ASX 200 Live Today - Thursday, 28th May

The S&P/ASX 200 is set to fall after a weak overnight session for commodities and miners. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Thursday, May 28. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

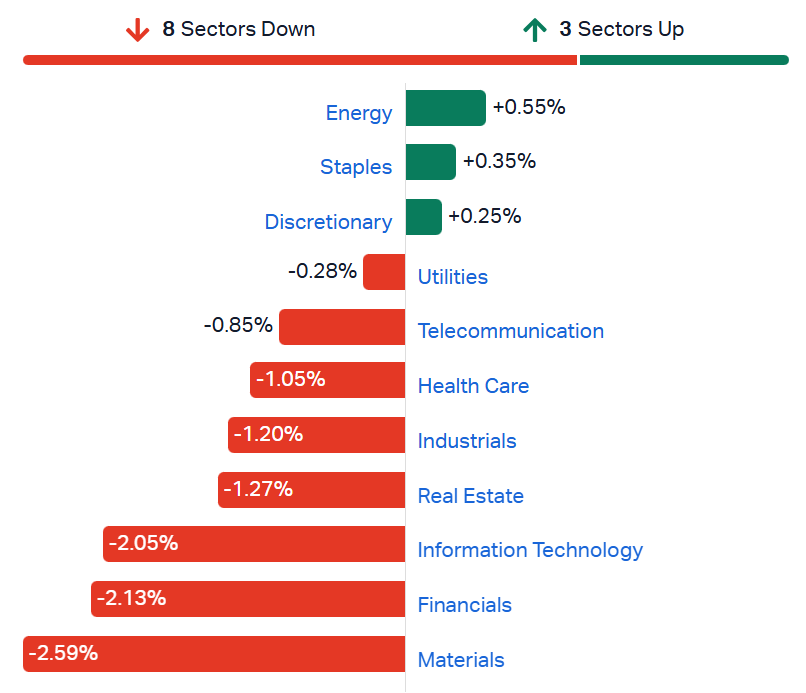

Banks, miners and tech tumble more than 2%

[2:12 pm] That's all for today. What an ugly session, with Banks, Miners and Tech all down more than 2%, and the Emerging Companies index down 2.5%.

S&P/ASX 200 sectors (Source: TradingView)

Markets are weighing fresh escalation after US airstrikes on Iran and new sanctions on the Persian Gulf Strait Authority, with Brent up 2.9% to $95.55 a barrel and Asian equities pulling back from record highs.

US Central Command struck an Iranian drone-launching unit in Bandar Abbas and shot down four one-way attack drones fired at a commercial ship, with officials framing the action as defensive and consistent with last month's ceasefire

US Treasury sanctioned Iran's Persian Gulf Strait Authority, which has been demanding payments of up to $2m for safe passage as Iran asserts expanded jurisdiction over the waterway

With no accord in sight, commodities are trading broadly lower, with notable declines for silver (-3.1%), gold (-1.7%), palladium (-1.7%) and copper (-1.2%). S&P 500 and Nasdaq futures currently down 0.38% and 0.83% respectively.

Gold stocks sharply lower

[1:47 pm] A rough day for gold miners, with the S&P/ASX All Ords Gold index down 7.1% to the lowest since 26 March.

Gold is currently down 1.8% to US$4,374/oz and trading right on its 200-day moving average. A close at these levels will mark the first beach of the key 200-day since October 2023.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

