ASX 200 Live Today - Thursday, 7th May

The S&P/ASX 200 is set to surge as US-Iran proposal outlines path to end the war. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Thursday, May 7. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

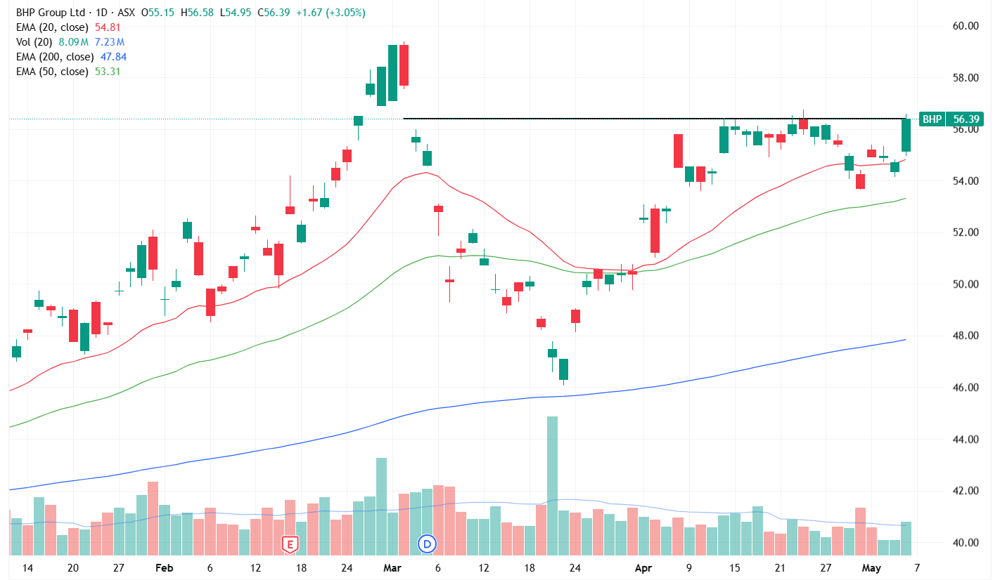

ASX 200 higher, BHP within 2% of all-time highs

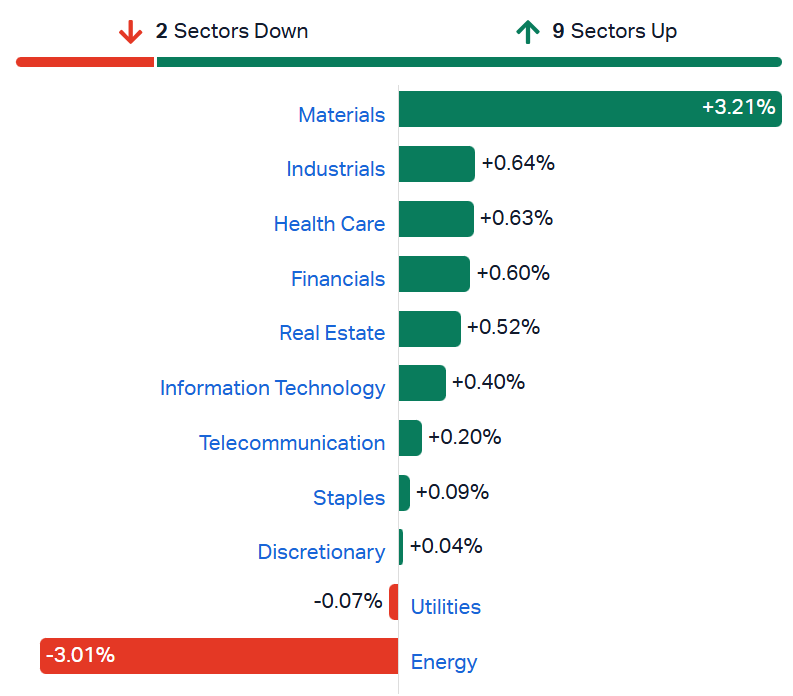

[2:15 pm] A rather encouraging session, with the ASX 200 up 0.80% (vs. session highs of 1.07%). The index dipped below the key 200-day moving average earlier this week, but has now soared back above this key level (and above the 50-day too). Breadth is a little dicey, reflecting weakness from sectors like Energy (-3.1%), Utilities (-1.2%), Healthcare (-0.4%) and Tech (-0.2%).

