ASX 200 Live Today - Wednesday, 27th May

ASX 200 futures point towards a flattish open despite another record setting session on Wall Street. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Wednesday, May 27. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 higher, a solid session beneath the surface

[2:10 pm] That's a wrap. A pretty solid session, with the ASX 200 currently up 0.18%, largely thanks to a slightly cooler-than-expected CPI print. Breadth is fairly strong, with only two sectors (Financials and Staples) lower, and 132 constituents (66%) higher.

Tech (+1.53%) leading today, though the sector has been flat in the past month

Utilities (+0.87%) bouncing after falling seven of the last eight sessions

Discretionary (+0.84%) now up ~6% since 12-May and trading above the 50-day moving average for the first time since February, still down ~13% YTD

Materials (+0.77%) up for a fifth straight session and within 3.5% of its 2 March record high

Financials (-0.64%) was the main drag on markets, with most major banks down around 0.5-1.5%

Today's CPI print was slightly cooler-than-expected, with headline inflation easing to 4.2% in April from 4.6% in the prior month and below market expectations of 4.4%. Trimmed mean edged up to 3.4% from 3.3%, but in-line with consensus. The likelihood of another RBA hike in June has effectively hit zero. Plenty up in the air as trimmed mean inflation keeps grinding higher and remains well above target, and the US-Iran standoff has turned into an exchange of strikes over recent days.

Macquarie warns proposed tax changes could trigger major housing market downturn

[1:39 pm] Reversal of the CGT discount and removal of negative gearing would compound already-exhausted structural tailwinds, pointing to little or no real house price growth for the next decade or two, according to Macquarie.

Real house prices up about 160% since 1980 (2.1% CAGR), but two-thirds of the period was flat, with most gains in two bursts:

2000-2003 (+45%, 10.6% CAGR) post-CGT discount

2012-2022 (+55%, 4.8% CAGR) on ultra-low rates

Post-affordability stress historically means long sideways stretches, Melbourne took ~11 years to top its 1989 peak, Perth 17 years to recover 2006 levels

Structural tailwinds since 1997 (falling rates, financial deregulation, rising female workforce participation) are largely exhausted, removing the main supports for further real price growth

Proposed reversal of the CGT discount and abolition of negative gearing would add to existing downward pressure, with risk skewed to another material decline (real prices have fallen >9% six times since 1980, twice in the past decade)

Base case is real prices flat for a decade or two, which would also mean negligible incremental CGT revenue from housing

Endeavour tumbles 5% to yet another all-time low

[1:35 pm] Endeavour can't catch a break, down another 5.0% today to a fresh all-time low of 2.93%. The stock is now down 19.5% year-to-date and down 27.5% in the last twelve months.

Endeavour daily price chart (Source: TradingView)

The company's Investor Day today issued a number of strategies to drive revenue growth and operational efficiency (which reads well), offset by a change in dividend policy.

$300m of cost savings targeted by FY29, including $100m in FY27, as part of the three-year transformation program

Group exiting the majority of its existing winery and vineyard portfolio, including Chapel Hill, Oakridge and Josef Chromy, with Pinnacle Drinks repositioned to back Retail and high-performing brands

Targeted dividend payout ratio revised to 50-75% of group underlying NPAT (from prior policy) to fund growth investment

Capital deployment in Hotels to lift, with light touch renewals, refurbishments and whole-of-venue repositionings

As we noted earlier: The main concern here should be the dividend policy change, as Endeavour has historically maintained a payout ratio around 70-80%. UBS modelling (May-26) expects this trend to continue well into FY30, which implies a yield of around 4-5%. The revised range could result in some dividend uncertainty, and drive some selling pressure from income-oriented holders.

Dicker Data soars on AGM trading update

[12:52 pm] Dicker Data delivered a strong four-month start to FY26 with margin expansion and disciplined cost control, though management flagged moderating end-point growth and pricing-driven demand pressure into H2.

Gross revenue up 13.4% to $1,267.4m, driven by elevated end-point, software and data centre refresh demand

Gross operating profit up 19.3% to $120.9m, with gross margin expanding to 9.5% from 9.1%

EBITDA (ex one-offs) up 32.0% to $58.2m

NPBT up 45.5% to $47.3m, with PBT margin lifting to 3.7% from 2.9%

Operating costs held flat at 5.1% of gross revenue, with PBT further supported by disciplined enterprise segment approach

YTD AI-related revenue exceeds $20m with run rate expected to accelerate through H2, alongside building data centre refresh demand

End-point solutions growth expected to moderate, with higher vendor pricing flowing through in H2 likely to reduce unit demand though absolute revenue expectation remains strong

The AGM presentation was released to market at 12:28 pm AEST, with the stock currently up 9.0% to $9.71.