PRU | Perseus Mining | -9.1% | $4.89 | -11.3% |

RSG | Resolute Mining | -8.9% | $1.18 | -4.1% |

GMD | Genesis Minerals | -8.7% | $5.66 | -20.9% |

WGX | Westgold Resources | -8.3% | $4.79 | -24.0% |

AMI | Aurelia Metals | -8.1% | $0.29 | 16.3% |

ALK | Alkane Resources | -7.9% | $1.41 | 5.6% |

RRL | Regis Resources | -7.8% | $5.87 | -21.9% |

RMS | Ramelius Resources | -7.7% | $3.12 | -23.7% |

EVN | Evolution Mining | -7.4% | $11.70 | -6.9% |

VAU | Vault Minerals | -7.3% | $4.04 | -25.7% |

CMM | Capricorn Metals | -7.3% | $13.56 | -3.1% |

EMR | Emerald Resources | -7.1% | $5.61 | -10.7% |

BC8 | Black Cat Syndicate | -7.1% | $1.11 | -8.6% |

CYL | Catalyst Metals | -6.9% | $5.00 | -32.2% |

OBM | Ora Banda Mining | -6.9% | $1.29 | -15.7% |

NEM | Newmont | -6.8% | $146.39 | -2.5% |

NST | Northern Star Resources | -6.5% | $18.40 | -25.1% |

SBM | St. Barbara | -6.4% | $0.52 | -10.4% |

BGL | Bellevue Gold | -6.3% | $1.48 | -12.4% |

MEK | Meeka Metals | -6.2% | $0.12 | -54.8% |

PNR | Pantoro Gold | -5.9% | $2.97 | -39.5% |

Oil bounces, metals slip

[1:27 pm] Brent is currently up 2.4% to US$95.12 a barrel, but still down ~14% in the last seven sessions.

The bounce is driving most commodities lower, with gold down 1.59% to US$4,385/oz and within ~0.5% of its 200-day moving average.

Gold daily price chart (Source: TradingView)

Elsewhere, silver is down 2.5% to US$72.7/oz, platinum down 1.4% to US$1,899/t, copper down 0.69% to US$6.21/lb and iron ore futures trading fractionally lower at US$108.70.

Analysts' take on Eagers Automotive

[1:15 pm] Eagers Automotive's AGM trading update on Wednesday came in below market expectations, with 1H26 underlying PBT for the ANZ business guided to be in line with or slightly ahead of last year against consensus positioned for low double-digit growth. The stock dipped as much 12.8% but managed to finish the session 1.8% higher.

Analysts flagged a material second half skew supported by CanadaOne's full six-month contribution, improved Toyota supply and BYD deliveries, though concerns centred on margins, FX headwinds and demanding FY26 consensus expectations.

Jarden downgraded to Neutral from Overweight, lowered target from $25.25 to $23.90, citing H1 PBT guidance materially below consensus, disappointing margins despite accelerating EV sales, lower CanadaOne forecasts on softer Canadian sales and AUD/CAD headwinds, and caution on NEV demand sustainability with FY26 consensus setting a high hurdle.

Morgans retained Buy, lowered target from $30.00 to $27.25, viewing AGM guidance as mixed with OEM supply constraints weighing on H1, guidance potentially conservative given key May and June trading months, structural growth supporting the medium-term thesis, and recent share price weakness as a compelling buying opportunity.

Bell Potter retained Buy, lowered target from $29.25 to $28.75, highlighting 5% turnover growth, record order intake and strong EasyAuto123 and Carlins performance, a record consolidated H1 supported by CanadaOne with improved Toyota supply aiding H2, and modest FY26-FY28 PBT downgrades on lower revenue, FX and interest cost assumptions.

Household spending falls 1.1% in April as transport costs slide

[12:40 pm] ABS data shows the conflict in the Middle East drove a 4.7% drop in transport spending in April, while annual household spending growth slowed to 4.9% from 6.2% in March.

Household spending down 1.1% in April, following a 1.6% rise in March and 0.3% rise in February

Transport the main drag, with air travel the largest contributor as households scaled back trips and airlines cancelled routes amid higher jet fuel costs

Federal Government halved the fuel excise duty from 1 April, helping ease fuel spending versus March, though levels remain elevated relative to pre-conflict

Experimental ABS data shows fuel volumes rose 2.0% in April after a 1.5% fall in March, with EV sales lifting materially as households adjust to higher fuel prices

Food spending down 1.3%, reflecting a normalisation from March and continued shift towards generic brands and cheaper supermarket products

Private capex jumps 6.5% in March quarter as data centre spend surges

[12:39 pm] Data centre equipment, particularly server racks and processing gear, drove the lift in March quarter capex, according to the latest ABS data.

