ASX 200 Live Today - Tuesday, 2nd June

The S&P/ASX 200 is set to slip despite the S&P 500, Dow and Nasdaq closing at all-time highs overnight. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, June 2. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

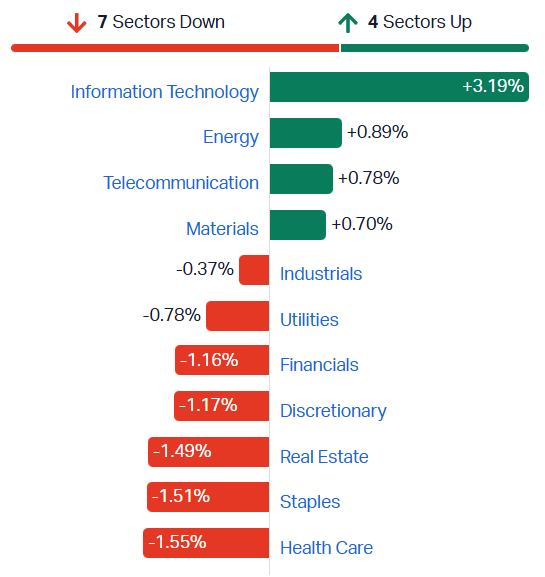

ASX 200 off lows but healthcare, staples and banks weigh

[2:10 pm] ASX 200 currently down 0.36%, well-above session lows of (-1.19%). Similar to the Monday session, Tech and Resources are trading higher, while almost everything else is down more than 1%. A fairly weak session beneath the hood, with 139 constituents (70%) trading lower. Healthcare has undercut the 18-May low and on track to close at a fresh ~9 year low. Staples, Real Estate, Discretionary and Financials all pulling back after a recent bounce. On the flip side, Tech is showing strong signs of a bottom, now up ~11% in the last three sessions and 7% away from its 200-day moving average. Energy stocks have started to creep higher, but still down ~5% in the past month. Materials are now within 2% of all-time highs, driven by strong gains across the commodity complex.

ASX 200 sectors (Source: Market Index)

Morgan Stanley flags peak ASX earnings expectations as housing slowdown filters into cyclicals

[1:40 pm] The analysts stay underweight Banks, Consumer-Facing and Housing-Linked names, arguing FY27e consensus growth of ~13% looks stretched as domestic channels slow.

Peak market earnings growth expectations reached, with downgrades emerging across FY26-FY28e and breadth narrowing through Health Care, Industrials, Consumer Discretionary, Staples and parts of Energy

FY27e consensus still sitting in the low- to mid-double digits at ~13% is the key calibration risk as housing and consumption channels weaken, with FY28e moderating to +6.9%

Banks most exposed via ~55% mortgage book weighting, with CBA and Westpac flagged as the highest-risk names on housing exposure and P/E multiples, NAB on broader macro, ANZ relatively less exposed

Consumer read-through: WES and Metcash most directly exposed via building products and hardware, with JB Hi-Fi and Harvey Norman exposed downstream through discretionary demand

Residential developers Stockland and Mirvac carry the highest direct earnings linkage to new build pricing and turnover, while REA Group faces a structural debate if tax-driven price declines erode residential property's relative attractiveness as an asset class

Industrials impacts longer-dated and mixed, with SGH (via Boral and Coates) and Reece most exposed, Bluescope meaningful through steel building products, and Reliance Worldwide and James Hardie less geared given offshore earnings mix

Macquarie nudges BlueScope target higher on US spread tailwinds

[1:38 pm] Macquarie reaffirmed an Outperform rating, with the central focus remaining a potential return of SGH/STLD to the bidding fray, layered onto strengthening US and now Asian steel spreads.

Target price raised to $35.95 from $33.80

US steel prices up 20% YTD and North Star spreads up 26%, with demand underpinned by data centre and infrastructure activity

Asian spreads recently lifted ~US$75/t to just over US$300/t, the first time at that level since mid-2023

M&A optionality intact with SGH's 'best and final' bid able to be revised after 18 June, and valuation now weighted to North America (~$21.14ps) versus ANZ, Asia and Property (~$15.14ps)

Australian housing softening though BSL's owner-occupier exposure offers some resilience, while Whyalla risk recedes after BSL exited the sale process as underbidder

Company page: BlueScope Steel (BSL)

Net trade to drag 0.8ppt from Q1 GDP

[1:35 pm] Australia's trade balance slipped into deficit for the first time since December 2017, with cyclone-disrupted iron ore and coal exports colliding with record AI server rack imports and higher fuel costs.