Company page: Dicker Data (DDR)

Coal stocks broadly higher

[12:47 pm] Coal stocks trading broadly higher following sharp rally on Monday and pullback on Tuesday. The catalyst behind Monday's rally as a gas explosion at China's Liushenyu mine, which triggered the closure of 25 mines in the Qinyuan region and 2-7 day halts at 109 underground met coal mines. UBS forecasts met coal prices could rise US$15-20 a tonne from current spot of ~US$240, with Shanxi sitting at the low-cost end of the global cost curve

Ticker | Company | % Chg | Price | 1 Week % |

|---|---|---|---|---|

CRN | Coronado Global | 5.9% | $0.27 | 20.0% |

TER | Terracom | 4.3% | $0.07 | 4.3% |

WHC | Whitehaven Coal | 2.9% | $8.79 | 8.1% |

SMR | Stanmore Resources | 1.4% | $2.56 | 2.2% |

NHC | New Hope | 1.1% | $5.73 | 3.4% |

YAL | Yancoal Australia | 1.0% | $6.88 | -0.1% |

Tech stocks broadly higher

[12:45 pm] A fairly strong day for tech stocks, with the S&P/ASX 200 Tech Index up 1.7% to a two-week high.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

DDR | Dicker Data | 8.0% | $9.62 | -6.5% |

MP1 | Megaport | 7.0% | $14.75 | 21.1% |

SDR | Siteminder | 6.5% | $3.04 | -50.5% |

AD8 | Audinate Group | 5.5% | $2.30 | -43.3% |

NXL | Nuix | 5.5% | $1.35 | -25.7% |

WBT | Weebit Nano | 3.8% | $7.61 | 52.2% |

DTL | Data#3 | 3.7% | $8.64 | -3.7% |

OCL | Objective Corporation | 3.4% | $10.55 | -36.3% |

NXT | NextDC | 3.0% | $15.10 | 22.6% |

PME | Pro Medicus | 3.0% | $131.11 | -40.6% |

CAT | Catapult Sports | 2.9% | $3.56 | -14.4% |

DGT | Digico Infrastructure Reit | 2.9% | $2.71 | -3.0% |

MAQ | Macquarie Technology Group | 2.4% | $72.99 | 8.9% |

IRE | Iress | 2.0% | $5.82 | -30.6% |

360 | Life360 | 1.6% | $19.12 | -40.7% |

WTC | Wisetech Global | 1.6% | $36.98 | -46.0% |

PPS | Praemium | 1.4% | $0.70 | -11.9% |

CDA | Codan | 1.2% | $41.77 | 47.0% |

XRO | Xero | 0.5% | $76.87 | -32.5% |

TNE | Technology One | 0.4% | $30.11 | 9.3% |

BVS | Bravura Solutions | 0.2% | $2.23 | -13.4% |

HSN | Hansen Technologies | 0.0% | $4.71 | -10.8% |

Australian Vintage refinances debt, flags ~5% second-half revenue growth

[12:40 pm] AVG secured a $128 million debt facility through to March 2028 this morning, and is on track for neutral underlying cash flow in FY26, with second-half cash generation of $20 million marking a ~$29 million turnaround on the prior year. The stock is currently up 31.0% to 7.6 cents.

Refinanced $128m facility agreed to March 2028 with a one-year extension option to 2029

Second-half revenue growth projected at +5% vs. -2% in H1, with the H2 run rate +10% above H1

Net debt expected to finish at ~$90m by 30 June, with full year underlying cash flow ~$33m better than FY23

Second-half cash generation of $20m versus -$9m in the prior comparative half, excluding asset sales

Poco Vino now selling ~500 bottles an hour across 8,000+ stores in 9 countries, with annualised run rate set to exceed $20m into FY27 as the range more than doubles

Targeting +$10m underlying cash flow (excluding investments) in FY27, with some risk of shipment delays into FY27 from Iran war impacts though cash target not at risk

Company page: Australian Vintage (AVG)

Nufarm 1H26 earnings call highlights

[12:35 pm] Nufarm laid out a margin-over-volume strategy at its earnings call, targeting $50 million in cost savings and a leaner portfolio to support a return to ~2x leverage by year-end.

Underlying EBITDA guided to strong growth in FY26, with positive free cash flow and net debt of ~2x underlying EBITDA by year-end

$50m cost-out program on track for FY26 delivery, with a further $50m run-rate targeted by end of FY27 (full benefit in FY28)

Capex guided to less than $200m in FY26, with D&A of ~$218m, net interest of ~$100m and underlying tax of $20-30m

Crop Protection margin profile improving as North America SKU reduction runs up to 20% in FY26, with global portfolio rationalisation continuing at ~10% per year

Seed Technologies expected to deliver strong EBITDA growth from hybrid seeds and emerging platforms, with emerging platforms segment EBITDA up $40m in FY26

Omega-3 cost base being lowered via production relocation to South America and anticipated China deregulation, with Europe and China deregulation targeted for 2028

Company page: Nufarm (NUF)