BHP (+3.2%) is showing some incredible strength as copper returns to US$6.2/lb and iron ore crosses US$110 a tonne. The stock has now rallied ~6.3% in the last two sessions and within 2% of all-time highs. The broader ASX 200 Materials Index has also gained 5.7% since Wednesday, but ~6% from its 2 March record high. Plenty of sub-sectors like uranium, gold and copper are still trading well-below recent highs.

Banks also choppy, with the ASX 200 Financials Index up 0.27% vs. session highs of 0.67%. This follows a massive 2.39% rally on Wednesday.

Overall, the index returns to a comfortable level, though not all gains are equal. Energy stocks are on the backfoot, tech is taking a breather and no one wants to touch healthcare stocks. Despite the challenges beneath the hood, the commodity complex is kicking on, with very broad strength. Thanks for tuning in and we'll catch you tomorrow.

Analysts divided on Imdex

[1:43 am] Imdex delivered a Q3 trading update on Wednesday with record quarterly revenue broadly in line with expectations, despite a ~6% FX headwind, with constructive read-throughs on the higher-margin sensors/SaaS mix shift and CY26 exploration budgets tracking materially above the prior year. The stock rallied 3.2% on the day, but down 9.4% on Thursday.

The key debate centred on whether the demanding Q4 step-up required to meet consensus is achievable, with most analysts constructive (citing North American seasonality and acquisition contributions) while one cut to Sell on valuation.

UBS retained Buy, raised target from $4.70 to $5.15. Growing confidence in continued double-digit revenue growth into Q4, with margin expansion from higher-margin mix and constructive FY27 momentum as juniors re-engage.

Jarden downgraded to Sell from Underweight, target unchanged at $3.60. Quarter-on-quarter momentum has stalled, the Q4 consensus hurdle is considerable, and valuation is viewed as extreme with no room for execution risk.

Atlantic Lithium agrees to $292m takeover by Huayou Cobalt

[1:40 pm] Atlantic Lithium has entered a binding Scheme Implementation Deed this morning with China's Zhejiang Huayou Cobalt for an all-cash acquisition of the Africa-focused lithium developer.

Cash consideration of US$0.25486 per share (A$0.354), valuing Atlantic Lithium at approximately US$210m (A$292m)

Offer represents a 26.6% premium to the last close of $0.280

Board unanimously recommends shareholders vote in favour, absent a superior proposal and subject to an independent expert concluding the Scheme is in shareholders' best interests

Largest shareholder Assore International (~26.4% stake) intends to vote in favour, subject to the same conditions

We're starting to see some fairly encouraging deals within the lithium sector, including the European Lithium ($835m bid from Critical Metals) and Global Lithium (China's Lopal Tech to provide maximum pre-payment of US$75m for offtake that won't be delivered until 1Q28).

Company page: Atlantic Lithium (A11)

Credit Corp rallies on reaffirmed guidance

[1:32 pm] A pretty big intraday rally for Credit Corp, which opened 3.8% higher, now up 9.2%.

The company reaffirmed its FY26 guidance this morning, including:

FY26 NPAT guidance reaffirmed at $100-110m

FY26 EPS guidance of $1.47-1.62 vs $1.53 ests (midpoint is ~1% ahead)

Ledger investment guidance refined to $295-330m vs prior $280-330m

Gross lending guidance upgraded to $420-430m vs prior $350-390m

On track for record earnings with investment growth to provide a platform for FY27 growth

As we noted this morning: Credit Corp suffered a sizeable 16.7% selloff on the day of its 1H26 result (4-Feb). This was where 1H26 net profits came in ~10% below market expectations, but FY26 guidance was reaffirmed (implying a big catchup in 2H26).

Today's update shows greater confidence in the full year guidance, and likely driving a strong bid to bring it back towards pre-selloff levels.

Analysts' take on Infratil

[12:14 pm] Infratil's ~50%-owned CDC signed Australia's largest ever data centre contract on Wednesday, a 30-year, 555MW deal with a US hyperscaler that lifted total contracted capacity above 1GW, alongside maiden FY28 EBITDAF guidance exceeding $1 billion (rising to ~$2B at full deployment), driving IFT shares ~13% higher on the day.

RBC Capital Markets retained Sector Perform, raised target from NZ$12.25 to NZ$14.00. Saw the deal as strategically significant with supportive pricing escalation and manageable debt-funded capex, though noted land costs remain an open question.

