ASX 200 Live Today - Wednesday, 6th May

The S&P/ASX 200 is up 0.7% in early trade, driven by a strong bounce in banks and REITs. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Wednesday, May 6. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 higher as banks and resources rally

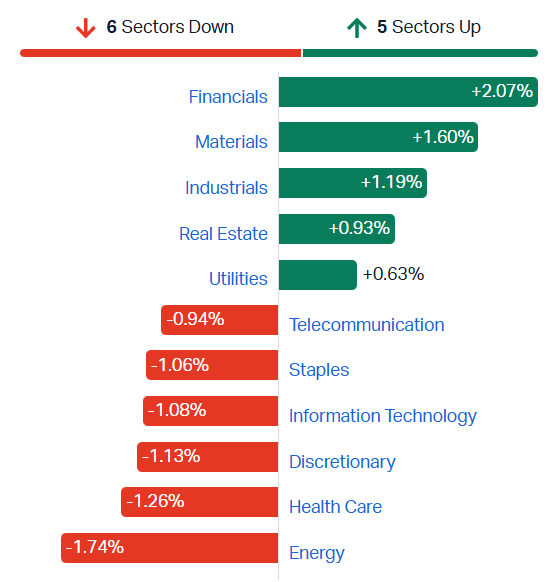

[2:25 pm] A fairly strong but bifurcated session with Financials up a massive 2.0%, along with solid gains for Materials, Industrials and Real Estate, while sectors like Staples, Tech, Discretionary, Energy and Healthcare tank more than 1%. As long as banks and miners rally, I guess that's all that matters at the index level.

ASX 200 sectors (Source: Market Index)

The S&P/ASX 200 is trading 0.98% higher, off session highs of 1.24%. A solid bounce lifting the index above the 200-day and now up 0.60% year-to-date. Overall, a very challenged backdrop for local equities. US markets contine to grind higher off the back insatiable compute demand and AI investments. Q1 S&P 500 earnings have soared 27.1% (as of last Friday) vs. the 12.6% expected at the start of earnings season. This is driving other tech-heavy markets such as South Korea's KOSPI and Taiwan's TWSE to all-time highs as well (KOSPI surged 6.7% today, now up 75% YTD).

Back at home, banks are finally bouncing after falling in ten of the prior eleven sessions. Though fundamentally, their recent trading updates/earnings have all highlighted a massive uplift in provisions and lacklustre earnings growth. The corporate backdrop has become a little more accommodative this week, with a long list of large caps reaffirming guidance at the Macquarie Conference. This compares to the prior 2-3 weeks where we've seen an avalanche of downbeat corporate commentary and earnings downgrades. Today's bounce provides some relief at the index level, though the bifurcation/poor breadth is a cause for concern.

Morgan Stanley take on RBA May hike

[2:06 pm] Morgan Stanley flagged that the RBA's May hike gives the Board space to watch data evolution from here, but stressed that weaker demand is still required to contain inflation pressures.

8-1 vote to hike 25bps to 4.35% was a more decisive response than the prior meeting's 5-4 vote

Governor noted policy is now "a bit" restrictive but with uncertainty given robust credit growth and rising inflation expectations

Updated forecasts: Inflation peaks at 4.8% in Q2 with core inflation above target through to Dec-27, GDP revised down to 1.3% in 2026 and 1.4% in 2027, with unemployment unchanged at 4.3% in 2026 and 1 pp to 4.6% in 2027

RBA assumes the oil price shock will be short-lived, have only a modest demand impact and pass through quickly to underlying price pressures

Bullock's two key messages: Hikes have given the Board "space" to watch responses to both the energy shock and tighter policy, but a growth slowdown is required to prevent cost pressures becoming entrenched in inflation expectations

Morgan Stanley views the press conference as lowering the probability of a fourth consecutive hike at the June meeting, with August more possible but mitigated by domestic growth slowing being more evident in macro data by then

Australian Industry Index rebounds in April but remains deeply negative

[1:27 pm] The Australian Industry Index recovered some ground in April but remained strongly negative at -24.4, with energy crisis impacts continuing to drive sharp input cost increases and margin compression across industries.

The index is based on monthly surveys from a national sample of Australian industrial businesses.

