ASX 200 Live Today - Wednesday, 20th May

The S&P/ASX 200 has given back Tuesday's gains as rising yields and high oil prices continue to pressure global equities.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Wednesday, May 20. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

What a weak market: ASX 200 gives back gains

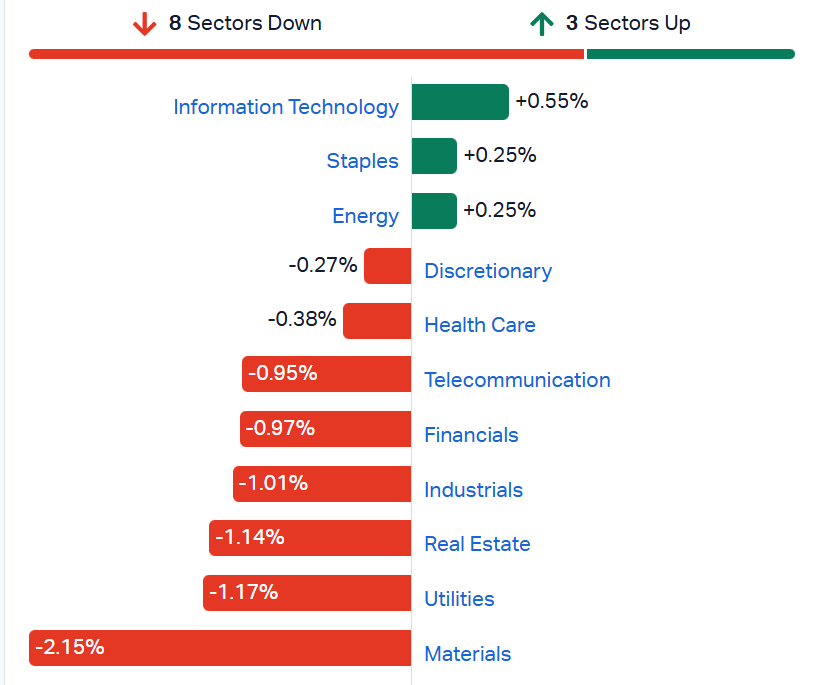

[2:10 pm] ASX 200 down 1.12% and still hovering around session lows. Sectors that opened strongly (Tech, Staples and Discretionary) have given back the bulk of their gains, if not trading lower. The rising yields, US dollar and oil backdrop is weighing on sectors like Materials (-2.0%) and Real Estate (-1.7%), while Financials (-1.1%) dip after bouncing ~3.5% in the last three sessions.

The Aussie 10-year experienced a brief dip in early trade, but now almost flat for the session at 5.08% and on the cusp of breaking out to the highest since July 2011.

Australia 10-year yield (Source: TradingView)

The pain has been far more pronounced for the smaller end of town. The S&P/ASX Emerging Companies Index is on a five-day losing streak, down 8.6%.

S&P/ASX Emerging Companies Index (Source: TradingView)

That's a wrap! The path of least resistance for markets remains lower against this challenged backdrop of soaring yields, high oil prices and an increasingly hawkish outlook for global interest rates. Nvidia reports tonight, but even a blowout result might not shift what's currently dragging markets lower.

Analysts' take on TechnologyOne

[1:15 pm] TechnologyOne's 1H26 result on Tuesday was broadly in line at the headline level, with a revenue miss attributed to late-half contract timing rather than weakening demand, while constant currency ARR growth of ~19% marked a record period and PBT came in slightly ahead of consensus. The stock finished 2.9% lower on the day.

RBC retained Outperform, target unchanged at $33.00. Viewed the market reaction as an overreaction, with the capitalised commission doubling and Showcase pipeline signalling a strong 2H conversion setup.

JPMorgan retained Overweight, target unchanged at $32.00. Flagged Showcase as a deliberate and returnable cost drag, with the AI product suite considered best positioned in coverage and SaaS+ margin pressure expected to unwind from FY27.

Morgans upgraded to Accumulate from Hold, raised target from $31.20 to $32.30. Underlying momentum seen as solid ex-FX, with PLUS pipeline build supporting NRR recovery and SaaS+ driving longer-duration, higher-value contracts.

McWilliam suspected behind big Southern Cross Media trade

[1:14 pm] The AFR reported a sizeable selldown by Southern Cross' Aitken Mount on Wednesday morning, with former Stokes family lieutenant Bruce McWilliam suspected as the buyer.

Aitken Mount crossed 20 million shares at 56 cents, representing 4.2% of shares on issue or $11.2m worth

McWilliam previously used Aitken Mount in April to build a 5.3% stake, much of which was acquired from long-time shareholder Spheria Asset Management

If confirmed, the trade would lift his holding to 9.5%, moving him into the company's top five shareholders

Source: AFR

Catapult gives back early gains

[1:10 pm] Catapult has gone full circle after opening 9.7% higher, surging to a session high of 23.6% and now up 9.2%. The FY26 results announcement this morning was mostly ahead of market expectations, though featured a widening loss of -$24 million vs. -$8.8 million a year ago.