Analysts' take on Super Retail

[12:11 pm] Super Retail Group's 18-week H2 trading update disappointed across most divisions, with BCF hit hardest as the US-Iran conflict drove fuel prices higher and crushed outdoor recreation demand over the Easter/school holiday period, while Rebel proved the relative outperformer. The stock fell as much as 13.5% today, now down just 3.2%.

JPMorgan retained Overweight, lowered target from $17.00 to $15.30. Viewed the sales inflection as more severe than peers but exogenous and largely past its worst, with valuation already discounting a weaker outlook.

RBC Capital Markets retained Outperform, lowered target from $17.30 to $15.50. Saw BCF as the most exposed to holiday activity dependency, but expects recovery as the fuel excise cut restores consumer confidence.

UBS retained Neutral, lowered target from $13.50 to $12.50. Flagged Auto and BCF as having the highest fuel price sensitivity in their coverage, with operating deleverage from CODB inflation seen as an ongoing headwind.

Uranium stocks up 5-7%

[11:00 am] Most ASX-listed uranium names are up 5-7% in early trade. This move is broadly in-line with how uranium equities performed overnight, where the NYSE-listed Global X Uranium ETF rallied 7.4%.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

PEN | Peninsula Energy | 7.3% | $0.44 | -8.1% |

AGE | Alligator Energy | 7.3% | $0.04 | 41.9% |

PDN | Paladin Energy | 6.4% | $12.69 | 98.3% |

NXG | Nexgen Energy | 6.3% | $17.68 | 110.2% |

BOE | Boss Energy | 6.0% | $1.42 | -61.9% |

DYL | Deep Yellow | 5.8% | $1.83 | 48.4% |

EL8 | Elevate Uranium | 5.8% | $0.28 | -8.3% |

BMN | Bannerman Energy | 5.7% | $4.09 | 56.1% |

AEE | Aura Energy | 5.4% | $0.14 | 19.1% |

LOT | Lotus Resources | 1.2% | $0.83 | -61.0% |

Copper stocks surge

[10:58 am] Copper stocks trading sharply higher after copper prices surged 3.4% overnight to US$6.2/lb. Plenty of smaller cap explorers/developers up 5-7%, though most are trading well-off Jan-Feb highs.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

AR1 | Austral Resources | 7.7% | $0.10 | -40.6% |

FFM | Firefly Metals | 5.8% | $1.83 | 112.8% |

CYM | Cyprium Metals | 5.5% | $0.39 | 62.1% |

29M | 29Metals | 5.2% | $0.24 | 118.3% |

HGO | Hillgrove Resources | 5.0% | $0.04 | 16.7% |

CSC | Capstone Copper Corp | 5.0% | $12.28 | 64.0% |

SFR | Sandfire Resources | 4.0% | $17.63 | 68.2% |

HCH | Hot Chili | 3.5% | $1.79 | 278.5% |

AIS | Aeris Resources | 3.2% | $0.39 | 103.7% |

BHP | BHP Group | 3.1% | $58.14 | 53.6% |

Banks higher for a second day

[10:54 am] Major banks are trading broadly higher after Wednesday's 2.3% rally. The S&P/ASX 200 Financials Index is now at a two-week high and recovered almost half of its recent drawdown (fell 5.9% between 10-Apr and 5-May).

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

WBC | Westpac | 2.2% | $39.78 | 24.7% |

CBA | Commonwealth Bank | 1.0% | $179.75 | 7.6% |

BEN | Bendigo & Adelaide Bank | 0.9% | $10.83 | -4.4% |

ANZ | ANZ Group | 0.8% | $37.39 | 24.9% |

BOQ | Bank Of Queensland | 0.7% | $6.40 | -14.6% |

MQG | Macquarie Group | 0.5% | $241.87 | 23.7% |

NAB | National Australia Bank | -1.8% | $39.29 | 8.1% |

Top ASX 200 gainers

[10:49 am] A massive session for resources, led by uranium, gold and nickel names. Orica is also trading sharply higher, off the back of a relatively positive 1H26 result (the stock was rather aggressively sold off in recent weeks amid supply chain concerns).

