ASX 200 Live Today - Monday, 27th April

The S&P/ASX 200 is set for a flat open despite another record setting session on Wall Street. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Monday, April 27. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 reverses early losses, still down for the day

[2:00 pm] That's a wrap. Another soft-ish session, but the ASX 200 finished down just 0.15%, well off session lows of -0.65%. The recovery was largely driven by the Materials Index, which fell 0.66% in early trade before rallying to close up 0.75%. Most other sectors stayed in the red.

The local market remains in a challenged state, weighed down by a persistent pullback in Financials (down ten of the last eleven sessions) and what's becoming a death spiral in healthcare. It's a rather odd place to be, watching our market grind through a five-day losing streak while the S&P 500 and Nasdaq keep printing fresh all-time highs.

On that note, 36% of the S&P 500 is due to report this week, including four of the Mag 7 names (on top of the FOMC meeting and Aussie inflation data). Throw in the ongoing Iran developments, and it's shaping up to be a wild week.

Analysts' take on IGO

[1:48 pm] IGO's March quarter result last Friday was a material disappointment, with Greenbushes production falling well short of expectations and prompting a significant downgrade to full-year production and cost guidance, driven by declining ore grades, weaker recoveries and persistent plant instability. The stock finished the session down 17.9%.

RBC Capital Markets maintained Sector Perform, lowered target from $9.00 to $8.00. Persistent operational misalignment between mine and plant, combined with deferred JV dividends, has materially reduced confidence in near-term cash returns, with Nova's solid performance insufficient to offset broader portfolio volatility.

Jarden maintained Neutral, lowered target from $5.50 to $5.30. The continued absence of operational momentum at Greenbushes, a deteriorating grade trajectory and JV opacity are compounding credibility concerns, with the stock offering limited near-term catalysts despite an apparent valuation discount.

JPMorgan maintained Overweight, lowered target from $10.50 to $8.50. Grade recovery timelines lack clarity and broader lithium market strength is failing to translate into shareholder returns, with improved transparency on the growth pathway seen as critical to any valuation rerating.

Macquarie's take on Newmont

[12:57 pm] Macquarie was impressed by Newmont's first quarter result last Friday, noting: "Q1 was exceptional and demonstrated the exceptional cash generation of the business. We believe the upsized share buyback demonstrates NEM's commitment to capital return to shareholders."

Q1 production of 1.30Moz vs. MQe 1.25Moz (4% beat)

Q1 AISC (by-product) of US$1,029/oz vs. MQe US$1,613/oz (~36% beat)

Adjusted EBITDA of US$5,154m was 21% ahead of MQe

Q1 dividend of US$0.26 cents per share was in-line with estimates

The analysts raised their target price by 1% to $192, with an Outperform rating.

China industrial profits accelerate in March

[12:51 pm] China's industrial profits grew at a faster pace in March as a rebound in producer prices offset cost pressures from the Iran war, though Bloomberg Economics flags risks ahead.

Industrial profits up 15.8% year-on-year in March, accelerating from 15.2% in Jan-Feb

Q1 profits up 15.5%, more than Bloomberg Economics had expected

Improvement follows a March uptick in factory prices after 3.5 years of deflation, lifted by higher oil and metal costs which likely supported upstream/mining earnings

Consumer-facing industries squeezed by higher raw material costs as they struggled to pass them through to customers

Source: Bloomberg

Goldman Sachs lifts oil price forecasts on prolonged Hormuz closure

[12:50 pm] Goldman Sachs has raised its Brent oil price forecasts as the prolonged closure of the Strait of Hormuz drives record inventory draws and a sharp deficit through 2026.

Q2 Brent forecast lifted to US$100/bbl, Q3 to US$93/bbl, and Q4 to US$90/bbl (up from US$80/bbl prior)

Q2 deficit estimated at 9.6 million b/d vs. a surplus a year ago, with Goldman flagging that even sharper demand losses could be required if the supply shock persists

Now assumes normalisation in Gulf exports by end-June (versus mid-May prior) with a slower production recovery

Goldman flags net upside risks to oil prices, unusually high refined product prices, product shortage risks and the unprecedented scale of the shock as risks beyond its crude base case

Source: Bloomberg

Healthcare stocks at fresh 8-year lows

[12:25 pm] The S&P/ASX 200 Healthcare Index is currently down 0.5%, trading at the lowest since February 2018. It's down 6.6% in the last four sessions, largely driven by Cochlear's ~40% one-day selloff last Thursday.

