Lithium just dropped 30% as sodium batteries and China supply threats loom

Rival battery chemistries, a resumption of Chinese production, and yet experts still see upside for lithium prices and ASX lithium stocks.

Source: ChatGPT

Mentioned

KEY POINTS

- Benchmark lithium carbonate futures have tumbled nearly 30% from the May peak as fears surrounding the rapid development and deployment of new sodium battery technologies and the threat of new supply have spooked investors.

- ASX listed lithium producers like Pilbara Minerals (PLS), Liontown (LTR), IGO and Mineral Resources (MIN) have collectively seen their share prices substantially pared in response to commodity price moves.

- Yet the research tells a different story – lithium demand remains robust, supply has tightened since last year’s bear market nadir, and the sodium threat may not be as dire as the headlines would have you believe.

Few commodities do drama like lithium. In 2020, you could buy a tonne of lithium carbonate in China for around CNY39,500. Two years later, at the peak of the electric-vehicle mania in November 2022, that same tonne changed hands for CNY597,500 – a fifteen-fold surge that minted fortunes among those who rode the wave and launched a thousand ASX small-caps.

But as with any cyclical commodity, what goes up that fast comes down just as hard. Supply hit the market, initially a trickle, then a deluge, crashing the lithium price nearly 90% by June 2025’s CNY59,900 low. By then, the cycle had done its work: high-cost supply had been shuttered, expansion plans shelved, and survivors left lean.

%20CNY-mt.png)

Lithium Carbonate 99.5pct Battery Grade (China, Japan & Korea) CNY/mt. Source: SMM

Then came the rebound. As marginal Chinese supply stayed offline, and with bullish narratives surrounding battery energy storage systems (BESS) coming to the fore – plus a handy energy price spike (thanks US-Iran!) – lithium prices soared to over CNY200,000 by May. The recovery looked unstoppable – until it wasn't. Over the past few weeks, prices have tanked around 30%.

Why? Is it press-filled headlines about new sodium battery technologies? CATL’s giant Chinese lithium operations threatening to resume production? Or something else?

To work out what is really going on, I have gone through the most recent research from five major research houses. They disagree on plenty. But on the big question, most of them land at the same conclusion: the market may be tighter than the tumbling price would have you believe.

Why is the lithium price falling?

Here is the uncomfortable truth about a 30% move in a futures market: nobody can tell you precisely why it happened. We cannot poll every buyer and seller. What we can do is line up the plausible narratives that might explain the move – and on this occasion, there are several:

Speculative unwind: Open interest on GFEX, where the benchmark lithium carbonate contract trades, has rolled over – back below the levels seen in January when regulators last moved to curb speculative trading. It’s now harder for frothy demand to act on the futures market than when lithium was running hot earlier this year.

Renewed supply fears: Chiefly the prospect of Zimbabwean material returning to the market from mid-July. There’s also growing talk this week of a restart at CATL's giant Jianxiawo lepidolite operation in Jiangxi – more on which below.

Accounting quirk: A change to China's inventory reporting scope has inflated visible carbonate stocks, a one-off that, according to Macquarie, shouldn’t be read as fresh oversupply (again more below).

Sodium-battery development and deployment press: It feels like the battery technology industry is moving at break-neck speed, and talk of sodium-ion alternatives to the incumbent lithium-ion supremacy – right or wrong – are likely having at least some impact on sentiment.

No EV sales step change: EV sales since the Middle East conflict sparked a massive spike in carbon-based fuel sources have been robust, but not the tectonic shift in adoption many lithium bulls had hoped for.

Some reasons are sentiment-based, some are supply-related, and others impacting the demand-side. Let’s check in on the latest in lithium market fundamentals.