ASX 200 sharply lower

[12:42 pm] The S&P/ASX 200 has trended sharply lower, now down 1.11%, effectively giving back the entirety of yesterday's ~1.1% bounce.

Tech, Staples and Energy continue to trade in positive territory, but well off session highs (e.g. Tech up as much as 1.5% in early trade, now up just 0.5%). While sectors like Telcos, Financials, Industrials, Utilities and Real Estate opened relatively mixed, they're now all down around 1%. It's getting ugly out there.

S&P/ASX 200 sectors (Source: Market Index)

Tech stocks mixed

[12:10 pm] The S&P/ASX 200 Tech Index is up 1.6%, reflecting slight gains for heavyweights Wisetech and Xero, as well as results-driven gains from Catapult and TechnologyOne (announced yesterday).

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

CAT | Catapult Sports | 18.9% | $3.43 | -17.7% |

TNE | Technology One | 8.8% | $30.26 | -14.6% |

360 | Life360 | 1.8% | $18.32 | -41.1% |

DTL | Data#3 | 1.5% | $8.39 | 8.5% |

XRO | Xero | 1.3% | $79.67 | -56.0% |

DGT | Digico Infrastructure Reit | 1.1% | $2.65 | -18.7% |

OCL | Objective Corporation | 0.9% | $10.63 | -39.9% |

HSN | Hansen Technologies | 0.8% | $4.91 | -3.7% |

WTC | Wisetech Global | 0.7% | $38.38 | -62.0% |

PME | Pro Medicus | 0.1% | $130.42 | -53.4% |

DDR | Dicker Data | 0.1% | $8.73 | 0.9% |

NXL | Nuix | -0.4% | $1.33 | -44.3% |

MP1 | Megaport | -0.5% | $12.54 | -0.1% |

CDA | Codan | -0.5% | $39.86 | 135.4% |

NXT | NextDC | -0.7% | $14.46 | 9.3% |

SDR | Siteminder | -0.7% | $2.75 | -37.5% |

PPS | Praemium | -0.8% | $0.65 | -7.1% |

IRE | Iress | -1.0% | $5.73 | -31.7% |

MAQ | Macquarie Technology Group | -1.3% | $73.56 | 16.9% |

BVS | Bravura Solutions | -1.3% | $2.23 | 10.4% |

AD8 | Audinate Group | -2.6% | $2.21 | -68.4% |

WBT | Weebit Nano | -5.0% | $6.05 | 249.7% |

Japanese stocks under pressure as bond yields approach 3%

[12:08 pm] Rising Japanese government bond yields are testing equity market resilience as the gap between nominal growth and borrowing costs narrows.

10-year JGB yield hit 2.8% on Monday, the highest in roughly 30 years, with 3% seen as the level that would place a tangible burden on the real economy

Nikkei 225 fell 4.3% over four days as upward pressure on yields continued

Spread between nominal GDP growth (4.2% for fiscal 2025) and long-term yields is steadily narrowing, with sustainable nominal growth estimated at just 2.5%

Market concentration risk is elevated, with roughly 80% of Nikkei 225 gains since end of March driven by just the top 10 contributors including SoftBank and Kioxia, up from about 60% in the January-February rally

Source: Bloomberg

Webjet at record lows

[11:23 am] Webjet dipped as much as 18.3% in early trade, now down 10% to fresh record lows. For context, Webjet listed in September 2024 as part of its demerger from Webjet Travel Group (hence the record low).

The company's FY26 result flagged a wide net profit miss, along with downbeat management commentary and a substantial reduction in Virgin commercial arrangements. Here are the key numbers from the earlier post:

Revenue up 1% to $136.4m vs $133.5m ests (2% beat)

Underlying NPAT down 24% to $13.6m vs $17.4m ests (22% miss)

TTV down 3% to $1.46bn vs $1.43bn ests (2% beat)

FY26 total dividends of 4 cps (>100% payout of underlying NPAT)

"Operating conditions remain fluid and challenging, with ongoing geopolitical conflicts, together with continued inflationary pressures and low consumer sentiment."

"In addition, FY27 is expected to be materially impacted by lower airline commissions, alongside RBA surcharging regulation changes and lower variable revenue items."

Webjet OTA: Bookings and TTV were down 12% and 15% espectively with international leisure demand continuing to shift toward short-haul Asian destinations, contributing to lower average booking values and TTV

Virgin will substantially reduce commission streams and commercial arrangements from 1 July 2026, with an estimated $3.0m revenue impact

Copper stocks give back gains

[11:18 am] Last Monday and Tuesday was euphoric for copper miners, as copper prices soared to record highs of US$6.66/lb.