Current account deficit widened to $27.1bn in Q1 2026, the fourth consecutive quarterly deterioration and the largest as a share of nominal GDP since June 2016

Net trade expected to detract 0.8ppt from Q1 GDP, with exports down 1.2% (iron ore and coal hit by cyclones Koji and Mitchell alongside weaker iron ore prices) and imports up 0.8%

ADP equipment imports hit historic highs on bulk AI server rack shipments tied to NSW and Victoria data centre buildout, while crude and refined petroleum prices rose sharply on the Strait of Hormuz closure

Primary income deficit widened to $23.7bn as foreign-owned miners repatriated higher gold-driven profits to offshore shareholders

Net international investment liability position rose $62.3bn to $707.6bn, the highest since December 2023, as Middle East-driven equity volatility and a stronger AUD cut the value of super funds' overseas equity holdings

Source: ABS

Analysts' take on Peter Warren

[12:44 pm] Peter Warren Automotive issued a trading update on Monday, flagging a material deterioration in FY26 profit expectations, well below consensus, driven by new car margin compression as the mix shifts toward lower-margin small vehicles and EVs and competition from Chinese brands intensifies during the critical May/June period. The stock fell 25% on the day, and now down 58% year-to-date.

Jarden retained Buy, cut target from $2.50 to $1.55, viewing NTA backing as a valuation floor and OEM mix positioning as a differentiator that outweighs near-term earnings concerns.

E&P retained Positive, cut target from $2.50 to $1.70, noting the speed of deterioration surprised management but a broken downgrade cycle and meaningful property backing support a valuation recovery, with Chinese OEM additions key to margin normalisation.

Australian wheat crop tipped to shrink 26% as input costs and dry weather bite

[12:43 pm] The Department of Agriculture's first 2026/27 survey points to a sharp pullback in plantings, with Middle East war disruptions keeping fuel and fertiliser prices elevated.

2026/27 wheat production forecast at 26.7m tons, down 26% from last year and below both the 5- and 10-year averages

Planted area down 12% to 10.9m hectares, the smallest footprint since 2019/20, as weak global prices erode margins versus competing crops

US-Iran war (now in its fourth month) and Strait of Hormuz disruption have pushed fuel and fertiliser costs higher, with the department warning input costs could stay elevated for longer if the conflict drags on

Extremely dry conditions in NSW and southern Queensland have curbed plantings, with an expected El Niño set to reduce spring rainfall across the eastern states

Farmer willingness to buy urea at elevated prices remains a key swing factor for yields, while a building mouse plague in Western Australia is an additional risk to crops

Source: Bloomberg

Korea overtakes India as world's sixth-largest equity market

[12:42 pm] Samsung and SK Hynix have powered Korea's market cap 86% higher this year, while India battles foreign outflows and a weakening rupee.

Korea's total market cap up 86% year-to-date to $5 trillion vs. India's $4.8 trillion

Samsung Electronics and SK Hynix both joined the $1 trillion club, doing the heavy lifting on the rally and underscoring concentration risk tied to the memory cycle

India's Nifty down around 11% year-to-date, on track for its first annual drop after a decade of gains, dragged by a weakening rupee and roughly $26bn of foreign equity outflows

Korea has also leapfrogged Canada and parts of Europe this year, with Taiwan another AI-chipmaking hub reshaping global equity rankings

Source: Bloomberg

Banks broadly lower

[12:09 pm] A pretty heavy day for banks, with most names down 1-2%. The S&P/ASX 200 Financials Index is down 1.5% and down 3% in the last seven sessions.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

JDO | Judo Capital | -4.7% | $1.41 | -20.8% |

ANZ | ANZ Group | -3.0% | $33.99 | -6.7% |

BEN | Bendigo & Adelaide Bank | -2.1% | $10.20 | -3.7% |

WBC | Westpac | -2.0% | $35.44 | -7.9% |

MQG | Macquarie Group | -1.4% | $235.00 | 15.8% |

BOQ | Bank Of Queensland | -1.0% | $6.14 | -6.5% |

CBA | Commonwealth Bank | -0.8% | $161.94 | 0.8% |

NAB | National Australia Bank | -0.7% | $37.09 | -12.3% |

Tech stocks continue to bounce

[12:08 pm] Another solid day for tech stocks, with the S&P/ASX 200 Tech index up 2.4%, though off session highs of 4.2%.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

