Latest on lithium: sure, everyone wants a BYD – but sodium-ion is coming!

Lithium is back in an upcycle and everyone’s rushing to buy an EV — but a rival battery chemistry is gaining traction fast.

Source: Shutterstock

Mentioned

KEY POINTS

- Lithium has delivered two massive boom-bust cycles in the past decade — surges of hundreds of percent followed by 80–90% crashes — making timing everything for investors in ASX lithium stocks.

- The Middle East conflict jolted EV sales back to life, but so far, the data shows the effect has been modest — global EV sales were flat in the first four months of 2026 relative to the same period in 2025.

- This article investigates two structural forces shaping lithium's next move: the strength of the EV demand recovery, and the rise of sodium-ion batteries as a genuine alternative chemistry — with the latest industry news and expert views.

Few commodities have captured the imagination of ASX investors quite like lithium. Over the past decade, it has delivered not one but two extraordinary boom-bust cycles — surges of several hundred percent followed by withering drawdowns of 80–90%.

As with most commodity price cycles, timing is everything. Get it right, and the returns can be life changing, but miss the turn, and you could end up holding all the way back down again. Sound familiar?

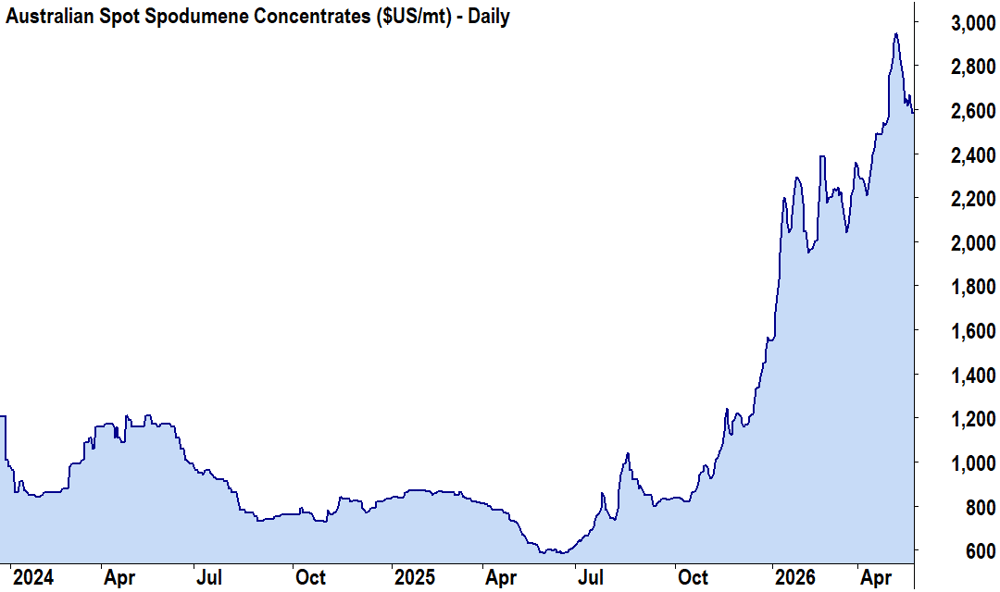

There is good news for investors: lithium appears to be in a new upcycle. Australian spot spodumene concentrate is trading above US$2,500/t, having recently traded as high as US$2,945/t. Compare this to the US$585 bear market low set in June last year — and one could be forgiven for thinking the worst is well and truly behind for those producing this critical energy transition metal.

Australian Spot Spodumene Concentrate (SC6%). Source: Author’s chart using SMM price data.

But how long this up-cycle lasts — and how high it runs — will depend on a contest between two powerful forces. On the demand side, the big question is whether the spike in EV sales triggered by the Middle East conflict represents a genuine structural acceleration, or a temporary blip. On the supply side, the question is subtler: even if EV adoption continues, will lithium be the dominant battery chemistry to carry it forward?

Sodium-ion batteries — a chemistry that has been developing alongside lithium-ion for decades — are now moving into commercial deployment at scale, particularly in China. The implications for long-run lithium demand are real, even if the near-term pricing story remains firmly constructive.

This article investigates both forces. I'll walk through the latest EV sales data, the sodium-ion commercial picture, and the key supply-side dynamics — before turning to what the charts and broker price forecasts are telling us.

EV sales: temporary oil shock or structural shift?

The thesis that the current Middle East conflict will supercharge global EV adoption has substantial intuitive appeal. Since the conflict began at the end of February, Brent crude spiked from around US$63 per barrel to as high as US$120 per barrel by April — the kind of fuel price shock that historically reshuffles consumer preferences and accelerates technology adoption.

In a recent research report on the impact of higher oil prices on the global EV market, leading global investment bank Canaccord Genuity notes there is clear historical precedent: every major oil shock since the 1970s produced a lasting step-change in powertrain technology, from the downsizing era of the 1970s and '80s through to electrification in the 2010s.

