ASX 200 Live Today - Monday, 16th February

The S&P/ASX 200 is set to bounce after experiencing a sharp pullback on Friday. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Monday, February 16. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 higher as broader gains offset bank and miner weakness

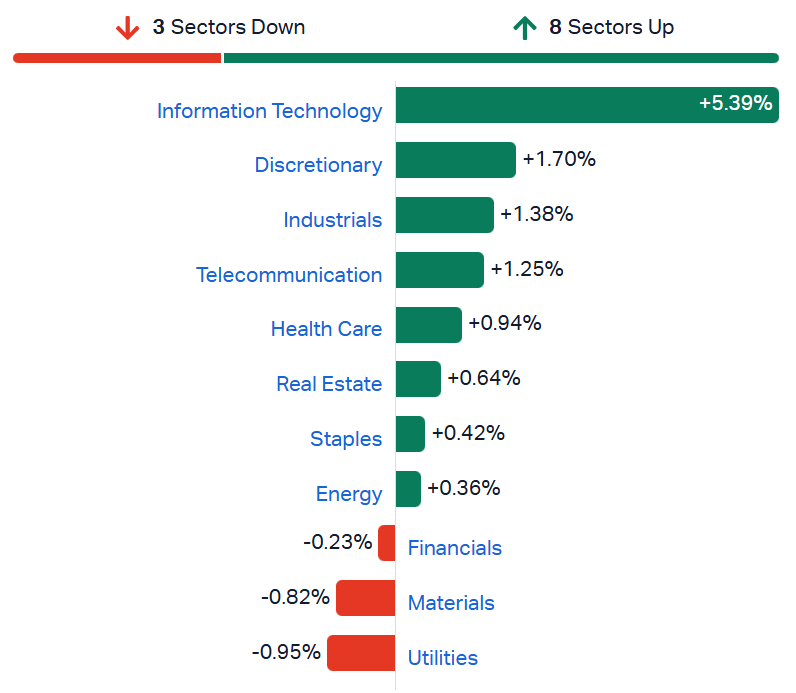

[2:30 pm] The S&P/ASX 200 is trading 0.27% higher, following a sharp 1.39% selloff last Friday, where sectors including Energy, Materials, Discretionary, Healthcare and Tech all dipped more than 2%.

We're seeing a bit of strength today, in-line with the broad rally on Wall Street overnight. Eight out of 11 sectors are trading higher, while 146 S&P/ASX 200 constituents (73%) are in positive territory. There's been a slight pullback for Utilities after a strong run up (XUJ up 9% in three sessions), some volatility among miners and Banks trading slightly lower after experiencing a 6% rallying between 11-12 Feb.

Overall, a bit dicey at the index level as overbought/extended` sectors take a breather. Though some encouraging results from JB Hi-Fi and Aurizon today. Tech is experiencing a sizeable bounce, though a lot more work is needed to establish a clear low.

S&P/ASX 200 sectors (Source: Market Index)

That's all for today. I'll catch you all tomorrow.

JB Hi-Fi 1H26 earnings call highlights

[1:30 pm] JB Hi-Fi is trading 6.8% higher after a volatile open (shares dipped as much as 5.7% within the first four minutes of trade). The result was relatively in-line with market expectations, though margins and the trading outlook may have been viewed as pockets of weakness.

January sales moderated post-promotional period but two-year growth remains robust: Value-seeking customers drove promotional outperformance, CODB rose slightly above sales due to wage and IT investments, though workforce flexibility allows cost adjustment if needed.

Gross margin held steady at 22% with no compression expected from PC price increases: Strong execution, supplier scale leverage, and in-store attachment strategies supporting margins, PC category faces ~20% supplier-driven price increases from March, but product range adjustments aim to maintain customer price points without margin impact.

The Good Guys continues gaining market share in core appliances:

Value positioning and strong execution during key periods driving share gains; traditional multichannel retailers remain primary competition with no significant change in Amazon's competitive stance.

