ASX 200 Live Today - Wednesday, 11th February

The S&P/ASX 200 is set to rise as defensive and value-oriented sectors gained traction overnight. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Wednesday, February 11. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Be sure to refresh manually for the latest updates — and let us know how we can make it even better.

ASX 200 pushing intraday highs, within 1% of all-time highs

[1:50 pm] Wrapping the blog up a little early today. Pretty hectic day (but it only gets busier from here). At a glance, a very challenging reporting season where you have situations like:

CSL reporting a soft 1H26 and CEO transition, gapping down but ripping off session lows as the stock finds some valuation support and is extremely oversold

Amotiv reported what was a relatively in-line 1H26 result on Tuesday, opened 3.9% higher but U-turned to a -3.7% close. It's down another 3.3% today. Its 4WD segment underperformed and weighed on the overall result, and aftermarket conditions remain challenging

CBA's 1H26 cash NPAT beat expectations by 5%, which is pretty big for a bank. However, the stock is ripping ~7% higher off the beat, adding approximately ~$20bn in market cap.

Lots of wild moves where there is more than just the face value result at play.

Anyway, the ASX 200 is tracking 1.46% higher and continues to push intraday highs, largely off the back of CBA ticking higher, AGL rallying off the back of its 1H26 result (+9.5%) and resource strength (XMJ on a three-day win streak). While we're in the early innings of reporting season, we're seeing some big hitters have a material impact on the index. A note from UBS earlier this week said FY26 will mark a stepchange in ASX 200 earnings, with expectations of 12% EPS growth (after three years of flat-to-negative earnings).

CSL 1H26 earnings call highlights

[1:43 pm] CSL currently down 6.5%, well-off session lows of -12.3%. A few interesting takeaways from the earnings call:

Incoming CEO signalled full accountability for performance, with focus on execution and capturing operational and commercial opportunities.

H2 Ig growth expected as headwinds fade, contract wins flow through and recent commercial investments gain traction.

KCENTRA recovery remains long-dated, with contracted volumes growing at mid-single digits but offset by ongoing price pressure, keeping returns subdued for several years.

FY26 gross margin guided broadly flat to slightly higher, supported by cost reductions, yield gains and network optimisation, with the full benefit skewed to FY27.

Albumin revenue seen modestly down year-on-year in FY26 before returning to growth from FY27, while high single-digit NPAT growth guidance for FY27–28 remains unchanged.

Amotiv downgraded despite solid 1H26

[1:05 pm] Amotiv reported a slightly better-than-expected 1H26 on Tuesday, with most metrics tracking marginally ahead of consensus. Management reaffirmed FY26 guidance despite cost inflation and margin pressure.

However, the 4WD segment underperformed, dragging on the Group result. The stock opened 3.9% higher, but finished the session down 3.8%. Here's what analysts are thinking:

RBC Capital Markets downgraded to Sector Perform, target $11.50. Revenue and EBITA beat, but domestic cost inflation and weak 4WD performance pose risks to FY26 guidance.

Morgans downgraded to Accumulate, target lowered to $9.15 from $11.25. Mixed segment results, subdued 4WD outlook, and limited near-term catalysts suggest patience is required.

UBS maintained Buy, target raised to $11.40 from $11.00. Result seen as credible with cost controls offsetting inflation, though new car volumes remain a risk; valuation remains attractive.

Analysts lift Macquarie target prices

[12:34 pm] Macquarie shares edged 0.8% higher on Tuesday after the company provided a Q3 trading update, noting stronger contributions from pretty much all business segments including MAM, CGM and Macquarie Capital.

Brokers are broadly positive on the result, most of which have lifted their target prices this morning.

Jarden upgraded to Buy, raised target from $220.00 to $240.00. Improved valuation outlook and durable CGM recovery support the upgrade, though NIM drag and AI overfocus are flagged.

JPMorgan maintained Overweight, target $236.00. Divisional mix and commodities upgrade support positive outlook, with tech spend plateauing improving leverage.

Goldman Sachs maintained Neutral, raised target from $208.73 to $221.37. Strong divisional performance offset by tax drag, with BFS slightly underwhelming; commodities upgrade is a key positive surprise.

