ASX 200 Live Today - Tuesday, 7th April

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, April 7. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up a little earlier than usual, at ~12:00 pm AEST. Let us know how we can make it even better.

ASX 200 up 1.44%, that's a wrap from us today

[12:10 pm] The ASX 200 is currently up 1.44% with 9 of 11 sectors in the green.

Information Technology is leading the charge, up 4.06%, followed by Materials up 2.15%, Financials up 1.63% and Discretionary up 1.38%.

Industrials and Staples are the only detractors, each down less than 0.1%.

That's all from us today. Make sure to come back tomorrow morning for more coverage. As always, thanks for tuning in.

Lithium stocks broadly higher

[12:07 pm] Lithium stocks are broadly higher, with Chinese lithium carbonate futures up 1.04% to 160,980 yuan a tonne.

Ticker | Company | % Chg | Price |

|---|---|---|---|

PAT | Patriot Resources | 7.89% | $0.04 |

INR | Ioneer | 7.69% | $0.14 |

DLI | Delta Lithium | 6.98% | $0.23 |

CXO | Core Lithium | 6.67% | $0.27 |

LKE | Lake Resources NL | 5.33% | $0.08 |

AGY | Argosy Minerals | 4.84% | $0.07 |

VUL | Vulcan Energy Resources | 4.42% | $3.43 |

NVX | Novonix | 3.92% | $0.27 |

MIN | Mineral Resources | 3.87% | $54.72 |

IGO | IGO | 3.33% | $8.22 |

PLS | PLS Group | 2.65% | $5.23 |

LTR | Liontown | 2.48% | $1.74 |

WR1 | Winsome Resources | 1.39% | $0.37 |

EUR | European Lithium | 0.89% | $0.23 |

ATC | Altech Batteries | 0.00% | $0.02 |

PMT | PMET Resources | 0.00% | $0.46 |

5EA | 5E Advanced Materials | 0.00% | $0.22 |

GL1 | Global Lithium Resources | -2.04% | $0.48 |

JBWere cuts ASX 200 year-end target to 8,800 amid stagflation warning

[12:02 pm] As we go through the broker notes that accumulated on our desks over Easter, one from JBWere stood out, cutting its ASX 200 year-end target to 8,800 and warning of a potential 20% downside in a hard landing scenario.

JBWere warns the oil price shock will drive EPS downgrades across the ASX over coming weeks, with UBS economists revising Australian headline CPI higher to a Q2 2026 peak of 5.5% year-on-year while cutting 2026 GDP growth to 1.9%, down from a pre-conflict forecast of 2.4%

Building Materials, Diversified Financials and Consumer Services are flagged as the fastest sectors to see earnings cuts, while Banks are characterised as "deniers" of the stagflationary impact before ultimately facing broad-based downgrades

In a hard landing stagflationary scenario where price-to-earnings multiples revert toward their 30-year average with no EPS growth, JBWere sees ASX 200 fair value at around 6,720, a ~20% decline from current levels, though the base case sees earnings fall before prices gradually recover by year-end

State Street sees gold "down but not out" with $4,750-5,500/oz year-end target

[11:59 am] State Street Investment Management's gold strategy team maintains gold's longer-term bull case despite the steepest monthly decline since the 2008 financial crisis in March.

Base case of US$4,750-5,500/oz by year-end (50% probability), with the bear case of US$4,000-4,750 at 20%, and oil normalising to US$80-85/bbl seen as capable of pushing gold back above US$5,000/oz

China onshore gold price premiums jumped to US$50/oz in March, the strongest since April 2025, with retail imports up 123% year-on-year in January-February and the People's Bank of China adding to reserves for 16 consecutive months to an all-time high of ~2,309 tonnes

Western gold ETFs saw US$12.4bn (~90 tonnes) of outflows in March, partly offset by US$1.1bn of Chinese gold fund inflows, with mainland China gold ETF inflows of US$8.1bn year-to-date, contrasting with US$2.0bn of outflows in the US over the same period

