Beauty, 6 iKOU), with a further four Adore Beauty and one iKOU store to open in H1 FY27

CEO Sacha Laing noted "more pronounced cost-of-living pressures have seen an increase in promotional activity in the market through April and May resulting in a tempered slowdown in trading in Q4"

ABY shares are up 9.3% at the time of writing to 35 cents, but still down 72% year-to-date.

Company page: Adore Beauty (ABY)

China coking coal futures hit daily limit after mine blast

[11:48 am] China's coking coal futures rose by the daily limit following a mine blast at the Liushenyu Coal Mine in Shanxi province. Local coal names are trading sharply higher at noon.

Ticker | Company | % Chg | Price |

|---|---|---|---|

CRN | Coronado Global | 19.53% | $0.26 |

SMR | Stanmore Resources | 7.44% | $2.60 |

WHC | Whitehaven Coal | 7.29% | $8.76 |

YAL | Yancoal Australia. | 6.34% | $6.97 |

TER | Terracom | 5.97% | $0.07 |

NHC | New Hope Corporation | 2.73% | $5.65 |

Uranium sector: PDN upgraded to Outperform, BOE to Neutral

[11:25 am] Macquarie has refreshed its uranium sector views, upgrading Paladin Energy to Outperform on improving value and Boss Energy to Neutral as concerns become better priced in.

PDN upgraded to Outperform: Shares now imply US$77/lb uranium vs spot US$84/lb, with underperformance vs. NexGen, Cameco (13-15% in last five weeks) and Namibian developer peers (~4%) seen as unwarranted given Langer Heinrich ramp-up nearly hitting FCF and PLS approval progress

BOE upgraded to Neutral from Underperform: Concerns remain on Honeymoon resource downgrades and the new feasibility study (smaller and more marginal asset than previously believed), but now more adequately reflected in the share price

BMN (Outperform): Etango approaching FID with CNNC partnership substantially reducing funding need, with Chair Brandon Munro flagging uranium term prices may need to push to ~US$120/lb to incentivise further greenfield supply

DYL (Outperform): Tumas project has completed earthworks and entered civil works phase (10-12 months), with a strong cash balance preserving FID timing flexibility while engaging with potential strategic partners including from the US

LOT (Outperform): Target cut to $1.30 from $1.90 on raised equity dilution discount factor to $0.80/sh (was A$0.21/sh), reflecting possible capital raise risk if export approvals or prepayment/inventory finance face delays

Paladin viewed as the best way to invest in the uranium cycle/AI megatrend, given largely uncontracted PLS volumes will access higher realised prices post 2030

Charter Hall rallies on guidance upgrade

[11:08 am] Charter Hall shares are up 5.4% in early trade after the company upgraded its FY26 operating EPS guidance by a further 3% to 103 cents, which represents a 26.5% increase on FY25.

“With $6.5 billion in FYTD inflows, FY26 is set to be the strongest year of capital raising in the Group’s 35-year history," said CEO David Harrison.

“We also note the recent changes in the Federal budget to capital gains tax and negative gearing for the residential property sector. We expect these changes could drive a rotation of capital demand towards higher yielding commercial assets from low yielding residential investments."

Charter Hall daily price chart (Source: TradingView)

Gold and oil correlation at extreme negative

[11:04 am] The correlation between oil and gold has hit a level not seen in decades, which is rather unusual as they often move together as commodities, inflation hedges and/or beneficiaries of a weaker US dollar.

.png)

Source: Market Index

Gold stocks broadly higher

[10:50 am] Gold stocks are trading broadly higher in response to a strong uptick in gold prices this morning, currently up 1.48% to US$4,575 an ounce.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