Prices are now down 6.5% in the last five sessions, including a 2.2% fall overnight to US$6.21/lb. Most copper names are down 2-4% in early trade.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

AIS | Aeris Resources | -4.7% | $0.41 | 138.2% |

HGO | Hillgrove Resources | -4.4% | $0.04 | 16.2% |

CYM | Cyprium Metals | -2.4% | $0.41 | 70.5% |

CSC | Capstone Copper Corp | -2.4% | $12.80 | 70.4% |

SFR | Sandfire Resources | -2.0% | $17.72 | 65.6% |

HCH | Hot Chili | -2.0% | $1.65 | 244.6% |

BHP | BHP Group | -1.9% | $57.57 | 47.5% |

FFM | Firefly Metals | -1.9% | $1.80 | 93.5% |

AR1 | Austral Resources Australia | -1.2% | $0.08 | -49.7% |

MC2 | Marimaca Copper | 0.1% | $8.58 | -11.5% |

29M | 29Metals | 0.8% | $0.26 | 85.5% |

CPM | Cooper Metals | 5.0% | $0.06 | 61.5% |

Gold stocks broadly lower

[11:19 am] The All Ords Gold Index is down 3.0% and on track to record a five-day skid, trading at the lowest since 30 March.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

ALK | Alkane Resources | -4.8% | $1.46 | 102.4% |

CYL | Catalyst Metals | -4.6% | $5.22 | -27.4% |

VAU | Vault Minerals | -4.1% | $4.31 | 54.0% |

RSG | Resolute Mining | -4.0% | $1.20 | 104.3% |

EVN | Evolution Mining | -3.8% | $11.50 | 40.2% |

NEM | Newmont | -3.8% | $147.59 | 86.7% |

RRL | Regis Resources | -3.6% | $6.23 | 34.8% |

BGL | Bellevue Gold | -3.4% | $1.49 | 67.1% |

AMI | Aurelia Metals | -3.3% | $0.29 | -3.3% |

GMD | Genesis Minerals | -3.2% | $5.89 | 49.7% |

RMS | Ramelius Resources | -3.1% | $3.12 | 23.8% |

BC8 | Black Cat Syndicate. | -3.1% | $1.05 | 26.9% |

WGX | Westgold Resources | -3.0% | $5.06 | 94.4% |

SBM | St. Barbara | -2.9% | $0.60 | 94.2% |

PNR | Pantoro Gold | -2.7% | $3.07 | -5.4% |

PRU | Perseus Mining | -2.3% | $5.26 | 54.1% |

EMR | Emerald Resources | -2.0% | $5.75 | 35.0% |

CMM | Capricorn Metals | -2.0% | $12.57 | 43.4% |

NST | Northern Star Resources | -1.6% | $19.55 | 1.8% |

OBM | Ora Banda Mining | -0.2% | $1.40 | 37.5% |

MEK | Meeka Metals | 6.1% | $0.12 | -6.2% |

Beach Energy CEO flags M&A interest amid domestic gas reservation policy

[10:55 am] Beach Energy's CEO told Bloomberg the company could become a more attractive takeover target as export-focused LNG producers look to offset new domestic supply obligations under the government's gas reservation policy.

Beach Energy sells exclusively to the domestic market, making its portfolio appealing to east coast LNG exporters needing to offset domestic supply obligations

CEO Brett Woods sees "some risk of some of the larger players starting to look at Beach"

Australian government policy announced earlier this month will require LNG exporters to set aside 20% of new production for the domestic market

New rules apply to prospective contracts and the spot market from 1 July 2027

Source: Bloomberg

Analysts' take on MinRes

[10:33 am] MinRes held an investor site tour at Wodgina and announced the restart of Bald Hill on Tuesday. Analysts viewed the restart as a lower-risk, capital-efficient pathway to volume growth and margin improvement amid the lithium price recovery. Key positives from the tour included improving ore quality, recovery gains, faster-than-expected three-train operation at Wodgina, and a more disciplined capital allocation framework.

Macquarie retained Outperform, target unchanged at $75.00. Highlighted smooth COO-led succession planning, Stage 3 ore quality inflection supporting margins, and a preference for recovery improvements and debottlenecking over Train 4, with underground optionality extending Wodgina's mine life beyond 20 years.

RBC Capital Markets retained Outperform, target unchanged at $70.00. Noted Wodgina underground is now tangible optionality, succession planning reflects organisational maturity, and regional exploration around Wodgina Queen is building, but cautioned that geo-met variability at depth remains a key unappreciated execution risk.

