ASX 200 Live Today - Tuesday, 5th May

The S&P/ASX 200 is set for another weak start after a sharp spike in oil prices and bond yields. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, May 5. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 lower, RBA lifts inflation forecasts

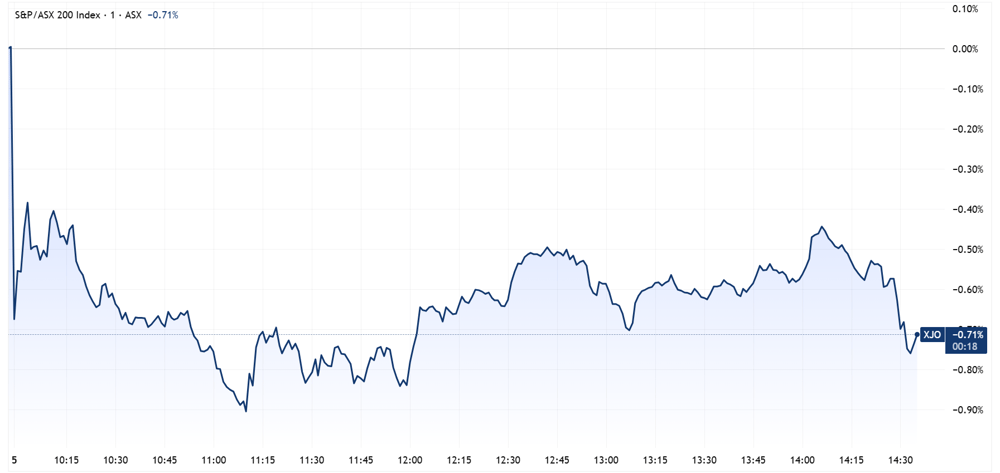

[2:45 pm] That's a wrap! Not much volatility at the index level in response to the widely expected RBA hike. The ASX 200 is currently down ~0.6% and on-track to close near a four-week low.

ASX 200 intraday chart (Source: TradingView)

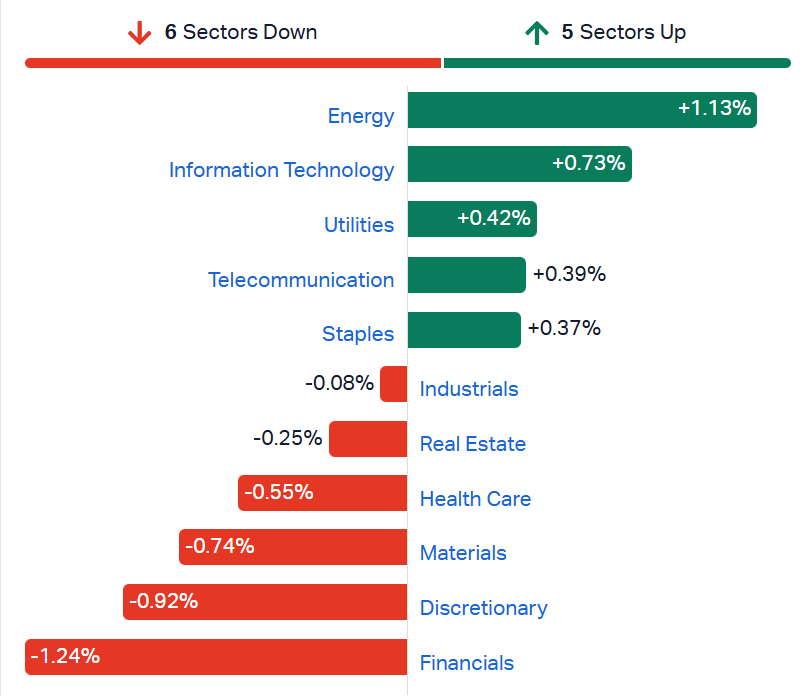

Banks have experienced some notable intraday weakness, with Westpac (-2.5%) back near session lows, and most other Big Four Banks down around 1%.

S&P/ASX 200 sectors (Source: TradingView)

