Pilbara Minerals, Lynas Rare Earths, Liontown, WA1 Resources... 2025 Diggers & Dealers Mining Forum Day 2 highlights

All the big movers and shakers from Day 2 of this year's Diggers & Dealers Mining Forum 2025 that kicked off Monday.

Source: Shutterstock

Mentioned

KEY POINTS

- Everyone who’s anyone in ASX mining is at the Diggers & Dealers Mining Forum 2025!

- This year’s event will see 67 of the ASX’s most important mining companies share their latest progress and try to convince investors to part with their hard-earned cash.

- We bring you the latest updates from the likes of Pilbara Minerals, Lynas Rare Earths, Liontown Resources, Northern Star, Deep Yellow, WA1 Resources and many more...

The Diggers & Dealers Mining Forum is back for 2025! It's hands down the biggest annual mining get together in Australian, and is one of the biggest and most influential globally, too. Diggers & Dealers serves as a vital platform for mining executives to showcase their projects and attract investors' attention (and no doubt for striking the odd deal!).

Tuesday saw Day 2's delegates, some 23 of them, discuss their latest progress, key wins, and upcoming challenges. Given not everyone can be in Kalgoorlie to see our mining elite present live, we thought we’d bring you the key takeaways from the day.

So, in market capitalisation / alphabetical order, find below summaries of what we thought were the 12 most interesting presentations from Diggers & Dealers 2025 Day 2:

Mid-Large Cap (>$500 million market capitalisation)

Deep Yellow (DYL) - Andrew Mirco, Head of Business Development & Darryl Butcher, Head of Project Development

Greatland Resources (GGP) - Shaun Day, Managing Director

Liontown Resources (LTR) - Tony Ottaviano, Managing Director & Chief Executive Officer

Lynas Rare Earths (LYC) - Alex Logan, General Manager, Development

Northern Star Resources (NST) - Simon Jessop, Chief Operating Officer

Ora Banda Mining (OBM) - Luke Creagh, Managing Director

Pilbara Minerals (PLS) - Dale Henderson, Managing Director & Chief Executive Officer

WA1 Resources (WA1) - Paul Savich, Managing Director

Small Cap (<$500 million market capitalisation)

Antipa Minerals (AZY) - Roger Mason, Managing Director & Chief Executive Officer

Arafura Rare Earths (ARU) - Darryl Cuzzubbo, Managing Director & Chief Executive Officer

Gorilla Gold Mines (GG8) - Charles Hughes, Chief Executive Officer

Larvotto Resources (LRV) - Ron Heeks, Managing Director

Be sure to also read: Diggers & Dealers Day 1's Summaries

>>> Mid-Large Cap (>$500 million market capitalisation) <<<

Deep Yellow (ASX: DYL)

Presentation: N/a

12 month price chart

Deep Yellow presented a compelling vision for becoming a leading global uranium producer, underpinned by its diversified asset base across Namibia and Australia. Andrew Mirco, Head of Business Development, outlined the company’s plan to produce over 10Mlb of uranium annually within a decade by sequentially developing its Tumas, Mulga Rock, and pipeline projects.

The Tumas Definitive Feasibility Study (DFS) confirmed robust economics, and detailed engineering is now approximately 50% complete, but a Final Investment Decision (FID) was deferred pending long-term uranium price support. Mirco also highlighted the sector’s growing demand amid global energy security concerns and a nuclear renaissance, with small modular reactors (SMRs) and new reactor builds driving exponential uranium needs.

,%20Incorporating%202025%20DFS%20Results.png)

Deep Yellow, Tumas Project Analysis (US dollars), Incorporating 2025 DFS Results

Darryl Butcher, Head of Project Development detailed Deep Yellow’s transformative work at Mulga Rock, now a globally significant resource at 105Mlbs U3O8. New discoveries of critical minerals (copper, nickel, cobalt, and rare earth elements (REEs)) will materially offset uranium production costs.

The team’s innovative processing approach, including resin-in-pulp extraction and recycled process water, aims to produce uranium at very low quartile costs. A revised DFS incorporating by-products is underway and due in 2026, with Butcher noting the development strategy remains within existing approvals – critical in uranium.

Greatland Resources (GGP) (ASX: GGP)