360 | Life360 | 8.59% | $22.12 | -31.35% |

MP1 | Megaport. | 7.02% | $16.61 | 36.37% |

PME | Pro Medicus | 6.35% | $153.64 | -30.37% |

XRO | Xero | 6.07% | $85.86 | -24.62% |

CAT | Catapult Sports | 4.85% | $3.89 | -6.49% |

WTC | Wisetech Global | 4.16% | $40.78 | -40.46% |

DDR | Dicker Data | 2.16% | $11.11 | 7.92% |

WBT | Weebit Nano | 1.69% | $7.23 | 44.60% |

SDR | Siteminder | 1.68% | $3.95 | -35.64% |

TNE | Technology One | 1.21% | $32.14 | 16.60% |

AD8 | Audinate Group | 1.17% | $2.16 | -46.92% |

BVS | Bravura Solutions | 0.21% | $2.41 | -6.42% |

DTL | Data#3 | -0.16% | $9.38 | 4.52% |

HSN | Hansen Technologies | -0.32% | $4.74 | -10.32% |

NXL | Nuix | -0.33% | $1.51 | -16.85% |

ELS | Elsight | -0.40% | $7.53 | 140.58% |

NXT | NextDC | -0.45% | $15.45 | 25.46% |

MAQ | Macquarie Technology Group | -0.76% | $75.76 | 13.07% |

OCL | Objective Corporation | -0.96% | $11.29 | -31.78% |

CDA | Codan | -1.93% | $42.00 | 47.77% |

IRE | Iress | -3.32% | $5.97 | -28.82% |

PPS | Praemium | -3.52% | $0.69 | -13.84% |

DGT | Digico Infrastructure Reit | -5.12% | $2.41 | -13.62% |

Analysts' take on Pro Medicus

[11:31 am] Pro Medicus announced a fresh batch of US contract wins and renewals on Monday, including deals with Beth Israel Lahey Health, Northwestern Medicine, TidalHealth and a third consecutive term renewal from Allegheny Health Network.

Analysts were broadly positive, viewing the multi year term commitments as evidence against the bear case that healthcare enterprises are shortening contracts ahead of AI disruption, while flagging strong renewal pricing uplifts (typically more than doubling per transaction), growing Cardiology cross sell traction, and FY27 as the key earnings inflection year.

Morgans retained Buy, target unchanged at $210.00. Procurement feedback reinforces strong competitive positioning, the AI disruption bear case is not showing up in contract data, and the Cardiology upsell adds meaningful value at near zero incremental cost heading into the FY27 inflection.

RBC retained Sector Perform, target unchanged at $195.00. The TidalHealth and Allegheny deals confirm no preference for shorter contract durations, the Allegheny renewal value more than doubled versus the prior contract, and Cardiology is gaining traction as the third signed customer to date.

Goldman Sachs retained Buy, lowered target from $200.00 to $197.00. Diverse contract wins across multiple US states and healthy hospital capex (with imaging a priority) support the thesis, while AI contracts contain no direct component to preserve upside and easing FDA approvals are seen as a potential tailwind for AI monetisation.

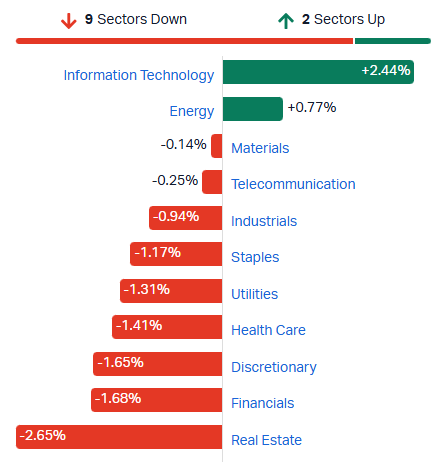

ASX 200 tumbles in early trade

[11:04 am] The ASX 200 was aggressively sold down despite opening ~0.3% lower. The index is currently down 0.95%, with six sectors down more than 1%. Breadth is very weak, with 150 constituents (75%) trading lower.