Health Care stocks up 1.56%, but still down 17% year-to-date

[11:43 am] The S&P/ASX 200 Health Care Index is up 1.56% to 27,957, though the sector remains one of the harder hit year-to-date, down 17.06% in 2026. Telix Pharmaceuticals (TLX) is the standout, surging 6.29% to $13.77 following this morning's quarterly update, while CSL is up 2.03% and Sonic Healthcare (SHL) is a rare laggard, down 1.70%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

TLX | Telix Pharmaceuticals | 6.29% | $13.77 |

4DX | 4DMedical | 4.70% | $5.91 |

PME | Pro Medicus | 3.48% | $122.97 |

FPH | Fisher & Paykel Healthcare | 2.87% | $31.15 |

CSL | CSL | 2.03% | $141.75 |

EBO | Ebos Group | 1.87% | $19.57 |

ANN | Ansell | 1.54% | $28.95 |

SIG | Sigma Healthcare | 1.13% | $2.69 |

COH | Cochlear | 1.08% | $174.23 |

RMD | Resmed | 0.92% | $32.51 |

RHC | Ramsay Health Care | 0.85% | $39.25 |

MSB | Mesoblast | -0.47% | $2.12 |

SHL | Sonic Healthcare | -1.70% | $19.64 |

Financial stocks outperform as sector rallies

[11:33 am] The S&P/ASX 200 Financials Index is up 2.27% to 9,654, outperforming the broader market, with Bank of Queensland (BOQ) the standout, surging 5.22% to $7.16 following this morning's Challenger capital partnership announcement, while the major banks are all up between 2.42% and 2.82%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

BOQ | Bank Of Queensland | 5.22% | $7.16 |

MQG | Macquarie Group | 2.83% | $211.41 |

NAB | National Australia Bank | 2.82% | $42.98 |

WBC | Westpac | 2.66% | $40.91 |

CBA | Commonwealth Bank | 2.65% | $177.39 |

ANZ | ANZ Group | 2.42% | $37.52 |

BEN | Bendigo & Adelaide Bank | 2.17% | $10.34 |

JDO | Judo Capital | 2.03% | $1.36 |

Gold stocks higher

[11:27 am] Gold stocks are broadly higher this morning after the gold price steadied around US$4,649/oz, down 0.59% overnight, as investors remain focused on President Trump's threats to target Iranian civilian infrastructure.

Ticker | Company | % Chg | Price |

|---|---|---|---|

AMI | Aurelia Metals | 4.62% | $0.27 |

RSG | Resolute Mining | 3.58% | $1.45 |

GMD | Genesis Minerals | 3.58% | $6.08 |

OBM | Ora Banda Mining | 3.57% | $1.16 |

RRL | Regis Resources | 3.27% | $6.94 |

WGX | Westgold Resources | 3.08% | $6.20 |

NST | Northern Star Resources | 2.97% | $22.56 |

MEK | Meeka Metals | 2.94% | $0.18 |

RMS | Ramelius Resources | 2.85% | $3.79 |

PRU | Perseus Mining | 2.75% | $5.43 |

NEM | Newmont Corporation | 2.69% | $163.61 |

EMR | Emerald Resources | 2.30% | $5.79 |

CYL | Catalyst Metals | 2.29% | $6.26 |

CMM | Capricorn Metals | 2.29% | $11.19 |

VAU | Vault Minerals | 2.06% | $4.21 |

ALK | Alkane Resources | 2.01% | $1.52 |

PNR | Pantoro Gold | 1.71% | $3.56 |

BGL | Bellevue Gold | 1.63% | $1.56 |

BC8 | Black Cat Syndicate | 1.17% | $1.04 |

SBM | St Barbara | 0.79% | $0.64 |

EVN | Evolution Mining | -0.38% | $12.97 |

BMR | Ballymore Resources | -5.56% | $0.17 |

GYG surges 20.8% as Australian trading surprises to the upside

[11:17 am] GYG shares are up 20.8% to $18.36 following this morning's Q1 update, with the market latching onto stronger-than-expected Australian trading and reaffirmed guidance calming execution risk concerns.