MEK | Meeka Metals | 13.0% | $0.13 | -51.9% |

BC8 | Black Cat Syndicate | 7.2% | $1.12 | -7.8% |

RSG | Resolute Mining | 6.9% | $1.31 | 6.9% |

CYL | Catalyst Metals | 6.0% | $5.63 | -23.7% |

CMM | Capricorn Metals | 6.0% | $14.06 | 0.4% |

RMS | Ramelius Resources | 5.6% | $3.38 | -17.4% |

SBM | St. Barbara | 4.9% | $0.58 | 1.2% |

GMD | Genesis Minerals | 4.5% | $6.17 | -13.9% |

PNR | Pantoro Gold | 4.5% | $3.27 | -33.3% |

NST | Northern Star | 4.4% | $19.66 | -20.0% |

OBM | Ora Banda Mining | 4.3% | $1.39 | -9.3% |

NEM | Newmont | 4.2% | $157.29 | 4.8% |

ALK | Alkane Resources | 4.1% | $1.52 | 14.3% |

EMR | Emerald Resources | 4.1% | $6.12 | -2.5% |

BGL | Bellevue Gold | 3.6% | $1.59 | -6.2% |

WGX | Westgold Resources | 3.5% | $5.14 | -18.5% |

VAU | Vault Minerals | 3.5% | $4.56 | -16.3% |

PRU | Perseus Mining | 3.4% | $5.42 | -1.6% |

EVN | Evolution Mining | 3.2% | $12.57 | 0.0% |

RRL | Regis Resources | 2.7% | $6.52 | -13.3% |

AMI | Aurelia Metals | 1.7% | $0.30 | 22.4% |

Energy stocks struggle

[10:47 am] The S&P/ASX 200 Energy index is down 2.2% in early trade, in response to an ~8.3% dip in Brent to US$95.66 a barrel. While oil and gas, refiners and LNG stocks are trading broadly lower, coal stocks are catching a bid and trading 1-3% higher.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

KAR | Karoon Energy | -5.0% | $2.01 | 30.2% |

STX | Strike Energy | -3.8% | $0.13 | 19.0% |

WDS | Woodside | -3.4% | $31.02 | 30.7% |

VEA | Viva Energy Group | -3.2% | $2.24 | 8.0% |

BPT | Beach Energy | -2.9% | $1.10 | -6.2% |

STO | Santos | -2.9% | $8.00 | 29.4% |

ALD | Ampol | -2.7% | $34.49 | 8.0% |

BRK | Brookside Energy | -2.2% | $0.46 | -3.2% |

NHC | New Hope Corporation | 1.5% | $5.59 | 39.3% |

WHC | Whitehaven Coal | 3.1% | $8.42 | 8.3% |

YAL | Yancoal Australia | 3.4% | $6.78 | 36.0% |

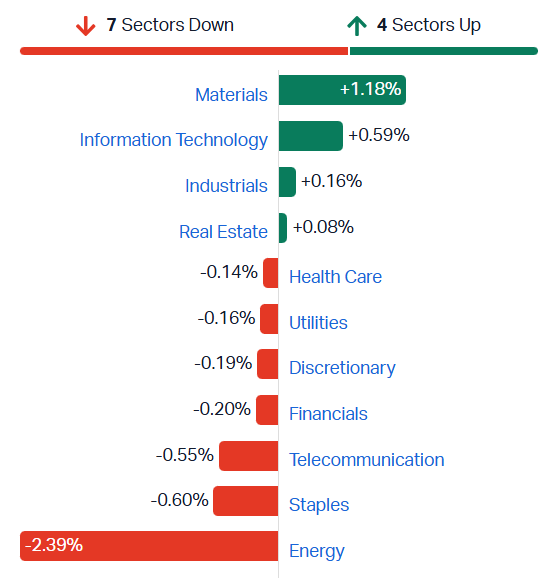

ASX 200 breakeven as miners continue to bounce

[10:41 am] ASX 200 up 0.06% in early trade as miners offset weakness a sharp dip in energy stocks and softness among staples, telcos, banks and retailers.

The Materials Index is on a three-day winning streak, up 5.0%. Today's upside features broad gains from BHP (+0.22%), Sandfire (+2.1%), Lynas (+2.1%), Newmont (+3.9%) and Aloca (+7.0%).

S&P/ASX 200 sectors (Source: Market Index)

Analysts' take on Guzman Y Gomez

[10:17 am] Guzman y Gomez announced the immediate cessation of its US operations last Friday, with one-off exit costs of $30-40 million to be recognised in FY26, alongside FY26 Australia underlying EBITDA guidance of ~$85 million, slightly ahead of some analyst expectations. The stock rallied as much as 20.2% on the day, but finished the session 9.5% higher.

The move was widely viewed the exit as a strategically correct decision that demonstrates capital discipline and removes a multi-year earnings drag, with attention now shifting to the Australian growth outlook underpinned by store rollout, mid-single-digit same-store sales growth, and Uber Eats exclusivity.

RBC Capital Markets retained Outperform, raised target from $22.00 to $23.00, viewing the US exit as a tough but strategically correct decision that allows management to focus on network growth and franchise economics, with Uber-funded promotions and easier comps supporting near-term sales momentum.