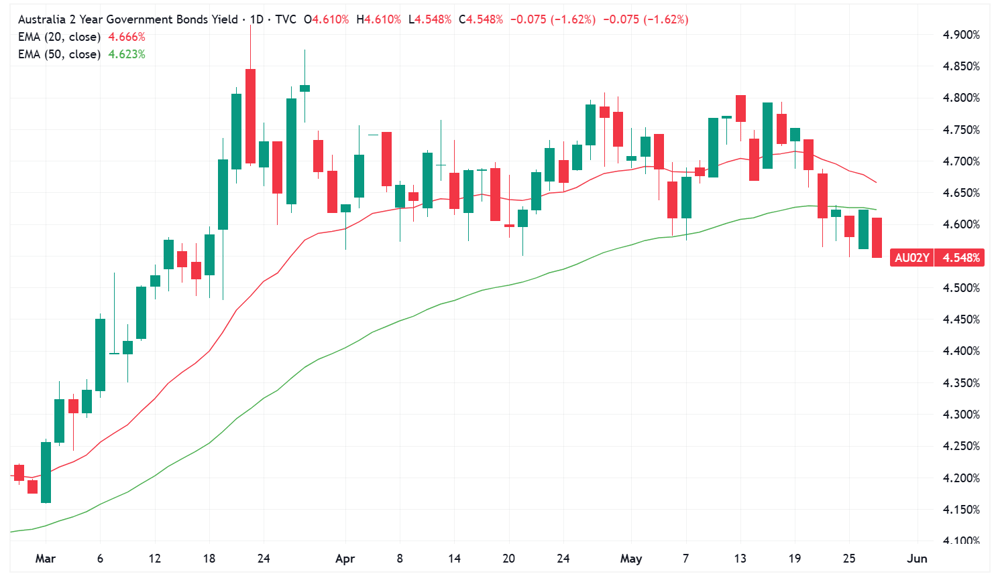

ASX 200 back at breakeven, yields dip

[11:50 am] The ASX 200 is back at breakeven, bouncing from session lows of (-0.37%) following the cooler-than-expected CPI print.

You've now got a situation where unemployment unexpectedly jumped to 4.5% in April (from 4.3% in the prior month) alongside a cooler, albeit still elevated, inflation print.

This is driving a sharp pullback in near-term rate expectations, with the Aussie 2-year down 8 bps to 4.53%, the lowest since 18 March.

Australia 2-year government bond yield (Source: TradingView)

Australian CPI eases to 4.2% in April

[11:34 am] Headline inflation softened in April but trimmed mean ticked higher, with electricity and housing costs continuing to drive underlying price pressures.

Headline CPI up 4.2%, down from 4.6% in March and below market expectations of 4.4%

Trimmed mean inflation edged up to 3.4% from 3.3% but in-line with consensus, with automotive fuel excluded in both months

Housing was the largest contributor at 6.3%, reflecting higher electricity, new dwelling and rent costs

Electricity prices up 22.5% year-on-year as Commonwealth and State government rebates roll off

Automotive fuel fell 7.0% month-on-month following the 1 April halving of the fuel excise, though still 23.5% above February levels pre-Middle East conflict

Freight and logistics flow-through visible in Postal services (up 12.4%) and New dwelling construction (up 4.7%) year-on-year

Another strong day for miners

[11:23 am] The S&P/ASX 200 Materials Index is on track for a fifth straight day of gains, up 0.97% today and up 6.96% since last Wednesday.

S&P/ASX 200 Materials Index (Source: TradingView)

BHP (+1.0%) and Rio Tinto (0.0%) both within 2% of recent all-time highs.

South32 (+4.2%) has experienced a vertical move, up 19.4% in the last five sessions.

South32 daily price chart (Source: TradingView)

Macquarie on Tuesday said Middle East supply disruptions may offset weak demand to drive aluminium deficits over the next 1-2 years, while alumina fundamentals remain challenging.

LME aluminium positioning extended after Middle East de-escalation rebound, with demand indicators soft and China inventories elevated, pointing to near-term price consolidation

Over 3Mt of supply disruption expected from the Middle East conflict, more than offsetting demand weakness and substitution

Resulting deficits likely to support higher aluminium prices and premiums over the next 1-2 years, regardless of whether flows through the Strait of Hormuz resume

Lithium stocks like MinRes, Liontown, IGO and PLS all slightly higher, up 0.5-1.0%. The same for gold, with the All Ords Gold Index up 0.98%.

Analysts' take on Goodman Group

[11:21 am] Goodman Group reaffirmed FY operating EPS guidance and retained its work-in-progress target on Tuesday, alongside continued growth in its global data centre powerbank, though the absence of new customer contracts or Australian capital partnership announcements disappointed investors expecting near-term leasing momentum. The stock dipped as much as 4.6% on the day, but finished the session down just 0.1%.

Bell Potter retained Buy, lowered target from $36.45 to $35.50. Sees powerbank growth supporting multi-year earnings visibility with phased lease signings, viewing the current valuation discount as reflecting execution timing rather than any erosion of competitive moat.

UBS retained Buy, target unchanged at $33.92. Highlights development yields potentially exceeding expectations, broader Australian capital partnership potential into Melbourne and lifting industrial development momentum at strong yields.

Jarden retained Buy, target unchanged at $35.56. Notes multiple data centre contracts under negotiation globally but flags subdued development starts and timing slippage as the key near-term downside risk.

Analysts' take on Santos

[10:37 am] Santos hosted its 2026 investor day on Tuesday, presenting a sustainable free cash flow profile anchored by Barossa and Pikka reaching plateau, alongside a disciplined ~$10 billion capex plan through 2030 focused on tier-one growth in Alaska, Papua New Guinea and the Beetaloo Basin.

Analysts viewed the strategy as a genuine inflection point, highlighting credible capital allocation, improving dividend sustainability and material undervalued upside from the three growth pillars.