Analysts' take on Amplitude Energy

[12:30 pm] Amplitude Energy suffered a sharp 22.1% selloff on Tuesday after the company announced that its Elanora-1 well failed to find gas, delivering a water bearing result. This was the company's largest prospect for its ESCP program, which has since triggered a wave of valuation downgrades.

RBC Capital Markets downgraded to Sector Perform, lowered target from $3.25 to $2.70. Elanora failure raises risk for remaining drill targets, with reservoir quality and gas composition concerns, and M&A may be needed if outcomes disappoint.

Jarden downgraded to Overweight, lowered target from $3.40 to $2.67. Market likely cautious until seismic issues clarified; exploration uncertainties remain, but share price may undervalue remaining program potential.

Aussie consumer sentiment continues to slip

[11:59 am] Completely missed this economic report from Tuesday, still very interesting to see consumer sentiment continue to deteriorate amid growing rate hike expectations. Here are some of the key takeaways from the Westpac report:

Index down 2.6% to 90.5 in February from 92.9 in January, below historical post-rate hike average falls of 3.8% but well above lows seen in 2022–2024.

‘Time to buy a major item’ sub-index fell 5.6% to 93.5 and ‘family finances vs a year ago’ down 4.7% to 78.8, reflecting higher rates and cost-of-living pressures.

Near-term expectations largely stable: ‘family finances next 12 months’ ticked slightly lower to 97.7, ‘economy next 12 months’ 88.5,

Medium-term economic outlook weaker: ‘economy next 5 years’ sub-index down 2.5% to 93.5, signalling ongoing caution due to slow inflation return to target.

Australian first home buyer loans jump 6.8%

[11:48 am] The number of new first home buyer loans jumped 6.8% in the December quarter 2025, according to the ABS.

Dr Mish Tan, ABS Head of Finance Statistics said, "There was strong growth across all borrower-types this quarter. The number of first home buyer loans rose 6.8%, investor loan numbers rose 5.5% and the number of owner-occupier non-first home buyer loans rose 3.6%."

Tan notes this was the largest rise in the number of first home buyer loans since the December quarter 2023, and their value increased by 15.5%.

There were rises in New South Wales (10.9%), Queensland (6.4%), Victoria (3.5%), Western Australia (9.8%), South Australia (4.8%), Australian Capital Territory (7.1%) and Northern Territory (3.2%), while there was a fall in Tasmania (-1.7%).

The size of the average first home buyer loan hit a record $607,624 in the quarter (up 8.5%), driven largely driven by first home buyers in NSW.

Source: ABS

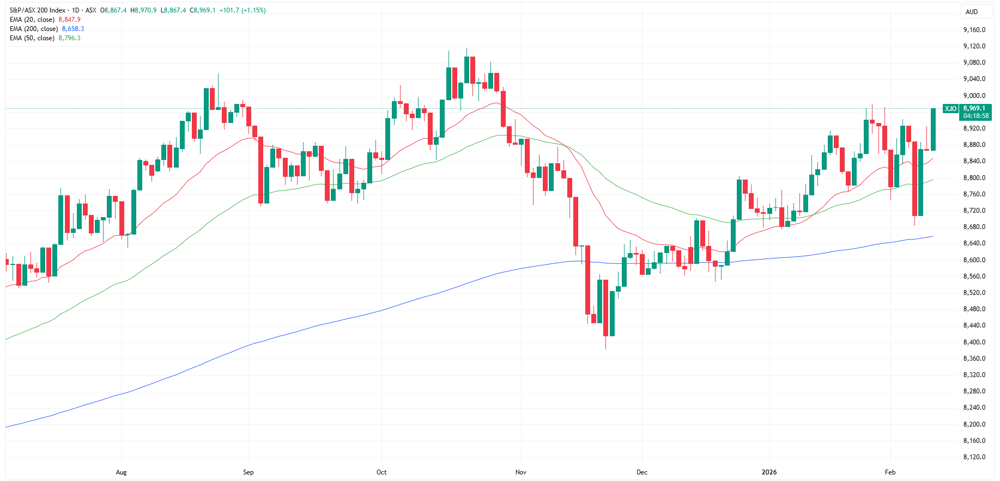

ASX 200 rallies to near 4-month high

[11:43 am] ASX 200 trading sharply higher this morning, up 1.16% to the highest since late October and within 2% of all-time highs. Today's gains are largely driven by CBA's massive 7.7% rally, which has more than offset CSL's ~6% tumble (houses over health eh?).