Headline Index rebounded 9.8 points to -24.4, with activity (-31.2), employment (-25.2) and new orders (-24.8) all stabilising slightly but remaining in deep contraction

Manufacturing weakened again in April while construction saw slight recovery, with both struggling under fixed price contracts that constrain fuel cost pass-on

Input prices surged 13.5 points to 69.3 (highest since November 2022), with the widening 46.2 point gap between input and sales prices (23.1)

Rising input costs were the dominant factor for one-third of businesses, with fuel levies on transport services the primary inflation vector, uncertainty (24%), demand (20%) and supply chain (19%) issues also flagged

Energy crisis impacts expected to broaden from fuels and transport to other industrial materials in coming months as oil and gas shortages work through supply chains

Wages continued to rise to 36.2 with workforce pressures from higher fuel and travel costs adding to employment expenses, particularly in regional areas

Source: Australian Industry Index

Mixed day for tech

[1:25 pm] The S&P/ASX 200 Tech Index is down 0.90% despite opening in positive territory. A very strong day for data centres, with DigiCo (+21.2%), Ifratil (+12.1%), NextDC (+1.9%) and Macquarie Telecom (+1.5%) broadly higher, offset by weakness from heavyweights like Life360 (-6.5%), Pro Medicus (-3.9%) and Wisetech (-2.4%).

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

DGT | Digico | 21.2% | $2.86 | -1.4% |

WBT | Weebit Nano | 3.7% | $4.43 | 150.3% |

NXT | NextDC | 1.9% | $14.26 | 10.6% |

HSN | Hansen Technologies | 1.9% | $4.89 | -3.2% |

DDR | Dicker Data | 1.8% | $9.38 | 11.3% |

MP1 | Megaport | 1.8% | $9.13 | -20.0% |

MAQ | Macquarie Technology Group | 1.5% | $71.25 | 14.9% |

PPS | Praemium | 1.0% | $0.68 | -11.5% |

DTL | Data#3 | 0.6% | $8.03 | 7.1% |

AD8 | Audinate Group | 0.4% | $2.40 | -60.0% |

CAT | Catapult Sports | 0.0% | $3.27 | -19.3% |

NXL | Nuix | -0.2% | $1.52 | -36.5% |

CDA | Codan | -0.4% | $39.63 | 145.8% |

SDR | Siteminder | -0.5% | $2.96 | -26.3% |

XRO | Xero | -0.7% | $85.54 | -48.4% |

BVS | Bravura Solutions | -0.9% | $2.21 | 4.7% |

IRE | Iress | -0.9% | $6.60 | -19.8% |

TNE | Technology One | -1.8% | $27.66 | -10.8% |

WTC | Wisetech Global | -2.4% | $44.66 | -50.5% |

OCL | Objective Corporation | -2.6% | $11.36 | -29.5% |

PME | Pro Medicus | -3.9% | $130.91 | -45.0% |

360 | Life360 | -6.5% | $19.72 | -10.4% |

Lithium stocks higher, PMET soars

[1:17 pm] Lithium stocks are trading broadly higher, with a notable 10.2% gain for PMET Resources. The Canadian developer provided an update on Tuesday for its Shaakichiuwaanaan Property in Quebec, with the federal ESIA submission complete and key studies/infrastructure milestones advancing toward FID.

The bellwether PLS Group (+1.1%) is a little flattish today, and has traded mostly sideways since 17 April – likely take a breather after a ~45% YTD run (and up ~430% since Jun-25).

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

PMT | Pmet Resources | 10.2% | $0.72 | 177.7% |

PAT | Patriot Resources | 8.0% | $0.14 | 125.0% |

LTR | Liontown | 6.9% | $2.56 | 405.9% |

IGO | IGO | 6.1% | $8.05 | 104.7% |

WR1 | Winsome Resources | 6.1% | $0.52 | 205.9% |

EUR | European Lithium | 5.6% | $0.48 | 779.6% |

MIN | Mineral Resources | 2.9% | $68.56 | 234.4% |

AGY | Argosy Minerals | 2.8% | $0.07 | 289.5% |

VUL | Vulcan Energy Resources | 2.5% | $3.75 | -0.8% |

GL1 | Global Lithium Resources | 1.7% | $0.59 | 268.8% |

PLS | Pls Group | 1.1% | $6.11 | 312.5% |

CXO | Core Lithium | -1.0% | $0.31 | 332.4% |

DLI | Delta Lithium | -2.0% | $0.24 | 50.0% |

Chinese lithium futures surge

[1:12 pm] Chinese lithium futures currently up 6.8% to 198,560 yuan a tonne, now ~5% above the prior late-January highs of 189,440 yuan. The Chinese market has been closed for the past week for Labour Day.