Presentation: Investor Presentation - Diggers and Dealers 2025

12 month price chart

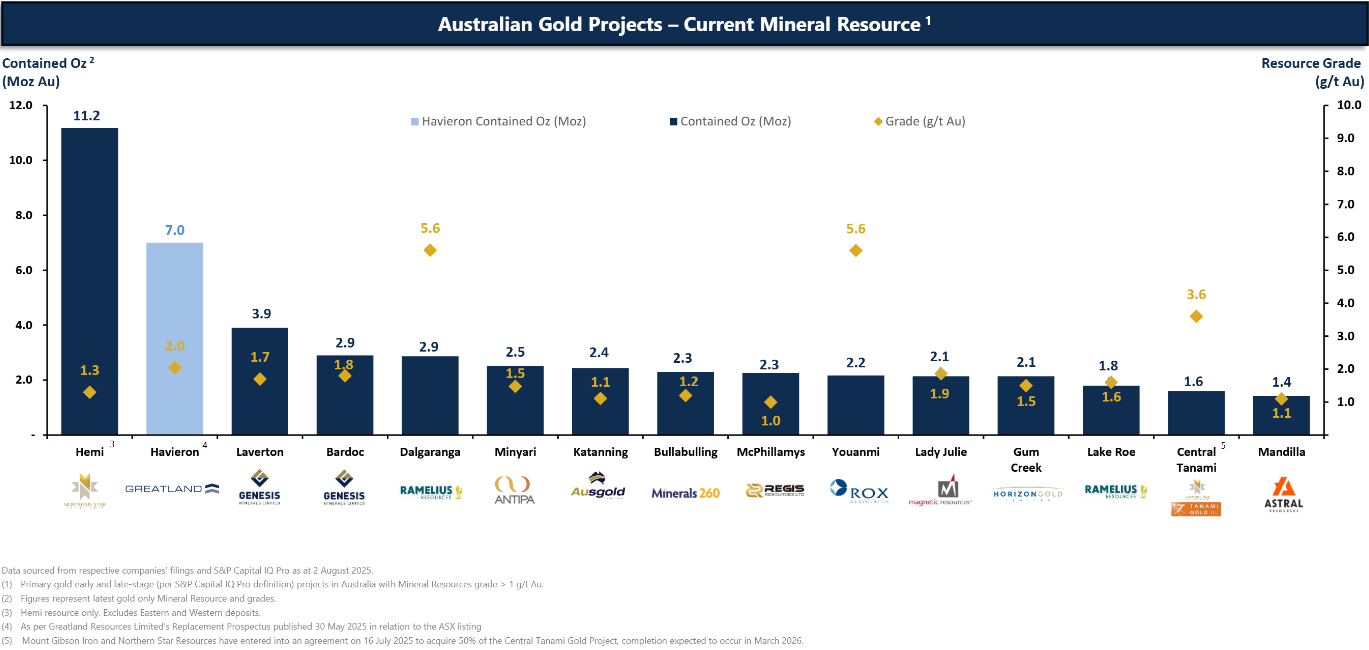

Greatland Resources touted its transformation into a significant, cash-generating Australian gold miner following its acquisition of the Telfer and Havieron assets in WA’s Patterson Province. MD Shaun Day outlined production of 198,000oz gold equivalent in the first 7 months of Telfer ownership, generating over $600 million in free cash flow, and that the company had ending FY25 debt-free with $575 million in cash. FY26 guidance of 260–310koz at AISC of A$2,400–2,800/oz reflects a conservative outlook amid asset transition.

Greatland Resources, Havieron is the second largest undeveloped gold project in Australia (click here for full size image)

{kind=link}

Day emphasised Telfer’s status as Australia’s third-largest gold processing centre, with two 10Mtpa trains offering scale, optionality, and future leverage. Over 240 square km of drilling is planned in FY26 – Telfer’s biggest exploration campaign in 50 years – targeting life extension and new underground zones like West Dome.

Greatland Resources, Havieron is the second largest undeveloped gold project in Australia (click here for full size image)

{kind=link}

Havieron, just 45km away, is a high-grade, low-capex brownfield project with over 7,900oz per vertical metre over a 1km vertical extent, and is expected to deliver outstanding economics. A DFS is due by end-2025, with plans to grow to 4–4.5Mtpa operating capacity via a second decline and conveyor.

Greatland's vision is to operate the region as a unified, long-life gold system, supported by unmatched infrastructure, talent, and community partnerships.

Liontown Resources (ASX: LTR)