Despite being brutally oversold, Cochlear has continued to drift lower, down 2.5% today.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

TLX | Telix Pharmaceuticals | -2.8% | $14.48 | -48.0% |

COH | Cochlear | -2.5% | $94.94 | -64.3% |

RHC | Ramsay Health Care | -1.8% | $39.26 | 18.7% |

MSB | Mesoblast | -1.6% | $2.16 | 24.6% |

PME | Pro Medicus | -1.4% | $136.34 | -34.8% |

EBO | Ebos Group | -1.2% | $17.24 | -49.9% |

SHL | Sonic Healthcare | -1.2% | $20.09 | -21.1% |

RMD | Resmed | -1.1% | $30.56 | -12.7% |

FPH | Fisher & Paykel | -0.9% | $29.15 | -6.2% |

SIG | Sigma Healthcare | -0.4% | $2.78 | -8.9% |

ANN | Ansell | -0.3% | $26.67 | -10.4% |

CSL | CSL | 0.3% | $130.36 | -45.2% |

4DX | 4DMedical | 2.8% | $4.90 | 1617.5% |

Analysts' take on PLS Group

[11:37 am] PLS Group delivered a standout quarterly update on Friday, with record production and unit costs materially below guidance, reflecting structural benefits from the completed Pilgangoora expansion.

Analysts broadly praised operational execution and balance sheet strength, though sentiment diverged on valuation, with some brokers downgrading on the view that recent share price appreciation had absorbed much of the near-term upside.

Macquarie retained Outperform, target raised from $5.50 to $6.20. A strong production beat and below-consensus costs were highlights, with early signs of P2000 acceleration, including potential pre-FID spend in FY27, driving a 13% target price increase, though sub-optimal LiOH operating rates remain a near-term watch point.

Jarden downgraded to Underweight from Neutral, raised target from $2.50 to $2.60. While operational quality and management execution were acknowledged, the current valuation is seen as implying stretched long-term lithium price assumptions, warranting patience for a better entry point.

RBC Capital Markets maintained Outperform, raised target from $5.20 to $5.40. Structural improvements in plant reliability and recovery rates were highlighted as durable, with deferred shipments providing a near-term earnings tailwind, though elevated capex introduces some timing risk around P2000 delivery.

Lithium stocks rally

[11:35 pm] Lithium stocks are trading broadly higher, with Chinese lithium carbonate futures currently up 2.0% to 181,140 yuan a tonne.

Ticker | Company | % Chg | Price |

|---|---|---|---|

PAT | Patriot Resources | 17.35% | $0.12 |

VUL | Vulcan Energy Resources | 7.12% | $3.91 |

PMT | Pmet Resources | 6.73% | $0.59 |

AGY | Argosy Minerals | 6.33% | $0.08 |

CXO | Core Lithium | 6.15% | $0.35 |

ATC | Altech Batteries | 5.56% | $0.02 |

IGO | IGO | 5.49% | $7.40 |

INR | Ioneer | 5.19% | $0.14 |

WR1 | Winsome Resources | 4.35% | $0.48 |

PLS | PLS Group | 4.16% | $6.01 |

LTR | Liontown | 3.35% | $2.32 |

MIN | Mineral Resources | 1.68% | $60.37 |

GL1 | Global Lithium Resources. | -0.85% | $0.59 |

DLI | Delta Lithium | -1.30% | $0.23 |

Chinese lithium prices open higher

[11:02 am] Chinese lithium futures just opened, with prices up 3.1% to 183,2800 yuan a tonne. Prices are now just ~3% away from January highs of 189,400 yuan. This has driven a sharp U-turn for most lithium names, with PLS Group currently up 2.0% (vs. open of -0.3%).

Analysts' take on Suncorp

[11:01 am] Suncorp announced a five-year aggregate reinsurance arrangement last Friday, designed to reduce earnings volatility following elevated catastrophe losses in the first half, with management confirming underlying insurance trading ratio margins would remain within target range. The stock rallied 4.5% on the day.