Private new capex up 6.5% in the March quarter, taking the annual rise to 14.6%

Non-mining business investment up 8.8%, while mining was broadly flat

New equipment and machinery investment at a record high, up 18.1%, driven by non-mining (+20.1%) and specifically information media and telecommunications (+196.1%); mining equipment also up 7.2%

Buildings and structures down 3.8% as large manufacturing, utilities and mining projects completed, though data centre construction within info media and telecoms rose for the seventh straight quarter (+12.6%)

NSW (+22.1%) and Victoria (+12.7%) led state gains, capturing the bulk of data centre investment

Source: ABS

Endeavour makes a second straight day of record lows

[12:37 pm] Endeavour dipped as much as 5.4% this morning, now down 3.2% to $2.84. The stock is now down 8% in the last two sessions and down 22.2% year-to-date.

On Wednesday, Endeavour's Investor Day presentation revealed a material strategy shift:

$300m of cost savings targeted by FY29, including $100m in FY27, as part of the three-year transformation program

Group exiting the majority of its existing winery and vineyard portfolio, including Chapel Hill, Oakridge and Josef Chromy, with Pinnacle Drinks repositioned to back Retail and high-performing brands

Targeted dividend payout ratio revised to 50-75% of group underlying NPAT (from prior policy) to fund growth investment

Capital deployment in Hotels to lift, with light touch renewals, refurbishments and whole-of-venue repositionings

Yesterday's blog post noted: "The main concern here should be the dividend policy change, as Endeavour has historically maintained a payout ratio around 70-80%. UBS modelling (May-26) expected this trend to continue well into FY30, which implies a yield of around 4-5%. The revised range could result in some dividend uncertainty, and drive some selling pressure from income-oriented holders."

Banks broadly lower

[12:33 pm] Most major banks down around 1% at noon, with the broader S&P/ASX 200 Financials Index down 1.5%.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

ANZ | ANZ Group | -1.7% | $34.96 | -4.1% |

BEN | Bendigo & Adelaide Bank | -1.5% | $10.25 | -3.2% |

CBA | Commonwealth Bank | -1.5% | $162.31 | 1.1% |

NAB | National Australia Bank | -1.5% | $37.20 | -12.0% |

WBC | Westpac | -1.4% | $35.87 | -6.8% |

BOQ | Bank Of Queensland | -1.4% | $6.18 | -5.8% |

MQG | Macquarie Group | -0.8% | $234.36 | 15.4% |

JDO | Judo Capital | -0.2% | $1.39 | -21.8% |

SiteMinder rallies on Powered platform launch

[12:30 pm] SiteMinder is opening its distribution engine to third-party hospitality platforms, starting with a deepened Mews partnership, though no material FY26 financial impact is expected. The stock is currently up 9.2%.

Mews will integrate SiteMinder's distribution engine natively as "Mews Channel Manager - Powered by SiteMinder", including Channels Plus, Demand Plus and Dynamic Revenue Plus products

Existing joint SiteMinder-Mews customers expected to transition to the integrated experience over coming months

No material financial impact expected in FY26, but management flags incremental long-term revenue from expanded hotel reach, higher adoption of transaction and commerce products, and deeper software integration

CEO Sankar Narayan: "As those workflows become more automated, the infrastructure connecting hotel systems, distribution channels and commerce capabilities becomes more valuable"

Company page: SiteMinder (SDR)

Analysts' take on Web Travel Group

[11:15 am] WEB's FY26 result modestly beat expectations on Wednesday, with a standout 2H26 TTV margin driven by the shift toward directly contracted hotel inventory and AI-led dynamic pricing, though management withdrew its B2B EBITDA margin target citing Middle East conflict uncertainty. The stock closed 2.1% higher on the day.

RBC Capital Markets retained Outperform, target unchanged at $6.00, highlighting the standout 2H26 TTV margin uplift, structural margin gains from AI pricing and direct contracting, Middle East exposure as a material near-term headwind, an inexpensive valuation capped by earnings uncertainty, and WEB's role as essential infrastructure in an AI-driven travel environment.