S&P/ASX 200 sectors (Source: TradingView)

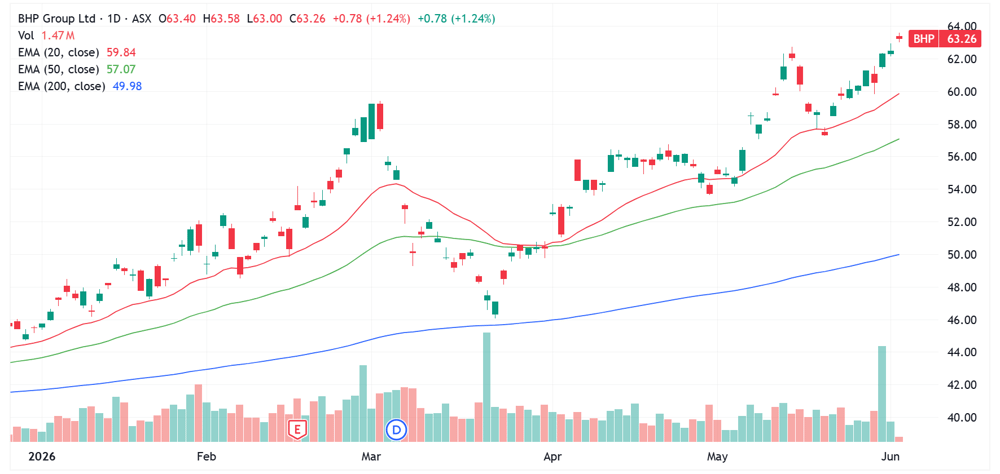

BHP opens at fresh all-time highs

[10:21 am] BHP is on track to record its third straight all-time high, up 1.31% in early trade to $63.30. This follows a strong overnight lead as copper prices rallied 2.7% to US$6.60/lb.

BHP shares are now up 37.6% year-to-date and up 66.2% in the last twelve months.

BHP daily price chart (Source: TradingView)

Top All Ords gainers and losers

[10:18 am] Tasmea rallies off the back of a highly earnings accretive acquisition, while large cap tech stocks still dominate today's leaderboards and gold stocks trade broadly lower.

Ticker | Company | % Chg | Price |

|---|---|---|---|

TEA | Tasmea | 15.77% | $8.00 |

HGH | Heartland Group | 11.17% | $1.05 |

360 | Life360 | 9.23% | $22.25 |

SRG | SRG Global | 8.92% | $3.42 |

PME | Pro Medicus | 8.10% | $156.16 |

MP1 | Megaport | 7.02% | $16.61 |

NST | Northern Star Resources | 6.92% | $19.79 |

LIN | Lindian Resources | 6.33% | $0.84 |

XRO | Xero | 6.14% | $85.92 |

VSL | Vulcan Steel | 6.13% | $5.89 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

SPZ | Smart Parking | -6.74% | $0.83 |

SRV | Servcorp | -5.85% | $6.28 |

PNR | Pantoro Gold | -5.43% | $2.88 |

BTL | Beetaloo Energy Australia | -5.08% | $0.28 |

SPL | Starpharma | -4.83% | $0.69 |

GMD | Genesis Minerals | -4.82% | $5.63 |

RSG | Resolute Mining | -4.38% | $1.20 |

KCN | Kingsgate Consolidated | -4.27% | $6.05 |

OBM | Ora Banda Mining | -4.27% | $1.35 |

NCK | Nick Scali | -4.26% | $13.72 |

Top ASX 200 gainers and losers

[10:16 am] SRG rallies on an FY26 guidance upgrade, tech stocks continue to trend higher, while REITs experience a broad-based selloff.

Ticker | Company | % Chg | Price |

|---|---|---|---|

SRG | SRG Global | 9.24% | $3.43 |

360 | Life360 | 9.18% | $22.24 |

PME | Pro Medicus | 8.42% | $156.62 |

NST | Northern Star | 7.08% | $19.82 |

MP1 | Megaport | 7.02% | $16.61 |

XRO | Xero | 6.87% | $86.51 |

WTC | Wisetech Global | 5.42% | $41.27 |

SEK | Seek | 5.04% | $12.93 |

4DX | 4DMedical | 4.65% | $4.28 |

DRO | Droneshield | 4.52% | $3.24 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

SCG | Scentre Group | -4.24% | $3.61 |

GGP | Greatland Resources | -4.05% | $13.26 |

VCX | Vicinity Centres | -3.97% | $2.42 |

GMD | Genesis Minerals | -3.89% | $5.68 |

LOV | Lovisa | -3.81% | $22.22 |

OBM | Ora Banda Mining | -3.77% | $1.35 |

DOW | Downer | -3.68% | $7.85 |

DRR | Deterra Royalties | -3.67% | $4.33 |

ALK | Alkane Resources | -3.48% | $1.47 |

MGR | Mirvac Group | -3.30% | $1.61 |

DroneShield wins $19.3m counter-drone contract

[10:04 am] DroneShield has secured a $19.3 million contract for mobile and fixed-site counter-drone solutions supporting the US Department of War's Joint Interagency Task Force 401, with at least $10 million expected to be recognised as FY26 revenue and the balance in FY27.