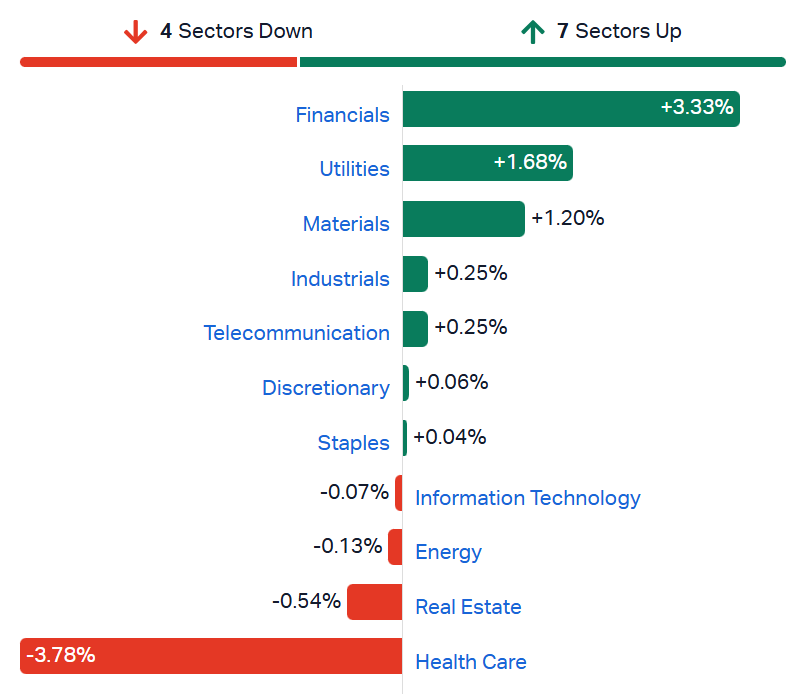

S&P/ASX 200 sectors (Source: TradingView)

S&P/ASX 200 daily chart (Source: TradingView)

James Hardie Q3 earnings call highlights

[11:20 am] James Hardie just wrapped up its Q3 earnings call, where management flagged mixed construction demand, offset by pricing, operational efficiencies, and strategic growth initiatives.

Here are the key takeaways:

New construction soft in Texas, West, and Southeast; Midwest shows resilience, repair/remodel activity stabilising with improving contractor sentiment

Fiber Cement pricing well received, modest input cost inflation expected in back half of FY27, supporting value-based pricing

Commercial revenue synergies targeted at $125m by FY27, with early wins realised; siding & trim volumes face tough comps, margin pressure from marketing and delayed plant closures

Operational optimisation underway: closing older plants, realigning footprint to modern sites for $25m+ annual savings, focusing on material conversion and industry consolidation opportunities

CSL bounces from session lows

[11:17 am] CSL has rallied from session lows of ~$150, now down just 6.0% to $161.10. Despite the unexpected CEO transition and weaker-than-expected 1H26 result, the bounce may be driven by short covering, extreme oversold conditions and a 'cheap' valuation relative to historical levels (now at 17x vs. ~30x a year ago).

CBA rallies to 3-month high

[10:48 am] CBA opened sharply higher this morning, up 3.9% ($165.00) thanks to a stronger-than-expected 1H26 result. Price action has been overwhelming positive, with the stock now up 6.6% ($169.21) to the highest since November 2025.

Some of the key numbers from our earlier post include:

Cash NPAT up 6% to $5.45bn vs $5.20bn ests (5% beat)

NIM down 4 bps to 2.04% vs 2.04% ests (in-line)

CET1 ratio of 12.3% vs 12.3% ests (in-line)

Interim DPS up 4% to $2.35 cps vs Morgans ests of $2.30 (2.1% beat)

CSL tumbles, trading at the lowest since April 2018

[10:29 am] CSL has extended its sell-off, now down about 16% over the past two sessions to around $151.

