BHP, Fortescue, Rio Tinto or Mineral Resources – Which ASX mining stocks offer the best value?

We leverage the latest research from a major broker to figure out which ASX mining stock currently offers the best value.

Source: Shutterstock, Market Index

Mentioned

KEY POINTS

- Commodity prices play a pivotal role in determining the share prices of our major ASX mining stocks like BHP, Fortescue, Rio Tinto, Mineral Resources, Pilbara Minerals etc.

- But commodity prices are always on the move, as too are the share prices of the companies that produce them. How do current spot commodity prices relate back to the current share prices of major ASX companies?

- We review the latest spot commodity prices versus share prices data from major broking and research house Morgan Stanley to determine which ASX mining companies currently offer the best value to investors.

Aussie investors love their mining stocks – and why not? We have some of the biggest and best in the world. I know many of you who clicked on this article probably already own every stock in the title. But for those who are looking to add one, or perhaps just a couple – and want to know which offers the best value – then this article is for you!

Major broking and research house Morgan Stanley has compiled a list of valuations for major ASX mining stocks, adjusting their models to reflect the latest commodity prices. The exercise is designed to give investors a sense of how much mining stocks might be worth if current market prices for iron ore, copper, coal, lithium and other key resources persist.

This article will investigate how the Morgan Stanley came to its conclusions, and which ASX mining stocks currently look the cheapest – or the most stretched – based on the broker's estimates.

How much are Aussie mining co's worth?

Each week Morgan Stanley runs a simple but powerful exercise: Plug current spot commodity prices into their existing financial models and compare the resulting valuations with consensus forecasts and market prices. By holding all other assumptions steady, this approach isolates the effect of commodity price moves on cash flows and valuations, giving investors a clearer picture of how today’s pricing environment translates into equity value. In doing so, Morgan Stanley provides useful context for how mining stocks might perform if current spot prices were to persist.

Before we discuss the broker’s latest estimates, we must first tackle the definition of discounted cash flow (DCF) analysis. Yes, painfully boring, done by only the most experienced and skilled financial analysts… so, ahem, try to stay awake here…😴

DCF analysis (for beginners) Discounted cash flow analysis is a way of estimating what a company is worth today by forecasting all the cash it is expected to generate in the future, and then “discounting” those amounts back to today’s dollars using a cost of capital. In practice, analysts use assumptions about commodity prices, production volumes, costs, and risks to arrive at a valuation per share.

By comparing Morgan Stanley’s “Spot DCF” (i.e., based on today’s current or "spot" commodity prices) with the current share price, we can see whether the market is pricing a mining stock as cheap, fair, or expensive. Okay, now you’re an expert on DCF analysis 🧐, to the Spot DCF vs Current Price Table!

Morgan Stanley Spot DCF vs Current Price for ASX Mining Stocks (Source: "Spot Base Consensus: 22 Aug 2025", Morgan Stanley, 22 August 2025) (click here for full size image)

{kind=link}

Key takeaways from Morgan Stanley’s Spot DCF vs Current Price analysis:

Cheapest (+10% upside): Mineral Resources (ASX: MIN) stands out with a 49% upside to spot DCF, followed by Whitehaven Coal (ASX: WHC) at 30% and BHP Group (ASX: BHP) (+18%) which also screen as attractively valued against their current vs Spot DCF potential.

Fairly undervalued (0-10% upside): Rio Tinto (ASX: RIO) (+9.6%) only just missed making the cheapest list, as did South32 (ASX: S32) (+9.2%). Fortescue (ASX: FMG) is also modestly attractively valued at +6.9% as is Iluka Resources (ASX: ILU) at 7.7%. Others like Boss Energy (ASX: BOE) (+1.7%) and Deterra Royalties (ASX: DRR) (+0.5%) appear to be roughly fairly valued.

Overvalued/Expensive (<0% upside): Several miners look expensive relative to spot – most notably Paladin Energy (ASX: PDN) (-30%), Sandfire Resources (ASX: SFR) (-29%), IGO (ASX: IGO) (-27%) and Lynas Rare Earths (ASX: LYC) (-9%). Pilbara Minerals (ASX: PLS) (-2.8%) is only just on the wrong side of fair value.

It’s important to remember this is a snapshot in time. Commodity prices move daily, and a mining stock's real value is shaped by more than just the spot curve – operational efficiency, cost control, capital discipline, and management strategy – all play critical roles. Still, Spot DCF analysis like this offers a useful insight into what the market is paying for today’s commodity prices.

Morgan Stanley’s commodity price forecasts

Which begs the question: What are the commodity prices used in Morgan Stanley's Spot DCF analysis? And there's perhaps an even more important question: How might these commodity prices change and therefore impact the share prices of our major mining stocks? 🤔

I'm glad you asked! The other half of the equation is Morgan Stanley’s outlook for the underlying commodities that are critical to mining stock valuations. We’ve all seen what happens when, say, the iron ore is up a few per cent on the day for BHP, RIO, and FMG, or how recent gyrations in the lithium price have moved the dial for MIN, PLS and IGO.