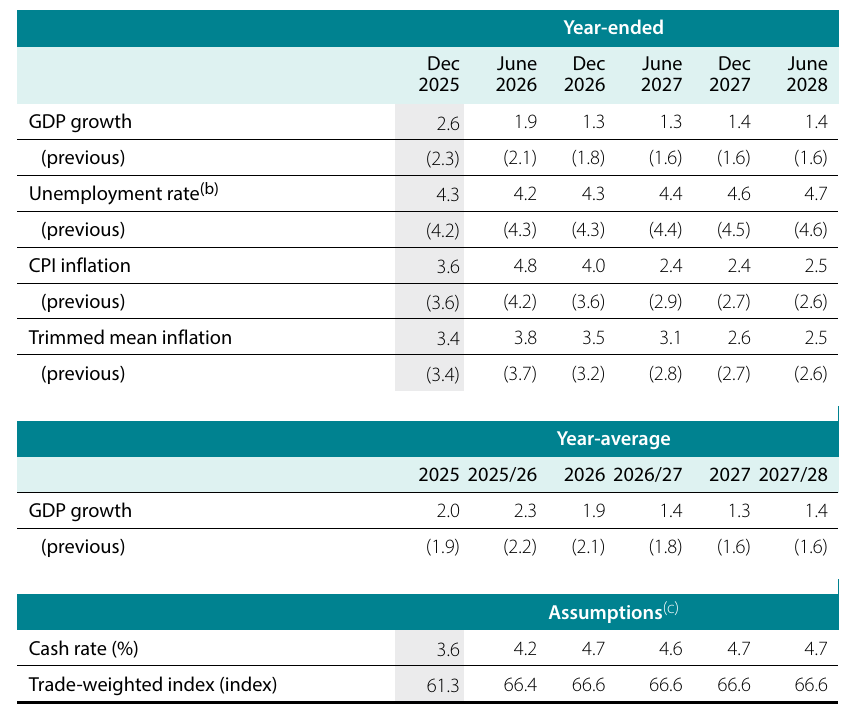

The RBA's Statement on Monetary Policy has trimmed GDP growth expectations, edged unemployment forecasts higher and expected trimmed mean inflation to get back below 3% by the December quarter 2028.

Source: RBA Statement on Monetary Policy

RBA hikes cash rate 25bps to 4.35% as Iran war fuels inflation

[2:30 pm] The RBA delivered a third consecutive 25bps hike, lifting the cash rate to 4.35%, citing capacity pressures and Middle East-related fuel price increases that are starting to flow through to broader prices.

Cash rate raised 25 bps to 4.35% on a majority 8-1 vote (one member voted to leave rates unchanged at 4.10%)

Underlying inflation picked up materially, with capacity pressures and Middle East fuel/commodity prices adding to inflation pressure

Early signs of firms looking to increase prices of goods and services in response to cost pressures

Updated baseline forecast (which assumes Middle East conflict is resolved soon and fuel prices decline) sees underlying inflation peaking higher than expected in February

Risks tilted to the upside, with plausible scenarios for higher inflation and lower activity if the conflict is prolonged or more severe

Board flagged it will be "attentive to data" and "do what it considers necessary" to achieve price stability and full employment, signalling continued willingness to act

Qantas more upbeat on fuel supply despite Iran war disruption

[2:17 pm] Bloomberg reports that Qantas CEO Vanessa Hudson struck a more positive tone at the Macquarie Conference, flagging improved fuel supply visibility, resilient travel demand and no plans to defer new plane deliveries.

Qantas now has fuel commitments stretching to mid-June, with suppliers diversifying sources and bringing in more from the Americas

Fuel suppliers committing to deliveries on a rolling six-week basis, in line with pre-conflict patterns

Appetite for domestic and international travel is holding up even with higher fares; Hudson noted "strong demand right across our network"

No plans to defer new plane deliveries to preserve cash, Hudson said "we don't believe what is happening is permanent"

April flagged 2H26 fuel bill of $3.1bn-$3.3bn (up from an earlier $2.5bn estimate) on the back of the Middle East conflict

Source: Bloomberg

Gentrack tumbles 34% on FY26 guidance downgrade

[1:54 pm] Gentrack cut its FY26 revenue and EBITDA guidance this morning, while flagging an intent to launch an on-market share buyback of up to $20 million. The stock opened 23.8% lower, currently down 34% to a near three-year low.

FY26 revenue guidance lowered to $229m-$238m (vs. previous higher guidance) and up just 1.4% vs. FY25

Recurring revenues expected to grow more than 10% to ~$174m in FY26

FY26 EBITDA guided to $13.5m-$20m (excluding acquisition costs), down 39.7% year-on-year

Medium-term revenue CAGR target of more than 15% reaffirmed

EBITDA margin target of 15-20% maintained (after expensing all development costs)

Strategic decision to prioritise growth via continued investment in international expansion and product development

Board signals intent to launch an on-market share buyback of up to $20m (capped at 5% of shares on issue) over up to 12 months following H1 results

Company page: Gentrack Group (GTK)

Westpac 1H26 earnings call highlights

[12:40 pm] A fairly mixed 1H26 result from Westpac, with solid lending and deposit growth, offset by a sharp decline in margins. The stock was already down ~9% heading into the result (13-Apr to 4-May). A few key takeaways from the earnings call include:

NIM facing headwinds in H2 from higher-rate term deposit growth and competitive deposit/lending pricing

Business credit growth to slow to 5-6% annualised in H2 (skewed to large corporates) as SMEs feel macro uncertainty

Deposit growth to remain strong in H2 driven by higher-yielding products

FY26 investment spend ~$2bn (UNITE range narrowed), structural productivity savings of at least $550m

Mortgage arrears and credit quality metrics expected to improve through the rest of FY26

Management assumes three RBA rate rises in 2H26, potentially taking the cash rate to 4.85%, with the Australian economy slowdown more pronounced in H2 and impacting lending demand

Tech stocks mostly higher

[12:34 pm] A relatively positive day for tech stocks, with the ASX 200 Tech Index up 1.15% to the highest since 9 March.