UBS retained Buy, raised target from $19.25 to $19.60. Aggregate coverage meaningfully reduces catastrophe claims variability, and a capital target reduction funded by improved earnings visibility supports the case for the valuation discount to peers narrowing.

JPMorgan retained Neutral, target unchanged at $18.30. The agreement provides meaningful downside certainty on catastrophe outcomes and supports a capital target reduction, but the company will likely need a pricing and expense response to sustain margins through the cycle.

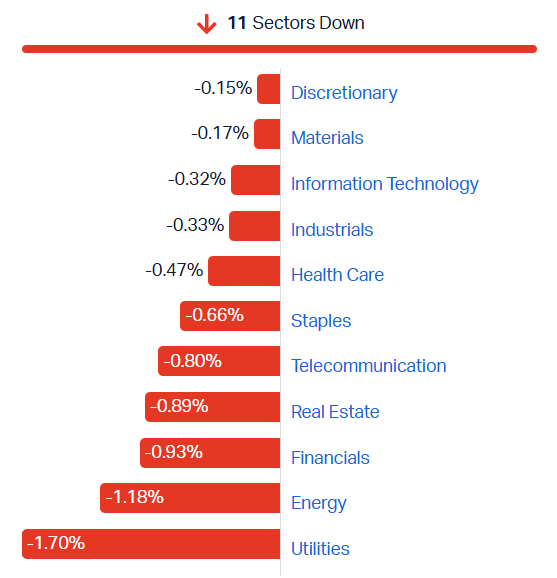

ASX 200 down for a fifth session, all sectors red

[10:59 am] Another weak session for the S&P/ASX 200, down 0.58% in early trade and on track for a fifth straight day of declines. All sectors are currently red, with 158 constituents (79%) trading lower.

Utilities weighed by Origin Energy (-2.8%), which reported a mixed quarterly update

Energy (-1.3%) lower after a 5.7% dip in Brent last Friday

Financials (-0.9%) now down ten of the last eleven sessions

Tech (-0.2%) faded early gains of 1.3%

S&P/ASX 200 sectors (Source: Market Index)

Analysts' take on Judo Bank

[10:23 am] Judo Bank reaffirmed FY26 pre-tax profit guidance last Friday, at $180–$190 million (at the lower end), while lifting its cost of risk guidance to 70–75 bps following a customer-by-customer loan review targeting fuel-sensitive sector exposures.

Morgans upgraded to Buy, target $2.09. The recent share price pullback has created a genuine buying opportunity, with current valuations not fully reflecting the growth potential of the challenger bank model.

JPMorgan retained Overweight, lowered target from $2.20 to $2.15. The update was largely anticipated, operational metrics remain healthy, and improving capital generation supports the case for eventual multiple expansion.

Goldman Sachs retained Buy, raised target from $2.18 to $2.20. Strong quarterly execution, new savings products outperforming, and an improving deposit franchise support confidence despite the broader uncertain environment.

Top ASX 200 gainers

[10:17 am] Newmont rallies off the back of its better-than-expected quarterly result last Friday, IGO bounces after a 17% selloff in the previous session and software stocks edge higher.

Ticker | Company | % Chg | Price |

|---|---|---|---|

NEM | Newmont | 6.36% | $165.49 |

OBM | Ora Banda Mining | 4.07% | $1.54 |

360 | Life360 | 3.12% | $21.50 |

GNE | Genesis Energy | 2.63% | $1.95 |

BRG | Breville Group | 2.62% | $31.48 |

IGO | IGO | 2.28% | $7.17 |

XRO | Xero | 1.61% | $82.82 |

4DX | 4DMedical | 1.47% | $4.83 |

ELV | Elevra Lithium | 1.41% | $12.21 |

GGP | Greatland Resources | 1.15% | $14.05 |

Top ASX 200 losers

[10:17 am] Relatively broad weakness among uranium, rare earths and utilities this morning.