Presentation: Investor Presentation - Diggers and Dealers 2025

12 month price chart

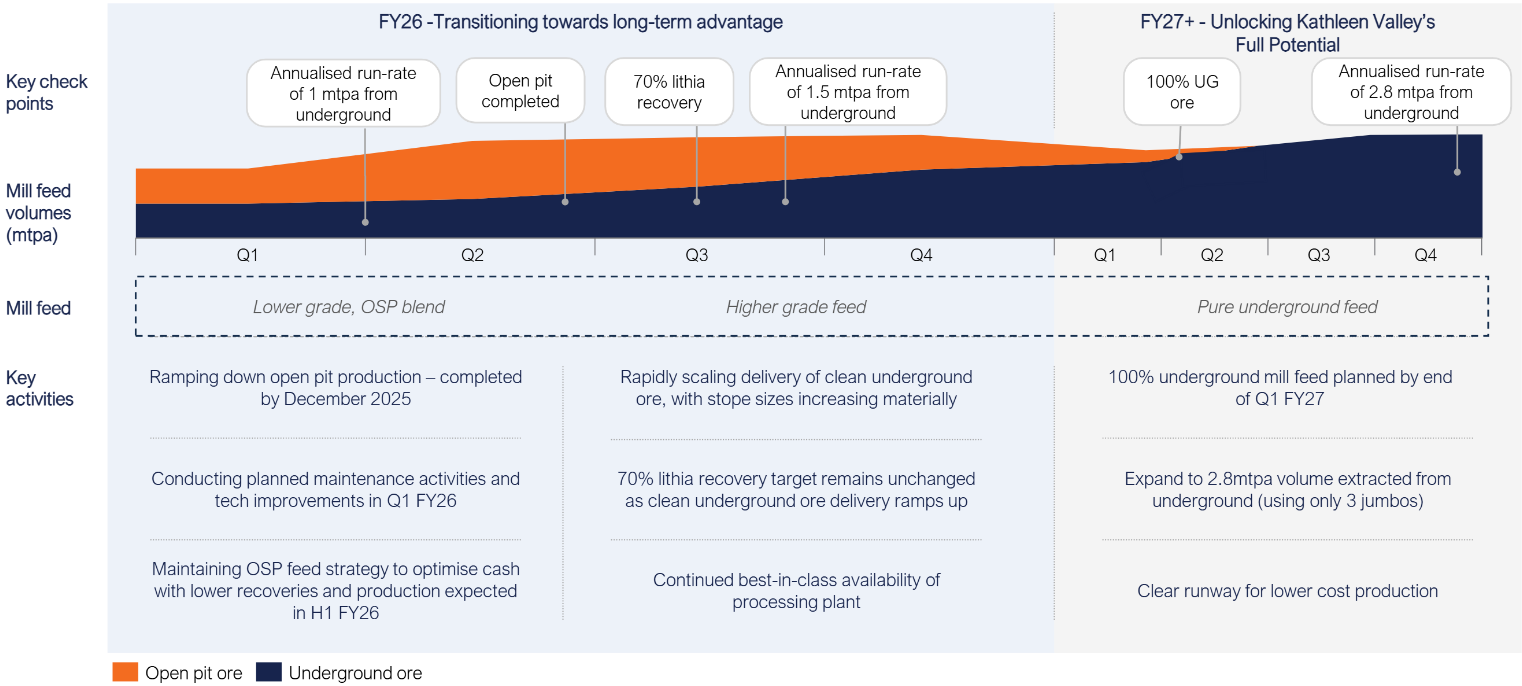

Liontown CEO Tony Ottaviano opened with trademark flair, joking, “I wore my gold tie… hoping to get some gold magic onto the lithium price!” He reaffirmed Liontown’s three-horizon strategy, with the immediate focus being to unlock the full potential of its flagship Kathleen Valley Project.

Ottaviano noted the company has achieved several milestones over the past year, including:

First shipment to LG in September 2024

A business optimisation plan delivering $112 million in savings and deferrals

Start of underground production at Kathleen Valley in April 2025

Commissioning of Australia’s largest paste plant (4Mt p.a.)

Ottaviano stressed the company’s ESG leadership, highlighting their 95-megawatt hybrid renewable power station, and a carbon footprint under 100,000t enabling fast-track approvals: “Our first tonnes to market were earlier than otherwise would have been the case.”

4. Liontown Resources, Value accretive action taken to set a strong foundation for long-term value (click here for full size image)

{kind=link}

Production at Kathleen Valley over 11 months reached 321,000t, with plant availability exceeding 89%. FY25 revenue hit $300 million, with a cash balance of $156 million. Liontown aims to be 100% underground-fed by FY27. Ottaviano concluded: “We’re well positioned for the recovery in lithium prices… and we haven’t torched the future – we’ve retained expansion optionality.”

Lynas Rare Earths (ASX: LYC)

Presentation: Diggers & Dealers Presentation 2025

12 month price chart

Lynas Rare Earths GM Alex Logan outlined the near-completion of the company’s Lynas 2025 strategy, capping a $1.5 billion investment across its Australian and Malaysian assets. The transformation includes two new plants, the Kalgoorlie Rare Earths Facility and the expanded Mount Weld operation near Laverton.

Mount Weld’s ore reserve now stands at 32Mt at 6.4% TREO, supporting a 20 year plus mine life. Its expansion has quadrupled throughput capacity to 1.3Mt p.a., enabling 12,000t of NdPr production. Commissioning of new circuits, flotation cells, and SAG mills is under way. Sustainability initiatives include a hybrid renewable power station (70% renewables when fully online) and 90% water recycling through a state-of-the-art treatment facility.

Logan proudly announced Lynas as the only commercial-scale producer of separated heavy rare earths outside China, following successful dysprosium and terbium production. This milestone unlocks pricing power and strategic leverage across defense, electronics, and magnet markets.

Lynas is forging strategic supply partnerships, including with Korean firm JSLink, and remains a central player in building secure, diversified global supply chains. Logan concluded: “Despite a decade of operation, we remain a growth stock in a growth market.”

Northern Star Resources (ASX: NST)

Presentation: Investor Presentation - Diggers & Dealers 2025

12 month price chart

CEO Simon Jessop opened with a tribute to the 30-year milestone of continuous mining at Kanowna Belle, which has produced over 7.2Moz of gold since 1995. “Back then, gold was A$550 per ounce,” Jessop noted. “Today, it’s over A$5,100.”