The deal also carries an additional $5.6 million in end-user options over a five-year period.

Company page: DroneShield (DRO)

TPG flags postpaid mobile outperformance and steps capex down to $550-650m through FY29

[9:39 am] Investor Day update points to mobile share gains and improving ARPU, though NBN competition stays tough and Fixed Wireless growth has only just resumed.

Mobile postpaid subscribers anticipated to outperform the market, with strong growth in Digital First and MVNO. Prepaid expected to decline following 1H26 plan refreshes

ARPU growing year-to-date across all mobile offerings on 2H25 and Q1 back-book plan refreshes, partly offset by EGW growth weighing on postpaid ARPU mix

Fixed Wireless returned to growth in Q2, but NBN competitive dynamics remain challenging

Capex guided to $650m in FY27 and $550m-$650m in FY28-29

Macquarie (Feb-26) forecast FY27 capex of $666m and FY28 of $654m

6G upgrades not expected before 2030

Company page: TPG Telecom (TPG)

Tasmea acquires Maxim Group in $254m deal

[9:35 am] The acquisition has been pitched as a step-change in scale across data centres, BESS and major infrastructure, with deal funded by cash, scrip and an earn-out tied to a $50 million EBIT hurdle.

Total consideration of up to $254m for 100% of Maxim Group, comprising $184m upfront ($112m cash and $72m in scrip at $6.00) plus up to $70m in cash earn-outs across FY27-29 tied to maintainable EBIT of $50m per annum

Valuation pitched at around 5.4x EV/EBIT on Maxim's FY26e underlying EBIT of $47m, with the business having delivered around 70% revenue CAGR FY24A-FY26e and an identified pipeline above $1.3bn (full FY27 revenue visibility, around 85% for FY28)

Forecast 31% pro-forma EPS accretion in FY26e (ex-synergies), lifting pro-forma FY26 underlying EBIT to $175m (from $128m pre-Maxim)

Post-deal leverage of around 0.8x net debt to pro-forma FY26e EBITDA, inside Tasmea's 1.0x target

Strategic exposure pitched to data centres (Victoria forecast at 22% CAGR CY25-30 per DC Byte), BESS (AEMO forecasting 58% CAGR in NEM utility-scale storage FY25-30) and Victorian rail infrastructure (Metro Tunnel, West Gate Tunnel, North East Link, Suburban Rail Loop)

Company page: Tasmea (TEA)

RFG narrows FY26 EBITDA guidance lower

[9:33 am] Retail Food Group's cost program is running ahead of schedule but a tough consumer backdrop forces a tighter, lower guidance range.

FY26 underlying EBITDA guidance narrowed to $20-21m from $20-24m, a 7% downgrade at the midpoint

Core Brand Network Sales down 4.8% in the first 20 weeks of 2H26, with Core Brand Same Store Sales down 0.8%

Weakness attributed to reduced customer count on café/coffee bakery closures, recent rate hikes, inflation and historically low consumer confidence

Cost rationalisation running ahead, with FY26 savings now expected at $2.3-2.5m (previously $1.2-1.8m)

Company page: Retail Food Group (RFG)

SRG Global upgrades FY26 EBITDA to top end and guides FY27 above consensus

[9:23 am] Contract wins across nine sectors underpin a step-change in FY27 earnings, with guidance ahead of consensus.

$1.85bn of new contracts secured across Water, Defence, Energy, Industrial, Resources, Ports, Data Centres, Health and Education

FY26 EBITDA guidance upgraded to the top end of the $164m-$168m range, implying $168m vs $166.1m ests (1% beat)

FY27 EBITDA guidance initiated at $190m-$200m, midpoint $195m vs $188.5m ests (3% beat)

Marquee wins include an 8-year Fortescue multi-disciplinary maintenance contract in the Pilbara, a 7-year Origin Energy asset integrity contract in Central QLD, a 5-year Alcoa asset integrity contract in WA, and an 8-year Gympie Regional Council water alliance through to 2034

SRG shares have traded relatively flat year-to-date, but up 105% in the last twelve months.

Company page: SRG Global (SRG)

Kelsian secures two-year Sydney Region 6 bus extension

[9:22 am] Kelsian subsidiary Transit Systems West has signed a Deed of Variation with Transport NSW, extending its inner-west Sydney bus contract through 30 June 2028.