The delivery partnership is flagged as a meaningful near-term boost to Australian trading, a detail the market appears to have responded to positively

US momentum remained soft and continues to be the key debate, with cost pressures also still a consideration

Company page: Guzman y Gomez (GYG)

a2 Milk settles shareholder class action for $62m

[11:15 am] a2 Milk has reached an in-principle agreement to settle a long-running shareholder class action relating to its FY21 disclosures.

The $62m settlement is fully covered by insurance with no FY26 earnings impact and no admission of liability

Subject to finalisation of a deed of settlement and Supreme Court of Victoria approval

Company page: a2 Milk (ATM)

Former TWE boss pushes for overhaul amid share price slump

[11:11 am] Ex-Treasury Wine Estates COO Robert Foye has approached chairman John Mullen with a turnaround blueprint, claiming 50-100% equity upside is achievable with the right execution.

Foye attributes the 60%-plus two-year share price decline to strategic missteps, weak US and China performance and insufficient operating expertise at board level

His proposal calls for a US business review targeting doubled EBIT within five years, a return to a geographic operating model, restored Asia and China momentum and $30-50m in annual savings

TWE has declined to engage, pointing to its existing TWE Ascent transformation program as the path to sustainable profitable growth

Company page: Treasury Wine Estates (TWE)

AI chip demand powers Samsung to record profit

[11:07 am] According to Bloomberg, Samsung Electronics has reported a blowout quarterly result driven almost entirely by memory chips, offering the strongest signal yet that AI-driven hardware demand remains resilient despite geopolitical turbulence.

Operating profit of 57.2 trillion won ($37.9bn), up 755% year-on-year, well ahead of analyst estimates of 39.3 trillion won

Revenue of 133 trillion won, comfortably above the 116.8 trillion won expected, with memory estimated to account for ~90% of total operating profit

Global DRAM average selling prices surged 64% in the first quarter, with supply of both high-bandwidth memory and conventional DRAM described as very tight as cloud providers accelerate data centre buildouts

South Korea's semiconductor exports soared 151% in March to a record $32.8bn, a broad indicator that AI chip demand extends well beyond a single company

Hyperscaler capital expenditure is forecast to top $650bn in 2026, with Citigroup forecasting Samsung's full-year operating profit at the equivalent of $206bn, underpinned by strong AI inference demand keeping pricing power elevated

Copper stocks broadly higher

[10:59 am] Copper stocks are higher despite an overnight session that saw copper close down 1.25% at US$5.64/lb, recovering from a deeper intraday dip of 0.79%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

CSC | Capstone Copper | 4.77% | $11.53 |

AIS | Aeris Resources | 4.47% | $0.40 |

BHP | BHP Group | 3.34% | $52.94 |

HGO | Hillgrove Resources | 2.86% | $0.04 |

SFR | Sandfire Resources | 2.47% | $16.78 |

AR1 | Austral Resources Australia | 2.41% | $0.09 |

HCH | Hot Chili | 1.71% | $1.31 |

29M | 29Metals | 1.41% | $0.36 |

FFM | Firefly Metals | 1.00% | $1.71 |

Bank of Queensland strikes $3.7bn capital partnership with Challenger

[10:47 am] BOQ has announced a significant balance sheet restructure, selling $3.7bn of whole-of-loans to Challenger while entering a forward flow arrangement to free up capital.

The whole-of-loan sale reduces debt funding by ~$3.4bn and supports a ~$300m return to shareholders via an on-market buyback and fully franked special dividend, with CET1 target unchanged at 10.25-10.75%

The deal is EPS and ROE accretive, with a 15-25bps cash ROE uplift expected in FY26, while BOQ retains servicing fees for managing customer relationships recognised as non-interest income

A 12-month forward flow arrangement allows BOQ to originate loans on or off balance sheet, with the H1 FY26 accounts capturing an estimated $31m post-tax loss from transaction costs, goodwill allocation and swap impacts

Company page: Bank of Queensland (BOQ)

Tech stocks surge

[10:42 am] The S&P/ASX 200 Information Technology Index is up 6%, well ahead of the NASDAQ's modest 0.54% gain overnight. Yields edged higher, rising 0.51%, and the VIX rose 1.26% to 24.17.