Wisetech opened sharply higher after the company reaffirmed its FY26 guidance at the Macquarie Conference (contrary to some analyst expectations of potential downgrades).

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

WTC | Wisetech Global | 5.9% | $46.06 | -51.8% |

XRO | Xero | 3.5% | $85.82 | -49.8% |

DGT | Digico Infrastructure Reit | 1.3% | $2.39 | -19.5% |

OCL | Objective Corporation | 1.2% | $11.53 | -29.4% |

BVS | Bravura Solutions | 0.9% | $2.25 | 4.2% |

MP1 | Megaport | 0.9% | $9.09 | -22.0% |

TNE | Technology One | 0.7% | $28.24 | -9.9% |

NXL | Nuix | 0.7% | $1.51 | -41.4% |

DTL | Data#3 | 0.4% | $8.15 | 7.4% |

360 | Life360 | 0.2% | $21.27 | -8.5% |

NXT | NextDC | 0.0% | $14.09 | 13.5% |

DDR | Dicker Data | 0.0% | $9.18 | 7.7% |

PPS | Praemium | 0.0% | $0.69 | -10.5% |

MAQ | Macquarie Technology Group | -0.1% | $69.63 | 12.6% |

IRE | Iress | -0.6% | $6.69 | -17.9% |

ELS | Elsight | -0.6% | $6.92 | 1349.7% |

PME | Pro Medicus | -0.7% | $137.76 | -42.6% |

HSN | Hansen Technologies | -1.0% | $4.90 | -7.2% |

CAT | Catapult Sports | -1.6% | $3.32 | -19.5% |

SDR | Siteminder | -1.6% | $3.00 | -28.6% |

AD8 | Audinate Group | -1.6% | $2.40 | -61.2% |

WBT | Weebit Nano | -3.3% | $4.30 | 132.2% |

CDA | Codan | -9.0% | $39.97 | 148.9% |

Banks broadly lower

[11:13 am] S&P/ASX 200 Financials Index down 1.0% today, reflecting broad softness among major banks. Westpac reported its 1H26 result this morning, with earnings largely in-line with market expectations, underpinned by strong volume growth but offset by a sharp decline in margins. The stock dipped as much as 2.2% in early trade, now down just 0.5%.

The Financials Index is now down 13 of the last 16 sessions, and trading right on its 200-day moving average today.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

BEN | Bendigo & Adelaide Bank | -1.1% | $10.57 | -7.7% |

ANZ | ANZ Group | -0.9% | $35.95 | 17.9% |

CBA | Commonwealth Bank | -0.9% | $170.73 | 0.9% |

BOQ | Bank Of Queensland | -0.8% | $6.37 | -15.0% |

MQG | Macquarie Group | -0.7% | $236.24 | 19.2% |

WBC | Westpac | -0.5% | $38.29 | 16.9% |

NAB | National Australia Bank | -0.4% | $39.05 | 6.7% |

Accent Group target prices almost halved

[11:10 am] Accent Group delivered a material 2H26 EBIT guidance downgrade driven by a sharp April trading deceleration and 80 bps YTD gross margin compression, compounded by the announcement of an ASIC investigation into the CEO, a non-executive director and a senior employee.

RBC Capital Markets retained Sector Perform, lowered target from $1.30 to $0.80. April marked a clear inflection point with margin pressure extending beyond fuel costs, while the ASIC investigation adds management uncertainty ahead of the critical strategy day.

Jarden retained Neutral, lowered target from $1.20 to $0.70. The sharp April LFL deceleration and gross margin compression point to structural competition issues, with cost-out credibility key to offsetting operating deleverage.

Morgan Stanley retained Underweight, lowered target from $1.04 to $0.55. The downgrade reflects both LFL weakness and margin sustainability concerns, with limited valuation protection despite the share price decline and cost program detail required before any upgrade.

Analysts split on NAB

[11:08 am] NAB's 1H26 result met headline expectations but masked a revenue miss from lower deposit balances and rising asset quality concerns, with management pre-announcing one-off software amortisation and increased provisions.

Analyst views were split between those upgrading on compressed valuations and those staying cautious on credit quality, capital position and cost inflation.

