ASX 200 Live Today - Tuesday, 14th July

The S&P/ASX 200 is set to fall after Trump reinstated the Hormuz blockade, while AI-related stocks continue to fall overnight.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, July 14. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

Top ASX 200 gainers and losers

[10:26 am] Energy stocks, including refiners and coal names, top the leaderboard, while gold and uranium stocks open sharply lower.

Ticker | Company | % Chg | Price |

|---|---|---|---|

KAR | Karoon Energy | 6.23% | $1.54 |

LNW | Light & Wonder | 4.99% | $108.51 |

WDS | Woodside Energy | 3.65% | $30.39 |

YAL | Yancoal Australia | 3.51% | $5.60 |

WHC | Whitehaven Coal | 3.32% | $7.79 |

ELV | Elevra Lithium | 3.28% | $9.12 |

NHC | New Hope Corporation | 2.97% | $5.38 |

DMP | Domino's Pizza | 2.94% | $16.43 |

BPT | Beach Energy | 2.86% | $0.90 |

VEA | Viva Energy Group | 2.79% | $2.40 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

KCN | Kingsgate | -13.56% | $3.76 |

SLX | Silex Systems | -8.00% | $4.83 |

PDI | Predictive Discovery | -5.19% | $0.64 |

PDN | Paladin Energy | -5.16% | $9.19 |

DYL | Deep Yellow | -5.02% | $1.33 |

OBM | Ora Banda Mining | -4.48% | $1.07 |

PNR | Pantoro Gold | -4.43% | $1.94 |

CMM | Capricorn Metals | -4.20% | $12.33 |

CYL | Catalyst Metals | -3.81% | $5.55 |

MI6 | Minerals 260 | -3.74% | $0.59 |

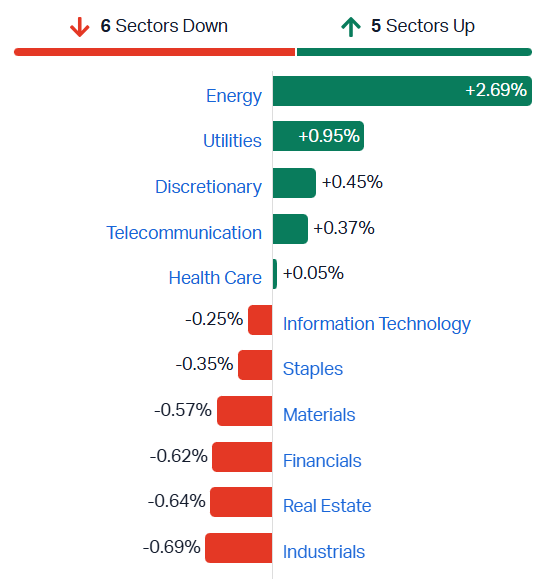

ASX 200 opens slightly lower, Energy stocks hit a one-month high

[10:22 am] Not the worst kind of open after a ~10% spike in oil prices. The ASX 200 is currently down 0.31%, as strength from Energy and Utilities offset the soft open for miners, banks and industrials.

BHP (+0.3%) is holding up well after copper prices slipped just 0.1% overnight to US$6.29/lb. Though relative strength from the majors is offset by the broad weakness among gold miners (XGD down 2.9%).

S&P/ASX 200 sectors (Source: Market Index)

SKS wins early works package for Melbourne hyperscale data centre

[9:57 am] SKS Technologies has secured $28 million of early works with Built on the MEL2 hyperscale data centre in Melbourne's northwest, following its earlier MEL1 build for the same client.

Scope covers substation and switchgear works, building fit-outs and in-ground high-voltage, low-voltage and communications infrastructure, with work starting immediately

MEL2 site is planned to deliver more than 354MW of capacity via over $5bn of investment

Contract lifts the order book to an FY27 starting position of $312m, up 7 times since June 2023

Work on hand has compounded at a 68% CAGR, rising from $39m in June 2023 to $312m in June 2026

Tender pipeline has grown almost 120% since February to $1,254.02m, with data centre tenders now just over $1bn versus $423.56m in February

SKS previously completed about $120m of works on the MEL1 facility, including the full suite of critical electrical systems

Company page: SKS Technologies Group (SKS)

Morgan Stanley calls miner pullback a buying opportunity, rotates to copper and uranium

[9:47 am] Morgan Stanley reads recent mining weakness as profit-taking after an 18-month run rather than a cycle top, and is rotating towards commodities with stronger demand, led by copper and uranium.