Despite a challenging FY25, largely due to timing at KCGM, Northern Star has delivered:

1.63 million ounces at an AISC of A$2,163/oz

Group reserves of 22Moz and resources of 70Moz

$3.2 billion in net mine cash flow over four years

FY25 shareholder returns of $1.4 billion in dividends (total $2.4 billion since 2012)

Northern Star Resources, Positioned for the next decade

At KCGM, the East Wall remediation is complete, setting the stage for higher-grade ore from Golden Pike North and the $1.5 billion mill expansion (due FY27), which will lift nameplate capacity to 27Mt p.a. Jessop highlighted growth across all hubs:

Yandal Hub (Jundee + Thunderbox): guiding 500–550koz/yr, with $430 million FY25 cash flow

Pogo (Alaska): 283koz FY25, $297 million cash flow; new portals to access high-grade (10 g/t) Goodpaster and Central Veins

Hemi (Pilbara): 11Moz resource, low-cost, long-life asset awaiting approvals. Jessop sees it as “the next leg of the journey.”

Northern Star is now transitioning from heavy capex into strong, sustained cash generation, with future optionality across its world-class portfolio, he noted.

Ora Banda Mining (ASX: OBM)

Presentation: Corporate Presentation - Diggers and Dealers

12 month price chart

Ora Banda Mining’s MD, Luke Creagh, presented a compelling case for why FY26 marks a pivotal turning point in the company’s evolution. He opened by reflecting on the past three years of transformation, where the business shifted its strategy from chasing surface gold in under-capitalised open pits to a more sustainable underground mining model. The result has been the successful commissioning of two underground operations, Riverina and Sand King, with a third and fourth likely on the horizon.

Financially, Ora Banda is in its strongest position to date. Cash grew from $26 million to $84.2 million in the past year, despite $124 million in capital investment. The company has also secured a $50 million revolving credit facility to support future expansion. Production is ramping up rapidly, with FY25 expected to deliver 100,000oz and FY26 tipped to generate $750 million in revenue, underpinned by a transition to dual underground mining and a proposed mill expansion to 3Mt p.a.

Ora Banda Minning, Strategy change to focus to underground delivered record revenues and strong cash flows

Looking ahead, Creagh unveiled an ambitious $73 million drilling program spanning 330km – nearly double the previous three years combined. The lion’s share will focus on four key targets: Sand King, Little Gem, Wahi, and Round Dam. He highlighted encouraging results from Little Gem, where strong intercepts suggest significant potential over a 1.6km strike, and described Wahi and Round Dam as misunderstood systems with untapped underground upside.

Creagh concluded by saying Ora Banda’s next phase is about right-sizing the business for long-term value creation: scaling the mill, unlocking new deposits, and building a multi-asset, lower-risk, high-margin gold producer capable of delivering consistently strong returns.

Pilbara Minerals (ASX: PLS)