Latest lithium demand factors

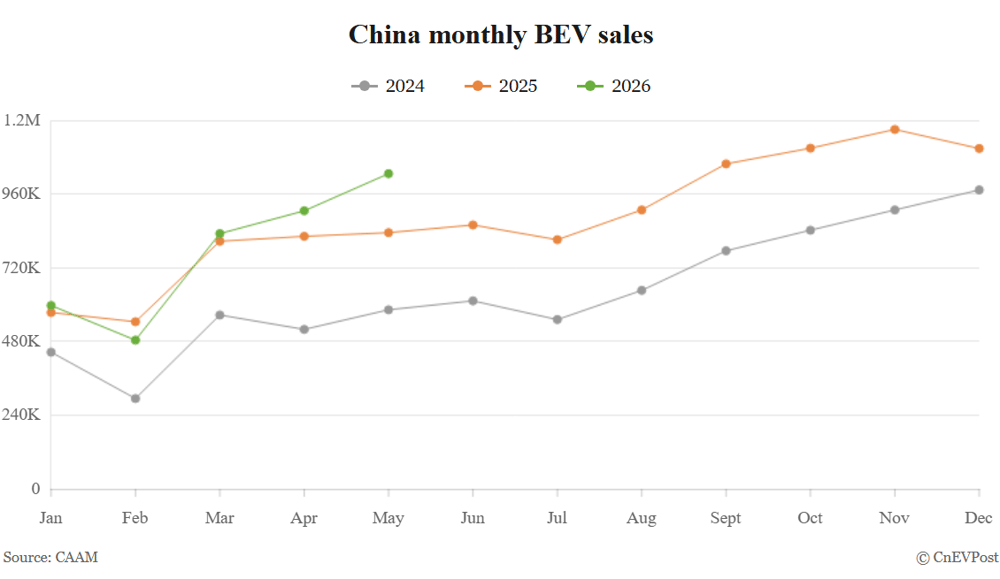

The most recent hard data is encouraging. Morgan Stanley's read of the latest Chinese EV sales figures for May showed battery-electric vehicle sales up 23% year-on-year, and 13% versus April. Exports of Chinese EVs surged 94% year-on-year, signalling strong demand from global markets. BESS shipments are running hotter still – up 79% year-on-year in the first quarter, comfortably ahead of forecast. Morgan Stanley expects the lithium market to stay tight in the near term.

China monthly BEV sales, May 2026. Source: CNEVPOST, 10 June 2026

But I would temper the enthusiasm. The same data showed overall Chinese passenger-vehicle sales down 23% year-on-year, a sign of soft domestic demand. Exports are doing the heavy lifting, and local EV sales were likely flattered by a rush of new model launches.

Indeed, in a briefing hosted in mid-June by UBS, lithium market consultancy Wood Mackenzie argued the China EV market faces a structural slowdown. It also flagged a looming distortion: China's rebate on battery-product exports has already been trimmed from 9% to 6%, and is set to be scrapped altogether from January 2027 – incentivising exporters to ship now and pulling demand forward into this year.

Wood Mackenzie went further, suggesting there is a ceiling to how far exports can paper over soft domestic demand. It also questioned the market's faith in the BESS narrative – while shipments appear strong, the consultancy argued, installations are lagging.

Latest lithium supply factors

If the demand debate is finely balanced, the supply story is where the lithium story gets interesting – and it remains, overwhelmingly, a China story.

In a note released on 23 June, Shaw and Partners offered a bold theory on the curtailment of Chinese lithium supply that began last year and continues today. In their reading, Beijing has shifted from maximising lithium production to maximising control of its lithium resources. CATL’s Jianxiawo lepidolite mine, which is estimated to account for roughly 95–100kt of annual lithium carbonate capacity – among the largest on earth – has remained shuttered since August 2025 when its licence lapsed.

CATL has sought a renewal, Shaw says, and has been knocked back. To Shaw, that refusal is no accident. Under an "anti-involution" campaign formalised at the depth of last year's rout, authorities banned below-cost selling and reclassified lithium as a strategic mineral, cancelling 27 mining permits in Jiangxi alone. All told, Shaw estimates the operations swept up by the new regime account for around 17% of global lithium supply this year.

The corollary is striking. With its own lithium banked, China is pulling in ever more Australian spodumene from the likes of Greenbushes and Pilgangoora to feed its refineries. China is consuming others' ore while preserving its own – a dynamic that, Shaw argues, puts a structural floor under Western Australian hard-rock producers like PLS, IGO, LTR and MIN.

Here is the irony. Part of what spooked the market was the fear that Jianxiawo is about to reopen. Yet, there’s plenty of disagreement in the latest broker research on what this will mean for lithium prices. Macquarie assumes just 5kt of carbonate from CATL this year, with a restart not before late in the third quarter. UBS pencils in around 40kt and a second-half restart. Wood Mackenzie thinks Jianxiawo stays offline until 2027 altogether.

There's also less to the inventory picture than meets the eye. Part of what has unnerved traders recently was a jump in visible lithium carbonate stocks sitting in Chinese warehouses – on the surface, a classic sign of oversupply. But Macquarie attributes the increase to previously unreported trader-held volumes now counted in the official tally. Strip out that accounting shift and total inventories have continued to draw down in recent weeks – the opposite of what you'd expect if the market were drowning in metal.

Altogether, the latest expert research suggests that fears of an imminent flood of new Chinese supply are, at the very least, premature.

Sodium is a threat, but not yet

Which brings us to sodium – lithium’s bogeyman. The case is real: sodium-ion batteries are cheaper, draw on an abundant raw material, and perform better in the cold, and CATL's recent launches have given the story fresh legs. I wrote about the rapidly developing battery chemistry in this article last month.

But Macquarie's latest analysis is a useful corrective. In a research note released 25 June, the investment bank noted that sodium-ion cells still carry meaningfully less energy per kilogram than the lithium chemistries that dominate mainstream EVs. Further, it noted that of some 300GWh of announced sodium capacity, only around 90GWh has actually been built. There are issues on the supply side as well, noted Macquarie, suggesting that the supply chain for battery-grade sodium feedstock barely exists at scale.