E&P upgraded to Neutral from Negative, target unchanged at $38.00. Customer experience improvements and underlying cost progress support franchise value, though significant ongoing technology investment is required to maintain competitive positioning.

Morgans upgraded to Trim from Sell, raised target from $34.56 to $36.10. Revenue missed on productivity timing delays and asset quality deterioration is a clear near-term risk, but business lending differentiation underpins the longer-term valuation case.

UBS retained Buy, lowered target from $50.50 to $48.50. Margins beat consensus on strong lending growth and ROE trajectory supports the through-cycle case, with the share price reaction viewed as disproportionate to management's messaging tone.

Analysts cut Endeavour target price

[11:06 am] Endeavour Group's Q3 sales update revealed mixed retail growth with deteriorating hotel momentum, compounded by a sizeable $400 million inventory build and incremental fuel/freight cost pressures that drove broad sell-side earnings downgrades.

UBS retained Neutral, lowered target from $3.60 to $3.45. Structural and cyclical headwinds make a retail recovery unlikely, with hotels now softening and promotional intensity expected to escalate rather than ease.

RBC Capital Markets retained Sector Perform, lowered target from $4.00 to $3.50. Market share gains are masking broad-based trading deterioration, while rising leverage raises near-term dividend sustainability questions.

ASX 200 nears one-month low

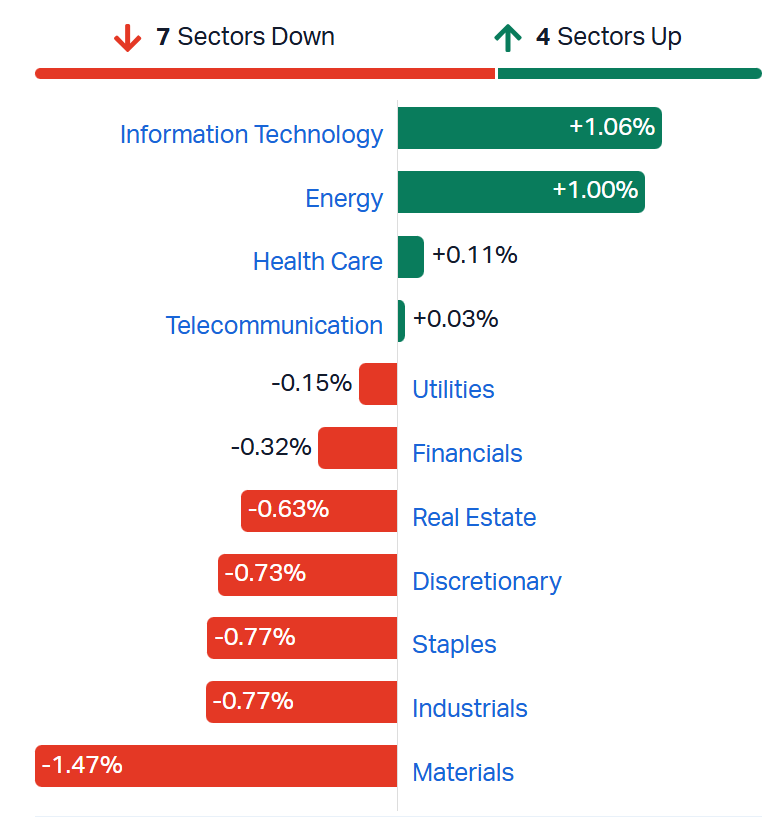

[10:31 am] Another heavy day for equities, with the ASX 200 down 0.64%, which undercuts the recent low (30-Apr) and marks a second straight day below the key 200-day moving average. The Materials sector leads today's declines following a relatively weak overnight session for commodities, where copper fell 1.7% to US$5.86/lb and gold tumbled 2.0% to US$4,521/oz. Banks are also under pressure, with all the majors down 0.3-0.5%, following a mixed 1H26 report from Westpac. Technology stocks have managed to buck the trend after a strong move for Nasdaq-listed software stocks, while Energy stocks edge higher off the back of a ~4% spike in oil prices.

ASX 200 sectors (Source: Market Index)

Top ASX 200 gainers

[10:14 am] Ventia is rallying off the back of a contract win and Vault Minerals higher off the back its merger with Regis Resources. Overall, a very catalyst driven day, with Flight Centre, Lottery Corp and Sigma Healthcare all announcing updates this morning.

Ticker | Company | % Chg | Price |

|---|---|---|---|

VNT | Ventia Services Group | 5.39% | $5.87 |

VAU | Vault Minerals | 5.22% | $4.74 |

WTC | Wisetech Global | 4.25% | $45.33 |

EOS | Electro Optic Systems | 3.94% | $10.28 |

FLT | Flight Centre Travel Group | 3.64% | $10.53 |

TLC | Lottery Corporation | 3.57% | $5.66 |

SIG | Sigma Healthcare | 3.53% | $2.93 |

PNI | Pinnacle Investment Management | 3.11% | $15.92 |

SGH | SGH | 2.44% | $40.71 |

XRO | Xero | 2.29% | $84.82 |

Top ASX 200 losers

[10:14 am] Codan tumbles on a block-trade, Endeavour continues to fall after yesterday's downbeat Q3 update, while building materials, copper and rare earth stocks trade broadly lower.