Presentation: Diggers & Dealers Conference 2025 Presentation

12 month price chart

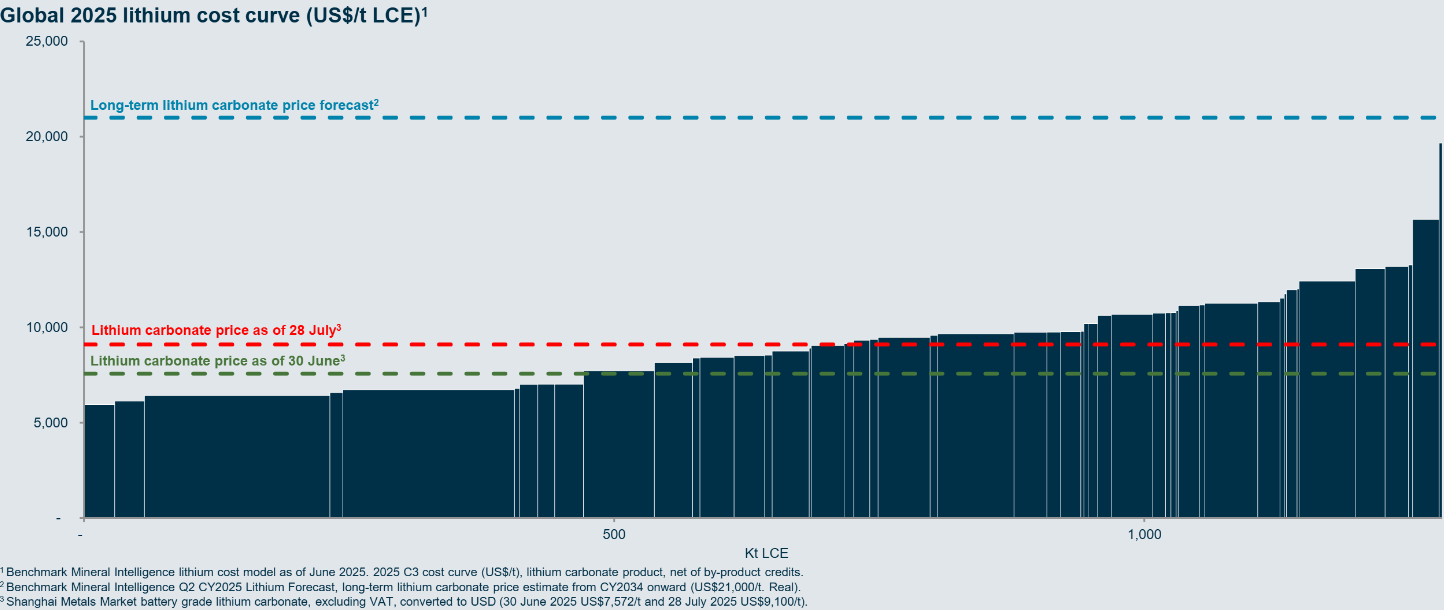

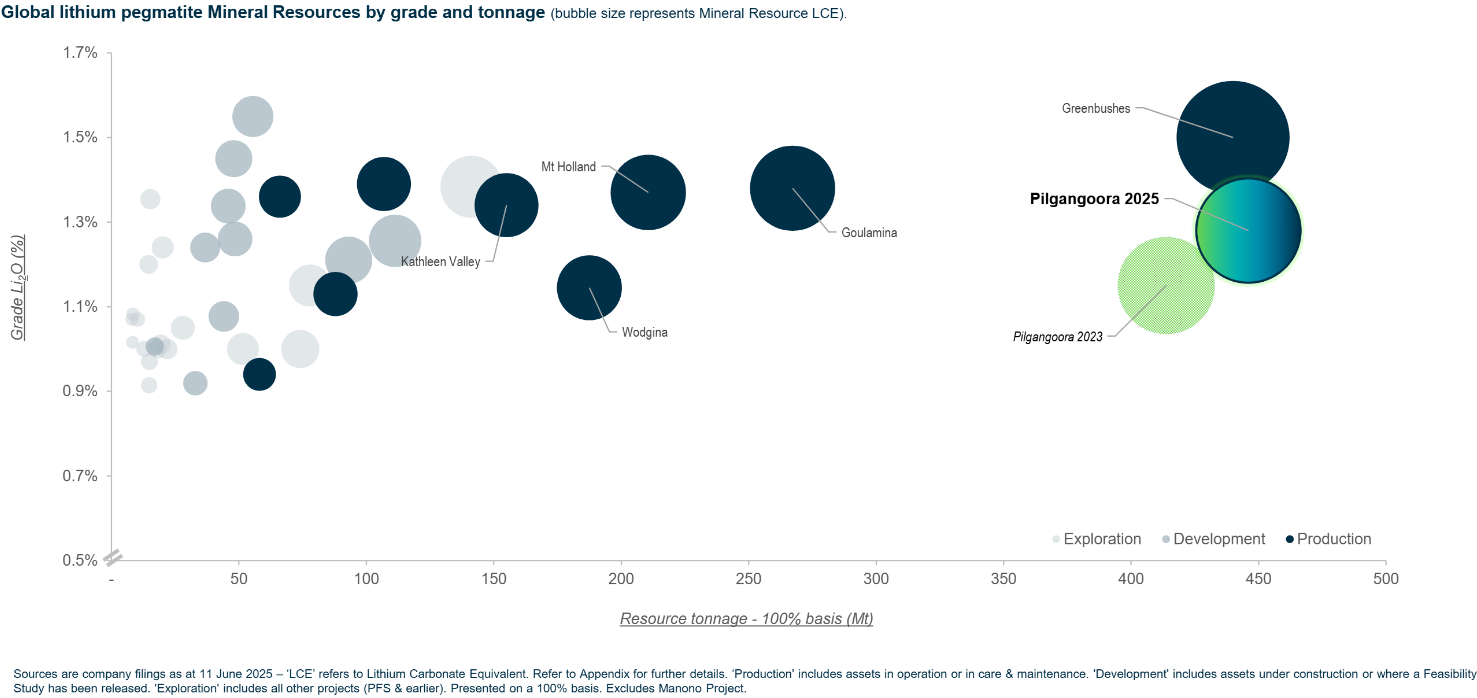

Pilbara Minerals CEO Dale Henderson described FY25 as a transformational year, marked by strategic execution and disciplined investment amid challenging market conditions. While lithium prices slumped through 2023 and early 2025, PLS delivered record production, completed its multi-year investment cycle, and brought its P1000 processing facility online—on time, under budget, and with improved lithium recoveries and unit cost reductions.

Pilbara Minerals, Lithium paradox: Demand rising. Pricing detached (click here for full size image)

{kind=link}

Pilgangoora’s total resource was upgraded to 446Mt, a 23% increase in contained lithium. The company also expanded globally, acquiring Brazil’s Kina project in a counter-cyclical, all-scrip deal, giving PLS an Atlantic-facing growth platform. It now holds roughly $1 billion in cash, backed by a new $1 billion revolving credit facility. A joint venture with POSCO added downstream lithium hydroxide production to its portfolio, offering margin expansion and geographic diversification outside China.

Pilbara Minerals, Pilgangoora Resource upgraded (click here for full size image)

{kind=link}

Henderson remained bullish on long-term demand, citing record EV and energy storage growth, and the rising impact of next-gen technologies like AI. “We haven’t wasted this part of the cycle,” he said. “We’ve used it to fortify our foundations and scale up. With more scale, a lower cost base, and greater strategic reach, we’re not just riding the cycle, we’re positioned to help shape it,” he said.