JPMorgan retained Overweight, lowered target from $6.00 to $4.85, citing an FY27 guidance reset that was not unexpected given peer commentary, confidence in the TTV margin trajectory despite macro headwinds, Americas and Europe tracking in line, Middle East resolution as a potential material re-rating event, and a more challenging FY30 TTV target on a rebased growth trajectory.

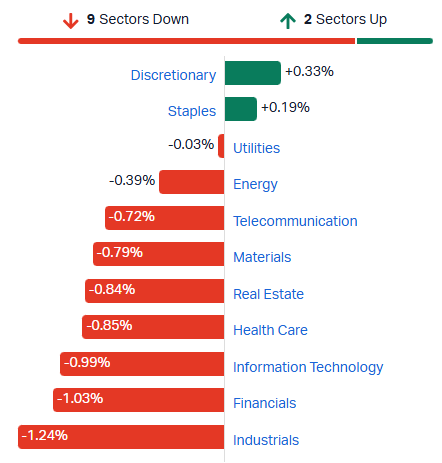

ASX 200 lower amid broad weakness

[11:12 am] A weak day for markets, with the S&P/ASX 200 down 0.74% and only two sectors trading slightly higher. Things are more downbeat beneath the surface, with 151 constituents (76%) in the red.

S&P/ASX 200 sectors (Source: TradingView)

Analysts' take on Endeavour

[10:47 am] Endeavour Group's first strategy day since December 2023 outlined a transformation plan centred on extended cost-out programs, accelerated hotel renewals, and reestablishing retail liquor price leadership, with management acknowledging that prior strategy had prioritised margin over customers. Shares closed down 4.9% on the day and fell a further 4.8% today.

Jarden retained Underweight, lowered target from $3.20 to $3.10, noting the strategy day was light on detail but flagging underutilised assets, an extended cost-out program alongside rising capex, a wider dividend payout ratio, and a less negative stance as value emerges.

JPMorgan retained Underweight, lowered target from $3.10 to $3.00, citing cost-out as necessary to offset operating deleverage and gross margin pressure, further retail liquor earnings declines, a payout ratio reduction driven by capital intensity, and limited clarity on cost allocation between segments.

UBS retained Neutral, lowered target from $3.45 to $3.25, highlighting the cost savings program and lower near-term capex guidance, a revenue-led focus on retail fundamentals and market share recapture, accelerating hotel renewals via a repeatable model, with the target cut reflecting elevated capex flowing through to depreciation.

Analysts' take on Nufarm

[10:44 am] Nufarm delivered 1H26 underlying EBITDA broadly in line with guidance on Wednesday, with analysts viewing the result as a genuine earnings inflection point underpinned by crop protection stabilisation, narrowing Omega-3 losses, and credible execution on $100 million in cost-out programs across FY26-FY28. Shares closed 13.7% higher on the day.

UBS upgraded to Buy from Neutral, raised target from $2.80 to $3.50, citing sustainable crop protection margins, an Omega-3 and hybrid seeds-led emerging platforms beat, and stronger FY27-28 earnings growth potential as cost programs outpace inflation.

RBC Capital Markets upgraded to Outperform from Sector Perform, raised target from $3.40 to $3.60, highlighting the capital efficiency pivot toward returns over volume, credible progress on dual cost programs, leverage tracking toward ~2x by year end, and improving ROIC from higher-margin mix.

Bell Potter retained Buy, target unchanged at $3.60, noting strong seeds revenue growth from hybrids and emerging platforms, solid cost program execution, positive FCF supporting the balance sheet, and a persistent valuation discount despite strategic progress.

Top All Ords gainers and losers

[10:19 am] HealthCo is rallying off a private hospital agreement, Galan Lithium proceed its first lithium chloride at its flagship Hombre Muerto West project, while Select Harvest rallies on a solid 1H26 result. Meanwhile, gold names dominate the top decliners list.