ASX 200 struggles as miners dip

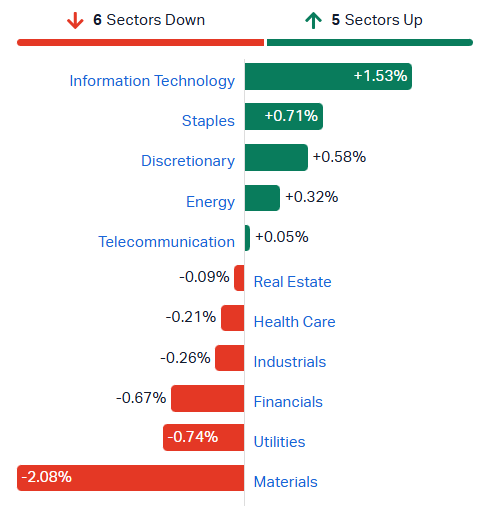

[10:29 am] ASX 200 down 0.49% in early trade, as declines from Financials (-0.6%) and Materials (-2.0%) weigh on the index.

CBA (-0.3%) is trading slightly lower after a four-day winning streak, while heavyweights BHP (-1.8%), Rio (-1.8%) and Fortescue (-0.9%) trade broadly lower after a rough overnight session for commodity prices.

S&P/ASX 200 sectors (Source: Market Index)

Catapult soars 20% in early trade

[10:13 am] Catapult opened around 9% higher, now up 20% to a six week high of $3.46.

Despite reporting a widening year-on-year loss, its 1H26 result was broadly ahead of market expectations.

Revenue up 19% (CC) to $140.7m vs $139.0m ests (1% beat)

Management EBITDA up 67% to $24.7m vs $23.0m ests (7% beat)

NPAT loss of ($24.0m) vs ($26.2m) ests (8% beat)

Closing ACV up 28% (CC) to $133.8m vs $133.4m ests (in-line)

Free cash flow ex-transaction costs of $6.5m, above the March trading update range of $5-6m

FY27 outlook: Strong ACV growth with low churn, continued margin improvement towards targets and higher free cash flow as the business scales

Catapult has experienced an aggressive build up in short interest in recent months, from ~1.3% in November to a high of 7.9% in mid-March. Short interest has since tapered off to a still-elevated 6.2%, which might explain the squeeze-like action this morning.

Source: Shortman

Top ASX 200 gainers

[10:10 am] Tech stocks are trading sharply higher, while coal, aluminium and energy stocks also catch a bid.

Ticker | Company | % Chg | Price |

|---|---|---|---|

TNE | Technology One | 6.29% | $29.55 |

AAI | Alcoa Corporation | 3.39% | $89.78 |

SMR | Stanmore Resources | 3.20% | $2.58 |

MCY | Mercury | 2.51% | $5.72 |

LOV | Lovisa | 2.50% | $21.71 |

ZIM | Zimplats | 2.16% | $16.05 |

ALD | Ampol | 2.13% | $36.45 |

DBI | Dalrymple Bay Infrastructure | 2.06% | $5.44 |

WTC | Wisetech Global | 1.97% | $38.87 |

XRO | Xero | 1.90% | $80.11 |

Top ASX 200 losers

[10:10 am] Copper and gold stocks are trading broadly lower after a rough overnight session for commodity prices.

Ticker | Company | % Chg | Price |

|---|---|---|---|

PDI | Predictive Discovery | -5.75% | $0.79 |

ALK | Alkane Resources | -4.90% | $1.46 |

KCN | Kingsgate Consolidated | -4.64% | $5.66 |

NXG | Nexgen Energy | -4.51% | $14.82 |

RRL | Regis Resources | -4.41% | $6.18 |

VAU | Vault Minerals | -4.23% | $4.30 |

MI6 | Minerals 260 | -4.18% | $0.76 |

WGX | Westgold Resources | -3.65% | $5.02 |

NEM | Newmont | -3.21% | $148.50 |

CSC | Capstone Copper Corp | -3.13% | $12.70 |

Copper gives back recent gains

[9:53 am] Copper experienced a sharp pullback overnight, down 2.2% to US$6.21/lb. Prices have now dipped 6.2% in the last five sessions.

The US-listed Global X Copper Miners ETF fell 3.0%, while NYSE-listed BHP shares also dipped 2.5%.

Copper daily price chart (Source: TradingView)

Gold hits seven-week low

[9:50 am] Another rough overnight session for gold, with prices down 1.8% to US$4,483 an ounce, the lowest since 27 March.

This drove the NYSE-listed VanEck Gold Miners ETF down 3.8%, while NYSE-listed Newmont shares also tanked 4.3% to the lowest since 30 March.

Gold daily price chart (Source: TradingView)

DBI lifts 2026-27 dividend guidance by 8.5%

[9:45 am] Dalrymple Bay Infrastructure announced a 2026-27 distribution guidance of 28.62 cents per share, with the per tonne charge it levies on coal terminal users rising ~8.1% to ~$4.02 a tonne.