JPMorgan retained Overweight, raised target from $22.50 to $23.00, noting structural US challenges made the exit inevitable and that the simplified outlook narrows investor focus to the attractive Australian earnings trajectory, though Uber exclusivity is unlikely to persist long-term.

UBS retained Buy, raised target from $22.00 to $24.00, viewing the exit as reflecting financial discipline and removing a multi-year earnings drag, with Singapore and Japan master franchise success seen as a better template for future offshore expansion.

Service Stream to acquire RIE Group for up to $8m

[10:17 am] Service Stream has agreed to acquire Queensland-based RIE Group, a specialised high-voltage electrical and instrumentation business, to expand its industrial services capabilities and geographical footprint.

Initial payment of $6.5m subject to a purchase price adjustment based on final net working capital at completion

Additional cash consideration of up to $1.5m may be paid on a pro-rata basis if the minimum FY27 financial performance threshold is exceeded

RIE generates approximately $13m in revenue and employs 60-120 staff at peak outage periods, operating across the Surat Basin, Darling Downs and Gladstone regions

Business serves oil and gas, power generation and renewable sectors, providing exposure to blue-chip asset owners and energy transition tailwinds

Company page: Service Stream (SSM)

Top ASX 200 gainers

[10:07 am] Aloca soars on an uptick in aluminium prices and broker updates, while gold stocks open broadly higher as gold prices rally 1.45% to US$4,573/oz this morning.

Ticker | Company | % Chg | Price |

|---|---|---|---|

AAI | Alcoa Corporation | 7.16% | $99.99 |

CMM | Capricorn Metals | 5.95% | $14.06 |

TLX | Telix Pharmaceuticals | 5.18% | $14.01 |

VGN | Virgin Australia | 4.49% | $2.56 |

CHC | Charter Hall Group | 4.37% | $20.18 |

NST | Northern Star Resources | 4.30% | $19.64 |

WAF | West African Resources | 3.99% | $3.13 |

MCY | Mercury Nz | 3.79% | $5.75 |

OBM | Ora Banda Mining | 3.76% | $1.38 |

RMS | Ramelius Resources | 3.75% | $3.32 |

Top ASX 200 losers

[10:07 am] Lendlease continues its spiral to fresh all-time lows (now down ~11% in the last three sessions), while energy names like Woodside, Santos and Viva Energy open 2-3% lower off the back of a sharp pullback in oil prices.

Ticker | Company | % Chg | Price |

|---|---|---|---|

LLC | Lendlease Group | -3.19% | $2.73 |

WDS | Woodside Energy Group | -2.96% | $31.15 |

SEK | Seek | -2.52% | $12.39 |

STO | Santos | -2.25% | $8.06 |

LNW | Light & Wonder | -2.24% | $112.23 |

GNP | Genusplus Group | -2.19% | $9.39 |

VEA | Viva Energy Group | -2.16% | $2.26 |

CGF | Challenger | -2.01% | $9.27 |

PNI | Pinnacle Investment Management | -1.94% | $15.18 |

ALL | Aristocrat Leisure | -1.84% | $49.49 |

Gold and copper sharply higher, yields slip

[9:35 am] The ~5% oil price dip is driving sharp moves across the commodity complex, with gold up 1.5% in early trade to US$4,577/oz and copper up 1.4% to US$6.49/lb.

Gold daily price chart (Source: TradingView)

Copper daily price chart (Source: TradingView)

The Australian 10-year bond yield has also opened lower for a fourth straight day, down 2 bps to a 10 week low of 4.89%.

Australia government 10-year bond yield daily price chart (Source: TradingView)

Brent tumbles ~5% in early trade

[9:29 am] Brent has tumbled 5.6% in early trade on Monday, to a one-month low of US$98.30 a barrel.

Brent daily price chart (Source: TradingView)

Charter Hall upgrades FY26 OEPS guidance for second time

[9:20 am] Charter Hall has lifted FY26 operating EPS guidance by a further 3% to 103.0 cents, representing a 26.5% year-on-year increase, underpinned by strong institutional capital momentum and FUM growth.