Jarden retained Overweight, target unchanged at $8.75. Sees growth anchored by Barossa and Pikka plateau rates, with capital discipline supporting sustained low-cost free cash flow and improving dividend yield potential into decade-end.

RBC Capital Markets retained Outperform, target unchanged at $8.50. Points to substantial undeveloped Alaska reserves, off-balance-sheet financing for Papua LNG and a clear capital allocation framework supporting Beetaloo resource conversion.

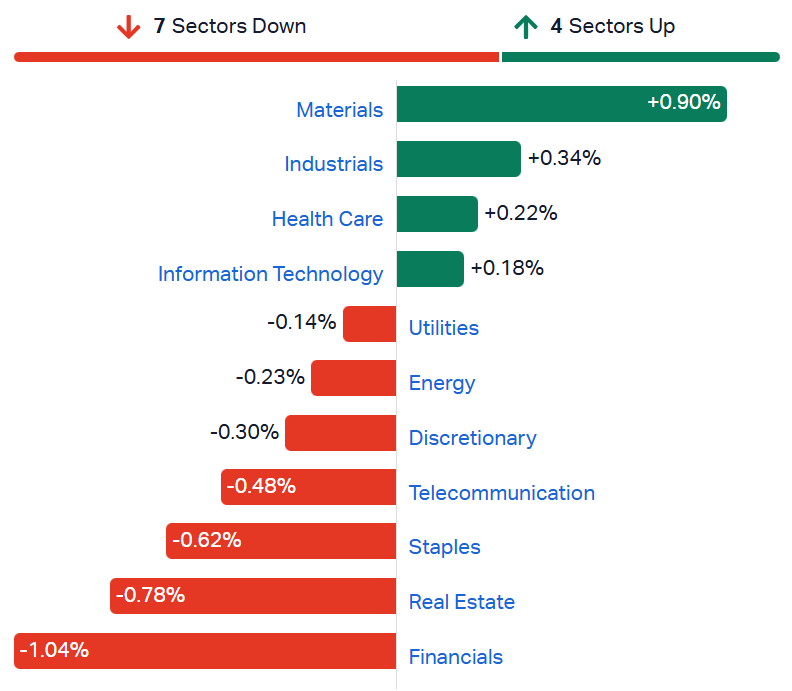

ASX 200 lower as banks tumble

[10:28 am] The S&P/ASX 200 is down 0.19% in early trade. Two of the market's largest sectors are moving in opposite directions, with Materials up 0.90% and Financials down 1.0%.

S&P/ASX 200 sectors (Source: TradingView)

Top ASX 200 gainers

[10:21 am] A very strong session for various resource-related sectors, including aluminium, uranium and rare earths. Meanwhile, Fisher & Paykel continues to rally off of yesterday's FY26 result, it's now up 12% in two days.

Ticker | Company | % Chg | Price |

|---|---|---|---|

S32 | South32 | 4.97% | $4.86 |

PDN | Paladin Energy | 3.61% | $11.49 |

LYC | Lynas Rare Earths | 3.60% | $19.59 |

MP1 | Megaport | 3.55% | $14.28 |

AAI | Alcoa Corporation | 3.20% | $104.34 |

SGM | Sims | 3.16% | $25.17 |

JHX | James Hardie | 2.71% | $29.90 |

NXG | Nexgen Energy | 2.66% | $15.43 |

FPH | Fisher & Paykel | 2.63% | $30.84 |

CSC | Capstone Copper | 2.58% | $14.70 |

Top ASX 200 losers

[10:21 am] The ASX (exchange operator) continues to tumble after announcing a surprise increase in cost and capex guidance on Tuesday. The stock fell 13.2% on the day, and down a further ~4% this morning.

Ticker | Company | % Chg | Price |

|---|---|---|---|

ASX | ASX | -4.23% | $48.87 |

APE | Eagers Automotive | -4.16% | $21.42 |

EDV | Endeavour Group | -3.57% | $2.97 |

L1G | L1 Group | -2.83% | $1.03 |

GNE | Genesis Energy | -2.48% | $1.97 |

MAH | Macmahon | -2.12% | $0.93 |

SPK | Spark New Zealand | -1.87% | $1.58 |

LOV | Lovisa | -1.78% | $22.09 |

NAB | National Australia Bank | -1.70% | $37.35 |

CGF | Challenger | -1.69% | $8.70 |

Web Travel Group rallies, Endeavour and Eagers tumble

[10:06 am] Here are some early reactions for the mid-to-large caps that had market-sensitive announcements this morning.

Eagers Automotive (-5.1%): Trading update flagged a record first half on two months of CanadaOne Auto contribution and a record FY26, with order bank up 70% since December and orders running 29% ahead of deliveries on supply constraints.

Endeavour Group (-3.9%): Investor Day unveiled a $300m cost-out by FY29, exit of most of the winery portfolio and accelerated Hotels capex, but the dividend payout ratio was cut to 50-75% (from ~70-80% historically). Clearly, some selling pressure from income-oriented investors.