Long-term focus on multichannel capabilities and product cycle tailwinds: e&s foundational investments continuing for at least 12 months with significant returns expected PC and mobile phone replacement cycles providing multi-year sales tailwind, while dividend payout ratio set at 70-80% of NPAT from FY26 onwards.

Aurizon 1H26 earnings call highlights

[1:27 pm] Aurizon is trading 6.1% higher after reporting a solid 1H26 result and sizeable dividend surprise. They've just wrapped up the earnings call, and these are the interesting takeaways:

Coal business delivered stronger than expected H1 performance: Demand, yield, and cost performance exceeded expectations, though full year margin normalisation anticipated as first half tailwinds unwind in 2HY26, no material contract losses in CQCN with competitive landscape unchanged.

Containerised freight targeting FY27 breakeven: Volumes rose significantly in H1 FY26 with operational improvements from Kewdale terminal (operational H1 FY27) and Cross River Rail mitigation expected to drive profitability.

Dividend payout increased to 90% reflecting improved confidence:

Higher payout ratio reflects new contracts like BHP Copper, operational enhancements, and stronger business outlook, intended as long term setting barring unforeseen events.

Decarbonisation and efficiency initiatives progressing: Battery electric locomotive trials begin next financial year in WA, ERP upgrade by FY28 and ongoing cost/productivity improvements underway while maintaining capital light growth focus and investment grade credit ratings.

Tech stocks bounce

[12:31 pm] Tech stocks are trading broadly higher, with the S&P/ASX 200 Tech Index up 4.5% at noon.

Despite the bounce, the tech index has barely recouped last Friday's dip and still down ~6% in the past week.

Ticker | Company | % Chg | Price |

|---|---|---|---|

WTC | Wisetech | 9.54% | $46.69 |

XRO | Xero | 6.71% | $78.42 |

BVS | Bravura Solutions | 6.01% | $2.21 |

360 | Life360 | 5.95% | $23.33 |

SDR | Siteminder | 5.78% | $3.66 |

TNE | Technology One | 5.35% | $21.25 |

WBT | Weebit Nano | 4.79% | $5.15 |

CAT | Catapult Sports | 4.37% | $3.47 |

OCL | Objective Corporation | 3.03% | $13.59 |

Japan's GDP growth disappoints

[11:42 am] Japan's Q4 GDP grew just 0.2% year-on-year, well below the 1.6% expected, as weak consumer spending and soft capital investment highlighted the fragility of the recovery despite Prime Minister Takaichi's landslide election victory.

Real GDP up 0.2% annualised in Q4 vs. 1.6% ests, following deep contraction in Q3

Consumer spending up just 0.1%, reflecting household strain from inflation that stayed above the Bank of Japan's 2% target throughout 2025

Net exports provided no contribution to growth despite monthly export increases throughout Q4, as inbound tourism took a hit from plunging Chinese visitor numbers following Beijing's travel warning after Takaichi's Taiwan comments

Results support PM Takaichi's expansionist policies following LDP's biggest post-war single-party election victory, securing two-thirds lower house majority for smooth budget passage

Government plans to expedite discussions on temporarily suspending sales tax on food, with stimulus package passed in December expected to support Q1 2026 economy

Real wages fell every month in 2025 despite nominal pay growth, with wage momentum uneven between large exporters benefiting from weak yen and margin-squeezed smaller companies

Source: Bloomberg

A2 Milk 1H26 earnings call highlights

[11:09 am] A2 Milk is trading sharply higher (+8.0%) after reporting a solid 1H26 beat and guidance. Here are the key takeaways from the earnings call:

Strong momentum across product portfolio with pediatric supplements expansion: Stage 2 and 3 products performed robustly while Stage 1 recovers from supply constraints; entry into China's $8bn pediatric supplements market offers high margins and fragmented competition.

Pokeno acquisition to transform margins and capacity: Transition of a2 Platinum production to Pokeno in H1 FY27 will significantly boost manufacturing capacity and margins beyond FY2026.

Market share gains driving growth amid flat category: Brand consolidation intensifying with top five brands capturing disproportionate share, company targets mid-20% in English label and sees significant runway in both segments despite birth rate declines.