Ticker | Company | % Chg | Price |

|---|---|---|---|

NXT | NEXTDC | 10.57% | $12.45 |

ELS | Elsight | 6.56% | $6.66 |

PME | Pro Medicus | 6.37% | $126.41 |

CDA | Codan | 4.89% | $33.59 |

MP1 | Megaport | 4.64% | $7.22 |

MAQ | Macquarie Technology Group | 4.62% | $63.47 |

TNE | Technology One | 4.53% | $28.13 |

SDR | SiteMinder | 4.53% | $2.89 |

DTL | Data#3 | 4.41% | $6.86 |

360 | Life360 | 4.39% | $19.52 |

DGT | DigiCo Infrastructure REIT | 4.31% | $1.82 |

WTC | Wisetech Global | 4.20% | $39.47 |

NXL | Nuix | 4.17% | $1.25 |

XRO | Xero | 3.65% | $76.76 |

AD8 | Audinate Group | 3.52% | $2.65 |

WBT | Weebit Nano | 3.10% | $3.66 |

DDR | Dicker Data | 2.76% | $8.55 |

CAT | Catapult Sports | 2.48% | $3.30 |

OCL | Objective Corporation | 2.26% | $11.77 |

PPS | Praemium | 1.50% | $0.68 |

IRE | Iress | 1.03% | $6.87 |

HSN | Hansen Technologies | 0.94% | $4.85 |

BVS | Bravura Solutions | 0.25% | $1.98 |

Top ASX 200 gainers and losers

[10:31 am] Here are today's top gainers and losers on the S&P/ASX 200.

Ticker | Company | % Chg | Price |

|---|---|---|---|

NXT | NEXTDC | 10.21% | $12.41 |

EOS | Electro Optic Systems | 8.22% | $9.74 |

ZIP | Zip Co | 7.62% | $1.70 |

TLX | Telix Pharmaceuticals | 7.18% | $13.88 |

HUB | HUB24 | 6.06% | $84.15 |

LYC | Lynas Rare Earths | 5.98% | $20.57 |

PME | Pro Medicus | 5.96% | $125.92 |

4DX | 4DMedical | 5.32% | $5.94 |

LNW | Light & Wonder | 5.27% | $126.33 |

PRN | Perenti | 5.19% | $2.03 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

MSB | Mesoblast | -2.82% | $2.07 |

AMC | Amcor | -1.28% | $57.78 |

RYM | Ryman Healthcare | -1.24% | $1.84 |

YAL | Yancoal Australia | -1.09% | $8.18 |

TCL | Transurban Group | -1.08% | $13.71 |

ALK | Alkane Resources | -1.01% | $1.48 |

ALD | Ampol | -0.87% | $32.98 |

SHL | Sonic Healthcare | -0.80% | $19.82 |

WHC | Whitehaven Coal | -0.72% | $9.02 |

BPT | Beach Energy | -0.61% | $1.30 |

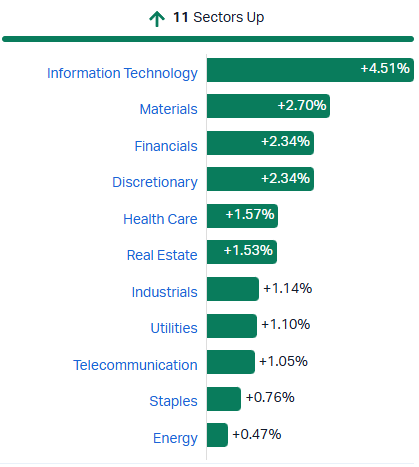

ASX 200 surges 2% after return from Easter break

[10:23 am] The ASX 200 is staging a strong rebound this morning, up 2.02% to 8,752, with all 11 sectors trading higher. The index has bounced sharply off yesterday's close of 8,579.

Information Technology leads the charge, up 4.51%, followed by Materials up 2.70% and Financials and Discretionary both up 2.34%. Health Care and Real Estate are also performing well, up 1.57% and 1.53% respectively. Even Energy, which has been under pressure recently, is participating with a gain of 0.47%. Defensives, including Utilities, Staples and Telcos, are all in the green but lag the broader market.