Samsung joins $1tn club on AI memory chip demand

[12:15 pm] Samsung Electronics has become only the second Asian company to hit a US$1 trillion market cap (after TSMC) as shares more than quadrupled over the past year on booming AI memory chip demand.

Shares rallied as much as 12% on Wednesday, lifting the Kospi above 7,000 for the first time

Samsung's semiconductor arm delivered a 48-fold jump in March quarter profit, with contract prices continuing to climb amid limited supply

Stock trading at just 5.9x one-year forward earnings (down from 14.4x in October) with sell-side targets implying ~30% upside over 12 months

Memory market currently undersupplied, with Samsung flagging 2027 supply-demand tighter than 2026, supporting continued NAND and DRAM price rises

Source: Bloomberg

Banks sharply higher

[12:14 pm] A massive day for banks, with most names up 2-4%. The S&P/ASX 200 Financials Index is trading 2.6% higher but still down 3.3% since its 10-Apr high.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

JDO | Judo Capital | 4.6% | $1.48 | 1.4% |

WBC | Westpac | 4.3% | $39.23 | 21.9% |

NAB | National Australia Bank | 3.4% | $40.27 | 12.3% |

ANZ | Anz Group | 3.2% | $37.10 | 23.5% |

CBA | Commonwealth Bank | 2.9% | $177.89 | 7.1% |

BEN | Bendigo & Adelaide Bank | 1.8% | $10.76 | -5.9% |

MQG | Macquarie Group | 1.7% | $240.95 | 23.6% |

BOQ | Bank Of Queensland | -0.1% | $6.34 | -15.0% |

Analysts cut Universal Store price target

[11:27 am] Universal Store delivered a trading update on Tuesday that was broadly in line with consensus, with FY26 guidance landing at the midpoint of expectations and LFL sales at the core Universal Store and Perfect Stranger banners accelerating through H2 despite a tougher macro backdrop.

The update was viewed as de-risking the near-term outlook, though continued deterioration in the CTC (Thrills) wholesale channel prompted a non-cash intangibles impairment, and FY27 earnings visibility remained the key point of friction with most brokers trimming outer-year estimates and price targets.

Universal shares fell 2.0% on Tuesday and down a further 3.0% today.

Jarden retained Overweight, lowered target from $10.00 to $8.80. US/PS resilience was better than feared given the macro backdrop, though FY27 caution reflects LFL deceleration and Thrills de-leverage, with valuation seen as attractive against the multi-year rollout opportunity.

UBS retained Buy, lowered target from $9.50 to $9.00. LFL acceleration at both core banners reinforces confidence in sustained momentum, with the youth consumer viewed as structurally resilient and the medium-term EBIT margin expansion thesis intact.

Bell Potter retained Buy, lowered target from $10.50 to $9.30. LFL acceleration at US was partly supported by favourable April comps, with gross margin assumptions improved on PS mix contribution though FY27 conservatism is warranted given consumer discretionary conditions.

Analysts' take on WiseTech

[11:25 am] WiseTech Global reaffirmed its FY26 EBITDA and margin guidance at the Macquarie Conference on Tuesday, removing a key downgrade overhang, while providing first-time underlying EBITDA disclosure that gave analysts greater confidence in the path back to a >50% margin by FY28.

Bell Potter retained Buy, target unchanged at $78.75. Guidance reaffirmation removes near-term downgrade risk and underlying cost disclosure supports the structural margin recovery thesis, with FY27 EBITDA margin forecasts viewed as potentially conservative.

Macquarie retained Outperform, target unchanged at $97.70. Management commentary skewed towards margin delivery over organic revenue growth, with the path back to ~50% EBITDA margins seen as achievable and potentially exceedable on execution.