Ticker | Company | % Chg | Price |

|---|---|---|---|

DYL | Deep Yellow | -4.51% | $1.91 |

RSG | Resolute Mining | -3.56% | $1.36 |

NXG | Nexgen Energy | -3.54% | $17.18 |

LYC | Lynas Rare Earths | -2.96% | $17.68 |

PDN | Paladin Energy | -2.70% | $12.27 |

LIN | Lindian Resources | -2.58% | $0.87 |

ORG | Origin Energy | -2.58% | $12.44 |

VEA | Viva Energy Group | -2.29% | $2.35 |

EDV | Endeavour Group | -2.00% | $3.43 |

ZIP | Zip Co | -1.80% | $2.46 |

Kogan launches on-market buyback

[9:44 am] Kogan has launched an on-market buyback of up 10% of outstanding shares, to run for 12 months from 13 May.

Kogan shares are down 15.6% in the last twelve months, with a current market cap of $365 million. The company's latest 1H26 result noted $71.8 million cash, with no external debt.

Company page: Kogan (KGN)

Altair Minerals raises $28m at a premium

[9:40 am] Altair Minerals is a $244 million market cap gold explorer advancing the Greater Oko Project in Guyana.

Placement of $28.2m to Endeavour Gold (a wholly owned subsidiary of Endeavour Mining) priced at 4.3 per share, representing a 5% premium to last close

On completion, Endeavour will hold a 9.90% stake in Altair, and both parties will establish a joint Technical Committee to share exploration expertise

Pro-forma treasury of approximately $40m will fund an expanded drill program of up to 50,000m (up from 30,000m), including multiple simultaneous rigs, accelerated geochemical programs at South Oko, and deployment of regional exploration teams across untapped greenstone terrain

Greater Oko spans 590km² and is the largest contiguous gold exploration landholding in Guyana's history, covering approximately 16km of strike along the Oko Shear Zone, which has already hosted over 9Moz Au in neighbouring discoveries

Company page: Altair Minerals (ALR)

Generation Life flags contained cyber incident via third-party provider

[9:39 am] GDG subsidiary Generation Life has suffered a cyber breach through a third-party service provider, though the company says core systems were unaffected and operations largely undisrupted.

Unauthorised access was limited to a part of Generation Life's network, detected quickly and immediately contained

The breach originated through a third-party service provider, with no impact reported on Evidentia Group or Lonsec Research and Ratings systems

Generation Life has engaged external cyber security experts and launched an investigation to determine the scope of the incident and whether any adviser or client data was compromised

Regulators including APRA, the OAIC, the ACSC and the National Office of Cyber Security have all been notified

Company page: Generation Development Group (GDG)

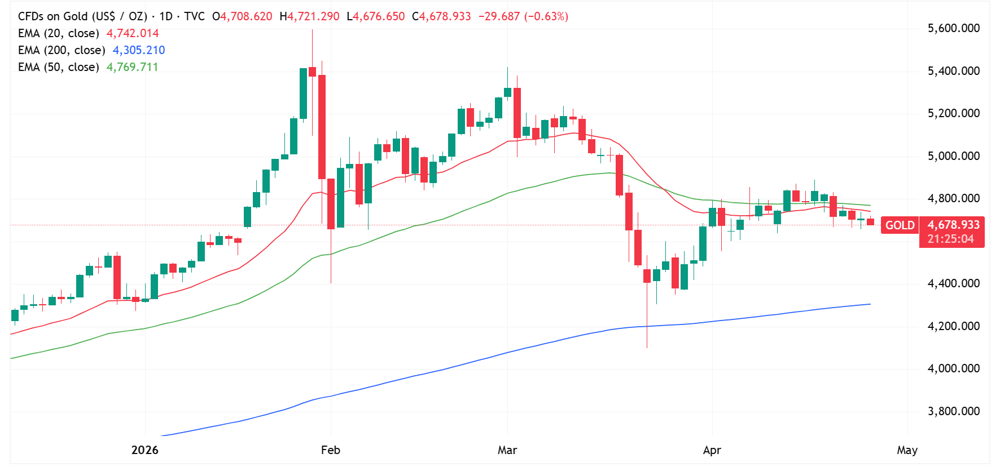

Gold slips in early trade

[9:38 am] Gold is tracking lower in early trade on Monday, down 0.6% to US$4,679.