Let’s investigate Morgan Stanley’s latest forecasts for the commodities most important to ASX mining stocks, and how these might impact their valuations if the broker is proved correct.

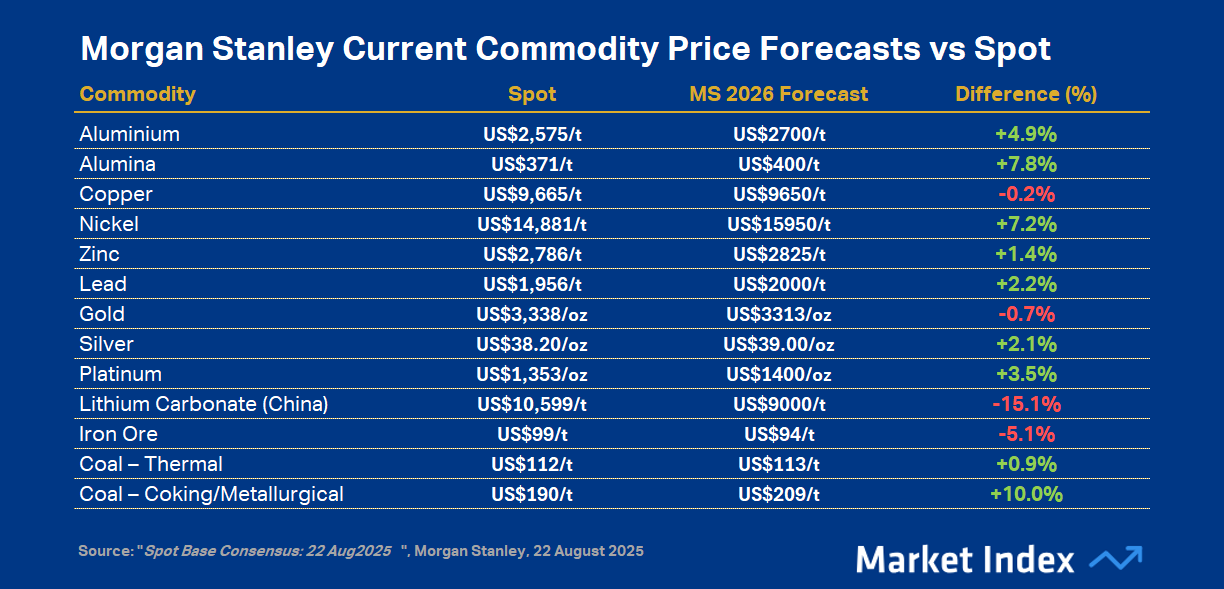

Morgan Stanley Current Commodity Price Forecasts vs Spot (Source: "Spot Base Consensus: 22 Aug 2025", Morgan Stanley, 22 August 2025) (click here for full size image)

{kind=link}

Key takeaways from Morgan Stanley’s Commodity Price Forecasts vs Spot analysis:

Undervalued vs forecasts: Coking coal (+10%), Alumina (+7.8%), Nickel (+7.2%), Aluminium (+4.9%) and Platinum (+3.5%) are trading modestly below Morgan Stanley’s 2026 forecasts, implying upside if prices move toward the broker’s view. This would be supportive for stocks like Whitehaven Coal (Coking Coal), IGO (Nickel), and South32 (Alumina).

At or near fair value: Copper (-0.2%), Zinc (+1.4%), Lead (+2.2%) and Silver (+2.1%) look broadly in line with MS forecasts. You could say that copper majors like BHP, Rio Tinto, and Sandfire Resources have little potential valuation upside from that area of their respective businesses.

Overvalued vs forecasts: Lithium carbonate (-15%) and iron ore (-5.1%) stand out as the two most overvalued commodities in Morgan Stanley’s 2026 view. If the broker is correct, lower prices for these commodities could weigh on lithium names like Pilbara Minerals and Mineral Resources, with the latter suffering a possible double whammy due to its iron ore exposure. A lower iron ore price would likely also drag on the share prices of BHP, Rio Tinto and Fortescue.

Note how Morgan Stanley’s commodities views help explain some of the mismatches in the first table – for instance, why lithium and uranium players are trading above their spot DCF levels. It suggests that the broader market is banking on better long-term commodity prices than Morgan Stanley’s forecasts.

Conclusion: In the eye of the beholder 😍

Valuations in the resources sector are inherently dynamic. As commodity prices shift day by day, and as companies adapt through cost controls, investment decisions and strategic pivots, the true value of a mining stock is constantly in a state of flux.

Morgan Stanley’s Spot DCF framework offers a clear window into how our mining stocks stack up against today’s commodity price landscape. For example, if spot prices fall as the broker expects for lithium and iron ore, current share prices for associated stocks may look stretched, just as if nickel or alumina rally, certain valuations look conservative.

I trust you found this investigation interesting, and we’ll continue to keep you abreast of Morgan Stanley’s latest Spot DCF and commodity forecasts as we receive them. The goal, as always, is to provide you with the very best information and research available to help you make informed decisions about your portfolio.