Markets at Midday: ASX 200 down for a sixth straight day, Origin extends selloff

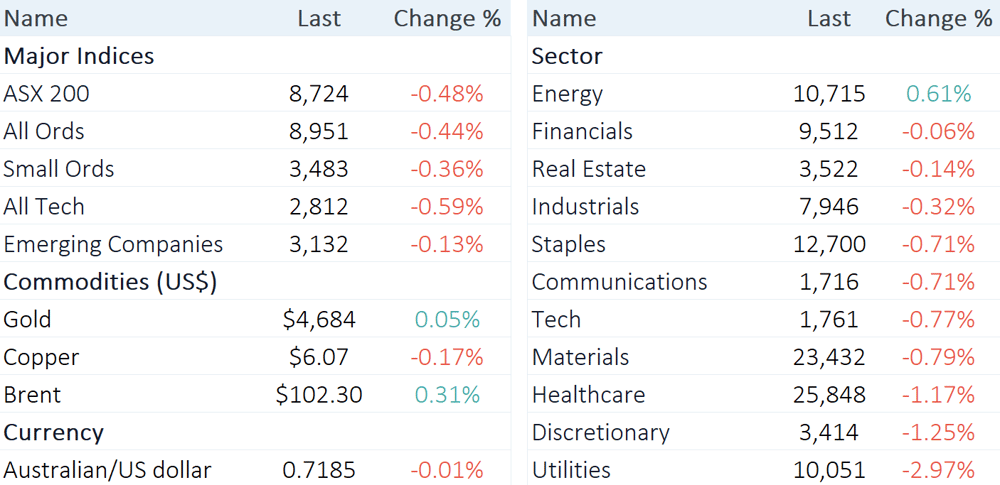

The S&P/ASX 200 is trading 42 pts lower (-0.48%) at noon.

Source: Market Index

The S&P/ASX 200 is trading 42 pts lower (-0.48%) at noon.

Another classic S&P 500 and Nasdaq at all-time highs, while the ASX 200 extends its losing streak to six. It's shaping up to be a heavy day , with all sectors in the red (ex-Energy) and with 129 constituents, or 65%, trading lower. The index is now back at breakeven for the year and hovering just below the key 200-day moving average – typically, not a good sign.

Let’s dive in

Midday market summary

Today’s big story: It's getting grim out there

One of my biggest concerns in recent weeks has been the step up in negative corporate commentary regarding macro uncertainty and Middle East concerns.

It's a pretty long list, but here's the gist of it.

Air NZ (10-Mar): Suspended guidance, shares down 1.1%

Orica (10-Mar): Trading update noted no immediate constraints related to Middle East conflict, shares down 3.4%

Ridley Corp (10-Mar): Investor day noted earnings not expected to be materially impacted by Middle East developments, shares up 0.7%

Orora (9-Apr): Trading update with lower EBIT guidance, shares down 18.0%

Transurban (9-Apr): Q3 traffic update flagged fuel costs, macro uncertainty and geopolitical concerns, shares up 0.2%

a2 Milk (13-Apr): FY26 NPAT guide lowered to "similar to down" with margins impacted by higher air freight costs, shares down 13.0%

Cleanaway (14-Apr): Lowered guidance, shares down 2.6%

Qantas (14-Apr): Update on FY26 outlook amid Middle East conflict, shares down 0.3%

Westpac (14-Apr): Q2 trading update mentioned geopolitical uncertainty, shares down 2.6%

NuFarm (15-Apr): H1 trading update noted supply chains are currently operating largely normally, shares up 11.3%

Virgin Australia (15-Apr): Flagged increase in fuel costs for 2H26 of ~A$30-40m vs prior expectations, shares up 7.2%

Fletcher Build (16-Apr): Q3 sales update noted Middle East impact can't yet be ascertained, shares down 2.4%

NAB (20-Apr): Increased impairment charges for sectors most exposed to geopolitical risks, shares down 3.6%

Qube (20-Apr): Trading update lowered guidance, shares flat

Worley (20-Apr): Update on Middle East impacts, shares down 5.8%

Atlas Arteria (21-Apr): Q1 trading update noted no major effect of rising fuel prices on traffic, shares down 0.9%

Cochlear (22-Apr): Trading update with FY guidance downgrade, shares down 40.7%

EBOS (22-Apr): Lowered guidance, shares down 3.4%

Iress (23-Apr): AGM flagged geopolitics and macro risks, guiding FY26 revenues towards bottom of range, shares down 1.1%

EVT Limited (24-Apr): FY26 update warned of emerging demand weakness, shares down 7.3%

Judo Capital (24-Apr): Q3 update reaffirmed guidance at low end with top-up provision in response to economic conditions, shares up 1.4%

The average stock was trading 7.0% lower since the Iran conflict began (27-Feb to date before the announcement) and fell an average 4.06% on the day of the announcement (though average weighed heavily by Cochlear's 40% one-day decline). The issue here is that these updates span a broad range of sectors, including Financials (WBC, NAB, JDO), healthcare (EBO, COH), industrials (CWY, ORA, WOR, ALX) and more.