Forecast Terminal Infrastructure Charge (the per tonne fee DBI charges customers for contracted capacity at the Dalrymple Bay Terminal) of ~$4.02/t for 2026-27, up ~8.1% year-on-year

Base charge up 4.09% to $3.66/t in line with CPI indexation

Non-expansionary capex charge (covering return on and of capital invested in maintaining the terminal) up ~$0.15 to ~$0.35/t, reflecting an additional $97.8m of commissioned spend over the past 12 months

Terminal remains fully contracted on a 100% take-or-pay basis at 84.2Mtpa to 30 June 2028, with evergreen renewal options

Q1-26 distribution of 6.750cps declared, in line with prior guidance (record 26-May, payable 12-Jun)

Company page: Dalrymple Bay Infrastructure (DBI)

Webjet Group misses on FY26 underlying NPAT, flags challenging FY27 outlook

[9:37 am] Webjet Group's FY26 underlying NPAT came in below market expectations, while FY27 is set to be materially impacted by lower airline commissions and weaker consumer demand.

Revenue up 1% to $136.4m vs $133.5m ests (2% beat)

Underlying EBITDA down 20% to $28.1m vs $27.5m ests (2% beat)

Underlying NPAT down 24% to $13.6m vs $17.4m ests (22% miss)

TTV down 3% to $1.46bn vs $1.43bn ests (2% beat)

FY26 total dividends of 4 cps (>100% payout of underlying NPAT)

Strong balance sheet with net cash of $93.9m, no borrowings and net assets of $138.4m

Outlook commentary was rather downbeat, with management noting:

"Operating conditions remain fluid and challenging, with ongoing geopolitical conflicts, together with continued inflationary pressures and low consumer sentiment."

"In addition, FY27 is expected to be materially impacted by lower airline commissions, alongside RBA surcharging regulation changes and lower variable revenue items."

Webjet OTA: Bookings and TTV were down 12% and 15% espectively with international leisure demand continuing to shift toward short-haul Asian destinations, contributing to lower average booking values and TTV

Domestically, leisure demand remains constrained by cost-of-living pressures, low consumer confidence and elevated airfares

Direct-to-business Bookings and TTV were up by approximately 20%, with demand, particularly international travel and ABV, moderating following relative resilience in FY26.

Company page: Webjet Group (WJL)

Catapult delivers record ACV growth in FY26

[9:33 am] Catapult Sports posted a strong FY26 with 28% constant currency ACV growth, beat on revenue and EBITDA, and pointed to continued momentum heading into FY27.

Revenue up 19% (CC) to $140.7m vs $139.0m ests (1% beat)

Management EBITDA up 67% to $24.7m vs $23.0m ests (7% beat)

NPAT loss of ($24.0m) vs ($26.2m) ests (8% beat)

Closing ACV up 28% (CC) to $133.8m vs $133.4m ests (in-line)

ACV growth ex-acquired up 18% (CC), with Performance & Health ACV +23% and Tactics & Coaching ACV +40% (CC)

Rule of 40 reached record 36% ex-acquired ACV (46% inclusive), with contribution margin expanding to 53% (vs 49% prior)

Free cash flow ex-transaction costs of $6.5m, above the March trading update range of $5-6m

FY27 outlook: strong ACV growth with low churn, continued margin improvement towards targets and higher free cash flow as the business scales

Company page: Catapult Sports (CAT)

Core Lithium kicks off mining at Finniss

[9:25 am] Core Lithium has commenced mining at the Grants open pit at its Finniss Lithium Operation, putting the restart on track for first spodumene concentrate shipment in the December quarter.

First blast and excavation activities initiated at the Grants open pit, marking the recommencement of mining at Finniss

Grants pit to provide approximately 784kt of ore, expected to deliver around 134kt of SC5 spodumene concentrate

First spodumene concentrate shipment targeted in the December quarter, with further shipments into CY2027

BP33 box cut and civil infrastructure works progressing in parallel to support longer-term underground production

Restart tracking in line with FID schedule and cost expectations, with NRW awarded the surface mining services contract in April 2026

Company page: Core Lithium (CXO)

Webjet flags Virgin Australia commission cuts to hit FY27 revenue

[9:20 am] Webjet Group has been notified that Virgin will substantially reduce commission streams and commercial arrangements from 1 July 2026, with an estimated $3.0m revenue impact.

Estimated revenue impact of ~$3.0m if the change had applied across FY26

Changes affect both agency and ancillary agreements, including performance-based commissions

Webjet flagged it will adjust its commercial and partnership strategy

For perspective, Webjet reported $139.7 million revenue in FY25.