March 2026 EV data appeared to confirm the thesis. They showed a 63% month-on-month surge to approximately 1.7 million units globally, with Chinese EV exports annualising at a 46% increase over 2025 figures. When April’s data came in, it was less confirmatory of a massive switch in consumer preferences.

This week, Macquarie's economics desk notes the latest global EV sales for April showed flat growth for the first four months of this year compared to the same period last year. Further it noted significant regional divergence in sales growth with US EV sales down 33% year-on-year over the four months, China 17% lower, while Europe and the rest of the world were up 26% and 77% respectively — albeit starting from a lower base.

On a positive note, Macquarie noted that search trends for EVs remain elevated above pre-conflict levels, and the International Energy Agency's (“IEA”) Global EV Outlook 2026 retains a constructive long-run view with global EV sales projected to grow roughly 10% this year.

Looking at the IEA’s research specifically, the agency is projecting more than a doubling of annual EV sales by 2035 — implying a global EV fleet of over 450 million vehicles. The current global EV fleet is estimated to be around 75 million. ASX energy sector investors may wish to take note here: on that trajectory, the IEA claims that EVs would be displacing around 9–10 million barrels per day of oil demand by 2035, compared to roughly 1.7 million barrels per day currently.

One can easily conclude that the structural EV demand growth story remains intact and compelling. Still, the near-term data does not yet support the idea that the Middle East conflict has delivered a substantial step-change in EV demand. Investors tempted to extrapolate March’s spike may wish to reconsider.

Sodium-ion is coming, fast

Even if EV adoption continues on its long-run trajectory, lithium's share of that demand is not guaranteed. Sodium-ion batteries — which use sodium rather than lithium as the charge carrier — are no longer a laboratory curiosity. They are moving into commercial deployment, and the pace of that deployment matters enormously to lithium pricing.

The chemistry has real advantages in specific applications. Sodium is cheaper and more abundant than lithium, sourced from soda ash, iron phosphates, and carbon — materials that are abundantly available globally and not subject to the supply chain bottlenecks that have plagued lithium.

Sodium-ion batteries are also inherently more stable at high temperatures, which improves fire safety relative to lithium-ion — a critical feature for large-scale battery energy storage systems (“BESS”) applications, particularly in AI data centres where a thermal event can destroy hundreds of millions of dollars of processing infrastructure. Peak Energy, a US sodium-ion battery developer, notes the technology allows for a fully passive cooling system, cutting battery storage system operating costs in half relative to lithium-ion equivalents.

Peak Energy's sodium-ion chemistry uses abundant materials like sodium, iron, and carbon and avoids lithium entirely. Source: peakenergy.com

The China deployment numbers are where the rubber meets the road. In a research report released this week, Morgan Stanley noted its China Energy and Chemicals analyst Jack Lu sees China's sodium-ion deployment rising towards approximately 1,000 gigawatt-hours by 2035. Lu noted that energy density of some sodium-ion batteries has already reached around 175 watt-hours per kilogram — close to early mass-market lithium iron phosphate (“LFP”) performance — making sodium-ion viable today for budget EVs, light trucks, and grid-scale storage.

Morgan Stanley's modelling has LFP's share of entry-level passenger vehicles in China — currently around 50%, with the balance largely made up of nickel-cobalt-based chemistries — falling below 20% by 2031, with sodium-ion rising to approximately 50% of that market. In light commercial vehicles, the displacement is even more pronounced: LFP could fall from around 20% share in 2026 to roughly 5% by 2031, with sodium-ion rising to approximately 90%.

Morgan Stanley concludes the demand displacement risk to LFP is real but differentiated by market segment. The read-through for lithium demand is not automatically disastrous. Sodium-ion's inroads are concentrated in mass-market and budget applications — not premium long-range EVs, which are likely to remain lithium-based for the foreseeable future.

The key takeaway for investors must be: a boom in electrification is not automatically a boom in lithium demand.

Lithium supply has tightened

On the supply side, the picture is unambiguously tighter than it was 12 months ago — and that tightness may persist longer than the market expects.

Two supply disruptions are dominating the near-term balance. CATL's Jianxiawo lepidolite mine in Jiangxi — which has an installed capacity of approximately 110,000 tonnes per annum of lithium carbonate equivalent (“LCE”) — remains suspended with no definitive restart date. Macquarie expects a restart could still be pushed to the third quarter of this year or later, given ongoing concerns about tailings management and water quality near the mine site. Adding to the uncertainty, several other Jiangxi lepidolite operations are facing mining licence renewal deadlines — introducing the possibility that any volume gained from Jianxiawo could be partially offset by temporary suspensions elsewhere.

