Morning Wrap: ASX 200 futures flat, S&P 500 closes little changed, Gold and uranium extend gains

ASX 200 futures are up 6 pts (+0.06%) as of 8:30 am AEDT.

In this article

ASX 200 futures are up 6 pts (+0.06%) as of 8:30 am AEDT.

In a nutshell:

Major US benchmarks gave back early gains to close relatively flat

S&P 500 crossed 7,000 for the first time before pulling back

Gold prices continue to surge, now close to US$5,400 and up almost 25% YTD

Fed kept interest rates unchanged, with commentary slightly hawkish but market rate cut pricing little changed

Microsoft and Meta reported quarterly results after hours, both beat market expectations but shares moving in opposite directors after hours

Let's dive in.

Overnight Summary

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

S&P 500 | 6,978 | -0.01% |

Dow Jones | 49,016 | +0.02% |

NASDAQ Comp | 23,857 | +0.17% |

Russell 2000 | 2,652 | -0.56% |

Country Indices | ||

Canada | 33,176 | +0.24% |

China | 4,151 | +0.27% |

Germany | 24,823 | -0.29% |

Hong Kong | 27,827 | +2.58% |

India | 82,345 | +0.60% |

Japan | 53,359 | +0.05% |

United Kingdom | 10,154 | -0.52% |

Name | Value | % Chg |

|---|---|---|

Commodities (USD) | ||

Gold | 5,383.19 | +3.90% |

Copper | 5.9986 | +2.34% |

WTI Oil | 63.4 | +1.62% |

Currency | ||

AUD/USD | 0.7034 | +0.32% |

Cryptocurrency | ||

Bitcoin (USD) | 88,781 | -0.50% |

Ethereum (AUD) | 4,261 | -0.66% |

Miscellaneous | ||

US 10 Yr T-bond | 4.251 | +0.66% |

VIX | 16.46 | +0.67% |

US Sectors

Sector | % Chg |

|---|---|

| Energy | +0.74% |

| Information Technology | +0.62% |

| Materials | +0.18% |

| Communication Services | +0.08% |

| Financials | -0.03% |

| Utilities | -0.24% |

Sector | % Chg |

|---|---|

| Industrials | -0.53% |

| Consumer Discretionary | -0.67% |

| Health Care | -0.77% |

| Consumer Staples | -0.78% |

| Real Estate | -0.92% |

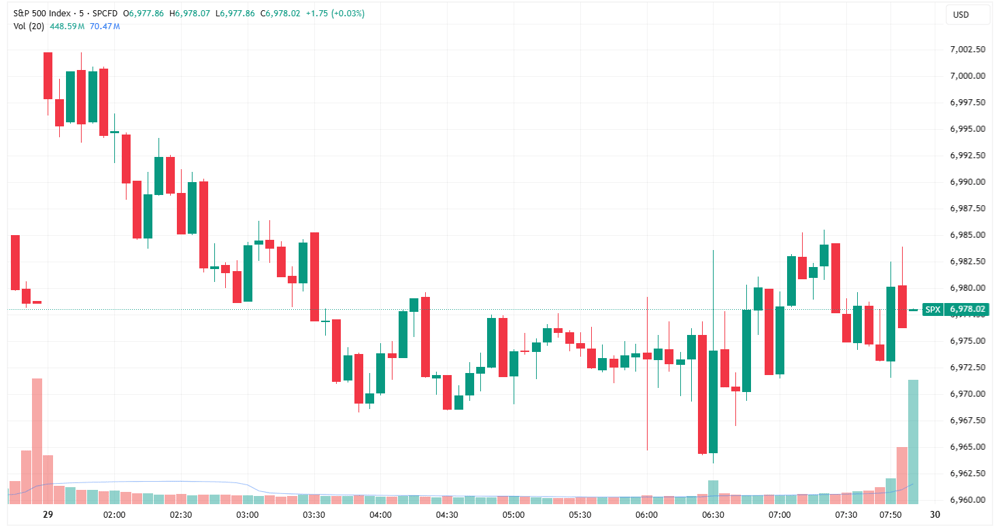

S&P 500 SESSION CHART

S&P 500 gave back early gains to close breakeven (Source: TradingView)