As we noted earlier this morning, CEO Paul McKenzie announced his retirement (4:05 pm on Tuesday) along with today's broadly weaker-than-expected result:

Paul McKenzie retires as CEO and Managing Director

Revenue down 4% to $8.33bn vs. $8.51bn ests (2% miss)

Underlying NPATA down 7% to $1.95bn vs. $2.05bn ests (5% miss)

Interim dividend flat at 130 cps vs. 133 cps ests (2.2% miss)

FY26 guidance reaffirmed, including NPATA growth of 4-7% and revenue growth of 2-3%

Outlook commentary flagged Seqirus expecting a lower second-half due to "normal seasonality of the global influenza business" and Vifor to be "adversely impacted by generic competition in iron products."

Top ASX 200 gainers and losers

[10:23 am] James Hardie is rallying, while banks and commodities stocks are trading broadly higher, as CSL drags at the other end of the spectrum, alongside weakness across uranium and lithium names.

Ticker | Company | % Chg | Price |

|---|---|---|---|

JHX | James Hardie Industries | 12.18% | $37.29 |

AGL | Agl Energy | 6.33% | $9.41 |

CBA | Commonwealth Bank Of Australia | 5.32% | $167.18 |

CEN | Contact Energy | 5.31% | $8.23 |

CPU | Computershare | 5.20% | $33.98 |

EVN | Evolution Mining | 3.54% | $15.51 |

DMP | Domino's Pizza | 3.31% | $23.09 |

A2M | A2 Milk Company | 2.98% | $8.65 |

NEM | Newmont Corporation | 2.24% | $171.23 |

MQG | Macquarie Group | 2.11% | $219.03 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

PDN | Paladin Energy | -2.72% | $11.80 |

DYL | Deep Yellow | -2.75% | $2.48 |

NWL | Netwealth Group. | -2.84% | $23.61 |

GQG | Gqg Partners, Inc | -3.33% | $1.60 |

PLS | Pls Group | -3.56% | $4.06 |

SLX | Silex Systems | -3.59% | $6.98 |

ASX | Asx | -3.87% | $54.17 |

RMD | Resmed Inc | -3.87% | $37.12 |

DRO | Droneshield | -4.73% | $3.22 |

CSL | Csl | -11.95% | $150.91 |

Evolution boosts earnings, trims cost outlook

[10:00 am] Evolution’s December half update showed higher earnings and cash flow, while FY26 production guidance was maintained and AISC guidance was revised lower.

Statutory NPAT up 110% to $767m vs $365m pcp, with underlying profit after tax of $785m vs $385m pcp

Underlying EBITDA up 57% to $1.59bn vs $1.01bn pcp, driven by on plan delivery and higher gold and copper prices

Production in line with plan at 365koz of gold and 36kt of copper, with FY26 guidance held at 710 to 780koz gold and 70 to 80kt copper, though copper is tracking toward the lower end after the Ernest Henry weather event

Group AISC guidance updated to $1,640-$1,760 an ounce, a 6% improvement on original guidance, supported by cost control and higher by product credits

Group cash flow rose to $608m vs $273m pcp, cash balance lifted to $967m, and the board declared a 20c fully franked interim dividend, payable 2 April with a 4 March record date

By Warren Masilamony | Company page: Evolution Mining (EVN)

Domino’s appoints Andrew Gregory as new CEO

[9:43 am] Domino’s has named experienced QSR executive Andrew Gregory as its incoming Group CEO & MD to drive growth and operational performance.

Andrew Gregory brings over 30 years of global QSR experience, including leadership roles at McDonald’s in the US, ANZ, and Japan.

Gregory will start no later than 5 August 2026, after fulfilling obligations with his current employer, with Executive Chairman Jack Cowin overseeing a structured transition.

Company page: Domino’s Pizza (DMP)

Aussie Broadband to acquire AGL’s telco business

[9:41 am] Aussie Broadband will buy AGL Energy’s telecommunications unit, targeting network growth and EPS accretion.