WA1 Resources (ASX: WA1)

Presentation: Diggers & Dealers Mining Forum Presentation

12 month price chart

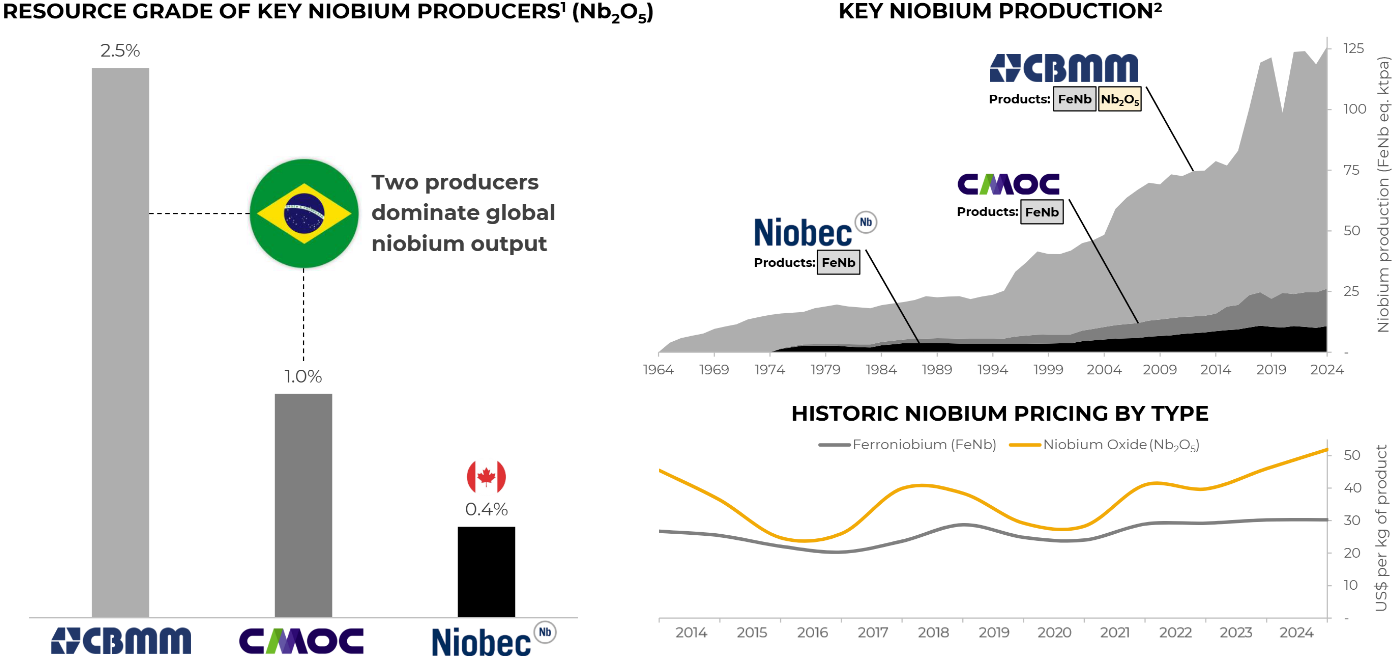

WA1 Managing Director Paul Savich delivered a confident and data-rich update on the company’s world-class niobium discovery at the Luni project in Western Australia. With just three operating niobium mines globally (2 are in Brazil), WA1’s Luni deposit is emerging as a major new source of supply in a highly concentrated market.

Savich noted that niobium is essential in steelmaking, aerospace, and defence, and sells for up to US$30,000/t in ferroalloy form, with purer niobium oxide fetching even more. He went on to emphasise Luni’s strategic significance, noting that China, which consumes 37% of global niobium, has no domestic supply.

WA1 Resources, From emerging to essential in 60 years (click here for full size image)