Mid-double digit sales growth maintained with geographic diversification: Full-year guidance reaffirmed across all categories and markets, expansion into Southeast Asia and Middle East underway to diversify beyond core geographies.

Analysts' take on Nick Scali

[11:05 am] Nick Scali suffered a 22% selloff last Friday despite the company delivering a 1H26 result that was broadly ahead of market expectations. The weakness was largely driven by a weaker-than-expected trading update. Here's what analysts are thinking:

JPMorgan retained Overweight, lowered target from $25.50 to $24.10. Strong first half results were offset by a sharp cooling in January momentum, though the UK refurbishment benefits came through and the path to breakeven looked closer than expected.

Canaccord Genuity retained Hold, lowered target from $26.77 to $20.43. Margin performance exceeded expectations and drove the half's results more than sales, while ANZ growth slowed as comparables became tougher and macro signals pointed to more cautious demand ahead.

Analysts' take on Westpac Q1

[10:56 am] Westpac’s Q1 update on Friday, 13 February was modestly ahead of expectations, but the stock fell 2% on the day. Shares had rallied 4.3% into the announcement (11-12 Feb) as investors bid up the sector following CBA’s strong result. Here's what analysts are thinking:

Morgans retained Trim, raised target from $32.20 to $35.12 (up 9.1%).

JPMorgan retained Neutral, raised target from $36.00 to $37.10 (up 3.1%). It noted NII missed by 0.4% and valuation looks full.

Morgan Stanley retained Underweight, raised target from $34.50 to $35.70 (up 3.5%). It argued the 5.6% profit beat was already in the price, with limited margin upside and a stock that looks vulnerable on current multiples.

UBS retained Neutral, target unchanged at $40.00. It highlighted the 5.6% profit beat and 0.5% NIM beat, but said there is still work to do on returns with expectations elevated.

WBC is trading flat at $40.4 this morning. By Warren Masilamony | Company page: (WBC)

Top ASX 200 gainers and losers

[10:47 am] Austal is bouncing after suffering a sharp 22% selloff last Friday, software stocks like Wisetech and Life360 also in the midst of a relief rally. Meanwhile, Nick Scali continues to tumble after missing margin and trading update expectations, iron ore stocks broadly lower, likely due to continued weakness in Chinese property prices (iron ore also back below US$100).

Ticker | Company | % Chg | Price |

|---|---|---|---|

ASB | Austal | 13.96% | $5.55 |

A2M | A2 Milk Company | 8.33% | $9.23 |

WTC | Wisetech Global | 8.21% | $46.12 |

ALK | Alkane Resources | 7.11% | $1.69 |

LNW | Light & Wonder | 5.85% | $146.11 |

360 | Life360 | 5.56% | $23.25 |

GQG | GQG Partners | 5.48% | $1.83 |

XRO | Xero | 5.36% | $77.43 |

AZJ | Aurizon | 5.29% | $3.78 |

WAF | West African Resources | 4.99% | $3.69 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

NCK | Nick Scali | -6.11% | $17.35 |

FMG | Fortescue | -3.16% | $20.54 |

AAI | Alcoa Corporation | -2.82% | $84.14 |

AMP | Ampol | -2.72% | $1.36 |

MEZ | Meridian Energy | -2.65% | $4.78 |

IGO | IGO | -2.63% | $8.16 |

NXT | NextDC | -2.43% | $13.68 |

ANZ | ANZ Group | -2.34% | $39.94 |

CDA | Codan | -2.22% | $33.46 |

RIO | Rio Tinto | -2.05% | $166.26 |

New Hope beats consensus, trims Bengalla capex guidance

[10:20] Q2 saleable coal production and coal sales topped expectations, while FY26 volume guidance was reaffirmed and Bengalla sustaining capex guidance was reduced.