Two-year extension from 1 July 2026 worth approximately $500m in additional revenue, covering operation and maintenance of 528 buses across four depots

CEO Graeme Legh framed the deal as "capital light" and flagged the contract includes revenue indexation mechanisms protecting against cost fluctuations

Company page: Kelsian Group (KLS)

Wesfarmers folds Blackwoods and Workwear Group into Bunnings

[9:21 am] Wesfarmers is transitioning its Industrial and Safety businesses into Bunnings Group from 1 July 2026, bringing together complementary customer bases and targeting incremental sales plus cost efficiencies.

Blackwoods and Workwear Group move into Bunnings on 1 July 2026, with financials consolidated into Bunnings' results from 1H27.

Strategic logic centred on leveraging Bunnings' scale to better serve small and medium sized customers via Blackwoods' product range and national fulfilment, while Blackwoods continues to service large enterprise customers

No material one-off costs expected, with further updates due at the full-year result in August 2026

Company page: Wesfarmers (WES)

Elliott pushes Northern Star for strategic review, CEO search and board refresh

[9:13 am] Activist Elliott, holding well over $1 billion in Northern Star, has published a "Northern Star Rising" presentation calling out operational missteps, cost overruns and inconsistent strategy, and is pressing for a strategic review run alongside a CEO search and operational improvement process. Elliott is also pushing for fresh board appointments and says it wants to work constructively with the company.

A very interesting slide deck (highly recommend you give it a whiz) - link to presentation here.

Otherwise, here are my key takeaways:

Elliott says NST has underperformed peers by 203% over the last three years, trading at the lowest price to NAV and EBITDA multiple of any peer

Missed guidance seven times in the past four financial years

KCGM, Hemi and Pogo described as "highly valuable, world-class assets", and "great mines deserve to be run by the best-in-class leadership"

Recommends company to explore all strategic alternatives, including a sale of the company

Enhance the Board with experienced and relevant executives, plus a world-class external CEO

My favourite slide is #31, which observes an ongoing talent exodus (all of which have joined other emerging gold names, leading to significant share price outperformance).

Company page: Northern Star Resources (NST)

Inghams shopped to private equity and food buyers

[9:10 am] Interesting piece by the AFR about Inghams being pitched to private equity and food companies like Tyson Foods, JBS and Cargill. However, the article does not cite any sources indicating these parties are interested/spoken with.

Investment bankers are shopping Inghams to buyers, with the stock at $2.08 vs. a May all-time low of $1.69 and a 2019 high of $4.61

CEO Ed Alexander conceded "ever since listing, it's fair to say we've fallen short"

Strategic shift toward branded products and away from chasing volume, with poultry volumes modestly improving as Inghams reallocates from Woolworths per Morningstar's Angus Hewitt

Bull case rests on chicken's structural tailwinds as a cheap, healthier protein in a cost-of-living squeeze, with private equity already active in growers (KKR's ProTen)

Source: AFR

Nvidia takes on Intel, AMD, Apple and Qualcomm with RTX Spark PC chip

[9:05 am] Jensen Huang used Computex to push Nvidia into the PC CPU market alongside Microsoft, while also moving the Vera data centre CPU into full production.

Nvidia unveiled the RTX Spark PC superchip with Microsoft, debuting in fall across ~30 laptops and ~10 desktops from Dell, HP, ASUS, Lenovo and MSI. Combines a Blackwell GPU with a new Arm-based Grace CPU and 128GB unified memory, built on TSMC's 3nm

Huang framed it as "the first completely re-engineered, reinvented line of PCs in 40 years" and sized the broader CPU opportunity at $200bn, with Arm-based architectures gaining share over the x86 incumbents

Direct competitive read for Intel, AMD, Qualcomm and Apple. Intel used the same conference to unveil its Xeon 6+ data centre CPUs, while AMD is reportedly working on its own Arm-based PC chip

Vera data centre CPU now in full production, shipping in fall to early customers Anthropic, OpenAI, xAI, Dell, Oracle and CoreWeave. Nvidia VP Ian Buck flagged Vera generates tokens 1.8x faster than x86, with Huang calling CPUs the company's "new major growth driver"

Nvidia shares surged 6.2% to $244.36 but still ~5% away from its 14 May record. The stock is up 17% year-to-date.

Anthropic confidentially files for IPO at $965bn valuation

[9:04 am] Anthropic's S-1 filing comes off a $47 billion revenue run rate and a record funding round, with SpaceX roadshowing this week and OpenAI's own filing also in progress.