FY26 DPS guidance maintained at 6% growth on FY25, marking 15 consecutive years of DPS growth, with guidance assuming nil contribution from performance fees

FYTD gross equity inflows of $6.5bn (up $1.7bn since 1H FY26), set to make FY26 the strongest capital raising year in the Group's 35-year history

Property Funds Management FUM up to $74.7bn from $71.7bn at 31 December 2025, with 25 new institutional investors added to the platform over the last 18 months

Recent activity includes a new $1.2bn diversified core direct institutional real estate mandate (taking combined mandates to $3.3bn) and the $1.15bn acquisition of The O'Connell Precinct in Sydney CBD

CEO David Harrison noted recent Federal budget changes to capital gains tax and negative gearing for residential property could drive a rotation of capital demand towards higher yielding commercial assets

Company page: Charter Hall (CHC)

Beach Energy to sell 60% Artisan interest

[9:09 am] Beach Energy has agreed to sell its 60% operated interest in VIC/L35 (including the Artisan gas discovery) to Amplitude Energy (50%) and OG Otway (10%), unlocking over $500 million of near-term capital for redeployment into higher-return opportunities.

Upfront cash consideration of $70m payable to Beach on completion, with a production royalty of $3.75/GJ nominal payable for 60% of all gas produced prior to 30-Jun-36 up to 62 PJ

Royalty equates to ~$140m in total payments from first gas (expected CY28) through to end FY36, with a top-up payment mechanism if volumes fall short by 30-Jun-36

Implied transaction value of ~$130m after tax or ~$3.50/GJ 2C Contingent Resources, with completion expected in Q1 FY27

Beach has chosen not to proceed with drilling and completing the La Bella 2 development well or pursuing the subsea tie-in to the Otway Gas Plant, redirecting over $500m of capital to more value-accretive opportunities

Company page: Beach Energy (BPT)

Aurum secures environmental approvals for Boundiali Gold Project

[9:06 am] Aurum Resources has received all three EIESA environmental certificates from Côte d'Ivoire's Ministry of Environment.

Three EIESA certificates granted on 20 May 2026 covering all three mining licence applications (BST, BD and BM tenements) across 572.67km², a mandatory pre-condition for mining licence grant under Ivorian law

Approvals follow a 12-month Category A process including a public inquiry and review by the Inter-Ministerial Technical Committee in Abidjan on 7 May 2026

Pre-Feasibility Study expected this quarter with Definitive Feasibility Study scheduled for Q4 CY2026

Company page: Aurum Resources (AUE)

Meeka commences ore development at Judy North

[9:05 am] Meeka Metals has commenced first ore development at Judy North, a new high-grade orebody at its Andy Well underground gold mine in WA, with grades performing in line with the Mineral Resource.

Judy North hosts an initial resource of 96koz at 5.4g/t Au, with no prior development history

Ore development underway on 2 levels with a further 3 levels expected to commence in the June 2026 quarter

Drilling has defined the Judy North resource a further 500m below the current development horizon, with grade expected to improve with depth

Company page: Meeka Metals (MEK)

Coronado divests Logan Mining Complex

[9:02 am] Coronado has agreed to sell its Logan Mining Complex in West Virginia to Phoenix Coal Holdings, though specific terms and sale price remains undisclosed.

Sale consideration is nominal cash (after working capital adjustments) with the purchaser assuming certain liabilities

Transaction expected to be free cash flow positive through the elimination of ongoing holding costs and future obligations

Logan Mining Complex comprises coal mining properties, leases, permits and related infrastructure including a preparation plant and loadout facility across Boone, Logan and Wyoming Counties

Interim CEO Gerry Spindler said the deal "transfers future obligations associated with Logan while enabling us to prioritise capital and operational focus elsewhere"

Company page: Coronado Global Resources (CRN)

Bain Capital to sell Estia Health to Stonepeak for ~$2.5bn

[9:00 am] Bain Capital has agreed terms to sell aged care operator Estia Health to US-based Stonepeak for circa $2.5 billion, the AFR reports.

Sale price of ~$2.5bn marks a significant return for Bain in under three years, after taking Estia off the ASX for $838m in 2023 when the sector was working through aged care royal commission fallout

Estia is Australia's No. 2 aged care operator with 94 homes and 9,250 places, generating $1.3bn revenue and $176m adjusted earnings in CY25, up from $765m and $116m in FY23

Under Bain's ownership the business completed seven bolt-on acquisitions (adding 24 homes), lifted occupancy to 93% (vs 89% for rivals) and grew accommodation prices an average of 12% since January 2025

The dual-track auction also attracted ASX-listed Regis Healthcare and PEP's Opal, with Estia having been one of the few compelling billion-dollar IPO candidates with a turnaround story

Source: AFR

Challenger CEO sells 120,000 shares

[8:54 am] Challenger CEO Nick Hamilton has disclosed an on-market sale of 120,000 shares via an Appendix 3Y filing, reducing his beneficial holding by ~15% to 666,000 shares. The sale comes after a volatile run for the stock, which fell as much as ~22% from January to April before rallying back to breakeven for the year.