Gold daily price chart (Source: TradingView)

IFM Investors tables "best and final" bid for Atlas Arteria

[9:28 am] IFM Investors is expected to launch a takeover bid for Atlas Arteria on Monday, lobbing a tiered offer that values the ASX-listed toll road operator at up to $7.4 billion, according to the AFR. IFM is already the company's largest shareholder with a 35% stake.

Base offer of $4.75 per share implies a deal value of $6.9bn

The offer steps up to $5.10 per share (19% premium, $7.4bn deal value) if acceptances combined with IFM's existing stake reach 45%, in a structure known as an accelerated creep

The "best and final" label applies only to the $5.10 price, and the base $4.75 offer sits above several broker targets, which vary from $4.31 to $5.43

IFM first built a 20% stake in 2022 but was diluted during Atlas Arteria's $3.1bn equity raise to fund the Chicago Skyway acquisition, with the stock down roughly 30% since then

A key condition requires no major portfolio changes, which could prove contentious given Canadian pension funds hold options to sell their Chicago Skyway stake, a clause some view as a potential poison pill that could trigger a large capital raising

Company page: Atlas Arteria (ALX)

Boab Metals completes project finance facility for Sorby Hills

[9:25 am] Boab Metals is seeking to develop its 100% owned Sorby Hills Silver-Lead-Zinc Project in WA, which hosts a 47.3 Mt resource at 123 g/t silver-equivalent. The latest feasibility study noted an NPV of $411 million and $126 million per annum in EBITDA.

Syndicate of $236m executed with Merricks Capital and Davidson Kempner, split equally between AUD tranches ($118m) and USD tranches (US$84.4m)

First drawdown expected in Q3 2026, with construction progressing well and all regulatory approvals in place

Construction is "progressing well" and project is on track for first concentrate production in the second half of 2027

Company page: Boab Metals (BML)

BOQ Chair Andrew Fraser lifts stake

[9:18 am] Bank of Queensland Chair Andrew Peter Fraser has disclosed an on-market purchase of ~18,000 shares, lifting his beneficial ownership by 150% to ~30,000 shares.

BOQ suffered a 9.0% selloff last Wednesday, after reporting a softer-than-expected 1H26 result. The key numbers included:

Cash NPAT down 4% to $176m vs $181.7m ests (3% miss)

Net interest income up 4% to $755m vs $766m ests (1% miss)

NIM down 3 bps on 2H25 to 1.67%, reflecting a highly competitive environment and non-repeat of prior half cash rate benefits, partly offset by improved asset mix and funding spreads

NIM of 1.67% represents a wide miss vs. Macquarie ests of 1.73% (Apr-26)

Interim fully-franked DPS up 11% to 20 cents vs 19.6 cents ests (2% beat)

Home lending contracted 4% on 2H25, while commercial lending grew 7% on 2H25 (above system)

Company page: Bank of Queensland (BOQ)

Megaport's Latitude secures $25 million compute and storage contract

[9:12 am] Megaport's wholly owned subsidiary Latitude.sh has signed a 36-month compute and storage contract worth $25.1 million with a US-based developer tooling customer, alongside a strong update on Network ARR growth.

Contract is worth ~US$8.4m (A$11.8m) in ARR, expected to commence in H1 FY27

Contract supported by ~US$12.2m (A$17.2m) in incremental capex on CPU servers, with a ~24-month payback; counts toward the US$86.0m capex commitment for CY26/CY27 from the Latitude.sh acquisition

Compute ARR for Latitude.sh's on-demand product (ex-this deal) up 31% to US$58.7m from US$45.0m at 31 December 2025

Megaport Network ARR (incl-India) of $272.0m at 31 March, up 23% year-on-year

CEO Reid flagged "explosion in AI use cases" driving demand for compute and storage, with CPUs remaining a critical component of AI infrastructure

In the same update, Megaport reaffirmed it FY26 guidance, including $302-317 million in revenue and EBITDA to be 21-24% of revenue.

Company page: Megaport (MP1)

Origin reports lower Q3 APLNG production, downgrades Octopus FY26 guidance

[9:06 am] Origin Energy delivered a softer March quarter with APLNG production and revenue easing on fewer days and natural field decline, while a sharp downgrade to Octopus Energy FY26 EBITDA guidance reflects UK regulatory headwinds and adverse weather.