S&P/ASX 200 sectors (Source: Market Index)

Regal Partners' Aitken: long defence, short government bonds is the trade of the decade

[10:12 am] Regal Partners' Charlie Aitken argues the defence spending super cycle is the most compelling investment theme of the next decade, with global bond markets already pricing the shift.

Trump's FY27 budget proposes a record $1.5 trillion in defence spending, with the US reportedly deploying ~80% of its JASSM-ER stealth missile inventory against Iran, leaving just 425 of a pre-war stock of 2,300 available elsewhere, making stockpile rebuilding and critical defence minerals a structural multi-year demand story; rare earth (NdPr) prices are already up 34% year-to-date

Global bond yields rising during a war is highly unusual and signals higher-for-longer inflation expectations, making long-duration government bonds a structural short and hard assets, commodities and defence equities the preferred longs

On Australia, Aitken is bullish on defence, mining, energy, agriculture and tourism, but cautious on the East Coast consumer with the RBA most likely to hike in May, discretionary retail sales weakening and auction clearance rates falling

UBS upgrades KMD Brands to Buy as balance sheet risk clears

[10:06 am] KMD's heavily discounted equity raise removes the key balance sheet overhang, shifting the investment debate from survival to earnings delivery.

KMD completed a ~$65m equity raise at a ~47% discount to TERP alongside a new ~$205m debt facility, materially de-risking the balance sheet with UBS forecasting FY27 net debt/EBITDA of 0.3x vs the company's own target of less than 0.5x

1H26 underlying EBITDA came in 19% ahead of UBS estimates and above the $8-11m guidance range, driven by a Kathmandu sales inflection of +12% year-on-year and more than 200bps of gross margin recovery, though a material Rip Curl recovery is unlikely before FY27

UBS upgrades to Buy with a price target of NZ$0.14 (from NZ$0.28), with the cut reflecting ~1.09bn new shares issued, though a meaningful re-rate is seen as likely into FY27 as margin recovery translates into earnings momentum

Company page: KMD Brands (KMD)

Macquarie cuts A-REIT earnings and valuations as rate outlook deteriorates

[10:01 am] Macquarie has downgraded earnings and asset value assumptions across the Australian listed property sector, citing a material shift in the interest rate outlook and its flow-on effects to capital costs, residential volumes and funds management earnings.

Macquarie has softened weighted average capitalisation rate assumptions by 40bps across all sub-sectors, reflecting the expansion in 10-year real bond yields since end of February, with asset value downside varying materially by sector: sub-regional retail the most exposed at ~21%, industrial ~12%, office ~7% and major regional retail ~6.5%

FY27 earnings cuts are the most significant, with SGP (-9%), CNI (-9%), MGR (-7%) and CHC (-6%) the hardest hit, driven by lower residential volumes and prices, higher construction costs and slowing equity inflows into unlisted real estate, with channel checks suggesting each 50bps move in mortgage rates impacts volumes by ~10% with a 6-month lag

Preferred picks are GMG, MGR, GPT, QAL and ARF; GOZ is downgraded to Neutral while CNI is upgraded to Outperform after a 22.9% year-to-date sell-off, with the broader A-REIT sector down 16.7% calendar year-to-date

Trump escalates Iran ultimatum with Hormuz demand and infrastructure strike threats

[9:46 am] Trump has hardened his negotiating position with Iran, demanding free passage through the Strait of Hormuz as part of any deal and threatening to destroy Iranian civilian infrastructure by a Tuesday deadline, according to Bloomberg.

Trump added the reopening of the Strait of Hormuz as a deal prerequisite, a shift from recent administration messaging, with the strait's closure representing the largest-ever disruption to global oil markets

Oil prices rose sharply on renewed fears of prolonged supply disruption, with Brent crude ending above $109 a barrel and US crude settling near $112, with Iran warning it would retaliate against any infrastructure strikes by escalating attacks on Gulf energy assets

Iran rejected a ceasefire proposal relayed via Pakistan, instead demanding a permanent end to the war, sanctions relief and reconstruction support, while Pakistan, Egypt and Turkey are reportedly pushing for a 45-day ceasefire to avert further escalation

Telix Pharmaceuticals Q1 FY26 revenue update

[9:41 am] Telix delivered strong Q1 revenue growth driven by its PSMA imaging portfolio, while advancing a broad therapeutics pipeline across multiple disease areas.