Company page: Webjet Group (WJL)

Telcos warn of further price hikes after $7.3 billion regulatory blow

[9:09 am] The ACMA has set spectrum renewal fees at $7.32 billion for Telstra, Optus, TPG Telecom and NBN Co, with telcos warning consumers will bear the cost through higher mobile plan prices, according to the AFR.

ACMA finalised spectrum renewal price at $7.32bn, down just $20m from the December proposal of $7.34bn

Telstra on the hook for $2.8bn, the largest single share

Final figure well above ACMA's initial April 2024 proposal of $5.0-6.2bn but below the $8.2bn charged at the last renewal

80% of spectrum used by 30m mobile services is due for renewal between 2028 and 2032

Telstra has flagged potential Federal Court challenge, arguing the pricing could be "legally unreasonable"

TPG labelled the decision a "mobile tax" that would weaken competition and pressure investment in coverage

Optus and Telstra have already hiked plan prices twice inside 12 months, well above inflation, with further increases now flagged

Source: AFR

James Hardie flags transformational FY26 but macro pressures intensify

[9:04 am] Management flagged a tougher operating backdrop with markets declining mid-to-high single digits and affordability pressures continuing to weigh on housing. Here are some of the key comments from the Q4/full-year result.

"Market conditions remained challenging, with subdued building activity and ongoing affordability pressures. Siding & Trim experienced weather-related volume headwinds in February and early March, reflecting its geographic exposure across key new construction markets."

"Year-over-year comparisons were further impacted by elevated channel inventory levels in the prior year, creating an additional headwind to current quarter volumes."

"During the quarter, the Company fulfilled strong early buy orders, resulting in elevated channel inventory levels as sell-through, which was up low-single-digits, moderated in February and early March due to weather related disruptions.

“We are not assuming a market recovery. What gives us confidence is execution — synergy realization, our enhanced go-to-market model, manufacturing cost actions taken in FY26, and disciplined capital allocation."

James Hardie 4Q26 mixed, guides to $500 million in free cash flow in FY27

[8:57 am] James Hardie reported a mixed fourth quarter, though FY27 guidance points to adjusted EBITDA growth of 4-8% and a meaningful step-up in free cash flow.

Q4 revenue up 45% to $1.40bn vs $1.41bn ests (in-line), with organic net sales down 1%

Q4 adjusted EBITDA of $380.9m vs $366.0m ests (4% beat)

Q4 adjusted net income of $172.6m vs $177.9m ests (3% miss)

FY26 net sales up 25% to $4.84bn vs. $4.82bn ests (in-line)

FY26 adjusted EBITDA of $1.27bn vs. $1.25bn ests (1.6% beat)

FY27 guidance: Pro forma adjusted EBITDA growth of 4-8%, with organic growth expected in Siding & Trim

FY27 free cash flow guided to at least $500m

Unclear if FY27 guidance is comparable to Macquarie's FY27 EBITDA ests of $1.54bn and free cash flow of $668m

Cost synergies running ahead of schedule, with confidence in achieving the $125m cost synergy target ahead of the original three-year timeline

NYSE-listed James Hardie shares are down 4.1% in after hours.

Company page: James Hardie Industries (JHX)

Infratil trims Contact Energy stake to fund future growth

[8:49 am] Infratil has sold 5.0% of Contact Energy via a fully underwritten block trade at NZ$9.25 per share, raising approximately NZ$495 million to support future growth opportunities.

Infratil's remaining Contact stake reduced to approximately 9.08%

Committed to retaining remaining shares through to at least Contact's FY26 full year results (expected ~18 August 2026)

No immediate funding requirements, with the divestment programme described as on track

Company page: Infratil (IFT), Contact Energy (CEN)

Ariadne and BGH terminate Webjet co-operation agreement

[8:48 am] Ariadne and BGH have terminated their May 2025 co-operation agreement, ending their associate status in relation to Webjet Group following BGH's takeover approach last year.

Co-operation agreement dated 12 May 2025 terminated as of 19 May 2026

Ariadne retains a relevant interest of 19.6m Webjet shares, or 5.00% (based on 392.5m shares on issue)

Both parties confirm they are now acting independently, with no agreement or understanding regarding Webjet's affairs

Company page: Webjet Group (WJL)

CVC CEO Mark Avery to step down after ~7 years

[8:47 am] CVC announced CEO Mark Avery will resign to pursue other opportunities, with internal successors set to take over by July 2026.