Company page: Challenger (CGF)

Fed slightly favoured to hike by year-end

[8:53 am] The likelihood of a 25 bp hike by year-end is tracking ahead of a hold, according to CME's Fedwatch Tool.

Source: CME Fedwatch Tool

Waller's hawkish pivot reinforces Fed's higher-for-longer stance

[8:52 am] Fed Governor Waller delivered notably more hawkish remarks in a Germany lecture, marking a continued evolution from his previously dovish posture and backing the removal of the easing bias from the FOMC statement.

Waller said "inflation is not headed in the right direction" and flagged uncertainty over energy prices given the ongoing Middle East conflict, supporting the removal of the easing bias from policy language (a view shared by "many" policymakers at the 28-29 April FOMC meeting)

Said he doesn't think the Fed should be considering rate hikes in the near future as a hike amid still-restrictive policy could cause damage, but voiced concern that inflation expectations could become unanchored if high inflation readings persist

Flagged he would need to see either improvement on inflation or significant labor-market deterioration before considering rate cuts

Marks a notable shift from Waller's previously dovish stance, having argued in December that policy was 50-100bp above neutral, dissented in favour of a 25bp cut on 18-Feb, and said as recently as 20-Mar that rate cuts could be appropriate this year

US consumer sentiment hits fresh record low

[8:49 am] Final May US consumer sentiment slid to a new record low as Strait of Hormuz disruptions drove petrol prices higher, though hard spending data and corporate commentary continue to paint a more resilient picture.

Final May consumer sentiment came in at 44.8 vs 48.2 ests, marking a third straight monthly decline to a new record low just below the prior Jun-22 trough

Year-ahead inflation expectations inched up to 4.8% from 4.7%, while long-run inflation expectations climbed to 3.9% from 3.5%

Cost of living remained the key concern with 57% of consumers saying high prices were hurting their finances (up from 50% last month), with lower-income and non-college consumers seeing particularly sharp sentiment declines

UK retail sales post worst drop in nearly a year

[8:48 am] UK retail sales fell at their fastest pace in nearly a year as the Iran war drove consumers to conserve fuel and pull back on discretionary spending, adding to evidence the conflict is weighing on growth.

Retail sales volumes down 1.3% vs 0.6% decline ests and a revised +0.6% prior month, the steepest fall since May 2025

Motor fuel sales down 10%, the largest monthly fall since November 2020, as drivers conserved fuel after stocking up in March

Retail sales ex-autofuel down 0.4% with declines across all categories apart from food, and clothing stores posting their worst performance since June last year

Source: Bloomberg

Bullish and bearish focus points for the week

[8:45 am] Here's a scan of the key positive and negative catalysts shaping market sentiment heading into this week, with AI momentum and consumer resilience offset by structural bond market concerns and elevated positioning.

Bullish points:

Nvidia delivered another beat and raise with CPU quantification ($20bn standalone CPU revenue in 2026, $200bn TAM), frontier LLM share gains and improved visibility on upside to $1tn 2025-27 Blackwell and Rubin guidance

Broader AI thematic strong with Anthropic revenue expected to more than double in Q2 (first operating profit), expanded Anthropic-SpaceX compute deal

US-Iran diplomatic traction building with Trump putting planned attack on hold for negotiations, both sides flagging "final stages" and gaps narrowing

Strait of Hormuz seeing increased flow with two Chinese tankers (4M barrels), a South Korean tanker (2M barrels) transiting, and IRGC coordinating 26 vessels in 24 hours

Consumer resilience reinforced by Visa and MasterCard commentary, with MasterCard pointing to global unemployment near historic lows underpinning spending strength

Positioning supportive with Goldman Sachs flagging hedge fund short exposure at a 10-year high (squeeze risk) and AAII bull-bear spread deteriorating to -11.9% from +2.7%

Bearish points:

Global bond yield backup intensifying with US 10-year breaking above 4.5% and 30-year hitting 5.18%, highest since 2007, with drivers (inflation, fiscal, geopolitical, populism) looking increasingly structural