{kind=link}

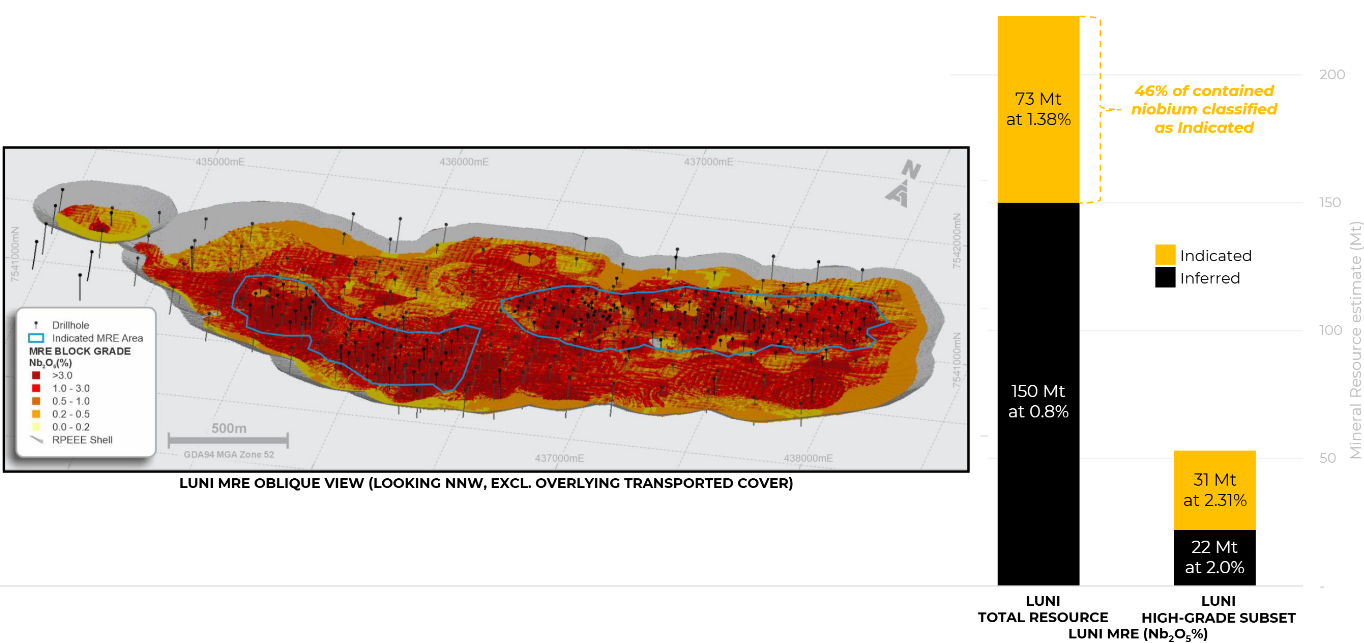

WA1's recent resource upgrade confirmed 220Mt at 1% Nb₂O₅, including 31Mt at 2.3% in newly defined high-grade zones. “These rocks are not staying in the ground,” Savich declared, highlighting a tight focus on mining the most valuable material first.

WA1 Resources, Luni Mineral Resource estimate (click here for full size image)

{kind=link}

He also pointed to recent test work that confirmed Luni’s potential to produce both ferro-niobium and high-purity oxide, enabling offtake discussions with global customers. With $70 million in cash, a growing institutional shareholder base, and early-stage development activities well underway, Savich concluded: “There has never been a better time in history to discover and develop the world’s second-best niobium deposit.”

>>> Small Cap (Market Capitalisation <$500) <<<

Antipa Minerals (ASX: AZY)

Presentation: Diggers and Dealers Mining Forum Conference Presentation

12 month price chart

Antipa Minerals CEO Roger Mason outlined a compelling growth story, underpinned by strong funding, a large-scale resource base, and significant upside potential in Western Australia’s red-hot Paterson Province. With a $350 million market cap and $71 million in cash, Antipa is progressing its flagship Minyari Dome project – an emerging standalone development opportunity.

%20at%20various%20gold%20price%20assumptions.png)

Antipa Minerals, Projected annual free cash flows (post-tax, a$m) at various gold price assumptions (click here for full size image)

{kind=link}

A 2024 scoping study highlighted potential production of 130,000oz p.a. over a 10-year mine life. At a base case gold price of $3,000/oz, the project carries a pre-tax net present value (NPV) of $834 million and an internal rate of return (IRR) of 52%. That jumps to $1.2 billion NPV and 79% IRR at $4,000/oz gold. “Every year we add to the mine life adds over $200 million in post-tax free cash flow,” Mason said.

Antipa Minerals, Minyari Dome Development Porject Delivery Schedule (click here for full size image)

{kind=link}

With a fully funded pre-feasibility study underway and a final investment decision targeted by mid-2027, Antipa is also chasing near-mine resource growth. High-grade hits, such as 15m at 15g/t, support substantial extensions. “This isn’t just about development, it’s about discovery too,” Mason added. Amid consolidation in the Paterson, Antipa stands out with a dominant 4,100km² footprint and a clear three-pronged strategy: development, growth, and discovery. First gold is targeted for late 2028.

Arafura Rare Earths (ASX: ARU)

Presentation: Diggers and Dealers Mining Forum Presentation

12 month price chart

Arafura CEO Darryl Cuzzubbo described the Nolans project as “the most advanced construction-ready rare earths project in the world that can bypass China”. The company's progress towards production comes amidst a rare earth supply chain crisis that’s only just beginning to unfold, with China still controlling 90% of light rare earths and 98% of heavy rare earths. Cuzzubbo concluded that the West’s dependency on China “makes no sense when a $47,000 EV can’t be built because of a $70 rare earth input.”

Arafura Rare Earths, More than one Nolans project required every year

He reassured delegates that Nolans is fully approved, engineered, and “ready to go,” with over $1 billion in debt already secured from nine international lenders. Just $500 million in equity remains to be raised. Phase 1 will produce 4,400t of NdPr oxide annually – enough to power over 4 million EVs – with by-product phosphoric acid helping to push the project “to the bottom of the cost curve.”

Arafura Rare Earths, Nolans sits comfortably in first quartile of cost curve

“We’re the only project globally that can go into construction in months and bypass China entirely,” Cuzzubbo said. Arafura already has binding offtakes with Hyundai, Kia, Siemens, and Traxys, and expects a market re-rating as it moves past the funding risk and into execution.