ASX 200 higher as banks bounce

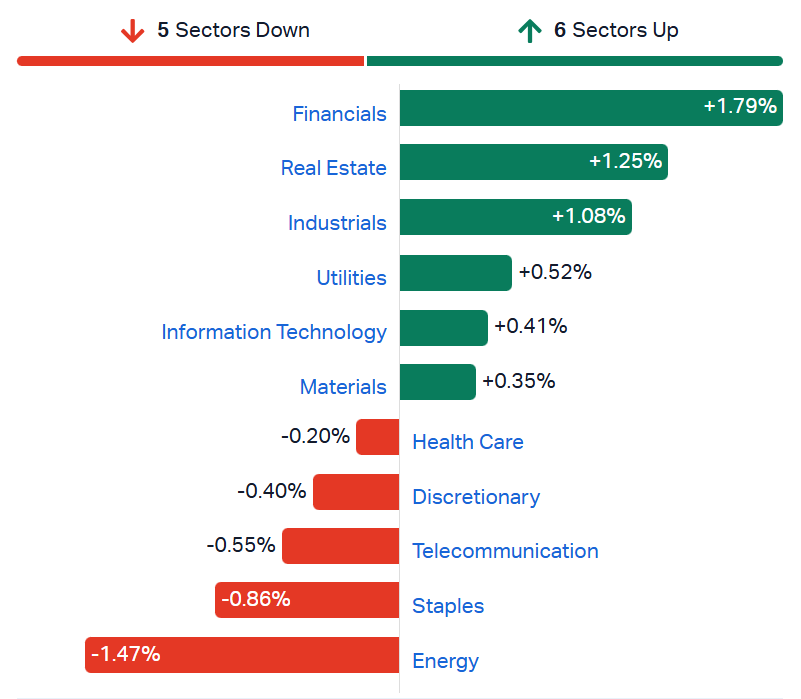

[10:50 am] ASX 200 up 0.74% in early trade, pushing back above the 200-day moving average. Let's see if we can hold on to these early gains.

Sectors are a little mixed, with Energy weighed by a ~3% pullback in oil prices (and down 1.4% in early trade today). Plenty of sectors moving in response to the RBA hike, including weakness among consumer-facing sectors like Staples, Telcos and Discretionary, and a sharp bounce for Banks and Real Estate (Aussie 10-year fell 6 bps yesterday to 4.95%).

ASX 200 sectors (Source: Market Index)

Infratil Q&A on CDC Data Centres contract

[10:45 am] Infratil provided additional colour on the 555MW CDC Data Centres contract via a business update call.

FY27 EBITDAF guidance unchanged at $680m-$720m

FY28 EBITDAF projected to surpass $1bn driven by new contract capacity coming online, with annualised contracted EBITDAF expected to reach ~$2bn once fully deployed post-FY28

FY27 capex guidance (ex-land) up to $3.8-4.2bn, up from $1.9-2.2bn a year ago

No additional shareholder equity required to fund the new contract, with funding sourced from existing debt capacity and hybrid markets

CDC maintains capacity to deliver additional large-scale contracts (hundreds of megawatts) before FY29 with an active pipeline

CDC on track to become the first 100% certified net zero data centre operator in 2026

Company page: Infratil (IFT)

Top ASX 200 gainers

[10:39 am] Infratil sharply higher off the back of a massive data centre contract, while banks, lithium and rare earth stocks trade sharply higher.

Ticker | Company | % Chg | Price |

|---|---|---|---|

IFT | Infratil | 11.71% | $11.73 |

WBC | Westpac | 3.11% | $38.80 |

LTR | Liontown | 2.93% | $2.46 |

LYC | Lynas Rare Earths | 2.64% | $19.06 |

ELV | Elevra Lithium | 2.55% | $12.88 |

REH | Reece | 2.54% | $13.74 |

NAB | National Australia Bank | 2.44% | $39.90 |

WOR | Worley | 2.38% | $12.27 |

ILU | Iluka Resources | 2.29% | $8.27 |

GMG | Goodman Group | 2.20% | $30.43 |

Top ASX 200 losers

[10:39 am] Not a lot of love for the Regis and Vault merger, Contract Energy is also giving back the entirety of yesterday's ~6% rally, JB Hi-Fi under pressure despite a relatively sound Q3 sales update (though management flagged significant supplier cost inflation and product shortages).

Ticker | Company | % Chg | Price |

|---|---|---|---|

RRL | Regis Resources | -6.67% | $6.30 |

VAU | Vault Minerals | -6.47% | $4.34 |

MFG | Magellan Financial Group | -6.44% | $9.01 |

CEN | Contact Energy | -6.01% | $7.98 |

TLC | Lottery Corporation | -5.48% | $5.27 |

OBM | Ora Banda Mining | -3.78% | $1.22 |

ALK | Alkane Resources | -3.39% | $1.43 |

360 | Life360 | -3.25% | $20.40 |

PDN | Paladin Energy | -3.05% | $11.76 |

JBH | JB Hi-Fi | -2.99% | $75.54 |

DigiCo and Infratil open sharply higher

[10:04 am] Both DigiCo Infrastructure REIT (+`16.9%) and Infratil (+10.6%) opened sharply higher after material data centre announcements supporting capital management flexibility and contracted growth.