Q2 saleable coal production 2.77Mt vs 2.70Mt (2.6% beat)

Q2 coal sales 2.90Mt vs 2.70Mt (7.4% beat)

Underlying EBITDA $106.9m, in line with the previous quarter

FY26 ROM coal production 15.7-17.7Mt, reaffirmed

FY26 saleable coal production 10.2-11.5Mt, reaffirmed

FY26 coal sales 10.2-11.5Mt, reaffirmed

Bengalla sustaining capex $100-130m vs prior $130-160m (midpoint down ~21%)

NHC is up 0.85% at $4.76. By Warren Masilamony | Company page: (NHC)

Early share price reactions: A2M and Aurizon soar, JB Hi-Fi dumped

[10:10 am] Reporting season volatility ensues, with A2 Milk (+11.5%) opening sharply higher and currently trading slightly above the open price, Aurizon (+6.9%) delivered a massive dividend surprise and trending higher and JB HI-Fi (+0.4%) is all over the place, as a strong 1H26 is likely offset by a mixed trading update. JB rallied as much as 5.6% at the open, and V-shaped its way to a 5.75 dip (yep, all that and the market has only been open for ~11 minutes).

Audinate returns to revenue growth, launches Iris subscription product

[9:57 am] Audinate returned to revenue growth while maintaining 82.6% gross margins and successfully launched its Iris camera control subscription offering in December.

Revenue up ~11% to $32.2m (US$21.1m) vs. $32.7m ests (2% miss)

Underlying EBITDA loss of $2.3m vs. $1.7m loss ests (better-than-expected)

NPAT loss of $10.6m vs. $7.7m loss ests (worse-than-expected)

Gross margin of 82.6% vs. 82.2% prior year, benefiting from product mix shift toward higher-margin software solutions

Secured 66 design wins in H1 (vs. 61 in 1H25) with 516 OEMs now having Dante products in market and additional 207 OEMs developing new Dante-enabled products

Successfully launched Iris usage-based subscription offering in December with 10 camera manufacturers onboarded, extending Dante into intelligent camera control and cloud-enabled video production

Implemented organisational changes expected to deliver approximately $5m in annualised cost savings

FY26 outlook maintained: US dollar gross profit growth of 13-15% with gross margins broadly in line year-on-year

Operating cost growth now expected at 20% over FY25 (down from previous 25% guidance)

Company page: Audinate Group (AD8)

Aurizon beats earnings, lifts dividend guidance and extends buyback

[9:48 am] Aurizon reported a strong beat, driven by higher volumes, regulatory revenue uplift and cost discipline, while increasing full-year dividend guidance by 15% and extending its buyback by $100m.

Revenue up to $2.10bn vs. $2.05bn ests (2% beat)

Underlying EBITDA up 9% to $891m vs. $860.9m ests (4% beat)

Coal EBITDA up $34m to $298m on 1% volume growth and improved revenue yield; Bulk EBITDA up $33m to $117m on 4% volume increase; Network EBITDA up $21m to $516m on track access revenue uplift

Underlying NPAT up to $237m vs. $216.7m ests (9% beat)

EPS up 20% to 13.6 cents driven by higher NPAT and buybacks

Interim dividend of 12.5 cps vs. Morgans ests of 9.7 cps (28% beat)

On-market buyback extended by $100m to total of $250m

Reaffirmed FY underlying EBITDA guidance of $1.68bn vs. $1.71bn ests (2% miss at midpoint)

Full-year dividend guidance increased to 22-23 cents per share from previous 19-20 cents per share (15% upgrade at midpoint)

Aurizon has had a pretty strong run up (up 17% in the past twelve months) but today's result looks like a broad beat, esp at the dividend line.

Company page: Aurizon (AZJ)

JB Hi-Fi beats earnings but cycling big numbers from last year

[9:38 am] JB Hi-Fi reported H1 NPAT of $305.8m, ahead of estimates, with total sales up 7.3% to $6.09bn driven by strong demand for technology products, as the company increased its dividend payout ratio from 65% to 70-80% of NPAT.