APLNG production (100% basis) down 2.7% quarter-on-quarter to 164.5 PJ, reflecting two fewer days (~4 PJ) and natural field decline

APLNG sales volumes down 6.0% to 159.3 PJ

APLNG commodity revenue down 11.4% to $1.86bn, on lower realised LNG prices (AUD strength) and lower sales volumes

Realised average LNG price of US$9.51/mmbtu and average domestic price of $4.30/GJ, both slightly lower QoQ

Energy Markets electricity sales up 9.3% to 9.4 TWh, with strong growth in business volumes driven by the data centre sector

Energy Markets natural gas sales down 31.5% to 27.2 PJ, on lower trading volumes and gas demand for power generation

Octopus Energy (ORG share) FY26 EBITDA guide cut to -$70m to +$30m, down from prior $0-$150m, driven by the wind-down of the UK ECO scheme, higher gas capacity charges and adverse UK weather in Feb/March

CEO Calabria flagged Middle East conflict impacts on oil/LNG, but noted lagged effect on APLNG long-term export contracts means no flow-through expected until FY27

Company page: Origin Energy (ORG)

Jarden reshuffles Australian retail ratings with broad target cuts

[9:01 am] Jarden upgrades JB Hi-Fi and Wesfarmers while downgrading Flight Centre and Harvey Norman, though target prices were trimmed across all four names.

JB Hi-Fi upgraded to Buy from Overweight; target lowered to $87.90 from $88.90

Wesfarmers upgraded to Neutral from Underweight; target lowered to $74.50 from $77.30

Flight Centre downgraded to Overweight from Buy; target lowered to $16.70 from $18.00

Harvey Norman downgraded to Neutral from Overweight; target lowered to $5.40 from $6.60

JB Hi-Fi shares have fallen ~34% since late October, trading at the lowest level since August 2024. The "upgrades" are really just a function of the price drop, with the stock now ~15% below analysts' target prices, therefore the implied upside is enough to justify an "Overweight" rating. The target price cuts, meanwhile, reflect trimmed earnings expectations. In other words, the upgrade is cosmetic, while the underlying fundamentals have softened.

Southern Cross Media appoints Rohan Lund as MD and CEO

[8:55 am] Rohan Lund will step into the MD and CEO role at Southern Cross Media on 1 May, bringing extensive media and digital transformation experience to the position.

Lund joined the board as a Non-Executive Director on 1 March 2026 and transitions to MD and CEO on 1 May 2026

He previously served as Group CEO of the NRMA from 2016 to 2025, leading its transformation into a diversified transport, tourism and services group

Prior media and telco experience includes COO of Foxtel, Group COO of Seven West Media, founding CEO of Yahoo!7, and Chief Strategy Officer at Singtel Optus

Company page: Southern Cross Media Group (SXL)

S&P 500 Q1 earnings season off to a strong start

[8:52 am] With 28% of S&P 500 companies having reported, early Q1 results are tracking well ahead of expectations across both earnings and revenue, according to Factset.

Blended EPS growth stands at 15.1%, above the 13.2% forecast at quarter-end, with blended revenue growth at 10.3%

84% of companies have beaten consensus EPS ests, above both the one-year average of 79% and the five-year average of 78%

81% have exceeded consensus revenue ests, ahead of the one-year average of 73% and the five-year average of 70%

In aggregate, companies are beating EPS ests by 12.3%, well above the one-year average of 7.2% and the five-year average of 7.3%

Bullish vs. bearish talking points

[8:52 am] A look at the key bullish and bearish narratives shaping markets this week, spanning Middle East dynamics, Q1 earnings, AI capex and Fed leadership.

