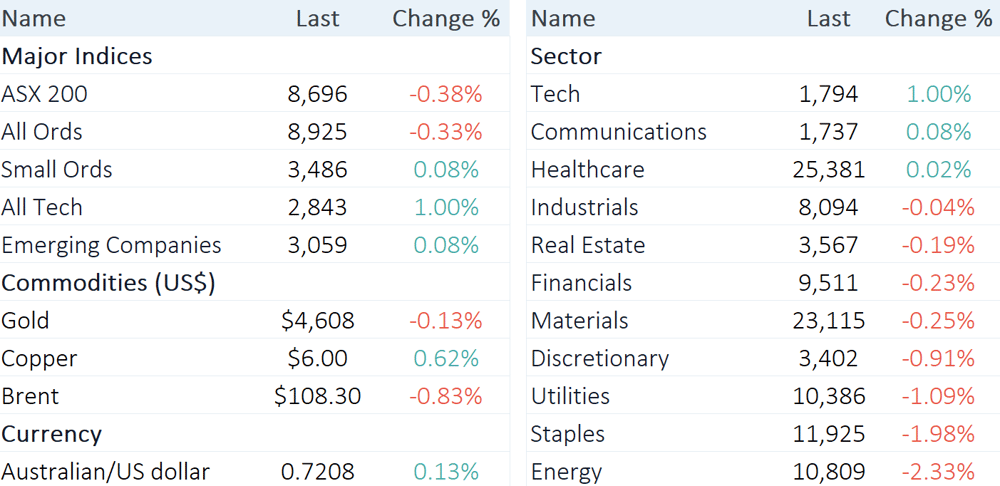

Markets at Midday: ASX 200 lower, Tech stocks buck the trend, Endeavour and A2 weigh on Staples

The S&P/ASX 200 is trading 33 pts lower (-0.38%) at noon.

Source: Market Index

The S&P/ASX 200 is trading 33 pts lower (-0.38%) at noon.

The market is back on the backfoot, despite Friday's more positive finish that snapped an eight-day losing streak. Today's session shows broad-based weakness, with most sectors trading lower and only Tech drawing support from Wall Street's record-setting session. Even Tech is struggling to hold its gains though, up just ~1% after touching session highs of 2.45%. Weighing on the index is the ongoing run of negative corporate updates and earnings downgrades, including:

Endeavour Group (-3.2%) Q3 update flagging a deceleration in sales growth, softening hotels momentum, and additional fuel and freight costs

A2 Milk (-11.5%) tumbled almost 20% in early trade after recalling three batches (~63k tins) of its US-label a2 Platinum infant formula after cereulide was detected

NAB (-1.5%) dipped as much as 4.0% after its 1H26 result flagged weaker-than-expected revenues, along with higher credit impairments and deteriorating asset quality

Let’s dive in

Midday market summary

Data as at 12:45 pm AEST (Source: Market Index)

Today’s big story: NAB and Endeavour

NAB and Endeavour join the growing list of large cap companies that have issued weaker-than-expected earnings or downgraded guidances in recent weeks.

Endeavour delivered some sales growth in Q3, but underlying momentum is deteriorating amid cost-of-living pressures, poor consumer confidence and additional costs arising from the Middle East conflict. The key highlights from the result include:

Q3 FY26 sales growth of 2.9% for Retail and 3.7% for Hotels but boosted by Easter timing falling in Q3 this year vs. Q4 in pcp

FY26 half-to-date sales growth (16-week vs. 16-week, both including Easter and ANZAC Day) of 0.7% for Retail and 3.7% for Hotels (this marks a slowdown vs. the prior first seven weeks of 2H26, which was 1.3% for Retail and 4.5% for hotels)

Hotels momentum softened in March, with March-April growth of just 1.5% vs. pcp despite a record ANZAC Day, reflecting weakness across food, bar, gaming and accommodation

Group proactively building up to $400m of additional inventory vs. pcp to buffer against Middle East-related supply disruption, temporarily impacting leverage via short-term debt facilities

Additional fuel and freight costs in FY26 estimated at $6-$8m, primarily impacting Retail gross margin

NAB's half-year FY26 result read well at face value, with cash earnings up 2.3% half-on-half and well-above consensus and net interest margins up 3 bps to 1.81% (vs. 1.79% ests). But beneath the surface competitive pressures continued to build in mortgages and business lending, asset quality is deteriorating and credit impairments soared 45.6% half-on-half to $706 million.

Last week, the market was hit by poor updates from South32 (massive capex blowout), Woolworths (tempered FY26 guidance), Qantas (cut capacity), Origin (cut Octopus Energy guidance) and more. It's not a good look.