Mark Avery to step down as CEO/Managing Director after nearly 7 years in the role and over 15 years as an executive at CVC

Avery expected to remain in his executive role until July 2026, subject to transitional arrangements

Executive Chair Craig Treasure will assume the additional role of Managing Director

Andrew Ashwood, currently General Manager Development, will be appointed CEO

Company page: CVC Limited (CVC)

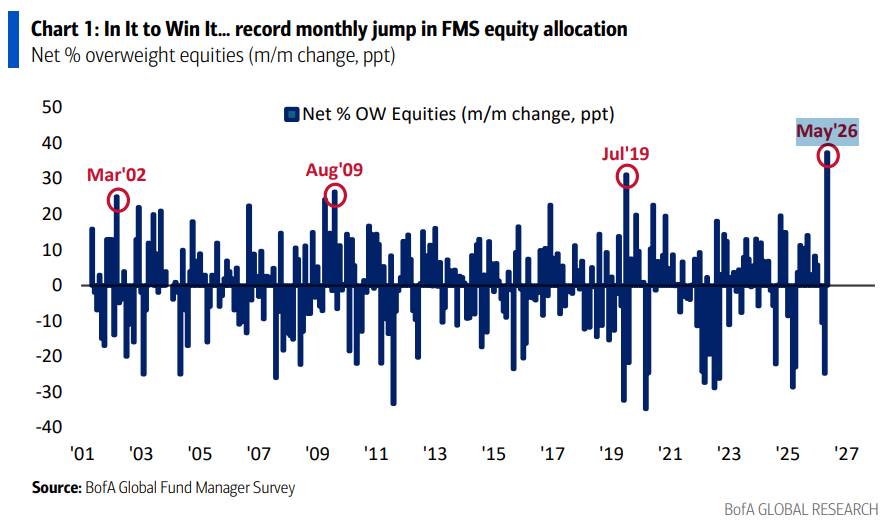

BofA fund manager survey signals euphoria with record jump in equity allocation

[8:44 am] BofA's May Global Fund Manager Survey showed a record rise in equity allocation and cash levels dropping into sell-signal territory, though the firm flagged early June as ripe for profit-taking.

Record 37pp jump in equity allocation to net 50% overweight, the highest since January 2022

Cash levels down 0.4pp to 3.9%, falling into sell-signal territory

Bull & Bear Indicator rose to 7.8, just below the 8.0 contrarian sell threshold (measures sentiment on a 0 to 10 scale)

Profit expectations jumped by the sixth-largest amount on record, with net 17% now expecting global profits to improve (vs net 14% expecting deterioration in April)

Half of respondents see the Fed cutting rates in the next 12 months, though net 23% expect higher short-term rates (highest since Oct-22) and net 66% expect higher global CPI

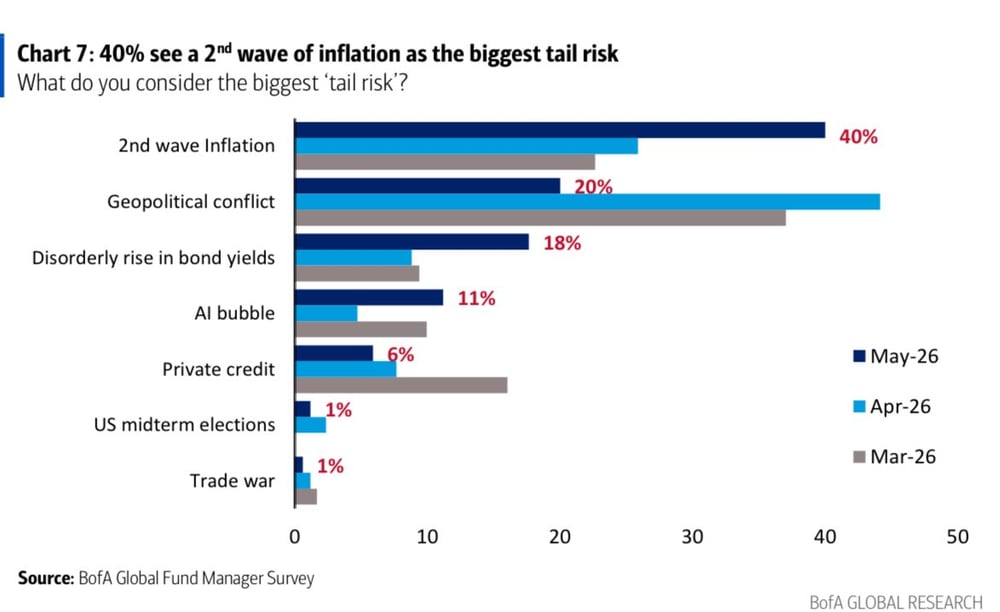

A second inflation wave seen as the biggest tail risk, US shadow banking flagged as the most likely source of a systemic credit event (down 15pp m/m to 42%)

Long global semiconductors now the most crowded trade, up 49pp m/m to 73%

RBA's Hunter warns inflation expectations risk becoming unanchored

[8:41 am] RBA Assistant Governor Sarah Hunter flagged heightened concern that successive inflation shocks could de-anchor expectations, warning a sharper slowdown may be needed if that occurs.