Acquisition valued at $115m in scrip at $8.85 per share, with up to $10m in additional shares issued in $2m tranches if net growth targets are met.

Migration of AGL Telco customers to Aussie Broadband’s network expected to start Q1 FY27 and complete in H1 FY27, with EPS accretive impact in the first year post-migration.

Acquisition expected to generate revenue of ~$235m and underlying EBITDA of ~$21m in the 12 months after migration.

Company page: Aussie Broadband (ABB)

AGL Energy 1H26 beats estimates, tightens FY26 guidance

[9:40 am] AGL delivered solid first-half results underpinned by operational performance and customer margin growth.

Revenue of $7.04bn vs $6.87bn ests (2% beat)

Underlying NPAT of $353m vs $311.7m ests (13% beat)

Adjusted EBITDA of $1.09bn vs $1.02bn ests (7% beat)

Interim dividend up 4.3% to 24 cps vs. 22 cps ests (9.0% beat)

FY26 guidance was also narrowed to:

Underlying EBITDA between $2,020-2,180m vs. prior $1,920-2,220m (1.4% higher at the midpoint)

Underlying NPAT now $580-680m vs. prior $500-700m (5.0% higher at the midpoint)

Management attributed this to a stronger first-half performance driven by consumer margins, lower than anticipated operating costs and lower than expected depreciation.

Company page: AGL Energy (AGL)

James Hardie Q3 adjusted net income beats estimates, strong EBITDA growth

[9:30 am] James Hardie delivered solid Q3 results, with adjusted net income and EBITDA exceeding expectations, driven by strong sales in Siding & Trim and Deck, Rail & Accessories.

Revenue up 30% to $1.24bn vs $1.21bn ests (3% beat)

Adjusted EBITDA up 26% to $329.9m vs $310.0m ests (6% beat)

Adjusted net income down 7% to $142.2m vs $129.7m ests (10% beat)

Adjusted EPS down 31% to 24 cents vs 23 cents (4% beat)

FY26 guidance upgrade, including total adjusted EBITDA of $1.232-1.263 billion vs. prior guidance of $1.20-1.25 billion and $1.23 billion ests (~1.5% beat at the midpoint).

Company page: James Hardie Industries (JHX)

SGH 1H26 NPAT beats estimates, strong cash flow supports dividend

[9:24 am] SGH delivered resilient first-half results with stable EBIT, improved margins, and strong cash generation, underpinning a higher interim dividend.

Revenue down 2% to $5.41bn vs $5.44bn ests (1% miss)

Adjusted EBIT flat at $844m vs $827.5m ests (2% beat)

Adjusted EBITDA up 1% to $1.11bn vs $1.08bn ests (3% beat)

Underlying NPAT up 2% to $518.2m vs $508.0m ests (2% beat)

Interim DPS up 7% to 32 cps

Adjusted net debt/EBITDA 1.9x

FY26 guidance of low to mid single-digit EBIT growth year-on-year reaffirmed

Company page: SGH Limited (SGH)

CBA 1H26 cash NPAT beats estimates, dividend up 4%

[9:20 am] Commonwealth Bank delivered a strong first-half result, supported by lending and deposit growth, solid operational performance, and resilient credit quality.

Cash NPAT up 6% to $5.45bn vs $5.20bn ests (5% beat)

NIM down 4 bps to 2.04% vs 2.04% ests (in-line)

CET1 ratio of 12.3% vs 12.3% ests (in-line)

Interim DPS up 4% to $2.35 cps vs Morgans ests of $2.30 (2.1% beat)

Performance supported by lending and deposit volume growth, partially offset by lower margins and higher operating expenses from inflation and technology investments

Economic backdrop: strong labour market, easing interest rates, rising consumer demand, and investment in AI and energy infrastructure underpin growth while inflation remains above RBA target

Comment on dividends: CBA said it continues to target a full-year payout ratio of 70-80% of cash NPAT

A very strong cash NPAT beat as far as bank results go, though the all-important NIM was in-line. Despite the solid result, CBA is still trading at 26x, which analysts will broadly say something along the lines of "this is still the world's most expensive bank" and hit it with a Sell.