Copper: BHP stays overweight and the preferred exposure on strategic demand, while Sandfire lifts to equal-weight from underweight as consensus looks conservative on Motheo

Uranium: term prices have hit US$95 to US$97/lb with a roughly 13.5mlb 2026 deficit, keeping Paladin a key beneficiary and Boss Energy offering mine-plan upside, both overweight

Rio Tinto (RIO) cut to underweight from equal-weight as aluminium momentum fades, with merger-talk risk potentially reviving after August 5

Deterra Royalties (DRR) cut to underweight from overweight after strong performance and a more cautious iron ore view

Lithium: IGO lifts to equal-weight from underweight on reset valuations and a seasonally strong third quarter, though earnings look at risk of a cut at the coming quarterly, with Pilbara (PLS) still preferred but equal-weight

Rare earths: Iluka (ILU) stays overweight on near-term pricing strength and Lynas (LYC) equal-weight, with China's export-control exemptions in focus ahead of the November 10 deadline

Gold: weaker ETF demand and reduced Fed-cut pricing imply a slower recovery, though Morgan Stanley sees upside to around US$4,450/oz by the fourth quarter

GR Engineering flags Tower Hill contract at risk from Genesis-Vault merger

[9:15 am] GR Engineering has told the market that Genesis Minerals' proposed acquisition of Vault could see its $229 million Tower Hill EPC contract avoided, with ore instead processed through the King of the Hills plant.

Genesis has advised that synergies from the Vault merger include processing ore through the King of the Hills plant and avoiding construction of the Tower Hill process plant

GR Engineering was awarded the $229m Tower Hill EPC contract on 21 May 2026 and has since commenced engineering works and procurement of long lead items

The company will keep working with Genesis to optimise outcomes based on work scheduled and performed to date

There will be no adverse impact to results for the year ended 30 June 2026 and the near-term pipeline for FY27 remains strong

Company page: GR Engineering Services (GNG)

Genesis and Vault agree $12.6bn merger to create new Australian gold major

[9:12 am] Genesis Minerals will acquire Vault Minerals in a cash and scrip scheme valuing Vault at about $5.6 billion, forming a top three ASX gold producer anchored in the Leonora-Laverton district.

Vault shareholders will receive 0.7629 new Genesis shares plus $0.475 cash per Vault share, implying $5.2741 a share at announcement, a 15.7% premium to Vault's last close

Genesis shareholders will own about 59.8% of the merged group and Vault shareholders 40.2%, with the Vault board unanimously recommending the scheme in the absence of a superior proposal

The deal follows Vault's termination of its earlier agreed merger with Regis Resources, triggering a break fee of about $50.7m payable by Vault to Regis

The merged group would have a pro-forma market capitalisation of about $12.6bn, annual production of 600koz to 700koz, mineral resources of 33.6Moz and ore reserves of 9.4Moz, plus $611m net cash and $1.4bn liquidity

Genesis estimates about $2.0bn in post-tax synergies including $1.5bn over ten years, largely from processing Tower Hill ore through the King of the Hills mill and avoiding construction of the Tower Hill mill, saving $715m in growth capex

Raleigh Finlayson will be managing director and Russell Clark non-executive chair, with a seven-member board of four Genesis and three Vault directors, and a strategic plan due in the first half of 2027

Company page: Genesis Minerals (GMD)

WA goldfields gold updates: Astral, Ora Banda and New Murchison

[9:08 am] Three WA gold developers reported drilling and inventory progress, spanning Astral's Theia extension, Ora Banda's Davyhurst resource and reserve growth and high-grade hits at New Murchison's Cloudkicker.