Ticker | Company | % Chg | Price |

|---|---|---|---|

CDA | Codan | -8.49% | $40.19 |

MFG | Magellan Financial Group | -6.48% | $9.67 |

SGM | Sims | -5.97% | $19.86 |

ARU | Arafura Rare Earths | -4.48% | $0.32 |

JHX | James Hardie | -3.94% | $27.57 |

RRL | Regis Resources | -3.63% | $6.91 |

CSC | Capstone Copper Corp | -3.62% | $11.19 |

VUL | Vulcan Energy Resources | -3.43% | $3.66 |

EDV | Endeavour Group | -2.74% | $3.20 |

ILU | Iluka Resources | -2.72% | $8.06 |

Vicinity Centres reaffirms FY26 guidance at top end of range

[9:43 am] Vicinity Centres delivered a strong 3Q FY26 with resilient retailer confidence and favourable industry fundamentals, reaffirming guidance at the top end of the FFO and AFFO ranges.

FY26 FFO and AFFO expected at the top end of guidance ranges of 15.0-15.2 cps and 12.8-13.0 cps respectively

Occupancy at 99.6%, leasing spreads at +5.1% and holdovers low at 3.1%

Total portfolio retail sales up 3.4% in 3Q FY26, supported by mini major growth of 3.7%

Occupancy Cost Ratio sustainable at 14.3% with retailer debt low, though management mindful of rising retailer costs and heightened macro/geopolitical uncertainty

Raised $654m of debt via a $500m 10-year AMTN

89% of total drawn debt hedged in FY26 and 85% in FY27

Chatswood Chase luxury precinct opened 30 April with strong visitation

Galleria redevelopment progressing well, on track for pre-Christmas opening and over 75% leased

Divestments of Whitsunday Plaza, Armidale Central and Gympie Central settled on 27 February 2026

Company page: Vicinity Centres (VCX)

Ventia awarded Victorian Road Maintenance Contracts

[9:40 am] Ventia Services has been awarded two Victorian Road Maintenance Contracts by the Victorian Department of Transport and Planning, valued at ~$340 million over a four-year base term.

Combined value of ~$340m over a four-year base term across the Grampians and Eastern Metropolitan regions

Contract terms include options to extend two years (+2) for Grampians and four years (2+2) for Eastern Metropolitan

Scope includes road network maintenance, inspections, hazard and defect rectification, emergency response and minor capital works across rural and metropolitan arterial roads

Company page: Ventia Services Group (VNT)

Regis Resources to merge with Vault Minerals

[9:36 am] Regis Resources and Vault Minerals have agreed to a merger-of-equals via scheme of arrangement, creating Australia's next major gold producer with annual production of over 700koz across five WA assets and significant scale.

Vault shareholders to receive 0.6947 new Regis shares per Vault share, leaving Regis holders with ~51% and Vault holders with ~49% of the combined company

Unanimously recommended by both boards, subject to no superior proposal emerging

Combined company anticipated to produce over 700koz gold per annum from five high-quality WA assets, positioning it as the 3rd largest primary ASX-listed gold producer

Pro forma market capitalisation of ~$10.7bn delivering increased liquidity and a step-change in global market relevance

Combined annualised free cash flow of $1.7bn, with $1.9bn in pro forma cash and bullion, no drawn debt and $300m in available debt facilities

Scope to unlock cost efficiencies and realise over $500m of corporate tax benefits, with potential to lower cost of capital

Combined milling capacity of ~22.3Mtpa across 9 mills (rising to ~24.3Mtpa following the King of the Hills mill expansion in FY27 Q2)

Implementation expected in August/September 2026

Company pages: Regis Resources (RRL), Vault Minerals (VAU)

The Lottery Corp leverage to hit upper end of target range

[9:30 am] The Lottery Corp will pay the Victorian Government in two instalments for its Public Lottery Licence renewal, with $250 million paid on 3-Jul-26 and $895 million paid on 1-Oct-26.

"To provide funding certainty to the State, the Company has obtained a commitment for a new $1,000 million bank loan facility, combined with approximately $145 million under existing undrawn debt facilities," the company said in a statement.

This will increase TLC's leverage towards the upper end of its 3-4x target leverage range.

The Lottery Corp secures 40-year Victorian licence extension

[9:28 am] The Lottery Corp has secured a 40-year extension to its Victorian Public Lottery Licence in exchange for an upfront $1.15 billion premium, materially improving the risk profile of the Lotteries business and providing long-term earnings certainty.