CATL's new TENER Sodium Energy Storage System unveiled on 22 June. According to CATL, sodium is over 1,000 times more abundant than lithium and is widely distributed. The battery manufacturer claims sodium battery chemistries offer better extreme-temperature performance, safety, and cost potential. Source: CATL, 22 June 2026..

By contrast, Morgan Stanley wrote in a 25 May note that it sees sodium taking real share – but in budget cars, light commercial vehicles and storage, and not in earnest until the early 2030s. I have not yet seen research anywhere that suggests premium, long-range EVs won’t remain lithium-powered. Shaw also acknowledges the sodium risk but similarly puts a post-2030 timeline on any substantial lithium market impact. Here’s my read: new sodium battery chemistries do pose a serious structural question for the lithium market in the medium term, but this is unlikely to be the main driver of this month’s 30% decline.

Experts remain bullish on lithium

Strip away the noise and the spread of opinion is narrower than the headlines suggest. Here is where each house sits:

Shaw and Partners – The most bullish. Reads China's supply restraint as a structural floor and a stronger-for-longer cycle, with Buy ratings on Wildcat Resources (WC8), Global Lithium Resources (GL1) and PMET Resources (PMT).

Macquarie – Bullish. Judges the sell-off overdone and fundamentals sound, carrying Outperform ratings on Elevra Lithium (ELV), IGO (IGO), Liontown (LTR), and Pilbara Minerals (PLS).

UBS – Modestly bullish. Prefers its own tight-market view to Wood Mackenzie's caution, and favours LTR, IGO, MIN and PMT in Australia and Albemarle (NYSE: ALB) and POSCO (KRX: 005490) internationally.

Morgan Stanley – Balanced. Expects a tight near-term market but more even risk-reward. No buys in the sector.

Wood Mackenzie – The cautious outlier. Concerned about EV demand durability and the gap between storage shipments and installations.

Conclusion: follow the money

This article likely poses more questions for you than it provides answers – such is the spread of expert views. That uncertainty is the point. Sodium and a softer EV cycle are genuine long-term questions, but the evidence I have read suggests neither explains a 30% rout in just four weeks. Either the market has it wrong, or the general view among the experts of a ‘tight market’ is overly optimistic.

From here, the tell will be simple enough. If this really was a sentiment-driven flush rather than a fundamental break, the clearest confirmation will be capital quietly rotating back into lithium commodities and lithium stocks. The price will bounce, it may pull back a little, but it will bounce even stronger again. The May high will be tested and breached.

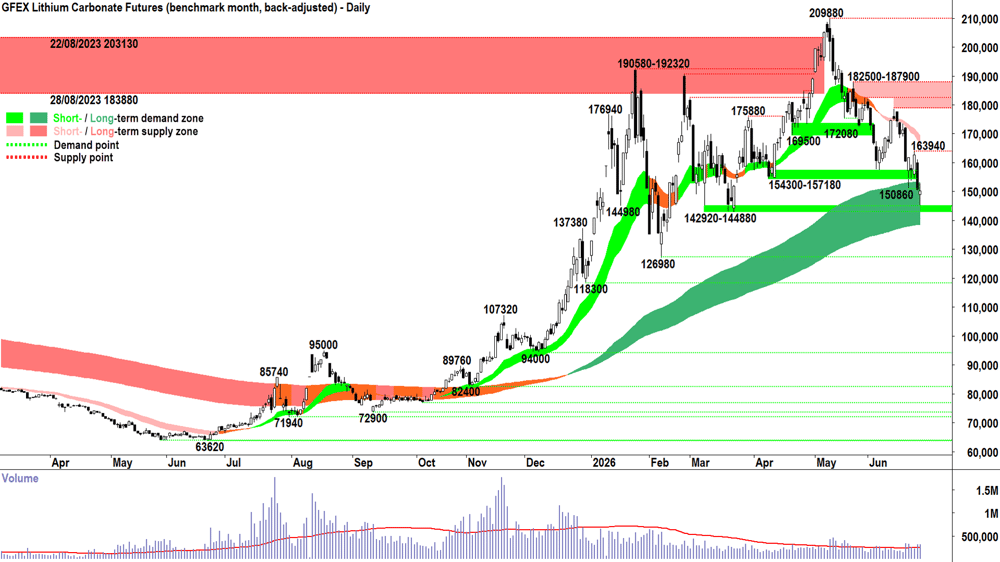

Lithium Carbonate Futures (Benchmark month, back-adjusted) GFEX. Source: SMM. The ChartWatch technical analysis model suggests that a potentially bull-market-ending trend change is underway. Watch my latest lithium carbonate futures technical analysis here, or weekly updates here.

This is exactly the kind of base-building I will be watching for in ChartWatch. But I’ll also be watching out carefully for the opposite: prices don’t bounce back quickly, but rather the May peak is reinforced by increasing supply and switching market sentiment back to that of the withering bear market – which will likely bring back some very painful memories for some.

This article draws on institutional research from Macquarie, Morgan Stanley, Shaw and Partners and UBS (all May–June 2026), with additional market commentary from Wood Mackenzie.