Astral's deep diamond drilling below the 1.4Moz Theia deposit at Mandilla returned 52.60m at 1.48g/t Au from 389.4m and 54.0m at 2.38g/t Au from 316.0m

Both Astral holes ended in mineralisation up to 250m below the current resource shell, with nine of the expanded 12-hole 7,500m program complete and more holes likely

Ora Banda's Davyhurst mineral resources rose 75% to 3.69Moz and ore reserves 159% to 610koz after $75m and 310,000m of FY26 drilling

Round Dam drove the Ora Banda upgrade with a maiden 1.3Moz resource and 223koz reserve, with a further 340,000m planned for FY27 and a maiden Little Gem resource due in 1H FY27

New Murchison returned shallow high-grade hits at Cloudkicker including 10m at 13.61g/t Au from 44m, 8m at 9.22g/t Au from 62m and 1m at 54.80g/t Au from 58m

Cloudkicker is within the approved Crown Prince mining proposal so mining has started, with first ore to be crushed in September 2026 and circa 20,000oz of gold in ore expected over 12 to 18 months

Company pages: Astral Resources (AAR), Ora Banda Mining (OBM), New Murchison Gold (NMG)

Coronado promotes CFO Barrie van der Merwe to CEO

[9:06 am] Coronado Global Resources has appointed chief financial officer Barrie van der Merwe as chief executive and managing director from 1 August, tasking him with returning the coal miner to profitability and cutting debt.

Van der Merwe steps up from CFO, a role he has held since 2025, and brings more than three decades of mining experience across turnarounds, restructuring and finance

Chairman framed the appointment around a phase in which the business needs to be returned to profitability and reduce debt to open up strategic options

Interim CEO and founder Gerry Spindler moves to a non-executive director role on the Board

Sandeep Deoji named interim CFO from 1 August pending a permanent appointment

Base salary set at $1.2m a year inclusive of super, plus $350,000 payments in December 2026 and December 2027 and participation in senior executive incentives

Company page: Coronado Global Resources (CRN)

Light & Wonder reaffirms FY26 growth outlook ahead of Q2 results

[9:05 am] Light & Wonder has reiterated its FY26 guidance for mid-to-high single-digit consolidated AEBITDA growth and updated on its buy-back, with Q2 results due after US market close on 4 August.

Reaffirmed FY26 outlook of mid-to-high single-digit consolidated AEBITDA growth

Committed to cutting net debt leverage towards the mid-point of its target range during 2026 and below 3.0x in 1H27

Around US$180m remains under the ongoing share repurchase program

Repurchased 1,612,580 CDIs in Q2 for about US$134m, with buy-backs paused from 29 June ahead of the blackout period

Shares outstanding, including common stock and CDIs, totalled 77,049,181 as at 1 July

Q2 results due after US markets close on 4 August, before the ASX opens on 5 August

Company page: Light & Wonder (LNW)

Mining stocks tumble to year-to-date lows

[9:00 am] The once high-flying sector was aggressively sold off in recent weeks. Below, we take a look at how these US-listed ETFs have performed.

Global X Uranium ETF (-5.2%) now trading at the lowest since 5-Sep-25, down 6.3% year-to-date vs. peak of ~42% in late January

VanEck Rare Earth/Strategic Metals ETF (-4.3%) now at the lowest since 2-Jan-26. It was up as much as 42% to early May, now up just 1.4% year-to-date

VanEck Gold Miners ETF (-2.8%) trading at the lowest since 20-Nov-25 and down 15.7% year-to-date

Global X Copper Miners ETF (-2.8%) have held up relatively well, but now up just 1.1% year-to-date

NYSE-listed Global X Uranium ETF (top left), VanEck Rare Earth and Strategic Metals ETF (top right), VanEck Gold Miners ETF (bottom left) and Global X Copper Miners ETF (bottom right) daily charts | Source: TradingView

Commodities on the backfoot

[8:53 am] A rough overnight session for most commodities, weighed by higher oil prices, rising bond yields and a firmer US dollar.

Symbol | Chg % | Last (US$) |

|---|---|---|

Brent | 10.76% | 83.31 |

Aluminium | 0.42% | 3145 |

Copper | -0.12% | 6.29 |

Nickel | -0.17% | 16673 |

Platinum | -1.91% | 1599 |

Zinc | -1.91% | 3542 |

Palladium | -1.99% | 1248 |

Gold | -2.86% | 4002 |

Silver | -3.70% | 57.62 |

Morgan Stanley's Wilson sees earnings broadening beyond tech

[8:44 am] Michael Wilson expects strong second-quarter earnings from the median US stock to widen the rally beyond the tech megacaps as reporting season kicks off with the big banks.