Ticker | Company | % Chg | Price |

|---|---|---|---|

PDN | Paladin Energy | 7.29% | $12.80 |

DYL | Deep Yellow | 7.07% | $1.85 |

NXG | Nexgen Energy | 6.23% | $17.66 |

ORI | Orica | 5.59% | $22.09 |

PDI | Predictive Discovery | 5.59% | $0.95 |

GGP | Greatland Resources | 5.54% | $14.85 |

WGX | Westgold Resources | 5.14% | $5.73 |

NIC | Nickel Industries | 4.76% | $1.10 |

CSC | Capstone Copper Corp | 4.70% | $12.25 |

RMS | Ramelius Resources | 4.68% | $3.58 |

Top ASX 200 losers

[10:49 am] Tabcorp smashed after Austrac launched an anti-money laundering probe, easing US-Iran tensions also driving energy names like Woodside and Viva Energy lower.

Ticker | Company | % Chg | Price |

|---|---|---|---|

TAH | Tabcorp | -20.26% | $0.92 |

LNW | Light & Wonder | -10.67% | $100.05 |

IMD | Imdex | -6.09% | $4.16 |

4DX | 4DMedical | -5.92% | $3.58 |

VEA | Viva Energy Group | -4.85% | $2.26 |

EOS | Electro Optic Systems | -4.11% | $9.56 |

WDS | Woodside Energy | -4.04% | $30.56 |

SUL | Super Retail Group | -3.95% | $11.20 |

NHC | New Hope Corporation | -2.82% | $5.17 |

ASX | ASX | -2.76% | $61.06 |

ASX 200 soars to two-week high

[10:20 am] The S&P/ASX 200 is trading sharply higher, up 0.97% and on-track to have gained over 2% in the last two sessions. Did someone say commodity supercycle?

Miners are ripping higher today, with broad gains for most large cap names like BHP (+3.4%), South32 (+3.3%), Sandfire (+2.9%), Rio Tinto (+2.3%), PLS Group (+2.0%) and more.

Much like the overnight session, defensives sectors like Utilities, Telcos and Staples are struggling for upside. While Tech stocks also struggling after the recent five-day winning streak.

S&P/ASX 200 sectors (Source: Market Index)

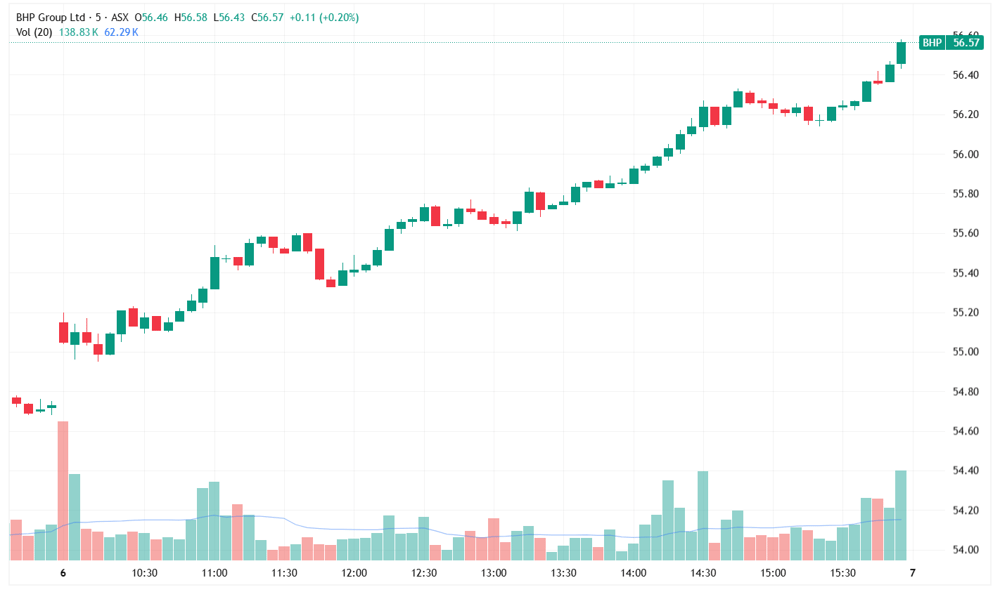

Miners caught an aggressive bid on Wednesday

[9:50 am] Most large cap ASX-listed miners trended higher into the close on Wednesday, perhaps an encouraging sign for the materials index.

BHP, for example, opened the session 0.79% higher and spent effectively the entire day trending higher, closing up 3.0%.

BHP intraday chart for Wednesday, 6 May (Source: TradingView)

On the daily chart, it's trying to break out to a two-month high.