Public Lottery Licence extended to 30 June 2068

Upfront premium of $1.15bn payable to the State of Victoria

Premium reflects valuation and return parameters consistent with prior long-term lottery licence acquisitions, implying a high single-digit EBITDA multiple

Significantly improves the risk profile of the Lotteries business and provides long-term earnings certainty, the next major lottery licence renewal not until 2050 (NSW)

Not expected to impact any FY26 dividends

FY27 dividend policy revised to 80-100% of NPATA ex-items (from 80-100% of NPAT ex-items)

Company page: The Lottery Corporation (TLC)

NextDC secures $1.8bn in new senior debt facility commitments

[9:26 am] NextDC has received credit-approved commitment letters for $1.8 billion of new senior debt facilities, lifting total available facilities to $8.2 billion and supporting capacity expansion following its record contracted utilisation announcement.

Margins on the new facilities are broadly consistent with existing senior debt facilities of similar tenor

Proceeds will primarily support capex tied to recent customer contract wins, ongoing data centre developments and general corporate purposes

Builds on the record increase in contracted utilisation announced 20 April 2026 and recent capital raising initiatives

Company page: NEXTDC (NXT)

Flight Centre Q3 pretax income up 18.5%, FY26 guidance reaffirmed

[9:23 am] Flight Centre delivered strong Q3 pretax income growth led by Corporate, while reaffirming FY26 guidance with caveats around Middle East-related disruption to short-term leisure trading.

Q3 pretax income up 18.5% to $102.6m

Leisure up 7.6% y/y and Corporate up 29.4% y/y

Q3 total transaction volumes up 6.8% of $7bn

FY26 pretax income guidance reaffirmed at $315m-$350m vs. ests $326.2m (in line at midpoint)

Leisure heavily affected in April with an estimated profit impact of ~$10m for the month due to Middle East hostilities

Global Corporate not significantly impacted to date, though flow-on effects from higher airfares and macro factors more likely to impact early FY27

Potential Q4 FX headwinds on overseas profit translation flagged given Australian dollar strength

Company page: Flight Centre (FLT)

Nine Entertainment Q4 advertising softness offsets resilient operational performance

[9:15 am] Nine flagged a softer Q4 for Total Television advertising amid Middle East uncertainty and election cycling, but reaffirmed momentum in Stan, Publishing digital subscriptions and QMS as the Group repositions toward a digital-first portfolio.

Total Television Q3 revenues grew in the low single digits year-on-year, cycling a strong prior corresponding period

Q4 has started softer reflecting underlying ad conditions and cycling of the Federal election that buoyed April 2025

YTD CY26 Total TV audiences up 8%

Stan 1H26 momentum to continue with further strong EBITDA growth projected in H2

Publishing Q3 digital subscription revenue up 15% with momentum into Q4, though higher fuel prices will impact distribution costs near term

Company page: Nine Entertainment (NEC)

Westpac 1H26: Solid lending growth offsets margin and impairment headwinds

[9:14 am] Quite a bit to unpack here, as cash earnings and net interest margins came in slightly below market expectations, reflecting higher impairments and elevated provisions for energy-intensive sectors.

Cash net profit (ex-items) up 1% year-on-year to $3.48bn vs. ests $3.52bn (1% miss)

Statutory NPAT up 3% to $3.41bn

Net interest income (cash basis) of $9.76bn vs. ests $9.90bn (1% miss)

NIM down 3 bps to 1.89% vs. ests 1.90%

Total impairment charges of $443m vs. ests $416m (7% above)

Interim DPS of 77 cents, payout ratio of 77.1% on statutory NPAT

Balance sheet and capital

CET1 of 12.42% vs. ests 12.46%, $2.7bn above target ratio of 11.25% post-dividend

Lending up 7% year-on-year to $890.3bn

Customer deposits up 7% year-on-year to $745.2bn

Australian mortgages (ex-RAMS) grew at 1.2x system, with proprietary channel mix increasing

Australian business lending up 16% year-on-year, diversified across agriculture, health and professional services

Credit quality

Stressed exposures to TCE down 12bps on Sep-25 to 1.16%

Credit impairment provisions increased to $5.2bn, with a new portfolio overlay added for energy intensive sectors

CEO Anthony Miller flagged Middle East war pressures continuing through the year, with energy supply chain disruption flowing through to businesses and households

Company page: Westpac (WBC)

Codan founding family pursues ~$200m block trade

[9:04 am] Billionaire philanthropist Pamela Wall, controlling shareholder of Codan via her late husband's stake, is selling down ~$200 million worth of shares, according to the AFR.