Zimbabwe's lithium concentrate export ban, introduced in February, has been partially lifted. The government introduced a quota system for selected large-scale producers in mid-April — predominantly Chinese-controlled operators — requiring written commitments to establish in-country lithium sulphate processing by January 2027 and compliance with new export duty arrangements. Here, Macquarie expects April export data (released with a one-month lag) to show a material decline, with further softness in May before a potential recovery from June. Zimbabwe accounted for approximately 8% of global hard rock lithium supply in 2025 — not trivial.

Latest expert lithium price forecasts

The broker price forecast picture is constructive but not uniform. All three research houses surveyed for this article see the lithium market moving into deficit from 2026 — Canaccord Genuity models that deficit at approximately 87,000 tonnes LCE this year, widening persistently through to 2035 as demand outpaces new mine supply. Where they diverge is on how aggressively prices respond, and how long the rally can sustain before downstream margin pressure bites.

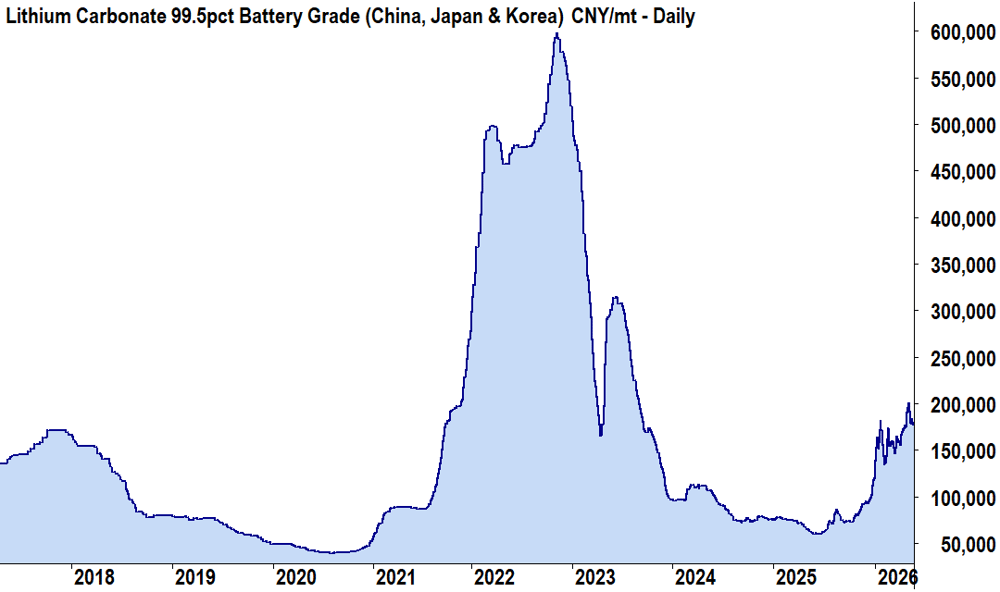

Lithium Carbonate spot chart — few commodities cycle like lithium does

UBS is the most bullish, projecting lithium carbonate to trade to US$30,519 per tonne in 2026 and US$41,875 per tonne in 2027, against a prior consensus of US$15,566 and US$15,984 per tonne respectively. For spodumene, UBS sees the long-term price settling at US$1,400 per tonne.

Canaccord Genuity is more measured, forecasting lithium carbonate at US$21,288 per tonne in 2026 and US$27,750 per tonne in 2027, reflecting an expected supply response through 2027/28. Spodumene is modelled at US$2,655 per tonne in 2026 and US$2,663 per tonne in 2027.

Macquarie is the most cautious near term, flagging a lithium carbonate price of US$29,500 per tonne as a likely psychological resistance level at which downstream battery and BESS project economics in China and Southeast Asia begin to face pressure..

(The chart above is in CNY. The current price of lithium carbonate of CNY 175,500/t is the equivalent of approximately US$26,000/t at the current exchange rate of 6.79 CNY/USD. Australian spodumene concentrate (SC6) is trading at US$2,565/t at the time of writing.)

Conclusion

Investment bank modelling that sees sodium-ion displacing lithium-ion as the dominant battery chemistry in key EV segments — and taking significant share in large-scale energy storage — is not something investors in the lithium story can afford to ignore. That said, the near-term supply picture is unambiguously tighter than it was 12 months ago, and this is being reflected in market pricing.

Yet lithium mineral prices have softened this week — the same week two major investment bank research reports questioned whether the Middle East conflict has delivered the structural jolt to EV demand that seemed intuitive just a month ago, plus documenting sodium-ion's steady march toward commercial dominance in mass-market applications. The confluence between price and data is worth noting.

Watch this video for my latest technical analysis on lithium markets and ASX lithium stocks including PLS Group (PLS), Mineral Resources (MIN), IGO (IGO), Liontown (LTR), Elevra Lithium (ELV) and more 👇

This article draws on institutional research from Canaccord Genuity, UBS, Macquarie and Morgan Stanley (April–May 2026), and background research from the International Energy Agency's Global EV Outlook 2026 and Peak Energy.