Gorilla Gold Mines (ASX: GG8)

Presentation: Diggers & Dealers Investor Presentation

12 month price chart

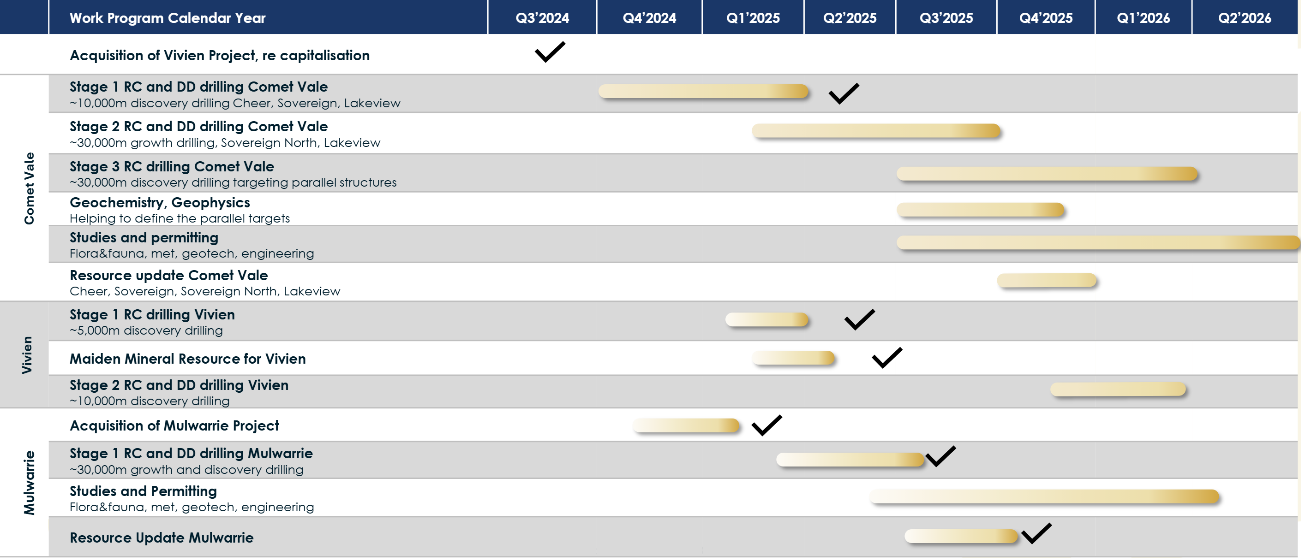

In his first Diggers & Dealers appearance, CEO Charles Hughes laid out Guerilla Gold Mines’ aggressive growth story built around high-grade gold exploration in Western Australia. The company’s three advanced projects – Comet Vale, Malwari, and Vivian – are all located on granted mining leases and within trucking distance of operating mills.

Gorilla Gold Mines, Upcoming Work Program (click here for full size image)

{kind=link}

GG8 has drilled 75,000 metres in 2025 alone, delivering maiden resources at Vivian (278,000oz at 4.1g/t) and Malwari (350,000oz at 3.6g/t), and a major discovery at Lake View within the flagship Comet Vale project. Five rigs are currently operating at Comet Vale, where results include multiple intercepts above 200g/m. A substantial resource upgrade is expected in Q4 2025.

Hughes emphasised Guerilla’s “drill-driven” model, backed by $25 million in cash and a $270 million market cap. “We’re rapidly discovering and defining ounces where infrastructure already exists,” Hughes said. “This is not exploration for the sake of it, we’re unlocking value on granted leases with a clear path to development.”

With an experienced team, institutional backing, and a commitment to spending 90–95% of funds in the ground, Guerilla aims to become a serious mid-tier gold developer within the next 24 months.

Larvotto Resources (ASX: LRV)

Presentation: Presentation - Diggers & Dealers Mining Forum

12 month price chart

Larvotto Managing Director Ron Heeks delivered a high-energy presentation on the company’s Hillgrove Antimony-Gold Project near Armidale, NSW – now Australia’s largest antimony deposit and the seventh-largest globally. With 1.7Moz gold-equivalent (including 96,000 tonnes of antimony) and another million ounces in exploration targets, the project is now fully funded and construction-ready (just 14 months after Larvotto acquired it for $3 million).

Antimony is emerging as a critical mineral for solar panels, defence, batteries, and semiconductors. “We will produce 7% of global supply,” Heeks said, noting the strategic value amid China’s 2024 export controls. Offtake agreements are already in place with global traders, and tungsten production will provide further upside.

Larvotto Resources, DFS confirms Hillgrove as a technically robust, high-margin critical minerals project

A recent DFS shows a pre-tax NPV of $1.2 billion and IRR of 153%, with all-in sustaining costs for gold at negative $3,200/oz thanks to antimony by-product credits. Larvotto raised $250 million in just six days through debt and equity and expects to produce first antimony by April 2026. “From nothing to fully funded in 14 months – this is a stunning outcome,” Heeks said, crediting his team and reaffirming a strong commitment to the local Armidale community over FIFO operations.