To recap the catalysts:

DigiCo Infrastructure REIT: Announced the binding US$750m sale of its Chicago CHI1 facility at a ~5% premium to purchase price, materially strengthening the balance sheet (gearing down to 17% from 36%) and freeing capital to fund the highly accretive SYD1 88MW expansion, with management also flagging intent to explore enhanced distributions above FFO

Infratil : CDC Data Centres (49.7% owned by IFT) signed a 555MW contract with a US investment grade customer, the largest data centre contract in Australian history, lifting CDC's total contracted capacity beyond 1GW with EBITDAF expected to exceed $1bn in FY28 (and ~$2bn annualised when fully deployed)

Capral downgrades FY26 earnings outlook on Middle East supply disruption

[9:55 am] Capral has downgraded its FY26 earnings outlook to broadly in line with FY25 (from prior guidance of slightly above FY25), citing Middle East-related aluminium supply disruption, elevated LME prices and unplanned freight cost increases.

Middle East conflict has significantly disrupted global aluminium supply (Gulf smelters represent ~9% of global capacity), with restrictions from Strait of Hormuz closure compounded by military damage to some smelters

Capral sources a portion of billet supply from the Middle East but has replaced that volume from alternative local and offshore suppliers at a premium

Higher fuel costs driving unplanned increases in freight and other costs, with the business seeking to recover these from the market

Detached housing sector expected to begin recovering in CY26 with benefits weighted to H2

Company page: Capral (CAA)

Atlas Arteria board rejects IFM takeover offer

[9:47 am] The Atlas Arteria Independent Directors have unanimously rejected IFM's hostile takeover offer as too low, opportunistic and highly conditional.

Independent Directors recommend holders to reject IFM's offer of $4.75 cash per stapled security (less any distributions), which increases to $5.10 if IFM's relevant interest reaches 45%+

$4.75 offer is below the prior day's close of $4.79 and represents less than 10% premium to the last close before the offer

The $5.10 scenario implies only ~3% premium to the 12-month average and less than 20% to pre-offer close, well below typical infrastructure control premiums

Board flags the offer is opportunistic given Middle East conflict, FX and rate movements, and increasing illiquidity from IFM's holding have weighed on the security price

Company page: Atlas Arteria (ALX)

AGL Energy lifts lower end of FY26 guidance on strong operational performance

[9:40 am] AGL Energy has narrowed its FY26 guidance, reflecting continued strong operational and financial performance since the first half result.

FY26 Underlying NPAT guided to $610m-$680m (vs. prior $580m-$680m), a 2.4% upgrade at the midpoint though in-line with $646m ests

FY26 Underlying EBITDA guided to $2.06bn-$2.18bn (vs. prior $2.02bn-$2.18bn), a 1.0% upgrade at the midpoint

Lift driven by improved plant availability and flexibility (particularly strong performance of the thermal generation fleet), improved Customer Markets performance and disciplined cost management

AGL well placed for at least the next three months during the global fuel crisis, with current diesel storage near capacity for the generation assets and ongoing supply expected as an essential services provider

Company page: AGL Energy (AGL)

Acusensus, Aurizon and Sims reaffirm FY26 guidance

[9:33 am] Three companies reaffirmed their full-year guidance with broadly supportive operating commentary across their respective markets.

Acusensus (ACE): Reaffirmed FY26 revenue of $83m-$87m and adjusted EBITDA of $7.2m-$8.2m, supported by a strong US sales pipeline, three concurrent UK operational programs, a 6+6 month extension of the Transport for NSW mobile speed camera program.