BHP daily price chart (Source: TradingView)

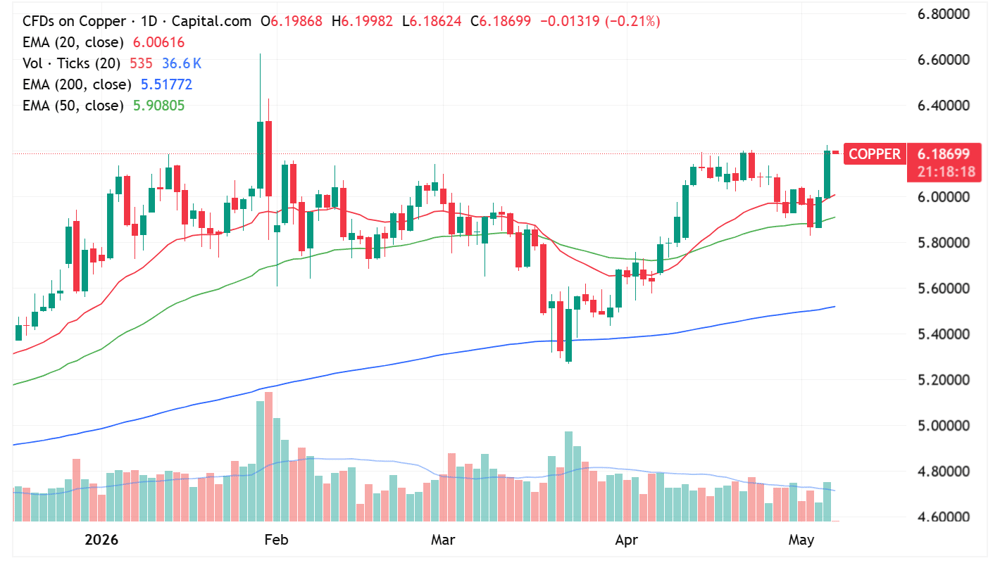

Copper back near all-time highs

[9:43 am] A massive overnight session for copper, with prices up 3.4% and within 2% of the 29-Jan record close. This drove a strong response for copper equities, with the NYSE-listed Global X Copper Miners ETF up 6.8%.

Copper daily price chart (Source: TradingView)

Tabcorp under AUSTRAC investigation over AML/CTF concerns

[9:35 am] The wagering operator has been notified by AUSTRAC of an enforcement investigation into its anti-money laundering and counter-terrorism financing compliance.

AUSTRAC has raised "a number of serious concerns" with Tabcorp's ability to effectively identify, mitigate and manage ML/TF risks

Enforcement investigation will initially focus on Tabcorp's compliance with AML/CTF Act obligations, including having a compliant AML/CTF Program and appropriately monitoring customers

AUSTRAC noted the investigation is at an early stage, with all potential outcomes open including the possibility no further enforcement action is taken

Company page: Tabcorp Holdings (TAH)

NRW Holdings awarded Tonkin Highway contract

[9:32 am] The civil contractor secured a major WA infrastructure contract from Main Roads WA, valued at $200 million.

The scope covers Tonkin Highway Grade Separations at Hale Road and Welshpool Road East, including reconstruction and widening to three lanes each way and a diamond interchange at Welshpool Road East. NRW says no material capital outlay is required for the contract.

Company page: NRW Holdings (NWH)

Zip reaffirms FY26 cash EBTDA guidance with strong US momentum

[9:28 am] Zip reaffirmed its FY26 guidance at the Macquarie Conference, with US TTV growth above 40% year-on-year and credit outcomes tracking in line with expectations.

FY26 cash EBTDA guidance reaffirmed at least $260m

US TTV growth above 40% year-on-year in April

US credit outcomes performing in line with expectations, on track to be less than 1.75% of TTV for 4Q26

All other FY26 guidance metrics reconfirmed

Company page: Zip (ZIP)

Credit Corp reaffirms FY26 NPAT guidance and upgrades lending volumes

[9:25 am] The credit and consumer lending business reaffirmed FY26 NPAT guidance, while upgrading gross lending and refining ledger investment to set up record earnings.

FY26 NPAT guidance reaffirmed at $100-110m

FY26 EPS guidance of $1.47-1.62 vs $1.53 ests (midpoint is ~1% ahead)

Ledger investment guidance refined to $295-330m vs prior $280-330m

Gross lending guidance upgraded to $420-430m vs prior $350-390m

On track for record earnings with investment growth to provide a platform for FY27 growth

Looking back, Credit Corp suffered a 16.7% one-day selloff after its 1H26 result (4-Feb).