Bulls

Ceasefire extension supported the US-Iran de-escalation narrative, with second-round negotiations potentially soon

S&P 500 Q1 blended earnings growth tracking just over 15%, up from 12.6% at the start of earnings season, ~82% of reporters beating, with aggregate upside surprise of ~12.3%

AI compute and infrastructure demand remains the dominant secular earnings theme, with semis (SOX on an 18-day winning streak), power, construction and data centre infrastructure names leading; Q1 also showing more company effort to quantify AI productivity benefits

Macro data solid: Core US retail sales +0.7% m/m in March (vs. +0.2% ests), April flash manufacturing PMI and its output/new orders components at ~4-year highs

DOJ dropped the criminal probe into Fed Chair Powell, paving the way for Kevin Warsh's confirmation

Blackstone pushed back on private credit concerns, noting ~75% of credit platform AUM is institutional/insurance, with low leverage and meaningful loss reserves

Bears

Second-round US-Iran ceasefire talks scrapped, with Strait of Hormuz tensions escalating (Iran firing on ships and reportedly laying mines the Pentagon estimates could take six months to clear)

JPMorgan flagged complacency on energy supply, noting outsized demand destruction already despite non-extreme prices, suggesting forced demand loss from physical shortages

Input cost pressures broadening across earnings and macro data: airlines hit by jet fuel spike, plus higher freight, packaging, feedstocks and memory costs; April flash composite PMI input prices highest since mid-2022

Capex concerns rising, with Tesla's $5bn lift to 2026 capex guide ($25bn, nearly 3x 2025) overshadowing its earnings beat and pointing to negative FCF

Software earnings off to a rough start, with ServiceNow down ~18% Thursday on Middle East-driven deal slippage, more muted cRPO upside and only a reiterated organic guide

Flow/sentiment shift, with systematic re-risking momentum fading and Goldman modelling $25bn of pension selling for month-end (largest non-quarterly estimate on record)

Intel beats on Q1 with strong AI-driven demand, lifts Q2 guide

[8:45 am] Intel delivered a sharp Q1 beat on revenue, EPS and gross margin, citing unprecedented demand for silicon in the AI era, and guided Q2 well above expectations.

Revenue up 7% to $13.58bn vs. $12.3bn ests (10% beat)

Adj. EPS up 123% to $0.29 vs. $0.01 ests (significant beat)

Gross margin of 41.0% vs. 34.5% ests (650bps beat)

Data Center & AI revenue up 22% to $5.1bn

Intel Foundry revenue up 16% to $5.42bn vs. $4.81bn ests (13% beat)

Q2 guidance

Revenue of $13.8bn to $14.8bn vs. $13.04bn ests (10% beat)

Adj. EPS of $0.20 vs. $0.086 ests (133% beat)

Gross margin of 39.0% vs. 36.5% ests (250bps beat)

CEO commentary

“The next wave of AI will bring intelligence closer to the end user, moving from foundational models to inference to agentic. This shift is significantly increasing the need for Intel’s CPUs and wafer and advanced packaging offerings."

“A year ago, the conversation about Intel was about whether we could survive. Today, it’s about how quickly we can add manufacturing capacity.”

"In recent months, we have seen clear signs that the CPU is reinserting itself as the indispensable foundation of the AI era. CPU now serves as the orchestration layer and critical control plane for the entire AI stack. "

Taiwan regulator lifts fund cap on TSMC, unlocking billions in potential inflows

[8:43 am] Taiwan's financial regulator has raised the single-stock fund holding limit from 10% to 25%, a move that could channel over $6 billion into TSMC and push the broader Taiex index higher.

JPMorgan estimates the rule change could attract more than $6bn in inflows into TSMC, and says the Taiex could reach 40,000 points, implying a ~6% gain from recent levels

The old 10% cap had become increasingly restrictive as TSMC's weighting in the Taiex surpassed 44%, leaving domestic funds unable to participate fully in the AI-driven rally

The new rule applies to local equity funds and active ETFs investing solely in Taiwanese stocks, allowing up to 25% exposure in any listed company whose index weighting exceeds 10%

JPMorgan also upgraded Taiwan to overweight, citing easing monetisation concerns and rising hardware pricing as additional tailwinds

Concentration risk remains a key concern, with TSMC making up over 44% of the Taiex and 13% of the MSCI Emerging Markets Index, meaning a sharp sell-off in the stock could have outsized market-wide consequences

Source: Bloomberg

Google to invest up to $40bn in Anthropic

[8:40 am] Google will invest $10 billion in Anthropic now with another $30 billion to follow if performance targets are hit, alongside a major expansion of Google Cloud capacity, as the two AI rivals tighten their commercial ties.