Nufarm (+4.3%): 1H26 underlying EBITDA up 18% to $243m (1% beat) at the top of guidance, though underlying NPAT of $52m missed by 10%. Leverage down to 3.6x targeting ~2.0x by FY26-end, FY26 outlook reaffirmed and Emerging Platforms uplift lifted to $40m (from $30m).

Web Travel Group (+6.7%): FY26 broadly in line (TTV $5.8bn, EBITDA $148.4m) with TTV margin of 6.8% ahead of Macquarie's 6.5%, but first 8 weeks of FY27 TTV up just 4% in constant currency. Some soft spots in the result, though margins running ahead of expectations for both FY26 and FY27 guidance.

Eagers flags record first half on CanadaOne contribution, FY26 record year in sight

[9:46 am] Strong order intake and bank growth is offsetting some near-term supply constraints, with the consolidated first half set for a record print on two months of CanadaOne Auto.

Australia and NZ turnover up around 5% year-to-date through April 2026, with orders exceeding deliveries by more than 29% as supply constraints defer delivery timing

Order bank up 70% since December 2025, with order intake at record levels

Independent used business (easyauto123 and Carlins) profit before tax up 40% year-on-year, delivering a record start to the year

1H26 underlying PBT expected in line with or slightly ahead of 1H25 across Australia and NZ, with two months of CanadaOne Auto contribution positioning the group for a record first half at the consolidated level

2H26 outlook positive on improved Toyota supply following a materially constrained first half, plus full-half contributions from CanadaOne and recent Australian acquisitions

May and June traditionally represent 20-25% of full year profits, with the group guiding to growth in both turnover and earnings and a record year for FY26

Eagers has held up relatively well compared to some retail peers, down 8.5% YTD vs. S&P/ASX 200 Discretionary (-13.7%).

Company page: Eagers Automotive (APE)

Amaero pauses titanium powder output 4-6 weeks after Tennessee fire

[9:45 am] A small fire during planned exhaust system remediation work prompts a temporary titanium production pause, though management does not expect a material revenue impact this quarter.

Small contained fire occurred 26 May during planned remediation work, with no injuries and no damage to the building or capital equipment

Titanium powder production expected to pause for around 4-6 weeks while the review and any remediation is completed

PM-HIP manufacturing and refractory powder production are not expected to be impacted

Pause not expected to materially impact current quarter revenue, given inventory on hand and customer inventory levels

Company page: Amaero (3DA)

Fed's Kashkari: Middle East inflation could kick off a series of hikes

[9:41 am] Minneapolis Fed President Neel Kashkari dropped some rather hawkish commentary a few hours ago, in an interview with Nikkei.

"The next rate change could be either a cut or a hike,” adding that it would depend on inflation’s behaviour

The persistent closure of Hormuz could affect long-term inflation expectations in households and businesses, which "could become anchored"

The bombshell comment: “Federal funds rate increases, potentially a series of them, could be warranted."

Endeavour reshapes portfolio with $300m cost-out, adjusts dividend payout ratio

[9:36 am] Endeavour Group's Investor Day presentation highlights three priority areas to position the business for growth: i) reset multi-brand retail strategy; ii) unlock growth potential in hotels and iii) simplify operations and reduce costs.

$300m of cost savings targeted by FY29, including $100m in FY27, as part of the three-year transformation program

Group exiting the majority of its existing winery and vineyard portfolio, including Chapel Hill, Oakridge and Josef Chromy, with Pinnacle Drinks repositioned to back Retail and high-performing brands

Targeted dividend payout ratio revised to 50-75% of group underlying NPAT (from prior policy) to fund growth investment

Capital deployment in Hotels to lift, with light touch renewals, refurbishments and whole-of-venue repositionings

Management commentary: "We examined the business through a number of lenses and have made the tough choices required to deliver the Group's next phase of growth"

It does read like a net positive, especially for a stock that's down 16% YTD and trading around record lows. The main concern here should be the dividend policy change, as Endeavour has historically maintained a payout ratio around 70-80%. UBS modelling (May-26) expected this trend to continue well into FY30, which implies a yield of around 4-5%. The revised range could result in some dividend uncertainty, and drive some selling pressure from income-oriented holders.

Company page: Endeavour Group (EDV)

Sovereign Metals confirms heavy rare earths across Kasiya pits

[9:28 am] Drilling confirms dysprosium, terbium and yttrium concentrations at roughly 7 times the world's largest rare earth producers, with monazite shaping up as a potential third revenue stream from existing DFS tailings at no additional mining cost.

Average 2.5% DyTb and 11.8% Yttrium within the TREO basket, vs 0.4% DyTb and 1.7% Yttrium across the five largest rare earth producers, with near-surface (0-6m) ratios up to 3.1% DyTb and 17.2% Yttrium

Monazite concentrate recovered from four planned pits in the Kasiya DFS mine plan, including Year 1 production pits, with all four magnetic rare earth elements (Nd, Pr, Dy, Tb) plus Yttrium present

Potential third revenue stream from the non-conductor tailings stream of the DFS flowsheet, with no additional mining or new primary processing circuit required (confirmation in progress)

Western supply-chain backdrop strengthening, with DyTb and Yttrium subject to Chinese export controls and USA Rare Earth agreeing to acquire Serra Verde Group for ~US$2.8bn on 20 April 2026, underpinned by a 15-year US government-backed offtake with floor pricing

Company page: Sovereign Metals (SVM)

Nufarm 1H26 EBITDA tops the range as deleveraging accelerates

[9:23 am] Underlying EBITDA came in at the top end of guidance with the FY26 outlook reaffirmed, though underlying NPAT fell short of consensus.