Median S&P 1500 constituent is delivering EPS growth above 10%, the best since the post-Covid recovery

Analysts continue upgrading profit estimates for the consumer discretionary and transport sectors, both tied to economic growth

S&P 500 firms are expected to post a 23% jump in profits, among the best readings outside major recession recoveries

Equal-weighted S&P 500 is outperforming the cap-weighted gauge for the first time since 2022, signalling broadening

Hyperscalers have largely missed this year's rally on concerns heavy AI capex may not pay off

Source: Bloomberg

TSMC sales jump 36% but report lands amid regional tech selloff

[8:39 am] TSMC's June-quarter revenue matched elevated estimates, reinforcing intact AI demand ahead of Thursday's full result, even as investors weighed stretched valuations.

Revenue up 36% to NT$1.27tn (US$39.6bn), in line with ests

June revenue up 6.2% to NT$442.68bn, putting 2Q sales near the top of US$39-40.2bn guidance

CEO CC Wei warned in June the company cannot meet US-led demand for years despite new capacity coming online

2026 capex set at close to a record US$56bn, closely watched as a barometer of AI component demand

Bloomberg Intelligence sees AI and server demand offsetting smartphone and PC weakness, supporting gross margin above consensus 67.1% toward the 67.5% guidance top end

July 16 call likely to focus on whether tight leading-edge and packaging capacity can support higher spending

Source: Bloomberg

Trump restarts Iran blockade and floats 20% Hormuz toll as strikes escalate

[8:37 am] Trump reinstated the US blockade of Iranian shipping and demanded 20% reimbursement on all cargo crossing the Strait of Hormuz, driving Brent toward its biggest single-day jump since 2020 as a third night of strikes began and investors tore up ceasefire-era trades.

US forces resume blockading traffic to and from Iranian ports from 4pm New York time on July 14, with Trump declaring the US the strait's "guardian"

Brent crude jumped 10.76% to US$83.31, a one-day move fractionally larger than the 10.71% spike on 9-Mar-26

A 20% charge equals roughly US$32m for a fully loaded large crude carrier at current prices, versus the roughly US$2m tolls previously charged by Iran

Tanker traffic through Hormuz fell to a two-month low, with just six vessels transiting on Sunday and many switching off transponders, as ship-to-ship transfers off Oman rise to bypass the chokepoint

Collection authority is unclear, with the US not a party to UNCLOS and the IMO opposed to charging for passage through international straits

Iran called the peace deal in a "crisis phase" and refused to abide by it, with Foreign Minister Araghchi mocking the toll

Stocks slide as Trump reinstates Iran blockade, oil surges

[8:35 am] Wall Street fell and crude spiked after Trump announced a US blockade on Iranian shipping through the Strait of Hormuz, with a 20% charge flagged on all cargo transiting the lane.

S&P 500 down 0.79% to 7,515.34, Nasdaq down 1.55% to 25,873.18, Dow down 0.26% to 52,498.64

Breadth was surprisingly even, with the Equal-weight S&P 500 (-0.03%) outperforming the cap-weighted index by 76 bps as Energy stocks rallied, while classic defensives like Utilities, Financials, Staples and Real Estate outperformed

Escalation followed weekend airstrikes, with Iran declaring the strait closed and Trump disputing the claim

Semiconductors under pressure, SK Hynix down 9% after Friday's 13% Nasdaq debut pop, Micron down 4%, Sandisk down 12%, AMD down 4%, Intel down 6%

Major banks including JPMorgan, Goldman and Morgan Stanley slipped ahead of results this week, with Netflix, J&J and UnitedHealth also reporting

Analysts expect second-quarter S&P 500 profits grew more than 23% year-on-year

Good morning!

[8:28 am] ASX 200 futures are down 8 pts (-0.09%).

The overnight session in a nutshell:

Major US benchmarks broadly lower as a renewed US-Iran conflict and a semiconductor selloff drove a risk-off session

KOSPI tumbled 8.9%, its third largest one-day decline since Lehman as giants Samsung and SK Hynix both tumbled more than 10%

Oil jumped to one-month highs after Trump reinstated the Strait of Hormuz blockade and floated a 20% toll on all cargo

Yields are now trading back at uncomfortable levels, gold and silver prices tumbled 2-3% overnight, and mining stocks are tumbling towards year-to-date lows