Block trade size of ~$200m on behalf of the Wall family, who own around 18% of Codan

Shares offered at ~$39 apiece, an 11% discount to the last close of $43.92

The stake was originally owned by co-founder Ian Wall (who established the company in 1959 with Jim Bettison and Alastair Wood) and is now controlled by his 93-year-old widow Pamela, who will retain ~$1.2bn in Codan shares post sell-down

Source: AFR

NAB 1H26 earnings call highlights

[9:02 am] A few key takeaways from the NAB 1H26 earnings call yesterday.

Credit impairment charges and impaired asset ratio could remain elevated near-term: Recent provisions stemmed from a few international exposures rather than broad-based deterioration, with RWAs projected to rise ~$3bn over the next 12-18 months

NIM facing minor headwinds from deposit mix shifts and competition, with replicating portfolio expected to add ~5bps in H2. Management assumes one more cash rate hike in FY26 with minor NIM impact

Business credit growth to moderate in H2 from the elevated 10% annualised rate in H1, though pipeline remains robust

FY26 cost growth to be below 4.6% year-on-year with productivity savings to exceed $450m

Capital overlays on risk models seen as temporary, with no changes planned to DRP neutralisation policy or payout ratio targets

Company page: National Australia Bank (NAB)

Sigma Healthcare flags strong Chemist Warehouse momentum, enters UK market

[9:00 am] Sigma reported double-digit LFL sales growth across Australian and international Chemist Warehouse stores, while announcing UK market entry via JV and a long-term NZ distribution centre lease.

FY26-to-date (1-Jul to 30-Apr) Chemist Warehouse-branded like-for-like sales: Australian store network up 14.4%, international store network up 11.8%

Signed MoU with UK's GreenLight Healthcare (22 stores in and around London) to bring Chemist Warehouse to the UK

Under the JV, Sigma will acquire a 75% interest in a number of stores (25% retained by GreenLight) and licence the brand, IP and retail support

Signed a 15-year lease (with extension options) on a 23,000 sqm temperature-controlled distribution centre in Wiri, 25km south of Auckland,

Targeting more than 100 CW stores in New Zealand over the long term

I don't have any (recent) broker data handy. The outlook commentary in Sigma's 1H26 result noted first seven weeks of 2H26 sales of 16.6% for Australian CW stores and like-for-like sales up 14.4%.

Chemist Warehouse is expected to deliver slower like-for-like sales as comparables become increasingly tougher to cycle (reflecting meaningful contributions fro GLP1 sales last year).

Company page: Sigma Healthcare (SIG)

PEXA Group Q3: Reaffirms FY26 guidance with NPAT at top end

[8:54 am] PEXA Group reaffirmed FY26 guidance and flagged Group Core NPAT at the top end of the range, supported by Australian market strength and disciplined cost management.

Australian transaction volumes up 7.3% year-on-year to ~935k with national market penetration steady at 90%

International remortgage activity strong with Optima instructions up 58% (completions up 10%) and Smoove instructions up 14% (completions up 13%)

FY26 revenue guidance reaffirmed at $395m-$415m vs. ests $407.9m (in line at midpoint)

FY26 Group core NPAT guided to the top end of the $15m-$25m range

FY26 EBITDA margin guidance of 34-37% maintained, with capex of $50m-$55m and International operating cash outflow of $59m-$63m

Company page: PEXA Group (PXA)

Insider transaction: Regal Partners Chair-elect Peter

[8:51 am] Incoming Regal Partners Chair Peter Yates has disclosed the purchase of 84,000 shares vs. prior shareholder of nil.

Yates was appointed as Independent Non-Executive Director and Chair-Elect on 13 April 2026, with the intention of assuming the Chair role at the conclusion of the AGM on 28 May 2026

Replaces current Chair Michael Cole AM, who will retire from the Board following the AGM after serving in the role since June 2022

Company page: Regal Partners (RPL)

ASX heavyweights skip Macquarie Conference as "confession season" looms

[8:47 am] A string of ASX-listed companies including CSL, Reliance Worldwide, Temple & Webster and Lendlease are believed to have pulled out of this week's Macquarie Australia Conference, notes the AFR.

The three-day conference is widely seen as the unofficial start of "confession season", where companies often use presentations to reveal whether they are likely to meet earnings guidance provided in February

February guidance was largely set just before the Iran war began, raising the risk that rosy profit outlooks will be cut as the conflict's impact flows through

The Macquarie Conference runs from Tuesday, 5 May to Thursday, 7 May.

Source: AFR

RBA poised for third straight hike as Middle East war fuels inflation

[8:45 am] The RBA is set to entrench its hawkish outlier status with a third consecutive rate rise on Tuesday, even as global peers hold steady to assess fallout from the Iran conflict.