Revenue up 7.3% to $6.09bn vs. $6.04bn ests (1% beat)

EBIT up 8.1% to $454.0m vs. $446.2m ests (2% beat)

NPAT up 7.1% to $305.8m vs. $302.6m ests (1% beat)

Gross margin of 21.95% vs. 22.2% ests (25 bps miss)

Interim dividend up 23.5% to $2.10 per share vs. $2.04 ests (3% beat)

JB Hi-Fi Australia total sales up 6.3% to $4.12bn with comparable sales up 5.0%

JB Hi-Fi New Zealand total sales jumped 32.6% to NZ$268.6m with comparable sales up 20.2%

January trading update: JB Hi-Fi Australia total sales up 4.0% (comparable +2.4%), JB Hi-Fi NZ up 26.4% (comparable +16.7%), The Good Guys up 2.7%, e&s down 4.6% (comparable -7.9%)

Board increased dividend payout ratio from 65% to range of 70-80% of NPAT from FY26

A bit of a mixed result, with gross margins below ests and the company cycling some big numbers from the prior corresponding period.

"These will be tough to cycle. Whilst the share price has pulled back over the last 6 months, the 1 year forward PE multiple at 20x is still over 1 standard deviation above its 10 year average and offering low single digit EPS CAGR over the next few years," flagged Morgans analysts.

Company page: JB Hi-Fi (JBH)

Bendigo Bank beats cash earnings on stronger NIM

[9:25 am] Bendigo & Adelaide Bank will join its peers CBA, Westpac and ANZ, all of which have topped market expectations in recent half-year or quarterly updates. The key numbers for the first-half of FY26 include:

Cash NPAT up 3.3% $256.4m vs. $247.8m ests (3% beat)

Net interest income of $871.1m vs. $870.6m ests (in-line)

Net interest margin up 4 bps 1.92% vs. 1.89% ests (3 bps beat)

Dividend per share flat at 30 cps, in-line with ests

Targeting ROE above 10% by 2030 with dividend payout ratio of 60-80% of cash earnings and CET1 ratio above 10%

BAU costs expected no higher than inflation through the cycle, with productivity program to offset increasing amortisation costs

Improved balance sheet growth expected in FY26 with savings growth above system

Residential loan growth to return to at or around system levels in the near term, targeting 5-8 bps of loans through the cycle

Interesting outlook commentary: "While Australian households are challenged with rising cost of living, our home loan customers have shown financial resilience with 45% of mortgage customers over a year ahead on their mortgage repayments, and 88% maintaining their financial buffers."

Company page: Bendigo and Adelaide Bank (BEN)

Treasury Wine 1H26: No surprises

[9:18 am] Treasury Wine's results should contain no surprises as the company already announced plans to suspend its dividend late last year, and provided FY26 EBITs guidance last week. TWE shares continue to trade around recent lows of ~$5.20, which marks the lowest price point since October 2015.

Net sales revenue (NSR) of $1.30bn vs. $1.23bn ests (6% beat)

EBIT ex-items down 39.6% to $236.4m, in line with $225-235m preliminary guidance

NPAT ex-items down 46.3% to $128.5m vs. $124.1m ests (4% beat)

Statutory NPAT loss of $649.4m, reflecting $751.0m post-tax material items from non-cash impairment of US-based assets

Interim dividend suspended as temporary measure to prioritise capital preservation and reduce leverage

Performance impacted by adverse category trends in US and China, shipment restrictions contributing to parallel import activity in China, and cycling prior year shipments

Reached agreement with RNDC regarding California distribution closure during 2025, including settlement compensation

Company page: Treasury Wine Estates (TWE)

Australian Clinical Labs misses revenue, cuts FY guidance on market headwinds

[9:10 am] Australian Clinical Labs reported below-average market growth, prompting the company to downgrade full-year revenue and EBIT guidance despite margin expansion initiatives.