OVERNIGHT MARKETS

Major US benchmarks opened higher but finished little changed, with the S&P 500 and Nasdaq fading from record levels

Markets little changed after the widely expected Fed hold, though commentary took a slightly hawkish lean on improved economic growth and jobs wording

Microsoft and Meta announced quarterly earnings after market close, Microsoft down ~4% after hours, Meta up ~3%

Gold now closing in on US$5,400 despite closing at ~US$5,180 on Wednesday, prices have rallied almost 25% year-to-date

US dollar slides after Trump say he is not concerned about its weakness (BBG)

US dollar then bounced after Bessent affirms strong USD policy (RT)

Oil call options are on longest bullish run since 2024 amid Iran risks (BBG)

Bond traders betting on dovish Fed policy shift as BlackRock's Rick Rieder gains momentum to succeed Powell (BBG)

Japan bonds rally as 40-year auction sees strongest demand since March, easing immediate debt fears (BBG)

Swiss franc surges to decade high as investors seek safe haven (FT)

South Korea's market cap overtakes Germany's, buoyed by tech sector strength (BBG)

STOCKS

JPMorgan and BofA announce $1,000 Trump account match (YF)

Stellantis invests $13bn to revamp Jeep and Dodge brands (FT)

Deutsche Bank offices raided in German money laundering probe (FT)

Texas Instruments guides revenue above forecasts as industrial demand recovers, shares surge 9.9pc (BBG)

ASML says AI demand boosting orders and sees significant sales increase this year but plans 1700 job cuts (CNBC)

SK Hynix posts record quarterly profit, sees surging AI demand driving memory growth, shares rallied 5.1pc, now up almost 30pc YTD (CNBC)

Seagate forecasts Q3 revenue and profit above expectations as AI-driven storage demand rises, shares surge 19pc, lifting YTD gains to 57pc (RT)

Anthropic raises 2026 revenue forecast 20% but delays positive cash flow expectations (TI)

SpaceX weighs mid‑June IPO potentially raising $50bn at ~$1.5tn valuation (FT)

Logitech posts best quarterly earnings since pandemic, driven by video-conferencing and education sales, shares still dip 7.5pc to 7-month low (RT)

TARIFFS

China approves first batch of Nvidia H200 imports, opening way for high-profile names like ByteDance, Alibaba and Tencent to buy chips (RT)

US and Canada officially agree to begin formal discussions on possible structural and strategic reforms to USMCA (WSJ)

Ottawa, Seoul agree to work on bringing South Korean auto manufacturing to Canada (GM)

CENTRAL BANKS

Fed left rates unchanged at 3.50–3.75% as expected, Waller and Miran dissent in favour of a 25 bp cut, language around economic growth was upgraded from “modest” to “solid”, unemployment rate showed signs of “stabilisation” from previous “edging up”, overall slightly hawkish tone (BBG)

Bank of Canada holds, cites trade uncertainty, Fed independence concerns (RT)

ECB may cut rates if euro strength impacts inflation forecasts says Austrian governor Kocher (FT)

GEOPOLITICS

Gulf allies refuse support for US over possible Iran strike, constraining Trump's military options (WSJ)

Trump threatens to cut off assistance to Iraq if it reinstates Nouri al-Maliki as prime minister (RT)

ECONOMY

Australian inflation continued to accelerate in December, boosts odds of February RBA rate hike (RT)