Group revenue of US$230m, up 24% year-on-year and 11% quarter-on-quarter, with FY26 revenue guidance of US$950-970m reaffirmed

Precision Medicine revenue of US$186m, up 23% year-on-year and 16% quarter-on-quarter, reflecting growing uptake of both Illuccix and Gozellix in the PSMA imaging market

TMS third-party revenue of US$44m, up 29% year-on-year, flat quarter-on-quarter

Lead prostate cancer therapy candidate TLX591-Tx met safety and dosimetry objectives in Part 1 of the Phase 3 ProstACT Global study, with no new safety signals, paving the way for Part 2 enrolment expansion across multiple geographies

Pipeline progressing on multiple fronts: NDA resubmitted for brain imaging candidate TLX101-Px in the US, MAA filed in Europe, and NDA accepted in China for TLX591-Px, broadening the company's global regulatory footprint

David Gill appointed as Non-Executive Director from 11 May 2026, expected to succeed Mark Nelson as Chair, bringing deep US public company governance and biopharma experience to the board

Company page: Telix Pharmaceuticals (TLX)

NEXTDC launches $1.0bn hybrid securities offer backed by La Caisse

[9:26 am] NEXTDC (NXT) is raising $1.0bn in subordinated hybrid securities, with a cornerstone commitment from Canadian investment giant La Caisse, to fund its data centre growth pipeline.

$1.0bn hybrid securities offer fully backstopped by a binding commitment from La Caisse (formerly CDPQ), a CAD$517bn global investment group, with the offer now open to broader institutional investors

Hybrids carry a 7.50% fixed coupon for the first five years, stepping up to 9.20% thereafter, with a 100-year maturity and a five-year non-call period, coupons can be deferred at NEXTDC's election

Structured as deeply subordinated debt with no equity conversion features, expected to be tax deductible and sit outside senior debt covenants, preserving financial flexibility

Pro-forma liquidity reaches ~$5.2bn (cash and undrawn facilities) inclusive of this raise, providing significant runway to fund the contracted forward order book through to FY29

NEXTDC also intends to pursue a separate subordinated wholesale notes issue in the A$ debt market after this offer closes, further diversifying its funding base

Company page: NEXTDC (NXT)

Ramelius Resources Q3 FY26 production update

[9:22 am] Ramelius (RMS) delivered a soft Q3 production result but maintains full-year guidance confidence heading into a stronger June quarter.

Q3 gold production of 38,093oz, a relatively modest quarter with management flagging a stronger Q4 to keep the full year on track

FY26 production guidance of 185-205Koz reaffirmed

Cash and gold balance of $606.5m as at 31 March

Diesel costs are a watch point, with current prices of ~$2.10 per litre running well above the $0.95 per litre assumption baked into FY26 cost guidance, where diesel represents ~10% of total costs

Company page: Ramelius Resources (RMS)

Guzman y Gomez Q1 FY26 network sales update

[9:04 am] GYG delivered solid top-line growth in Q1 FY26, though same-store sales momentum continues to moderate.

Network sales up 19.5% to $345.9m, driven by continued restaurant expansion (278 vs. 241 a year ago)

Australian comp sales growth of 6.6%, a meaningful step down from 11.1% in the prior corresponding period, suggesting some normalisation after a strong run

US comp sales growth of 2.2%

FY26 guidance reaffirmed, with Australian segment underlying EBITDA margin expected to expand to 6.0-6.2% of network sales

On track to open 32 new restaurants in Australia in FY26, including 23 drive-thrus

Company page: Guzman y Gomez (GYG)

Good morning!

[8:44 am] ASX 200 futures are up 5 points (0.06%) as of 7:50 am AEDT.

In a nutshell:

US markets closed higher overnight, with the S&P 500 posting a fourth winning day, on hopes of a ceasefire in the Middle East

Asian markets had a solid Monday, with the Japanese, Indian and Korean markets rising 0.55-1.36%

Commodities were muted, but may see significant action depending on what exactly the US, Israel and Iran agree to (or not)