Goldman Sachs flagged the two-month correlation between US equities and 10-year yields is most negative since late 1990s, with BCA noting bear markets in US bonds historically don't end without major economic or market turmoil

Warsh scrutiny rising on lack of evidence AI is driving disinflationary productivity gains, with BofA noting yields up ~50bp on average three months after a new Fed chair term begins

Flash PMI data showed input costs at highest since late 2022 and selling price inflation highest since August 2022, with precautionary stock building from Middle East conflict flagged as unsustainable

April FOMC minutes leaned hawkish with "a majority" seeing policy firming as appropriate if inflation runs above 2%, and "vast majority" flagging greater risk inflation takes longer to return to target

May BofA Global Fund Manager Survey triggered a contrarian sell signal with cash dropping to 3.9% from 4.3% (biggest monthly drop since February 2024), and the firm's Bull & Bear Indicator also flashing sell

US-Iran Hormuz deal teeters on collapse

[8:42 am] The US-Iran peace deal remains as volatile as ever, with both sides walking back commitments and Trump appearing to abandon negotiations under domestic pressure.

Sources close to Trump's negotiation team say he is backing away from the deal under "extreme internal pressure from Israel and its US domestic allies", subsequently posting a Mark 84 bomb image on Truth Social with his "Thank you for your attention to this matter" catchphrase

Iran warns the agreement "will be completely cancelled" due to US obstruction on releasing Iran's $100bn of frozen assets, with the US now trying to link asset release to nuclear concessions which Iran rejects, per Tasnim

The White House is conceding the deal "could still fall apart", with Trump walking back from "deal coming shortly" to "time is on our side" and stating the blockade "will remain in full force"

Per Fars News, the leaked MoU contains no Iranian commitments on nuclear stockpiles, equipment removal, facility shutdowns, or weapons development, with all nuclear issues deferred to a 60-day post-signing negotiation period

Iran's preconditions to even start that 60-day window include $100bn in asset release, lifting the blockade and all oil sanctions, $270bn in war reparations, and Hormuz under "full permanent sovereign Iranian management and authority"

Bond markets brace for structural inflation era

[8:37 am] G7 long-term yields hit a two-decade high as investors increasingly believe the post-Covid inflation spike combined with the Iran war signals a structurally more inflationary regime, with central banks losing the battle to keep expectations anchored.

G7 sovereign long-term yields climbed above their post-Covid peak, with the $50tn-plus market signalling investors want compensation for sticky inflation risk and expect central banks to hike further to contain it

Bloomberg Economics estimates the AI-driven data centre buildout will add 0.4% to US headline inflation, peaking February next year, with JPMorgan noting "the tech sector boom is contributing" to broader upward price pressure beyond energy

Citigroup's Nathan Sheets says AI represents an "enormous positive supply shock" that should reduce inflationary pressures over a several-year period as productive capacity expands, and breakeven inflation measures aren't showing a major jump

Source: Blooomberg

US equities cap eighth straight weekly gain

[8:35 am] US stocks finished higher last Friday with the S&P 500 logging its longest weekly winning streak since 2023, though bond market pressures and structural concerns are mounting.

S&P 500 capped eighth straight weekly gain (longest streak since 2023) and sits ~0.3% below its record close

US weekly performance: Dow +2.13%, S&P +0.88%, Nasdaq +0.45%, Russell 2000 +2.72%

Treasury yields mixed on hawkish Waller comments and rising inflation expectations

May final US consumer sentiment marked down to 44.8 from 48.2 (fresh record low), with one-year inflation expectations up 0.3pp to 4.8% and longer-run up 0.5pp to 3.9%

AI compute demand remains key bullish theme after Nvidia beat and raise

Fed funds pricing now anticipates more than 22 bp of hikes through year-end, a ~60% likelihood of a hike at the October meeting

Good morning!

[8:28 am] ASX 200 futures are down 58 pts (-0.67%) as of 8:30 am AEST.

The overnight session in a nutshell:

S&P 500 closes higher for a third straight session and notches an eighth weekly gain, sitting just 0.3% off its 14-May record high

Fed's Waller turns hawkish, says "inflation is not headed in the right direction" and backs removing the easing bias from policy language, pressuring short-term yields

US consumer confidence collapses to a record low 44.8 (vs 48.2 expected), year-ahead inflation expectations jump to 4.8% as cost-of-living concerns deepen

Brent opens the Monday session ~5% lower and below US$100 a barrel as markets react to a potential US-Iran peace deal