RBA "more worried now than we have been in the past" about inflation expectations becoming unanchored amid successive supply shocks

Cash rate now at 4.35% after three consecutive hikes this year, fully unwinding last year's easing

Money markets pricing at least one more hike this year, with around a 40% chance of a second

Fuel accounts for ~2.5% of the cost of producing and distributing other CPI goods/services, with travel, transport, groceries and new dwelling construction most exposed

Hunter warned pass-through will be "faster and more extensive" this time, with a 1990s-style sharper slowdown potentially needed if expectations drift higher

Source: Bloomberg

RBA meeting minutes

[8:40 am] The RBA publishes minutes of the Monetary Policy meetings two weeks after each meeting. Here are the key takeaways from the recent hike.

Board voted 8-1 to raise the cash rate by 25bp, citing upside inflation risks from the Middle East conflict and persistent capacity pressures.

Headline inflation hit 4.6% in March (fuel contributing 0.8ppt) and is forecast to peak at 4.8% in the June quarter

Underlying inflation now expected to stay above 3% until late 2027 and only return to 2.5% by mid-2028

Unemployment forecast to rise to 4.7% by mid-2028, with GDP growth troughing at 1.3% over the next 6-12 months

Global supply hit hard, oil down ~10% and LNG down ~20%, though Australia benefits from higher LNG and thermal coal export prices

Source: RBA

US Treasury sell-off deepens as inflation fears and Iran war rattle bond markets

[8:38 am] The 30-year Treasury yield hit 5.183%, its highest level since 2007, as investors price in stickier inflation, fiscal concerns and potential Fed rate hikes tied to the Iran conflict.

10-year yield up 8 bps to 4.667%, the highest since January 2025, having risen from below 4% before the Iran war began 80 days ago

2-year yield up 7 bps to 4.12%, signalling markets now expect the Fed to hold or potentially hike, a sharp reversal from rate-cut expectations at the start of the year

BofA survey shows 62% of global fund managers expect 30-year yields to reach 6% (would mark highest since late 1999), implying another ~85bp of upside

Global bond rout broadening, with UK 30-year gilts at the highest since 1998 and Japan's 30-year yield at a record, driven by sticky inflation, defence spending and fiscal deterioration

NATO weighs Hormuz intervention as Trump threatens fresh Iran strikes

[8:37 am] NATO is considering helping commercial vessels transit the blocked Strait of Hormuz by early July, while Trump warned of renewed strikes on Iran within days as the war continues to roil energy and bond markets.

Strait of Hormuz remains effectively closed since late February

NATO leaders meet in Ankara 7-8 July, with several members backing intervention though unanimous support not yet secured, France/UK already developing a separate navigation plan

Trump threatened renewed strikes within 2-3 days after calling off a Tuesday attack at the request of Saudi Arabia, Qatar and the UAE, with VP Vance flagging "option B" of restarting the military campaign

US Senate moved toward a vote to cease hostilities, with four Republicans crossing the floor, signalling growing political unease ahead of the midterms

Source: Bloomberg

US equities slide as Treasury yields back up, 30-year hits 2007 high

[8:31 am] S&P 500 and Nasdaq fell for a third straight session as a renewed bond sell-off, with the 30-year yield hitting its highest level since 2007, weighed on momentum and high-beta names.

S&P 500 and Nasdaq down for a third straight session, with stocks closing near the day's lows

US 2-year yield up 7 bps to 4.12% (highest since Feb-25), 10-year up 8 bps to 4.66% (highest since Jan-25) and 30-year up 5 bps to 5.13% (highest since Jul-07)

Sell-off driven by a mix of inflation, fiscal concerns, solid macro data, Warsh and overseas dynamics, with momentum unwind a key focus

Laggards included Mag 7, semis, software, machinery, airlines, payments, homebuilders, chemicals, nuclear and quantum computing

Middle East still in focus with US-Iran ceasefire holding but diplomatic solution looking increasingly complicated, keeping adverse physical disruption scenarios in play

Good morning!

[8:20 am] ASX 200 futures are down 39 pts (-0.45%).

The overnight session in a nutshell:

S&P 500 (-0.67%), Nasdaq (-0.84%) and Dow (-0.65%) extended losses to a third straight session as a brutal bond rout dragged stocks lower

US 30-year yield briefly topped 5.19%, its highest in 19 years, with 10-year hitting 4.66% on persistent inflation, higher oil prices and growing rate hike concerns

Fed now expected to hike 25 bps by year end (42% probability), while the likelihood of two 25 bp hikes has jumped to 16.4% (from 0% a month ago)

Commodities continue to tumble against a backdrop of rising bond yields, a firmer US dollar and higher oil prices