Company page: Commonwealth Bank (CBA)

ASX CEO Helen Lofthouse to step down in May

[9:13 am] ASX CEO Helen Lofthouse will leave in May after leading a transformation agenda and technology modernisation, with the CHESS project now on a stable footing. The Board says the CEO search will not slow progress on strategic priorities, with the Executive team remaining fully accountable for delivering key initiatives.

Company page: ASX (ASX)

Computershare 1H26 in line with estimates

[9:07 am] Computershare reported stronger first-half results with revenue and EPS up year-on-year, supported by resilient operations and increased client activity despite lower interest rates. The result was announced after market closed on Tuesday, and has already attracted some analyst upgrades, with JPMorgan upgrading the stock to Overweight (from Neutral) and lifting its target price to $36.50 from $35.50.

Revenue up 4% to $1.57bn vs $1.52bn ests (3% beat)

Management of NPAT $392.6m vs $385.9m ests (2% beat)

Management EPS up 3.9% to $0.68 vs $0.68 ests (in-line)

Interim dividend up 22% to 55 cps vs. Citi ests (Jan-26) of 50 cps (10% beat)

Margin income down 5.4% to $372.9m due to lower interest rates, partially offset by hedging and increased client balances

FY26 management EPS upgraded to 144 cps vs. prior guidance of 140 cps and 141 ests (2.1% upgrade)

Overall, a very clean result, at a time where CPU has de-rated ~22% since last August, now trading at a trailing 20x, the lowest multiple since early 2025.

Company page: Computershare (CPU)

CSL 1H26 results miss market expectations

[9:00 am] CSL posted softer-than-expected first-half results, weighed down by impairments at CSL Vifor and Seqirus, but reaffirmed FY26 guidance and expanded its share buy-back.

Revenue down 4% to $8.33bn vs. $8.51bn ests (2% miss)

Underlying NPATA down 7% to $1.95bn vs. $2.05bn ests (5% miss)

Interim dividend flat at 130 cps vs. 133 cps ests (2.2% miss)

Total after-tax non-restructuring impairments of ~$1.1bn, including $843m in intangible assets (CSL Vifor impacted by generics) and $170m in property, plant and equipment

Statutory net profit after tax down 81% to $401m

FY26 guidance reaffirmed, including NPATA growth of 4-7% and revenue growth of 2-3%

Outlook commentary flagged Seqirus expecting a lower second-half due to "normal seasonality of the global influenza business" and Vifor to be "adversely impacted by generic competition in iron products."

CSL is trading at a trailing 18x, the lowest since mid-2012. However, the broad 1H26 miss and CEO departure is not a good look. Reaffirming guidance is not always a good thing. A glass half full take is that "great, full-year expectations are unchanged" vs. the glass half empty take which is "now the second half needs to work harder/possible earnings downgrades in the second half."

Company page: CSL (CSL)

CSL's after market bombshell

[8:50 am] For some reason, CSL thought it would be a good idea to announce the retirement of CEO Paul McKenzie at 4:05 pm AEDT on Tuesday. This crashed the share price at the closing auction, driving the stock from a ~1.5% gain to a 4.9% dip at market close.

Paul McKenzie retires as CEO and Managing Director after three years as CEO and seven years with CSL, credited with navigating COVID-19 challenges, stabilising supply chains, and growing plasma collections.

Gordon Naylor appointed interim CEO, effective 11 February, bringing 33 years of CSL experience including roles as CFO, President of Seqirus, and architect of global plasma and vaccine operations.

A search for a permanent CEO is conducted, focusing on strategic transformation and shareholder value.

CSL just released their results this morning, which was broadly below market expectations. I guess they wanted two moderately lower days, as opposed to announcing everything all at once (remember the Aug-25 results where it featured a soft FY25 result, guidance miss, potential Sequirus demerger, a massive buyback and restructure?).

Company page: CSL Limited (CSL)

Fed officials signal patience amid inflation and growth outlook

[8:47 am] Fed speakers stressed data-driven decisions, cautious optimism and balance sheet considerations.