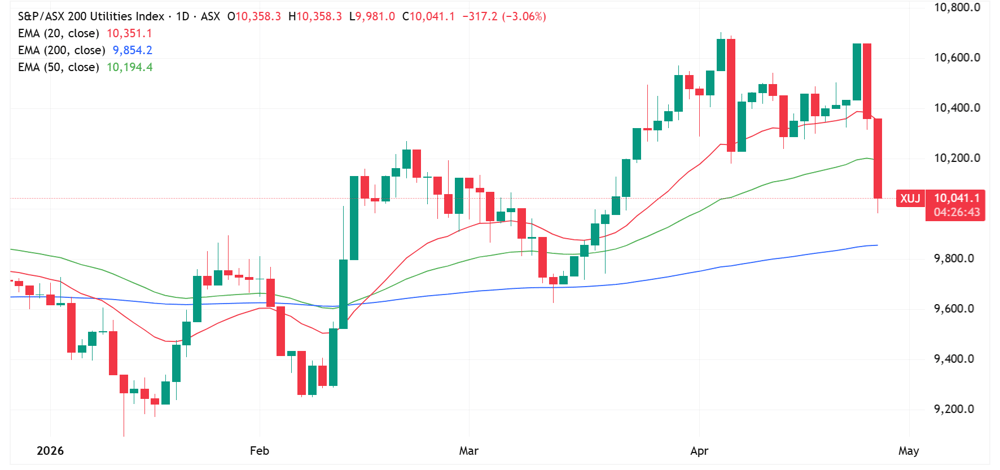

Sector moves: Utilities smashed

The S&P/ASX 200 Utilities sector is now down ~6.1% in the last two sessions, weighed largely by a sharp selloff in Origin Energy.

S&P/ASX 200 Utilities daily price chart (Source: TradingView)

On Monday, Origin released its Q3 result, with mixed signals across the portfolio. The APLNG division performed largely in-line with market expectations, though released pricing was softer-than-expected due to timing and a strong Aussie dollar. Domestic gas volumes and pricing remained pressured by summer demand weakness and competitive short term market conditions. What drove the sharp selloff was a substantial downgrade to Octopus Energy FY26 earnings (from $0-$150m to -$70m to $30m) due to costs associated with UK Energy Company Obligation scheme, higher gas capacity charges, and adverse weather effects. Origin shares tumbled 5.0% on the day, and down a further 5.1% today.

Here's what analysts are thinking:

RBC Capital Markets maintained a Sector Perform rating with a $14.00 target. The broker noted that regulatory cost recovery challenges in the UK led to a guidance downgrade for Octopus, while also highlighting significant hedging losses projected for the FY27–28 periods.

Jarden lowered its price target to $12.75 from $13.00, maintains an Overweight rating. The APLNG revenue miss to the timing of spot LNG cargo sales and the Octopus downgrade might present a valuation opportunity ahead of the Kraken investor briefing.

Citi maintained an Overweight rating and lowered its target from $13.00 to $12.75. Near-term headwinds persist, though the company’s coal exposure for FY27 is largely locked in at prices consistent with current year expectations.

Must read announcements

Beach Energy (BPT): Q3 production misses on weather disruptions, FY26 guidance revised lower

Greatland Resources (GGP): Q3 beats on AISC, eyes upper end of FY26 production guidance

Reliance Worldwide (RWC): Reaffirms FY26 outlook, tariff impact tracking to lower end of range

Whitehaven Coal (WHC): Q3 ROM production broadly in line, tracking upper half of FY26 guidance

Capital raisings

Arrow Minerals (AMD): $2.25m capital raising to advance Yarraloola

Fortifai (FTI): $15m strategic placement

Reach Resources (RR1): Rights issue and shortfall

US1 Critical Minerals (USC): $1m placement led by Snow Lake Energy

Intraday winners and losers

The below tables observe the S&P/ASX 200 stocks with the largest increase/decrease from today's open price.

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

ELV | Elevra Lithium | 5.38% | $13.71 |

JBH | JB Hi-Fi | 3.13% | $77.85 |

DYL | Deep Yellow | 2.85% | $1.99 |

IGO | IGO | 2.17% | $7.53 |

GGP | Greatland Resources | 1.96% | $14.06 |

ZIM | Zimplats | 1.89% | $17.75 |

REH | Reece | 1.86% | $13.71 |

ILU | Iluka Resources | 1.86% | $7.68 |

PLS | PLS Group | 1.84% | $6.10 |

OBM | Ora Banda Mining | 1.78% | $1.55 |

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

ORG | Origin Energy | -4.78% | $11.55 |

LIN | Lindian Resources | -3.33% | $0.87 |

RWC | Reliance Worldwide | -3.18% | $3.20 |

4DX | 4DMedical | -2.81% | $4.85 |

360 | Life360 | -2.54% | $20.37 |

BPT | Beach Energy | -2.50% | $1.17 |

GYG | Guzman Y Gomez | -2.31% | $18.22 |

RSG | Resolute Mining | -2.24% | $1.22 |

CSL | CSL | -2.14% | $128.85 |

TWE | Treasury Wine Estates | -2.13% | $4.36 |

Broker moves

AML3D (AL3)

Retained at buy at Shaw and Partners; Price Target: $0.40

Atlas Arteria (ALX)

Downgraded to negative from neutral at E&P; Price Target: $4.96

Origin Energy (ORG)

Retained at overweight at Jarden; Price Target: $12.75 from $13.00

Retained at sector perform at RBC Capital Markets; Price Target: $14.00

Polymetals Resources (POL)

Initiated at buy at Shaw and Partners; Price Target: $1.62

Webjet Group (WJL)

Downgraded to neutral from buy at Goldman Sachs; Price Target: $0.62 from $0.72