Underlying EBITDA up 18% to $243m vs $241m ests (1% beat), at the top of $239-244m guidance

Underlying NPAT up 35% to $52m vs $57.5m ests (10% miss)

Statutory NPAT up 28% to $38m vs $30.0m ests (27% beat)

Net debt down $135m to $1.23bn, with leverage at 3.6x (a 20% reduction year-on-year) and targeted at around 2.0x by FY26-end (from 2.7x at FY25)

FY26 outlook reaffirmed with strong uEBITDA growth expected, $50m cost savings on target, capex below $200m, and Emerging Platforms uEBITDA uplift lifted to $40m (from $30m prior) on the expanded bp carinata deal

CEO Rico Christensen: "We are pleased with first half performance and are well placed to deliver strong growth in underlying earnings and a significant reduction in leverage for the full year, consistent with previous guidance"

Company page: Nufarm (NUF)

Web Travel softer FY27 start as Middle East conflict weighs

[9:17 am] A somewhat positive FY26 result from Web Travel Group, with numbers mostly in-line with market expectations.

Group TTV up 20% to $5.8bn vs $5.80bn ests (in line)

Revenue up 20% to $394.1m vs $381.2m ests (3% beat)

Underlying EBITDA up 23% to $148.4m vs $148.9m ests (in line)

Underlying NPAT up 8% to $85.9m vs $85.7m ests (in line)

TTV margin lifted to 6.8% from 6.7%, with WebBeds EBITDA margin up 150bp to 43.8%, and cash conversion at 107% (from 73%)

Trading update (first 8 weeks): Bookings up 6%, TTV up 4% in constant currency but down 6% in AUD, with Middle East conflict materially impacting MEA and to a lesser extent APAC

FY27 outlook: TTV margins at least 6.5%, CapEx in line year-on-year, with circa $500m pro forma liquidity following the $250m Convertible Notes redemption

I want to say it reads somewhat positive, given:

WEB shares are down 49.7% year-to-date

Most figures in-line with expectations, TTV margin of 6.8% is ahead of Macquarie (May-26) ests of 6.5%

However, TTV is up just 4% in the first 8 weeks, while Macquarie is looking for 13.2% growth for FY27 (first 8 weeks is not a representation for the full-year but you get the idea)

FY27 TTV margin of at least 6.5% also strong vs. Macquarie ests of 6.4%

Company page: Web Travel Group (WEB)

Westpac hit with $26m penalty over hardship failures

[9:16 am] The Federal Court labelled Westpac's failure to respond to more than 200 hardship requests between 2017 and 2023 as "grossly negligent" and systemic, with Justice McEvoy rejecting the bank's $10m penalty submission as "derisory".

$26m civil penalty imposed, well above Westpac's proposed $10m, with breaches spanning Westpac, St George, Bank SA and Bank of Melbourne customers

Failures affected vulnerable customers seeking hardship assistance after job loss, illness, domestic abuse or natural disasters, with some waiting weeks beyond the legal deadline and others receiving no response

Downstream harm flagged by the court, including adverse credit file entries and debts sold to third-party purchasers who actively pursued repayment

Adds to a broader ASIC crackdown on hardship handling, following NAB's $15.5m penalty and ANZ's $40m penalty last year, with proceedings also underway against Resimac

Company page: Westpac (WBC)

Infratil FY26 earnings call highlights

[9:13 am] Infratil reported its FY26 earnings on Tuesday, though the stock dipped 4.9% as FY27 guidance came in below expectations due to higher costs and development losses.

At the earnings call, management leaned heavily into AI infrastructure and energy as the core growth pillars, with CDC and Longroad guidance underpinning a multi-year EBITDAF ramp and a further $1 billion of divestments planned to recycle capital.

FY27 guidance: CDC EBITDAF $680m-$720m on CapEx up to $2.1bn (ex-land), Longroad EBITDAF $120m-$135m with 1.7GW of new project construction

CDC EBITDAF targeted at $1bn in FY28 and $2bn by FY30, with the growth pipeline being extended by at least 1GW to support contracted capacity beyond 2030

$1bn-plus of further divestments planned over the medium term (excluding the recent $495m contract sale), with proceeds redirected to scalable AI infrastructure and energy assets

CDC valuations reference mid-to-high teens contracted EBITDA multiples, with CapEx guidance unchanged at mid-teens per megawatt ex-land

Development pipeline gains weighted to 2029 onward with larger contributions post-2030, while BBB+ credit rating to be maintained or improved to support funding flexibility

Company page: Infratil (IFT)

Experience Co flags weaker Q3 trading update

[9:11 am] Revenue and EBITDA both declined in Q3, with skydiving volumes the key drag and fuel costs creeping higher amid Middle East-driven price pressure. This joins the long list of companies that have flagged late-March and April as a key turning point for consumer spending patterns and behaviour.