Cleveland Fed’s Hammack (voter) said rates could remain on hold for an extended period, preferring patience over fine-tuning, and noted a resilient macro backdrop with fiscal policy supporting growth and inflation expected to ease later this year.

Dallas Fed’s Logan (voter) said she would only support further rate cuts if labor market weakness materialises, highlighted that balance sheet management is separate from policy stance, and noted reserve supply should adjust with economic growth and demand trends.

Despite the relatively hawkish Fedspeak, US bond yields continued to trend lower overnight. The most notable move was the 2-year on the cusp of trading at the lowest since September 2022.

US 2-year government bond yield weekly chart (Source: TradingView)

US retail sales stall in December

[8:44 am] US consumer spending slowed at year-end, with broad-based weakness highlighting pressure from cost-of-living concerns and uneven discretionary demand.

Retail sales flat month-on-month in December vs. expectations for a 0.4% increase

Sales ex-autos also flat vs. 0.3% ests

Increases in building materials/garden supplies (+1.2%), sporting goods (+0.4%), gas stations (+0.3%), food/beverage stores (+0.2%), online stores (+0.1%)

Declines in furniture/home (-0.9%), clothing/accessories (-0.7%), electronics/appliances (-0.4%), autos/parts (-0.2%), health/personal care (-0.2%), restaurants/bars (-0.1%), general merchandise (-0.1%)

Winter weather and demographic disparities likely weighed on spending, with lower-income households showing constrained discretionary outlays while wealthier households supported by markets

AI tax tool triggers wealth manager rout

[8:41 am] A new AI product for automated tax and advice workflows sparked a sharp selloff in wealth-management stocks as investors price in fee pressure and disinter-mediation risk.

Wealth managers sold off aggressively after Altruist unveiled an AI tool for personalised strategies and document automation, with Raymond James down 8.8%, Charles Schwab down 7.4% and LPL Financial down 8.3%, all among their worst sessions since 2020–21.

The move surprised analysts, with Schwab carrying just one sell rating out of 24, highlighting how fast AI risk is being repriced versus existing fundamentals and consensus views.

Investor concern centres on efficiencies being competed away, long-term fee compression and market-share shifts as AI lowers the cost of advice and back-office functions.

The selloff mirrors recent AI-driven rotations across software, insurance and private credit, though some groups have already rebounded, suggesting parts of the move may be knee-jerk rather than structural.

Source: Bloomberg

US share trading breaks the $1tn-a-day barrier

[8:40 am] US equity markets are seeing structurally higher turnover, with trading volumes surging even as volatility stays subdued, pointing to deeper, more persistent liquidity.

Average daily equity turnover hit a record $1.03tn in January, up ~50% from the same period in 2025, with more than 19bn shares changing hands per day, the second-highest on record.

Heavy volume is no longer volatility-driven, with the VIX averaging just 16.2 in January, signalling sustained liquidity rather than panic-led trading.

Participation is broad-based across retail, hedge funds, market makers and automated strategies, with zero-day options, ETFs and platforms like Robinhood and Schwab accelerating churn.

Market structure is shifting, with 93 sessions in 2025 above 18bn shares traded, or 37% of days, versus just 4% in 2024, suggesting elevated activity is becoming the norm.

Sector rotation amplified flows, with investors trimming mega cap tech and reallocating into energy, materials and industrials, marking the sharpest market broadening in five years.

Source: Bloomberg

A very, very busy morning

[8:37 am] Today is one of those mornings where it feels like I'll be playing typeracer through to market open. We'll quickly take a look at some key overnight headlines, before switching over to company results. Let's get it.

Good morning!

[8:31 am] ASX 200 futures are up 38 pts (+0.43%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks mostly lower, with the S&P 500 (-0.33%) and Nasdaq (-0.59%) closing around session lows

Breadth was positive as the Equal-weight S&P 500 (+0.36%) and Dow (+0.10%) both closed at a second straight all-time high

Various drivers for this defensive session, including insurers and financial advisory sectors hit by AI competition concerns, weaker-than-expected US December retail sales data and hawkish Fedspeak

To catch up on all overnight developments, check out today's Morning Wrap.