Anthropic confidentially filed its S-1 with the SEC, with timing dependent on market conditions. The official prospectus must land with investors at least 15 days before any roadshow

Revenue run rate has scaled to $47bn vs. $10bn in annual revenue last year. Last week's funding round closed at a $965bn valuation, ahead of OpenAI's $852bn mark in late March

Infrastructure capacity ramp continuing, with Anthropic agreeing to pay SpaceX $1.25bn per month through May 2029 to use compute at the Colossus 1 data centre in Memphis

US May ISM manufacturing tops ests at 54.0

[9:06 am] Despite the headline beat, 57% of respondents cited pricing volatility tied to the US-Iran conflict and input costs rose at the fastest pace since July 2022.

ISM Manufacturing printed 54.0 vs 53.0 ests and 52.7 prior

New orders rose to 56.8 from 54.1, with previews suggesting demand pull-forward as firms front-run price increases

Prices paid eased to 82.1 from 84.6, breaking a four-month run of increases but holding near the highest reading since April 2022. Employment improved but remained in contraction

Respondent commentary distinctly cautious, with 57% flagging pricing volatility tied to the US-Iran conflict and energy costs. Continued component shortages noted alongside strong demand

Trump shrugs off Iran talks collapse before later signalling progress, Hezbollah ceasefire flagged

[8:58 am] A classic Trump interview, where he stressed Iran talks are "continuing at a rapid pace" but "couldn't care less" if negotiations stalled.

Trump told CNBC he "couldn't care less" if Iran talks are over, accused Tehran of "stalling" and denied any direct word from Iran on ending negotiations. Said oil would be "dropping like a rock" with 1,700 tankers loaded and ready

Later Truth Social posts flagged a "very productive call" with Netanyahu, no US troops heading to Beirut, and Hezbollah agreeing via intermediaries that "all shooting will stop"

Netanyahu pushed back on X, warning Israel will strike Beirut targets if Hezbollah keeps attacking Israeli cities, and that the IDF will continue operating in southern Lebanon as planned, leaving the ceasefire framing fragile

Nuclear red line reiterated, with Trump threatening to "blow them up to kingdom come" if Iran pursues a weapon, signalling continued military optionality

Source: CNBC

Russia bans jet fuel exports through November

[8:56 am] A second consumer-fuel export ban this year, with refining throughput at 16-year lows after stepped-up Ukrainian drone strikes on energy assets.

Russia banned jet fuel exports through end-November to shore up the domestic market ahead of summer demand, on top of the gasoline export ban reimposed from 1 April

Crude-processing rates have fallen to the lowest in more than 16 years on Ukrainian drone strikes targeting refineries, ports and pipelines, part of a campaign to choke petrodollar inflows

Limited global market impact, with Russia averaging 30,000 b/d of jet fuel exports last year (under 2% of global supply) and 28,000 b/d in the first four months of 2026. Turkey the main buyer

Source: Bloomberg

Iran cuts US talks and vows to fully close Hormuz

[8:55 am] Tasnim's report flagged a potential full Hormuz blockade and threats of closing the Bab el-Mandeb passage.

Iran said it will stop messaging the US through intermediaries and move to "completely block" the Strait of Hormuz until Israel fully withdraws from Lebanon and halts attacks in Lebanon and Gaza

Tehran also flagged activation of the Bab el-Mandeb chokepoint linking the Red Sea to the Gulf of Aden, broadening the geographic risk premium beyond the Persian Gulf

Israel escalating in parallel, with Netanyahu ordering strikes on Hezbollah-controlled Beirut suburbs

Source: CNBC

Dollar pushes higher as Iran tensions, AI rally and four-year ISM high stoke Fed hike bets

[8:49 am] Speculative dollar longs have more than tripled in three weeks, with traders positioning for a Fed pivot to hikes as the AI-driven equity rally and Middle East risk premium reinforce the bid.

Bloomberg Dollar Spot Index rose 0.3% Monday after Iran said it would suspend negotiations over Israel's Lebanon offensive, with gains capped later by Trump claiming talks were progressing

US May manufacturing PMI expanded at the fastest pace in four years, reinforcing speculation the Fed under new Chair Kevin Warsh could start raising rates as soon as late this year

Speculative positioning has flipped sharply bullish as leveraged funds, asset managers and others now hold around $16.5bn in long dollar wagers per CFTC data, the most since April and up from roughly $5bn three weeks ago

Source: Bloomberg

Hedge funds hit fastest US equity buying pace in six months as risk appetite returns

[8:48 am] Goldman's prime desk flagged a sharp shift from late-May defensiveness, with financials drawing the biggest net buying in nearly six months and leverage metrics pushing into the 89th percentile.