Revenue down 1.0% to $365.4m vs. $378.5m ests (3% miss)

Impacted by below-average market growth and portfolio optimisation of commercial contracts

Underlying EBIT up 2.4% to $28.0m vs. $27.4m ests (2% beat)

Margins expanding 30bps on closure of loss-making ACCs and productivity improvements

Underlying NPAT up 8.9% to $13.2m vs. $14.5m ests (9% miss)

Interim dividend up 7% to 3.75 cps

MBS outlays contracted 1.4% vs. market growth of 1.8%, but adjusted MBS outlays up 1.3% excluding unprofitable ACC closures

Underlying EPS up 12.8% to 6.7 cents per share on improved profitability and buybacks (bought back 3.6m shares in first half

CEO Melinda McGrath flagged broad challenges for both the reporting period and guidance, including a 3.5% increase in wages and 0.5% increase to superannuation on 1 July 2025, broader inflationary pressures and challenging external environment.

FY26 revenue guidance cut to $735-745m from $760-780m and vs. $765.8m ests (3% miss at midpoint)

FY26 underlying EBIT guidance lowered to $66-69m from $67-73m and vs. $68.0m ests (in-line at midpoint)

FY27 outlook: EBIT of at least $8m

Company page: Australian Clinical Labs (ACL)

Genesis to acquire Magnetic in $639m deal

[9:07 am] Genesis Minerals has agreed to acquire Magnetic Resources in a cash and scrip scheme, adding a 2.2Moz high grade resource near its Laverton mill and strengthening its medium term production pipeline.

Binding Scheme Implementation Deed to acquire 100% of Magnetic via Scheme of Arrangement, implying equity value of ~$639m at $2.00 per share

This represents a 25% premium to Magnetic's $1.60 close last Friday

Consideration of $1.40 cash plus 0.0873 Genesis shares per Magnetic share, equating to ~70% cash and 30% scrip, with option for all cash or all scrip subject to scale back

Lady Julie Gold Project hosts ~2.2Moz at 1.8g/t Au, located ~20km from Genesis’ 3Mtpa Laverton mill, providing a clear pathway for incremental open pit and underground feed

Company page: Genesis Minerals (GMD)

Ansell beats earnings on tariff pricing and cost synergies, reaffirms guidance

[9:04 am] Ansell's first half was ahead of estimates, with EBIT margin expanding 180 bps to 14.3% on increased KBU synergies and lower freight costs, while reaffirming FY guidance despite US$80m annualised tariff headwinds.

Revenue down 0.6% US$1.03bn vs. US$1.09bn ests (6% miss)

EBIT margin improved 180 bps to 14.3%

Adjusted NPAT of US$95.7m vs. US$89.9m ests (6% beat)

Adjusted EPS up 19.0% to US$0.663 vs. US$0.63 ests (5% beat)

Interim dividend US$0.266 vs. US$0.26 ests (2% beat)

All tariff-related price increases now activated, offsetting annualised tariff cost of ~US$80m, though negative demand effects observed in automotive manufacturing and Mexico

Reaffirmed FY EPS guidance of US$1.37-1.49 vs. US$1.42 ests, expects organic constant currency sales growth in second half with increased KBU net cost synergies reaching ~US$12m for full year

Company page: Ansell (ANN)

BlueScope earnings beat on stronger US spreads

[9:00 am] BlueScope earnings topped analyst expectations on stronger US spreads, higher volumes across key markets and solid cost performance, while second half guidance slightly missed estimates.

Revenue of $8.22bn vs. $8.37bn ests (2% miss)

Underlying EBIT of $557.5m vs. $557.8m ests (in-line)

Underlying NPAT up to $382.0m vs. $349.8m ests (9% beat)

Interim dividend up 117% to 65 cps

Second half underlying EBIT guidance of $620-700m vs. $720.2m ests (14% miss at midpoint)

It'll be interesting to see how BSL trades. The stock closed at $29.16 on Friday, which is relatively in-line to the offer price it received from SGH and US-based Steel Dynamics ($30 per share) earlier this year.

Company page: BlueScope Steel (BSL)

A2 Milk smashes earnings expectations

[8:55 am] A2 Milk delivered a strong first half and upgraded full-year guidance to mid double-digit revenue growth. NZX-listed A2 shares are currently up 9.6%.