First-half net profits came in flat year-on-year and ~10% below market expectations, driven by higher lending related provisioning and marketing costs. While the company reaffirmed its FY26 guidance, this implied an outsized second half performance. Increased competitive pressure in the US (lost a forward contract due to pricing) and higher Australian investments was a key concern. The stock has drifted a further 8% lower since the result. To reaffirm guidance does seem like a net positive at this point in time?

Company page: Credit Corp Group (CCP)

Orica 1H26 NPAT beats with strong dividend lift and bullish FY26 outlook

[9:16 am] The explosives major delivered an 8% lift in NPAT pre-SI ahead of consensus, with all segments and regions guided to higher underlying EBIT for FY26 and minimal Middle East exposure flagged.

Revenue down to $3.88bn vs $4.05bn ests (4% miss)

EBITDA up to $761.4m vs $756.3m ests (1% beat)

EBIT up 5% to $512.0m vs $497.4m ests (3% beat)

NPAT (pre-significant itemes) up 8% to $283.1m vs $271.4m ests (4% beat)

Interim dividend up 14% to 28.5 cps (unfranked) vs 27.0 cps ests (6% beat)

Return on Net Assets of 14.7% (vs 13.1% pcp), highest in 13 years

Leverage at 1.53x within target range and $500m on-market buy-back completed in full

FY26 outlook: Underlying EBIT expected to increase across all segments and all regions vs pcp, not experiencing material constraints from Middle East conflict as products generally not transported through Strait of Hormuz, organisation-wide program underway targeting at least $100m enduring cost base reduction

Company page: Orica (ORI)

PlaySide upgrades FY26 revenue guidance

[9:09 am] The game developer lifted FY26 revenue guidance, driven by stronger-than-expected sales of Mouse: P.I. for Hire and recouped publishing costs.

FY26 revenue guidance lifted to $50-53m vs prior >$48.7m

Mouse: P.I. for Hire has sold ~730,000 units across all platforms since launch, with console now 50% of total units sold

Estimated gross platform sales of US$21.4m (~$29.7m) since launch, with ~US$13.0m (~$18.1m) in net revenue to PlaySide

Publishing milestone payments, publishing and marketing costs have now been fully recouped, supporting meaningful near-term cash inflows

Company page: PlaySide Studios (PLY)

Sezzle Q1 beats and lifts FY26 guidance

[9:07 am] Sezzle hasn't been listed on the ASX since early 2024 but its quarterly result may provide a read-through for local names like Zip and Block. The BNPL platform delivered a sizeable beat across revenue and earnings, with record purchase frequency and strong subscriber growth driving guidance upgrades across all metrics. Sezzle shares surged 13.3% in after hours.

Revenue up 29.2% to $135.5m vs $127.7m ests (6% beat)

Adj. net income up 41.5% to $50.0m vs $43.8m ests (14% beat)

Adj. EPS of $1.43 vs $1.20 ests (19% beat)

GMV up 37.3% to $1.1bn, with record average quarterly purchase frequency of 7.1x

FY26 guidance upgraded to:

Revenue growth +30-35% (prior +25-30%)

Adj. net income $180m (prior $170m) vs $168.8m ests (6.6% beat)

Adj. EPS $5.10 (prior $4.70) vs $4.70 ests (9% beat)

Amcor Q3 earnings call takeaways

[9:02 am] Management framed minimal direct conflict exposure, reaffirmed synergy targets and signalled elevated inventory through Q4 with deleveraging deferred to FY27.

Less than 5% of resin sourced from the Middle East, with no material impact from the conflict on Q4 FY26 earnings

Synergy targets reaffirmed at $650m over three years, with procurement and growth synergies tracking ahead of plan into FY27

Inventory levels to remain elevated through Q4 FY26 to secure supply continuity, with FCF normalisation hinging on supply chain normalisation in late 2026

Year-end leverage projected at 3.4-3.5x, deleveraging toward sub-3x targeted in FY27 via cash flow and asset sales

Core focus categories outperforming the broader business, with healthcare volumes slightly down on weather and market factors but positive mix trends

Company page: Amcor (AMC)

Amcor Q3 in line with EPS beat, narrows FY26 guidance on Middle East conflict

[8:58 am] Q3 results were resilient as Berry synergies tracked at the upper end of expectations, though FY26 free cash flow was materially cut to reflect higher inventory needed to secure customer service levels amid the Middle East conflict.