Aurizon (AZJ): Reaffirmed FY26 underlying EBITDA of $1.68bn-$1.75bn, with 10-month volumes showing Network up 2.6%, Coal up 0.8%, Bulk up 6.7% and Containerised Freight up 13.2% year-on-year. A small number of fuel adjustment mechanisms (mostly in Bulk) are expected to deliver a ~$10m negative EBITDA impact in FY26

Sims (SGM): Reaffirmed FY EBIT of $350m-$400m and SLS underlying EBIT of $165m-$185m, supported by sustained pricing strength, ongoing hyperscaler demand, strong non-ferrous pricing, US tariff protection and AI infrastructure build-out. Limited operational impact from the Middle East conflict (confined to inbound logistics and fuel costs), though ANZ ferrous pricing remains subdued on elevated Chinese steel exports

Company pages: Acusensus (ACE), Aurizon Holdings (AZJ), Sims (SGM)

Duratec awarded $68m Darwin Ship Lift Facility sub-contract

[9:25 am] Duratec has been awarded a $68 million sub-contract by the Clough BMD JV for construction and commissioning works at the Darwin Ship Lift Facility, a key NT Government infrastructure development.

The project will commence in June 2026 with completion anticipated mid to late 2027.

Strong contracting activity has lifted Duratec shares 38.7% higher year-to-date and up 61.8% in the last twelve months.

Company page: Duratec (DUR)

DigiCo Infrastructure REIT to sell Chicago facility for US$750m

[9:22 am] DigiCo Infrastructure REIT has agreed to sell its Chicago CHI1 facility, materially strengthening the balance sheet to fund the accretive SYD1 expansion and explore enhanced distributions.

Binding US$750m sale of CHI1 to a North American fund manager, representing a ~5% premium to the November 2024 purchase price, a passing yield of 5.8% and in line with the all-in carrying cost

Net cash proceeds of ~$360m post repayment of asset-level debt, net debt to reduce from $1.5bn to ~$0.5bn, available liquidity to ~$0.9bn and gearing to fall from 36% to 17%

DGT also intends to monetise LAX1 and LAX2 sites, Kansas City (KCM1) and Dallas Fort Worth (DAL1) to be retained and actively managed for value

US asset sales expected to be materially FFO accretive from FY27, with capital redeployed into the SYD1 88MW project

DGT to explore returning excess capital via enhanced distributions in the short term above FFO, with a medium-term distribution policy of 90-100% of FFO maintained

Company page: DigiCo Infrastructure REIT (DGT)

JB Hi-Fi CEO flags supplier cost pressure heading into EOFY

[9:18 am] JB Hi-Fi Group CEO Nick Wells flagged increasing uncertainty in the retail environment, with the EOFY trading period set to be impacted by supplier component cost increases, stock availability issues and heightened competition.

Wells said the Group is "pleased to see sales growth in JB Hi-Fi and The Good Guys in what is an increasingly uncertain retail environment"

In technology categories, "we are seeing significant supplier component related cost increases and stock availability shortages, along with heightened competitive activity."

"As always, we will remain focused on what we can control and seek to maximise demand through driving great value for our customers, leveraging our strong supplier relationships, and delivering exceptional customer service," said Wells

Company page: JB Hi-Fi (JBH)

JB Hi-Fi Q3 FY26 sales update

[9:17 am] JB Hi-Fi delivered sales growth across JB Hi-Fi and The Good Guys in Q3 FY26 but management flagged a more challenging Q4 with supplier cost increases and stock availability issues in technology categories.

The below figures refer to Q3 FY26 (1-Jan to 31-Mar), on a year-on-year basis.

JB Hi-Fi Australia sales growth +4.0%, comparable sales growth +2.6%

JB Hi-Fi New Zealand sales growth +23.2%, comparable sales growth +15.2%

The Good Guys sales growth +2.5%, comparable sales growth +2.5%

e&s sales (1.4%), comparable sales (4.8%)

What I like to do with these updates is compare the growth rates vs. those 'first x weeks" updates from the 1H26 result. For the period 1-31 January, JB Hi-Fi noted:

JB Hi-Fi Australia sales growth +4.0%, comparable sales growth +2.4%

JB Hi-Fi New Zealand sales growth +26.4%, comparable sales growth +16.7%

The Good Guys sales growth +2.7%, comparable sales growth +2.7%

e&s sales (4.6%), comparable sales (7.9%)

Overall, growth rates have remained consistent, with fractionally higher comparable sales in Australia and The Good Guys.

Company page: JB Hi-Fi (JBH)

CDC Data Centres signs largest data centre contract in Australia's history

[9:05 am] Infratil flagged that CDC Data Centres has secured a 555MW data centre contract with a US investment grade customer, the largest in Australian history, lifting total contracted capacity beyond 1GW.