Revenue down 3% to $33.0m

EBITDA down 11% to $5.1m

Skydiving revenue down 5% to $19.0m

Adventure Experiences revenue flat at $13.9m

April volumes: Skydive Australia down 17% year-on-year, Skydive NZ down 6% on weather (though booking trends remained strong and well ahead year-on-year), Reef Unlimited down 10%, Treetops Adventure up 12%

"These conditions are expected to continue to impact the Group’s future financial performance in the short to medium term."

Fuel costs rose from around 4% of revenue pre-Middle East conflict to around 6% in March and April

Company page: Experience Co (EXP)

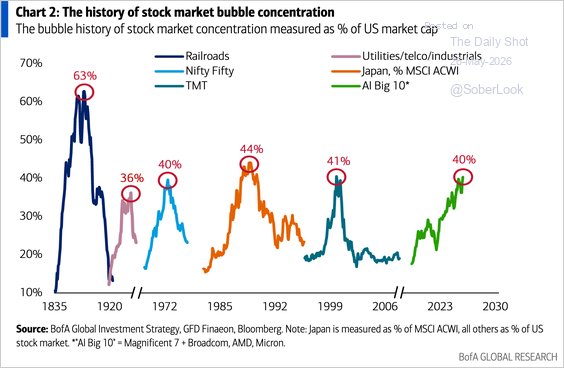

AI concentration hits an unprecedented level

[9:07 am] Parabolic gains for AI-related stocks has seen stock market concentration hit extreme levels.

Semiconductors make up approximately 22% of the S&P 500

Big AI now at 40%

The 41 AI-related stocks in the S&P 500 now make up 61% of the index

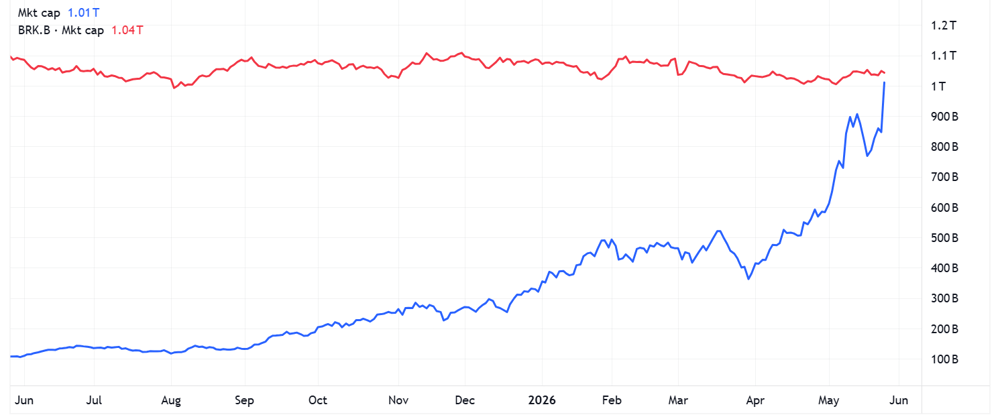

Micron now the 10th largest S&P 500 stock

[9:04 am] The 19% surge lifts Micron into the trillion dollar club, and now the S&P 500's tenth largest stock.

Micron had a market cap of just over US$100 billion a year ago and now on track to surpass Berkshire Hathaway. Insane stuff.

Micron (blue) vs. Berkshire Hathaway (red) | Source: TradingView

Micron crosses $1tn as UBS triples target on AI memory squeeze

[9:01 am] UBS lifted its price target to $1,625 from $535, arguing structural AI-driven changes in memory warrant a re-rating, with long-term agreements offering partially fixed pricing.

Shares popped 19%, taking Micron above a $1tn market cap for the first time, with the stock more than tripling year to date

UBS's new target implies shares could more than double from Friday's close, citing long-term agreement opportunities with partially fixed pricing

UBS: "We believe the market will start to put a more 'normal' multiple on the stock and MU will continue to re-rate higher as more details emerge about the structural changes AI has driven to the entire memory complex"

Global memory shortage has allowed Micron, SK Hynix and Samsung to hike prices as AI agentic workloads drive demand for memory alongside CPUs

Source: CNBC

Ferrari tumbles as Luce EV debut sparks "design hate" backlash

[8:58 am] Ferrari's first fully electric vehicle, the Luce, was met with a sharp investor revolt amid concerns the model dilutes brand equity and burdens returns with high R&D spend.

Milan-listed shares fell about 8% and US-listed shares dropped 5.3%, with the Milan stock now down more than 32% over the last 12 months

Luce priced at around €550,000, hits 60mph in roughly 2.5 seconds with a top speed of 192mph, and is Ferrari's first five-seater, with deliveries from Q4

Morningstar's Michael Field flagged fan disappointment that EV adoption dilutes the supercar brand, while investors fear high R&D costs will pressure returns

Former chairman Luca di Montezemolo, now on rival McLaren's board, said he hopes "they take off the prancing horse logo from that car"

Launch comes as Porsche and Lamborghini have scaled back their own EV plans on weak demand, with all Luce components built in house and design handled by Jony Ive's LoveFrom

Source: CNBC

JPMorgan calls time to buy low-vol stocks as rate hike fears seen overdone

[8:57 am] JPMorgan's Mislav Matejka argues the Iran war doesn't repeat the 2022 inflation playbook, opening up a contrarian opportunity in beaten-up low-volatility names like staples, utilities and insurers.