Economists overwhelmingly expect the RBA to hike the cash rate to 4.35%, fully unwinding last year's cuts

The likelihood of a hike sits at ~80%

Q1 inflation held well above the 2-3% target band, with pass-through now spreading to building products, takeaway food, freight, airfares, plastics, fertilisers, detergents and paints

The March decision was a narrow 5-4 split vote, and CBA's Belinda Allen flags the May call feels "more precarious"

RBA will release updated quarterly forecasts (the first to incorporate the oil shock) and Governor Bullock's press conference at 3:30 pm Sydney time

Decision precedes Treasurer Chalmers' budget next week, which must balance productivity support, household relief, intergenerational equity and structural deficits

Fed dissenters warn of inflation risks from Iran war

[8:43 am] Minneapolis Fed's Kashkari and Chicago Fed's Goolsbee both pushed back on the case for near-term rate cuts, with Kashkari signalling hikes may be needed if the war is prolonged.

Kashkari said he doesn't feel comfortable signalling a rate cut and "we might have to go the other direction"

Even a best-case strait reopening could mean six months for global supply chains to normalise, per a Minnesota CEO Kashkari spoke with

The Fed held the policy rate at 3.5%-3.75% on an 8-4 vote, the most divided since 1992 as Kashkari joined Cleveland and Dallas dissenting against forward guidance suggesting the next move is a cut, while Governor Stephen Miran dissented in favour of a cut

March headline PCE up 3.5% year-on-year vs. the Fed's 2% target, with Goolsbee calling the data "bad news" and noted inflation rising even in services largely insulated from tariffs and oil

Kevin Warsh on track to succeed Powell as Fed Chair when his term ends later this month

UAE under attack as Iran-US ceasefire fractures

[8:42 am] A drone attack on the UAE's Fujairah Oil Industry Zone and a series of skirmishes in the Strait of Hormuz have put the nearly month-long US-Iran ceasefire on shaky footing.

UAE air defences engaged 19 Iranian missiles and drones, a drone attack hit the Fujairah Oil Industry Zone, injuring three Indian nationals and triggering a major fire

Fujairah is critical to UAE oil exports during the war as it sits at the end of the Abu Dhabi Crude Oil Pipeline, allowing the UAE to bypass the Strait of Hormuz

US military "blew up" six small Iranian boats (Trump later said seven) in the strait after Iran launched cruise missiles, drones and small boats at US Navy and commercial ships

Trump declined to confirm whether the ceasefire (in place since 8 April) remains in effect, warning Iranian forces would be "blown off the face of the Earth" if they targeted US ships

Trump's "Project Freedom" plan to guide merchant ships out of the Strait dismissed by Iran's foreign minister as "Project Deadlock"

Maersk confirmed one of its ships traversed the strait under US military protection

Bitcoin tops US$80,000 for first time since January

[8:39 am] Bitcoin pushed above the key US$80,000 psychological barrier as crypto markets shrugged off Middle East tensions and grew optimistic on US stablecoin legislation progress.

Bitcoin climbed as much as ~2% to US$80,768, the highest level since 31 January

Bounced ~20% since the start of the Iran conflict, though down 8.4% YTD

Optimism that a US deal may be reached on a key stablecoin yield provision is potentially clearing a path for sweeping crypto legislation in the Senate

Funding rates for Bitcoin perpetual futures remain persistently negative (a contrarian bullish signal)

US Bitcoin ETFs saw $630m of net inflows on Friday per Bloomberg

US stocks slip as US-Iran escalation offsets earnings optimism

[8:38 am] US equities pulled back from record highs as escalation in the Iran war drove oil prices sharply higher and pushed long bond yields back into Wall Street's danger zone.

Reports of two Iranian strikes on a US patrol boat and a US warship being turned back in the Strait of Hormuz (denied by the US)

UAE said an ADNOC oil carrier and the Fujairah petroleum export complex had been struck by Iran

Iran warned it would take action against US ships in response to Trump's "Project Freedom" plan to help trapped ships exit the Gulf waterway, viewing any US "interference" as a ceasefire violation

US 30-year Treasury yield jumped 6 bps to 5.03%, the biggest one-day move since 20 March and highest since July 2025, the 5% zone has historically tightened financial conditions and pressured equities

FedEx and UPS both fell more than 8% after Amazon said it would open its product distribution network to companies outside its own platform

Good morning!

[8:20 am] ASX 200 futures are down 70 pts (-0.80%) as of 8:30 am AEST.

The overnight session in a nutshell:

S&P 500 (-0.41%), Dow (-1.13%) and Nasdaq (-0.19%) broadly lower, with all sectors red except Energy

Brent jumped 4.4% to US$114 a barrel amid Iran military escalation, which hit several ships in the Strait of Hormuz and a key UAE oil port

Higher oil prices and inflation concerns driving bond yields higher, US 10-year up 6 bps to 4.43%, breaking out to the highest since 18-Jul-25