30-year contract with a US high-end investment grade customer (with renewal options of up to 20 years), to be delivered across CDC campuses already under development and becoming operational over FY28 and FY29

555MW equates to ~40% of operating capacity across all Australian data centres in 2025

Total CDC contracted capacity now exceeds 1GW, with EBITDAF expected to exceed $1bn in FY28

FY27 EBITDAF guidance unchanged at $680m-$720m as the new capacity becomes operational from FY28

New contract is within CDC's current growth plan and does not require further shareholder equity (following the $500m equity injection in February), to be funded via existing cash, committed debt facilities, further debt and hybrid funding

Supported by Moody's Baa2 (Stable) credit rating assigned to CDC's Australian business on 21 April

For context, Ifratil owns 49.7% of CDC Data Centres and is the company's largest asset by value. NZX-listed Infratil shares are up 8.9% at the time of writing.

Company page: Infratil (IFT)

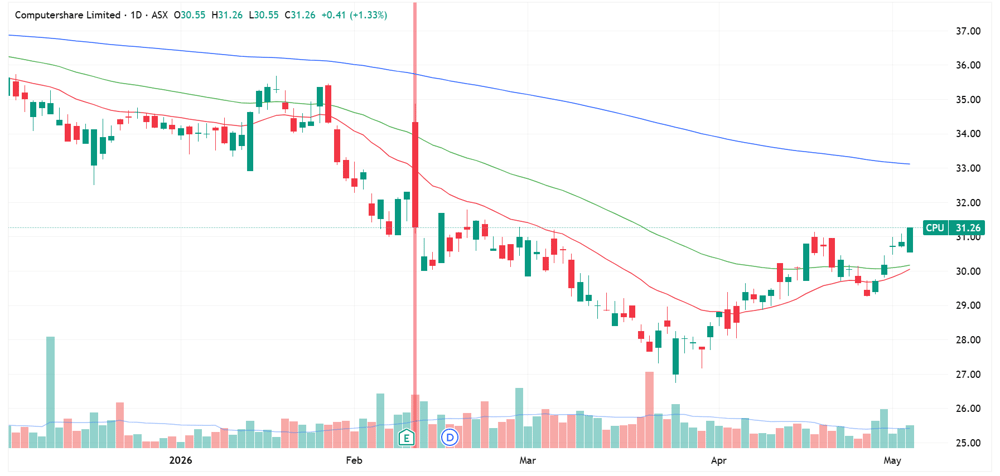

Thoughts on Computershare

[9:04 am] A few things to think about re Computershare's 2H26 update.

Computershare is trading around the same level as six months ago, when it reported its 1H26 result

The 1H26 result was modestly ahead of market expectations, with management EPS ahead and guidance upgraded to FY26

On this day (11-Feb), the stock rallied ~7% at the open but finished the day 3.1% lower

Looking further back, the stock has de-rated from a peak 26x in Jul-25 to now 19x

Today's update reaffirms FY26 management EPS, but upgrade margin income to $740m (vs. Macquarie ests of $733m)

Computershare daily price chart (Source: TradingView)

Computershare 2H26 trading update: Reaffirms FY26 Management EPS, lifts margin income guidance

[8:55 am]Computershare delivered a positive H2 trading update with consistent performance across divisions, reaffirming FY26 Management EPS guidance while upgrading margin income guidance on stronger client balances.

FY26 Management EPS reaffirmed at $1.44

FY26 Margin Income guidance upgraded to ~$740m from $730m, driven by average client balances now forecast to be $0.5bn higher than expected (the uplift coming from Corporate Actions)

Divisional commentary:

Issuer Services: Register Maintenance performing consistently, Corporate Action volumes broadly in line with expectations with the pipeline increasing

Employee Share Plans: Recurring client paid fee revenue continues to grow and trading revenues up year-on-year on increased transactions across energy sector clients

Corporate Trust: Overall issuance volumes and fee revenues higher year-on-year, Ginnie Mae document custodian approval secured in March 2026 supports further growth

Management flagged Computershare is well placed to deliver ongoing growth and high returns for shareholders in FY27

Company page: Computershare (CPU)

RBA Bullock signals pause to assess next steps

[8:53 am] The RBA delivered its third consecutive 25 bps hike to 4.35% on a decisive 8-1 vote, with Governor Bullock signalling policymakers will now pause to assess as forecasts show stubborn inflation through 2027.