Revenue up 77% to $5.91bn vs $5.71bn ests (4% beat), driven by the Berry acquisition

Adj. EBITDA up 87% to $892m vs $928.1m ests (4% miss)

Adj. EBITDA margin 15.1% vs 14.3% pcp

Adj. EPS up 6% to $0.96 vs $0.95 ests (1% beat)

Q3 acquisition synergies of $77m, at upper end of expectations

FY26 adj. EPS guidance narrowed to $3.98-4.03 vs prior $4.00-4.15 and $3.94 ests, midpoint implies ~12% growth and includes Berry synergies of $270m

FY26 free cash flow guidance cut to $1.5-1.6bn vs prior $1.8-1.9bn and $1.76bn ests, reflecting higher inventory levels at higher cost to secure customer service amid the Middle East conflict

NYSE-listed Amcor shares rallied 6.8% overnight.

Company page: Amcor (AMC)

Super Retail Group trading update flags Middle East impact and higher costs

[8:54 am] Group sales growth slowed in H2 with all brands hit by Middle East conflict-driven fuel pressures, while group costs guidance was lifted on accelerated project spend.

Group total sales up 3.3% year-on-year for the first 44 weeks of FY26

Group H2 LFL sales up 0.4% (weeks 27 to 44), with Supercheap Auto +1.6%, rebel +1.4%, BCF -3.3% and Macpac +2.5%

Brand total sales growth (weeks 1 to 44): Macpac +8.9%, Supercheap Auto +4.3%, rebel +4.0%, BCF -0.3%

Group gross margin H2 FY26 to date modestly below pcp, with sales momentum adversely affected by Middle East conflict, higher fuel prices, rising interest rates and fuel availability concerns, most pronounced over Easter

~$30m strategically invested in additional working capital to secure inventory ahead of pending price increases, most notably in Supercheap Auto

FY26 Group and unallocated costs guidance lifted to $66m (prior $60m), reflecting early commencement of projects previously targeted for FY27

Super Retail has been trending lower since August last year, down 27% year-to-date and trading at the lowest since October 2023.

This update was announced after market close on Wednesday, with E&P downgrading the stock this morning from Positive to Neutral and an aggressive target price cut from $17.50 to $13.80.

Company page: Super Retail Group (SUL)

Amotiv reaffirms FY26 guidance with Q3 trading update

[8:52 am] The auto parts supplier reaffirmed its FY26 underlying EBITA guidance, flagging soft 4WD conditions and largely manageable Middle East impacts to date.

YTD group revenue up 3.6% year-on-year to 31 March

FY26 underlying EBITA reaffirmed at ~$195m vs $194.4m ests (in line)

FY26 revenue growth expected, in line with consensus +3.7%

4WD remains soft with new vehicle sales in Q3 weaker than H1

Lightening, Power and Electrical seeing record H2 sales in US and Europe but ANZ resellers subdued

Powertrain, wear and repair resilient though some workshops reporting softer forward bookings

Early upward price pressure on petroleum-linked raw materials and sea freight premiums from Middle East conflict

Amotiv shares are down 29% year-to-date and trading slightly above recent lows (which marked the lowest since Feb 2016).

Company page: Amotiv (AOV)

Trump threatens higher-intensity bombing as US-Iran near 14-point memo

[8:46 am] Tensions remain elevated despite reported progress on a framework deal, with Trump warning of escalated strikes if Iran rejects the proposal.

Trump said Operation Epic Fury "will be at an end" if Iran agrees to terms, but bombing will resume "at a much higher level and intensity" if no deal

US and Iran reportedly close to a one-page 14-point MOU that would end the war and establish a framework for further negotiations, with Tehran's response on key points expected within 48 hours

Memo terms include Iran committing to a moratorium on nuclear enrichment, US lifting sanctions, and both parties retreating from controls on Hormuz ship transits

A US naval blockade of Iranian ports would be lifted under a deal, allowing Hormuz to be "OPEN TO ALL," with stocks rallying and oil falling on the news

Tech megacaps reaching the limit of carrying the market

[8:43 am] The narrow leadership of Big Tech is approaching a tipping point, according to Bloomberg.