Initial $10bn cash investment at a $350bn valuation, in line with Anthropic's February funding round, with up to $30bn more contingent on performance milestones

Google Cloud to provide 5 gigawatts of computing capacity to Anthropic over the next five years, with several more gigawatts potentially to follow, expanding the recent Anthropic/Google/Broadcom deal

Follows Amazon's $5bn investment earlier this week at the same $350bn valuation, with an option to add another $20bn over time

Anthropic considering an IPO as soon as October, with Claude Code and Cowork agent driving rapid demand growth and infrastructure needs

Source: Bloomberg

DOJ closes Powell probe, clearing path for Warsh confirmation

[8:38 am] US Attorney Jeanine Pirro closed the criminal investigation into Fed Chair Powell over Fed headquarters cost overruns, sharply lifting odds that Trump's nominee Kevin Warsh is confirmed before Powell's term ends on 15 May.

Investigation has been turned over to the Inspector General, though Pirro left the door open to restart the criminal probe if facts warrant

GOP Sen. Tillis had reiterated he would block the nomination until the investigation was dropped or completed, with other key GOP Senators floating a special Congressional committee to examine renovations

Kalshi odds of Warsh being confirmed before 15 May surged to 84% from 28% prior to the announcement

Policy-sensitive 2-year yield rallied on the news, with markets now pricing ~8bp of cuts from the current midpoint, up from ~3bp prior, signalling a more dovish path with Warsh seated sooner than expected

Trump's words drive biggest market swings in modern memory

[8:37 am] Trump's public comments and social media posts have become the single biggest catalyst behind the S&P 500's largest daily moves, an unprecedented level of influence according to Fundstrat analysis.

Trump's remarks have driven the five best and five worst days for the S&P 500 since he took office in January, more than any president going back to Reagan in 1981

Notable sessions: +9.5% on 9 April 2025 (tariff pause), +3.3% on 12 May 2025 (US-China 90-day truce), -6% on 4 April 2025 (China retaliation), -4.8% on 3 April 2025 (sweeping tariffs)

Volatility now extends to commodities, with oil market volatility hitting levels last seen at the onset of Covid-19

Counterpoint from Barclays: VIX has averaged 19.3 across Trump's second term, in line with Biden's term and the long-run average since 1990, suggesting the cadence of communication has changed rather than the magnitude of reactions

Passive investing amplifies the effect, with markets estimated to be 4-5x more reactive to headlines than historically

Source: Bloomberg

Semiconductors power S&P 500 and Nasdaq to fresh records

[8:35 am] US stocks diverged lats Friday as a blistering chip rally drove the Nasdaq and S&P 500 to record highs, while the Dow slipped ~0.2%.

Philadelphia Semiconductor Index rose for an 18th straight session since 30 March, with the VanEck Semiconductor ETF up roughly 40% over that stretch, a record 18-day rally since inception

Semis now make up 15.5% of the S&P 500 and have driven 4.9 ppts of the index's 12.8% rally since 30 March, accounting for around 40% of the gains

Intel up 23.7% post-earnings (best day since 1987) on a revenue beat and sharp gross margin beat, breaking above its dot-com era highs; Nvidia added US$260bn in market cap to retake the US$5tn crown, now US$1tn ahead of Alphabet at US$4.1tn

Good morning!

[8:23 am] ASX 200 futures are down 3 pts (-0.03%) as of 8:30 am AEST.

The overnight session in a nutshell:

S&P 500 (+0.80%) and Nasdaq (+1.63%) closed at fresh all-time highs as blowout Q1 earnings from Intel ignited tech stocks

Intel shares up 23% on broad earnings and guidance beat, largest rally since 1987

Nvidia (+4.3%) rallied back above US$5 trillion market cap, while the Philadelphia Semiconductor Index rose for an 18th consecutive session

Market breadth was poor, with defensive and value-oriented sectors struggling, the Dow (-0.16%) and Equal-weight S&P 500 (-0.21%) finished red

Markets eager to move on from US-Iran conflict, though ongoing ceasefire and peace talks remain fragile