Revenue up 18.8% to NZ$993.5m vs. NZ$969.2m ests (3% beat)

EBITDA up 18.4% to NZ$155.0m vs. NZ$148.8m ests (4% beat)

Underlying NPAT up 19.6% to NZ$122.6m vs. NZ$87.7m ests (40% beat)

Interim dividend NZ$0.115 vs. NZ$0.10 ests (15% beat)

Represents ~74% NPAT payout, with record date 20 March

Infant Milk Formula revenue up 13.6% with English label IMF up 20.9% and China label IMF up 6.5% to record market share

Underlying EBITDA margin up 90 bps to 16.6%

Closing cash of NZ$896.9m

FY26 revenue guidance upgraded from low double-digit to mid double-digit growth and EBITDA margin expected at 15.5-16.0% (vs. Citi ests of 15.2% and 15.7% consensus).

Company page: a2 Milk Company (A2M)

S&P 500 earnings growth accelerates to 13.2% in Q4, beating expectations

[8:46 am] With 74% of S&P 500 companies reported, Q4 earnings growth has reached 13.2%, well above the 8.3% expected at quarter-end, according to FactSet.

Blended earnings growth of 13.2% vs. 8.3% expected at end of quarter

74% of companies beat EPS estimates, below the 79% one-year average and 78% five-year average

73% surpassed revenue estimates, above the 71% one-year average but in line with the 70% five-year average

Companies reporting earnings 7.2% above expectations, slightly below the 7.4% one-year average and 7.7% five-year average

Revenue surprises of 1.6% above estimates, better than the 1.3% one-year average but below the 2.0% five-year average

China's new home prices fall 3.1% as property slump deepens

[8:45 am] China's new home prices dropped 3.1% year-on-year in January, the steepest decline in seven months, as the property sector's prolonged downturn continues despite government support measures since the 2021 crisis.

New home prices fell 0.4% month-on-month, matching December's decline

Annual fall of 3.1% accelerated from December's 2.7% drop

62 of 70 cities surveyed posted price declines, up from 58 in the previous month, signaling broadening weakness across markets

Resale market remained particularly weak with prices down 7.6% year-on-year in tier-one cities and over 6% in smaller cities

Heavy inventories in third-tier cities and weak demand remain unresolved, with analysts warning full improvement in market expectations will take time

Source: Reuters

US inflation cools to 10-month low, easing Fed pressure

[8:39 am] US January CPI came in slightly cooler-than-expected with headline inflation falling to 2.4%, the lowest since April 2025, while core CPI held at 2.5% annually, providing relief after concerns about potential upside risks.

Headline CPI up 0.2% month-on-month vs. 0.3% ests, down from December's 0.3%

Core CPI up 0.3% month-on-month vs. 0.3% ests, down from December's 0.2%

Annual headline inflation at 2.4% vs. 2.5% ests, the lowest reading since April 2025

Annual core CPI at 2.5% vs. 2.5% ests, down from December's 2.6%

Shelter index rose 0.2% (down from 0.4% in December) but remained the biggest contributor to monthly headline increase, while core goods stayed flat for second consecutive month

Price pressures eased across energy, used vehicles, food and medical care, but inflation persisted in airline fares, appliances, furniture and new vehicles

Markets now pricing ~70% odds of a June Fed rate cut (up from earlier expectations) and ~30% for April, after last week's stronger-than-expected jobs report had pushed easing expectations further out

AI disruption fears double as earnings calls reveal mounting concern

[8:39 am] Mentions of AI disruption on management calls nearly doubled quarter-on-quarter, sparking indiscriminate selling despite S&P 500 companies posting 12% earnings growth in Q4, well above the 8.4% expected.