Nasdaq 100 up over 20% and S&P 500 ~15% from March lows, but median stock still ~13% below its 52-week high and only 23% of S&P 500 members beat the index in the April rally

Average 12-month drawdown after this level of narrow breadth is ~10% since 1980, according to Goldman Sachs

Q1 earnings surprise for six of the Mag 7 was 12.5% with all posting double-digit growth

All 11 S&P sectors on track to show positive year-on-year earnings growth for first time in over four years

Real-economy spillover already showing in Apple's higher memory cost warning, Colgate-Palmolive's US sales concerns and Norwegian Cruise Line's lower 2026 guidance

Source: Bloomberg

US-Iran moving closer to one-page memo to end war

[8:39 am] The two sides are nearing a framework agreement that would end the nearly 10-week conflict, with Trump saying the war has "a very good chance of ending".

US and Iran moving closer to agreement on one-page MOU that would declare end of conflict and trigger 30-day period to resolve nuclear demands, unfreeze Iranian assets and negotiate Hormuz security

Deal would lead to gradual reopening of Strait of Hormuz and lifting of US blockade on Iranian ports, with Trump saying war could end "in as soon as a week"

Potential terms include Iran shipping enriched uranium stockpile to US and pledging not to operate underground facilities

Iran still reviewing latest US proposal with response to be conveyed via Pakistani mediators, while Trump threatened resumption of bombing if no deal

IRGC Navy said safe passage through Hormuz possible under "new procedures," though US military disabled an Iranian-flagged tanker in the Gulf of Oman

AMD CEO flags server CPU TAM doubling and lifts long-term EPS target

[8:36 am] Lisa Su's commentary reinforced the structural AI capex thesis, with bullish multi-year guidance on data centre AI revenue, server CPU growth and earnings power. Here are a few interesting quotes from the earnings call.

“Based on the demand signals we are seeing today and the structural increase in CPU compute requirements driven by agentic AI, we now expect the server CPU TAM to grow at greater than 35% annually, reaching over $120 billion by 2030.”

“It’s happening at a much faster pace … we’re seeing significantly more CPU demand from really every major cloud provider, as well as enterprise customers.”

“We have strong and increasing confidence in our ability to deliver tens of billions of dollars in annual data centre AI revenue in 2027 and to exceed our long-term growth target of greater than 80% in the coming years.”

“With the momentum we are seeing across the business and the expanding market opportunity, we see a clear path to exceed our long-term financial targets, including delivering more than $20 in EPS over the strategic time frame.”

AMD soars 18% on Q1 earnings beat and guidance upgrade

[8:32 am] The chipmaker delivered a sizeable beat on revenue and EPS with data centre now the primary growth engine, while Q2 guidance came in well ahead of consensus on accelerating AI infrastructure demand. AMD shares surged 18.6% to all-time highs, adding just over US$100 billion in market cap.

Revenue up 38% to $10.25bn vs. $9.89bn ests (4% beat)

Adj. EPS of $1.37 vs. $1.28 ests (7% beat)

Data Centre revenue up 57% to $5.8bn vs. $5.6bn ests (4% beat)

Adj. gross margin of 55%, in line with ests and up 1ppt year-on-year

Q2 revenue guide of $11.2bn (+/- $300m) vs. $10.52bn ests (6% beat), implying ~46% year-on-year growth at midpoint

Q2 adj. gross margin guide ~56% vs. 55.25% ests

S&P 500 and Nasdaq at all-time highs on AI tailwind and Iran de-escalation hopes

[8:26 am] US equities ended near best levels with semis the standout, as risk-on sentiment was driven by progress on a US-Iran deal and reinforced AI capex demand commentary.

S&P 500 (+1.46%), Nasdaq (+2.02%) and Russell 2000 (+1.47%) at fresh all-time highs

Brent down 7.5% to US$101 on hopes of a 14-point US-Iran MOU framing next round of talks, though Iranian response leaning cautious and Trump threatening return to bombing if no agreement

AI narrative reinforced by AMD demand commentary, Anthropic deals with Alphabet and SpaceX, and Nvidia-GLW partnership

Good morning!

[8:10 am] ASX 200 futures are up 95 pts (+1.08%) as of 8:10 am AEST.

The overnight session in a nutshell:

US benchmarks closed at fresh records, after Axios reported the US and Iran are nearing a 14-point memorandum to end the war, with Trump pausing the "Project Freedom" Hormuz escort mission to allow space for a deal

Oil tumbled, with Brent down nearly 8% as the prospect of a peace deal triggered the second sharpest sell-off in the energy complex since the Iran war began

Strong comeback session for commodities, copper surged 3.4% to US$6.19/lb and close to record highs

AMD ripped 18% to a record high after Q1 FY26 earnings smashed expectations