8-1 vote to lift cash rate to 4.35%, unwinding all of last year's easing

Bullock said the hike gives the RBA "space to sit and see what happens" and be alert to both upside and downside inflation risks

Markets trimmed hike expectations on Bullock's comments, now pricing just one more increase in Q3 vs. an almost 60% chance of two more by year-end pre-presser

Updated RBA forecasts assume a cash rate peak of 4.7% (vs. 4.3% peak in December 2027 in the February update), with trimmed mean inflation seen at 3.8% in June, 3.5% in December, 3.1% mid-2027 before nearing the 2.5% midpoint by end-2027

RBA tightening further separates Australia from peers including the Fed and BoJ, which remain on hold citing war-driven uncertainty

Source: Bloomberg

Narrow breadth fuels comparisons to the dot-com bubble

[8:50 am] The US stock market's rally to fresh highs is being driven by such a narrow group of stocks that strategists are flagging dot-com era parallels, with breadth metrics raising concerns about drawdown risk.

The median S&P 500 stock is ~13% below its respective high, one of the widest gaps in 25 years per Goldman's Ben Snider

Four of the last five S&P 500 closing records occurred with decliners outnumbering gainers

Just 23% of S&P 500 members beat the index in April per BofA, the fourth-lowest monthly reading since 1986. Goldman finds the average 12-month drawdown following a precipitous drop in breadth is 10% since 1980

Nvidia alone accounted for more than 10% of S&P 500 gains in April, with Intel, AMD and ON Semiconductor among top performers

Equal-weight S&P 500 hasn't closed at a record since the Iran war started and only 6 of 11 sectors within 5% of records and just 53% of S&P 500 companies trade above their 200-day moving averages

US services activity holds up in April but pricing pressures persist

[8:49 am] US services activity remained in expansion in April with cost pressures elevated, while March new home sales surprised to the upside.

April ISM Services 53.6 vs. ests 53.7

New orders fell sharply to 53.5 from 60.6

Employment index rose to 48.0 from 45.2, still in contraction for a second straight month

Prices index held at 70.7, still highest since October 2022

Respondent feedback skewed negative, with resilience in services, healthcare and infrastructure outweighed by weak housing demand, delayed capex and cost pressures

US plays down Iran war return as Hormuz tensions persist

[8:48 am] The US played down the prospect of returning to active war with Iran after Monday's clashes, with both sides confirming the ceasefire remains in place even as Tehran tightens its grip on the Strait of Hormuz.

General Dan Caine and Defense Secretary Hegseth confirmed the truce is still holding, with Project Freedom described as a "defensive and temporary operation" to guide neutral ships through Hormuz

Iran cast Project Freedom as "Project Deadlock" and announced a new protocol requiring ships to receive an official email signalling approval before transiting Hormuz

UAE intercepted almost all of ~20 projectiles fired from Iran on Monday, with three Indians injured at a Vitol-part-owned oil terminal in Fujairah

Source: Bloomberg

US stocks hit fresh records as Iran ceasefire holds

[8:44 am] US equities pushed to all-time highs and oil retreated as confirmation the US-Iran ceasefire remains intact despite Monday's flare-up restored calm to global markets.

S&P 500 hit fresh records with semis leading (SOX up ~4% to a record, led by Intel), AMD shares soared 15% after hours on earnings

Brent down 3.3% to US$110.30 as Defense Secretary Hegseth confirmed the US-Iran truce remains intact and State Secretary Rubio framed US Hormuz support as a "defensive operation"

Treasuries firmer with yields down 1-3bps after Tuesday's big backup that took 10-year yields to nine-month highs

April ISM services remained in expansion though orders growth slowed, March JOLTS job openings little changed with hiring rebounding and new home sales picking up

JPMorgan strategists noted the Iran war rebound has been narrow, leaving the market primed for broader gains on even modestly positive news

Good morning!

[8:30 am] ASX 200 futures are up 38 pts (+0.43%) as of 8:30 am AEST.

The overnight session in a nutshell:

S&P 500, Nasdaq and Russell 2000 closed at fresh all-time highs as as Hegseth's reassurance on the US-Iran ceasefire buoyed risk-appetite and lowered oil prices

Palantir, AMD, Pfizer and Ferrari Q1 earnings all printed above consensus expectations

Other overnight tidbits include Russia and Ukraine declare competing ceasefires, US ISM services PMI remains in expansion but price index also holding at four year highs