Hedge funds bought US equities at the fastest pace in six months last week, driven by long buys and short covers across index and ETF products

Financials the standout, with long purchases outpacing short sales roughly 6.5 to 1, led by payments and to a lesser extent banks, partly offset by selling in consumer finance and capital markets

Despite the inflows, gross and net allocations to financials remain in the 1st percentile of the past five years

Industrials remain under pressure, net sold for seven of the last eight weeks. Short exposure now at the 90th percentile on a one-year basis, with most of the selling since February driven by fresh shorts rather than long liquidation

Leverage signalling renewed risk appetite: US long/short net leverage rose to 55.3% (89th percentile, one-year), and the US Fundamental long/short ratio is now in the 99th percentile

Source: Bloomberg

SoftBank overtakes Toyota as Japan's most valuable company

[8:45 am] SoftBank's 14% Monday surge took it past Toyota for the first time since the 2000 dot-com bubble, capping a 90% YTD run as AI-linked names reshuffle Japan's corporate hierarchy.

SoftBank market cap pushed above ¥48tn vs. Toyota's ~¥46trn, with Toyota shares down more than 10% YTD

Kioxia now Japan's third most valuable company at around ¥40tn. The NAND supplier expects to earn more this quarter than it did in the full year ended March on AI data centre demand

Catalyst stack for SoftBank includes the weekend announcement of up to $87bn in AI data centre investment in France, plus pipeline IPOs at portfolio companies OpenAI and SB Energy

Toyota pressured by Iran-driven oil price spike weighing on global auto demand, alongside ongoing capital intensity of the EV and software transition

Source: Bloomberg

Memory chip frenzy drives historic AI rally

[8:44 am] Chip stocks have powered the S&P 500 to a two-month run only matched four times in 75 years, with strategists lifting targets and fund managers cutting cash despite valuation and inflation concerns.

S&P 500 up 16% across April and May driven by chip stocks, a move matched only four times since 1950. In each prior instance, the index was higher six months later by a median 17%

Memory and chip leadership has been extraordinary, with Micron up around 10-fold over 12 months to a market cap above $1tn, Samsung up around 465%, Intel tripled in 2026 to its first record since 2000, Cisco and Qualcomm both up around 50%

Goldman Sachs lifted its year-end S&P 500 target to 8000 from 7600, implying 5.5% upside on top of the 11% YTD gain

S&P 500 trading at around 22.5x forward earnings, slightly below the start-of-year multiple as earnings estimates have moved higher

Source: WSJ

S&P 500 and Nasdaq notch record closes as software rotation extends, oil jumps on Iran

[8:39 am] Indices closed at fresh highs despite mixed breadth, with software's run continuing to outpace semis and AI catalysts offsetting a cautious Middle East tape.

S&P 500, Dow and Nasdaq printed fresh record closes with only two sectors higher, software the clear standout (iShares Software ETF IGV up around 16% over the past three sessions, outperforming the SOX for a fourth straight session)

Middle East signals mixed, with Iranian state media saying Tehran has suspended mediated talks and will fully block the Strait of Hormuz, offset later by Israel delaying planned Lebanon airstrikes at US request and Trump saying Iran talks are continuing

AI catalysts driving tech sentiment. Nvidia unveiled its RTX Spark chip at Computex for the first personal laptops designed to run AI agents, Anthropic confidentially filed for IPO, and Intel said it would ship a new AI inference chip by year-end using cheaper memory and cooling tech

US May ISM Manufacturing beat and printed its highest level since May 2022. Prices paid ticked lower but remain elevated, employment improved but still in contraction

Good morning!

[8:32 am] ASX 200 futures are down 36 pts (-0.41%).

The overnight session in a nutshell:

S&P 500 (+0.26%), Dow (+0.09%) and Nasdaq (+0.42%) closed at record highs, though breadth was slightly negative, only Technology and Energy sectors finished higher

Nvidia rallied 6% after unveiling its RTX Spark PC superchip, lifting Arm and Dell while Intel, AMD and Qualcomm traded lower

Oil spiked as much as 6% (settled 3.6% higher) after Iran halted US talks and threatened to block the Bab el-Mandeb Strait, Trump told CNBC he "couldn't care less" if talks are over and accused Iran of "stalling" talks