CBRE shares plunged 20% over two days after CEO suggested AI could reduce long-term office space demand, despite beating earnings expectations

UBS baskets of AI-vulnerable stocks have crashed 40-50% over the past year, with short interest surging above 5% of free float (up from 2% two years ago) for European names like Randstad, Ubisoft, Adecco and WPP

More than 75% of S&P 500 companies reported positive earnings surprises, above average, yet the index has traded rangebound between 6,500-7,000 since early September

Capital spending by the big five tech companies (Amazon, Alphabet, Meta, Microsoft, Oracle) jumped 72% in 2025 and is expected to surge another 63% in 2026

Asian markets hit fresh record highs driven by AI infrastructure plays like TSMC and SK Hynix, while US and European digital businesses face mounting pressure from both investors and short sellers

Source: Bloomberg

EM currencies more stable than G7 peers for nearly 200 days

[8:38 am] Emerging-market currencies are experiencing unprecedented stability compared to developed-market peers, with JPMorgan volatility indexes showing lower swings for nearly 200 consecutive days.

Developing nations' currencies have been less volatile than G7 peers for almost 200 straight days, the longest stretch since 2008, nearing a record dating back to 2000 (208 days)

A Bloomberg index of eight EM currencies has risen 2.8% year-to-date, following a 17.5% gain last year, driven by weaker US dollar, gradual Fed easing expectations, strong commodity prices and robust capital inflows

Investors have poured money into emerging markets at the fastest pace for this period since 2019, with the carry trade thriving in the controlled volatility environment

Developed-market currencies face heightened turbulence from Trump tariff threats, Fed uncertainty and yen volatility concerns, prompting investors to favour less volatile EM currencies like the Singapore dollar, baht and yuan

Source: Bloomberg

AI's paradox: Disruption fears clash with doubts over Big Tech returns

[8:35 am] Investors are caught between fears AI will disrupt entire industries and skepticism that Big Tech's massive spending will deliver returns, wiping over $1.5 trillion from major tech stocks.

Microsoft, Amazon, Meta and Alphabet expected to spend over $600bn on capex in 2026, consuming nearly 100% of their operating cash flow versus a 10-year average of 40%

Microsoft and Amazon shares down more than 16% since late January earnings, with Amazon in its longest losing streak in roughly 20 years; Meta off 13% and Alphabet down 11% from recent peaks

Stocks across industries hammered as AI tools from Anthropic, OpenAI and startups threaten disruption in legal services, financial research, insurance, wealth management and logistics sectors

UBS downgraded tech stocks to neutral, warning the spending pace is unsustainable and increasingly funded by external debt rather than internal cash generation

Market volatility expected to persist as investors demand clearer timeline on when AI investments will generate commensurate revenue growth

Source: Bloomberg

Defensives and cyclicals kick into high gear

[8:23 am] The S&P 500 may have finished relatively flat last Friday, but there's a clear and ongoing rotation into defensive pockets of the market.

Communication Services (-0.76%) and Tech (-0.52%) underperformed as Big Tech continued to struggle for upside, with notable declines from Apple (-2.2%) and Nvidia (-2.2%).

On the flip side, sectors like Utilities (+2.69%), Real Estate (+1.48%), Materials (+1.1%) and Healthcare (+1.01%) all traded broadly higher.

S&P 500 heatmap (Source: TradingView)

A busy day for first-half FY26 reporters

[8:17 am] The corporate calendar is pretty stacked today, with notable reporters including: A2 Milk (A2M), Ansell (ANN), Audinate Group (AD8), Aurizon Holdings (AZJ), Australian Clinical Labs (ACL), Bendigo & Adelaide Bank (BEN), BlueScope Steel (BSL), EVT (EVT), Fiducian Group (FID), GWA Group (GWA), JB Hi-Fi (JBH), oOh!media (OML) and Treasury Wine Estates (TWE). I'll try cover as many results as possible before market open.

Good morning!

[8:16 am] ASX 200 futures are up 51 pts (+0.51%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks flattish after giving up early gains – S&P 500 (+0.05%), Dow (+0.10%), Nasdaq (-0.22%) and Russell 2000 (+1.18%)

Equal-weight S&P 500 (+1.04%) continues to outperform by a wide margin, driven by strength in cyclicals, defensives and small caps

US January CPI came in slightly cooler-than-expected amid deceleration in shelter, energy and used cars

To catch up on all overnight developments, check out today's Morning Wrap.