Markets pricing one Fed hike by March 2027 and two ECB hikes by year-end, which JPMorgan views as overdone given the conflict parties' focus on an off-ramp

Bond yields and oil prices seen lower in 6-12 months, with weaker US employment and wage growth making a wages-prices stagflationary spiral less likely

Goldman Sachs basket tracking US cyclicals over defensives trading at levels last seen 18 years ago, with low-vol stocks lagging the AI-driven rally and hit by rising global rates

Matejka sees opportunity in low-vol regardless of yield direction. A spike toward 5% on 10-year Treasuries could break the inverse correlation, while a fade in yields would lift them as it did pre-Iran war

Source: Bloomberg

Treasury curve flattens to tightest in a year as Warsh-era Fed seen staying hawkish

[8:55 am] The 5-and-30 year spread hit its tightest level since May 2025 as a short-end selloff reflects traders pricing in a higher-for-longer Fed under new chair Kevin Warsh, with Iran-driven inflation upending the easing bias.

5s30s spread narrowed to 81bp Friday, the tightest since May 2025, before edging back to around 82bp Tuesday, while 2s30s hit its tightest since July

Move driven by a selloff in shorter-dated Treasuries as the Iran war sparked the biggest inflation surge since 2023, prompting officials to drop their easing bias

Fed Governor Christopher Waller, previously a dove, said last week the next move is now just as likely to be a hike as a cut

ING, Goldman Sachs and Barclays flagging that elevated long-end yields may not fully unwind even if oil-driven inflation eases, given public debt burdens and AI capex fallout

Source: Bloomberg

US and Iran edge closer to deal as Hormuz strikes test fragile progress

[8:46 am] Reported memorandum of understanding would pause fighting and lift Hormuz constraints, though nuclear enrichment terms and parallel Israel-Hezbollah escalation keep the path tenuous.

Draft deal would halt fighting for 60 days, lift Strait of Hormuz constraints for 30 days and waive transit fees during a 60-day negotiation window

Iran reportedly agreed to surrender its highly enriched uranium stockpile, but US is pushing for a 20-year enrichment moratorium versus Iran's shorter offer, with release of frozen Iranian assets tied to a final nuclear agreement

Trump said negotiations were "proceeding nicely" but also flagged Sunday that a deal isn't fully negotiated yet

US launched fresh strikes Monday on Iranian missile sites and vessels in the Strait of Hormuz, with Iran claiming it downed a US drone Tuesday and warning against ceasefire violations

Netanyahu said Israel will intensify strikes against Hezbollah, with the IDF hitting over 70 infrastructure sites in Lebanon, while Iran has demanded cessation of Lebanon hostilities as part of any agreement

Diplomatic traction trumps Hormuz strikes

[8:45 am] Markets continue to look through Middle East kinetic flare-ups toward a potential deal, while bullish earnings revisions and AI capex demand square off against structural pressure on sovereign yields.

US and Israeli jets struck Iranian vessels in the Strait of Hormuz, but markets focused on reported diplomatic traction, though "deal imminent" calls have misfired before and nuclear remains the sticking point

Jefferies flagged a surge in the earnings revision ratio and favourable near-term guidance trends, while Morgan Stanley pointed to demand inelasticity in the AI capex boom

Goldman Sachs noted short exposure in US macro products (Index + ETF) at a 10-year high, raising index squeeze risk, but also five-year highs in HF exposure to US tech and a 90th percentile momentum factor tilt

Deutsche Bank highlighted large-cap tech positioning in the 93rd percentile going back to 2010, despite overall equity positioning looking fairly neutral

Drivers of upward pressure on yields increasingly viewed as structural, alongside a depressed US equity risk premium and a flattening Treasury curve

S&P and Nasdaq notch record closes as momentum rally rolls on

[8:43 am] Memory stocks led another leg higher in US equities, with Micron crossing $1 trillion market cap after UBS tripled its price target, while easing Iran tensions and a Treasury rally added fuel.

S&P 500 (+0.61%) and Nasdaq (+1.19%) closed at fresh all-time highs, with the Russell 2000 topping 2,900 for the first time ever as small caps outperformed

Micron surged 19.2% after UBS tripled its price target, crossing $1tn market cap and anchoring a broad semis/memory-led rally

US 10-year yield fell 7bp to 4.49%, now down 17bp over four sessions as inflation concerns eased and traders pared near-term Fed hike bets

Bull case leans on strong earnings growth and upward revisions, while extended positioning, narrow breadth, sticky inflation and the market still pricing 18bp of hikes through year-end remain points of scrutiny

Good morning!

[8:30 am] ASX 200 futures are down 3 pts (-0.03%).

The overnight session in a nutshell:

S&P 500 and Nasdaq hit record closes, though Dow lagged (-0.23%) as sectors like Healthcare, Staples and Energy underperformed

Micron surged 19% to crack the US$1 trillion market cap club after UBS nearly tripled its price target to $1,625

10-year Treasury yield fell 6 bps to 4.49%, Trump says US-Iran deal isn't fully negotiated while US fired "self-defence" strikes against Iran