Industry ETFs

Name | Value | % Chg |

|---|---|---|

Commodities | ||

| Uranium | 61.78 | +6.79% |

| Silver | 105.53 | +3.88% |

| Gold Miners | 112.13 | +2.60% |

| Copper Miners | 91.95 | +1.69% |

| Steel | 96.1585 | -0.01% |

| Strategic Metals | 97.5 | -0.11% |

| Lithium & Battery Tech | 74.69 | -0.68% |

Industrials | ||

| Agriculture | 25.87 | +0.12% |

| Construction | 100.27 | -0.21% |

| Global Jets | 27.695 | -0.59% |

| Aerospace & Defense | 233.6 | -1.44% |

Healthcare | ||

| Biotechnology | 174.03 | -1.62% |

Name | Value | % Chg |

|---|---|---|

Cryptocurrency | ||

| Bitcoin | 12.34 | -0.32% |

Renewables | ||

| CleanTech | 64.4 | +2.60% |

| Hydrogen | 40.615 | +2.38% |

| Solar | 57.35 | +2.30% |

Technology | ||

| Semiconductor | 360.46 | +2.67% |

| Electric Vehicles | 33.4595 | +0.21% |

| Video Games/eSports | 106.29 | -0.05% |

| Cloud Computing | 21.87 | -0.23% |

| Sports Betting/Gaming | 19.06 | -0.65% |

| Robotics & AI | 37.99 | -0.71% |

| E-commerce | 32.71 | -0.89% |

| Cybersecurity | 29.96 | -1.02% |

| FinTech | 28.27 | -1.43% |

ASX TODAY

ASX 200 futures flattish, big pullback in the Aussie 10-year (down 10 bps from 4.87% to 4.76%) but Aussie dollar now at 70.36 US cents (highest since Jan-23). Commodity prices continued to chug higher overnight, though recent rate hike chatter could dampen some consumer facing sectors. Lots of quarterlies and trading updates still coming through so I'll take a closer look on the blog

Ora Banda reports Q2 gold production of 32koz vs 37koz ests, AISC was A$3,505 vs. A$2,926 ests, FY26 guidance retained but expected to track towards lower end, AISC guidance increased to A$3,250-3,350/oz vs. prior A$2,800-2,900 due to higher third party processing costs (OBM)

Iluka reports above forecast zircon/rutile/synthetic rutile production for Q4, flags non-cash impairment charge of ~$350m relating to its Cataby mine (ILU)

SmartGroup weighing all scrip bid for FleetPartners (The Aus)

WHAT TO WATCH TODAY

Uranium: Uranium ETF added another 6.8% overnight as uranium prices continue to push above US$90/lb and towards fresh two-year highs. Lots of local uranium names like Paladin, Deep Yellow, Bannerman etc. look vertical, but clearly a big momentum shift as spot prices break out.

ASX: ASX reported a better-than-expected preliminary 1H26 result yesterday but hiked its FY26 expense guidance, so two very conflicting outcomes. The stock finished relatively flat, but seeing some analyst upgrades this morning.

BROKER MOVES

Amcor downgraded to Equal-weight from Overweight; target cut to $68.66 from $88.45 (MS)

ASX upgraded to Overweight from Neutral; target up to $62 from $60 (JPM)

Boss Energy downgraded to Hold from Buy; target cut to $1.95 from $2.00 (BP)

Fletcher Building downgraded to Underweight from Equal-weight; target cut to $2.89 from $3.13 (MS)

Greatland Resources downgraded to Sell from Neutral; target however up to $11.70 from $11.00 (GS)

Greatland Resources downgraded to Neutral from Outperform; target however increased to $13.00 from $11.40 (MQG)

Reece upgraded to Overweight from Equal-weight; target up to $16.00 from $12.00 (MS)

Key Events

Stocks trading ex-dividend:

Thu 29 Jan: 360 Capital Mortgage REIT (TCF) – $0.05, CD Private Equity Fund I (CD1) – $0.05, CD Private Equity Fund II (CD2) – $0.38, CD Private Equity Fund III (CD3) – $0.04, EUROZ Hartleys Group Ltd (EZL) – $0.025, Gryphon Capital Income Trust (GCI) – $0.012, KKR Credit Income Fund (KKC) – $0.017, Perpetual Credit Income Trust (PCI) – $0.006

Fri 30 Jan: Djerriwarrh Investments Ltd (DJW) – $0.072, MA Credit Income Trust (MA1) – $0.014

Other ASX corporate actions today:

Dividends paid: Turners Automotive (TRA), Tower (TWR), Solvar (SVR)

Earnings: Champion Iron (CIA)

IPOs: None

AGMs: None

Economic calendar (AEDT):

No major economic announcements.