Must read announcements

Accent Group (AX1): Cuts H2 EBIT guidance ~21% at midpoint, flags ASIC investigation into securities trading

Endeavour Group (EDV): Q3 retail growth holds up but hotels momentum softening, launches $100m cost-out program

NAB (NAB): 1H26 cash earnings beat estimates by 7.1%, NIM up 3 bps, interim dividend flat at 85 cps

Capital raisings

AdAlta (1AD): $2.5m placement

AKORA Resources (AKO): Equity raise comprising placement and entitlement offer

American West Metals (AW1): Strategic placement to raise $10m

Athena Resources (AHN): $3.5m capital raising to advance Narryer Project

Australian Mines (AUZ): Strategic placement by internationally renowned fund

Ballymore Resources (BMR): Capital raising of up to $4.7m to accelerate exploration

Breakthrough Minerals (BTM): $5m placement to drive resource growth at NQCG Project

Condor Energy (CND): Raises $2.25m to advance offshore Peru portfolio

Cynata Therapeutics (CYP): Secures commitments for $1.5m placement

Imricor Medical Systems (IMR): Completes $60m capital raise

ImpediMed (IPD): Successful $15.2m capital raise

Navigator Global Investments (NGI): Acquisition and equity raising

Stellar Resources (SRZ): $22.1m placement to advance Heemskirk

Terrain Minerals (TMX): Placement firm bids $1.5m

Vanadium Resources (VR8): US critical minerals development supported by placement

Zimi (ZMM): Placement to raise $1.4m

Thinking out loud: The 'slowdown we have to have'

An interesting note from Morgan Stanley this morning, where the investment bank is cautious on the Australian outlook as tightening policy and the global fuel supply shock combine to force a domestic slowdown, along with tightening monetary and fiscal policy.

Downgraded 2026 GDP growth forecast to 1.2% year-on-year vs. consensus of 1.6% and 2025 actual of 2.6%

Australia is the only region to have restarted a hiking cycle to counter inflation, with harder policy decisions ahead

Inflation pressures (housing, wages, administered prices) likely to persist for at least the next six months, keeping the RBA hawkish to anchor inflation expectations

Fiscal policy now in frame too, with public and corporate pressure building for reform and fiscal consolidation in the upcoming Federal Budget

Australia has felt the energy price shock more than peers (diesel prices up sharply more than Germany, UK, France, Canada, US and NZ on an Apr vs. Feb basis)

Market multiple has already de-rated from 20x to 17x, but Morgan Stanley argues from here the story shifts to earnings risk

Source: Morgan Stanley

Intraday winners and losers

A2 was aggressively bought up this morning, while lithium, rare earth and coal stocks sold off.

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

A2M | A2 Milk Company | 7.15% | $6.59 |

PDN | Paladin Energy | 3.75% | $12.45 |

L1G | L1 Group | 3.75% | $1.16 |

IMD | Imdex | 3.63% | $4.28 |

GLF | Gemlife | 2.83% | $4.73 |

DOW | Downer | 2.43% | $7.58 |

XRO | Xero | 2.18% | $82.77 |

SRL | Sunrise Energy Metals | 2.10% | $12.66 |

DVP | Develop Global | 1.98% | $5.41 |

Data as at 12:53 pm AEST, % change measures the move from today's open price

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

ARU | Arafura Rare Earths | -6.76% | $0.35 |

LTR | Liontown | -6.11% | $2.46 |

LOV | Lovisa | -4.84% | $22.83 |

4DX | 4DMedical | -3.90% | $3.94 |

REG | Regis Healthcare | -3.31% | $6.72 |

EDV | Endeavour Group | -3.11% | $3.28 |

VEA | Viva Energy Group | -2.80% | $2.43 |

OBM | Ora Banda Mining | -2.58% | $1.32 |

YAL | Yancoal Australia | -2.48% | $7.48 |

ELV | Elevra Lithium | -2.44% | $13.22 |

Data as at 12:53 pm AEST, % change measures the move from today's open price

Broker moves

ANZ Group Holdings (ANZ)

Retained at outperform at CLSA; Price Target: $40.30 from $41.20

Retained at hold at Jefferies; Price Target: $33.98 from $34.25

Retained at overweight at JPMorgan; Price Target: $39.00 from $38.50

Retained at neutral at Macquarie; Price Target: $33.50 from $34.00

Upgraded to trim from sell at Morgans; Price Target: $31.85 from $30.72

Upgraded to neutral from sell at UBS; Price Target: $36.50

Coles Group (COL)

Downgraded to neutral from overweight at Jarden; Price Target: $22.60 from $21.60

Retained at buy at Jefferies; Price Target: $25.50

Retained at overweight at JPMorgan; Price Target: $24.00 from $23.50

Retained at buy at UBS; Price Target: $25.50 from $25.00

Lotus Resources (LOT)

Downgraded to neutral from overweight at JPMorgan; Price Target: $0.90 from $1.80

Retained at outperform at Macquarie; Price Target: $1.90 from $2.75

Downgraded to hold from speculative buy at Ord Minnett; Price Target: $1.00 from $3.90

Liontown (LTR)

Downgraded to trim from hold at Morgans; Price Target: $2.20 from $1.80

Qantas Airways (QAN)

Retained at outperform at CLSA; Price Target: $10.09 from $10.74

Retained at overweight at JPMorgan; Price Target: $10.30

Retained at outperform at RBC Capital Markets; Price Target: $10.25 from $10.75