Ticker | Company | % Chg | Price |

|---|---|---|---|

HCW | Healthco Healthcare & Wellness REIT | 13.74% | $0.75 |

GLN | Galan Lithium | 12.64% | $0.49 |

SHV | Select Harvests | 12.15% | $4.06 |

SDR | Siteminder | 10.26% | $3.33 |

JHX | James Hardie | 5.37% | $31.57 |

VUL | Vulcan Energy Resources | 5.34% | $3.75 |

CNI | Centuria Capital Group | 5.26% | $1.90 |

PPC | Peet | 5.02% | $1.68 |

HGH | Heartland Group | 4.52% | $0.93 |

NUF | Nufarm | 4.47% | $3.04 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

APE | Eagers Automotive | -7.03% | $21.16 |

AGI | Ainsworth Game Technology | -6.67% | $1.40 |

USL | Unico Silver | -5.60% | $0.59 |

ALK | Alkane Resources | -5.57% | $1.44 |

DTR | Dateline Resources | -5.41% | $0.18 |

WIA | Wia Gold | -5.15% | $0.46 |

RSG | Resolute Mining | -5.04% | $1.23 |

WGX | Westgold Resources | -4.98% | $4.96 |

EMR | Emerald Resources | -4.97% | $5.74 |

KCN | Kingsgate Consolidated | -4.89% | $6.23 |

Top ASX 200 gainers and losers

[10:16 am] Quite a few CDIs have topped the leaderboard this morning (JHX, XYZ, AMC, NWS), while the biggest fallers consists mostly of gold miners.

Ticker | Company | % Chg | Price |

|---|---|---|---|

JHX | James Hardie | 5.31% | $31.55 |

SRL | Sunrise Energy Metals | 2.75% | $15.71 |

XYZ | Block | 2.50% | $99.55 |

GNP | Genusplus Group | 2.28% | $10.33 |

AMC | Amcor | 2.24% | $55.05 |

MCY | Mercury Nz | 2.15% | $5.70 |

SGM | Sims | 2.11% | $25.60 |

NWS | News Corp | 2.04% | $42.58 |

MEZ | Meridian Energy | 1.69% | $4.82 |

FLT | Flight Centre | 1.62% | $10.04 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

APE | Eagers Automotive | -6.90% | $21.19 |

RSG | Resolute Mining | -5.27% | $1.22 |

EDV | Endeavour Group | -5.12% | $2.78 |

ALK | Alkane Resources | -4.92% | $1.45 |

WGX | Westgold Resources | -4.79% | $4.97 |

NEM | Newmont | -4.74% | $149.67 |

EMR | Emerald Resources | -4.64% | $5.76 |

RMS | Ramelius Resources | -4.44% | $3.23 |

PRN | Perenti | -4.25% | $2.03 |

RRL | Regis Resources | -4.24% | $6.10 |

Peet upgrades FY26 NPAT guidance to $98-100m on strong WA and QLD demand

[9:58 am] Peet has lifted FY26 NPAT guidance to $98-100 million from $86-90 million, implying 67-71% earnings growth on FY25, driven by continued strength across Western Australia and Queensland.

Revised guidance reflects sustained elevated demand, with Peet accelerating its construction program to bring product to market sooner than expected

Strong demand in key markets has underpinned both price growth and consistent sales volumes through FY26

Company continues to target growth in FY27, supported by its established pipeline and contracts on hand

Population growth and constrained housing supply remain supportive, though management is monitoring the impact of interest rate rises, cost of living pressures and broader macro risks

Peet shares are flat in the last twelve months, though down 19.4% year-to-date.

Company page: Peet (PPC)

Select Harvests lifts underlying NPAT 33%, declares dividend and launches buy-back

[9:55 am] Select Harvests reported underlying NPAT up 33%, declared an interim dividend and announced an on-market buy-back of up to 10% of issued capital.

Revenue down 43% to $59.0m on lower carryover crop and a late harvest from wet weather

EBITDA down 6% to $59.0m

Reported NPAT down 7% to $26.6m

Underlying NPAT up 33% to $29.1m

Interim dividend of 3.5 cps fully franked, versus nil in HY2025

2026 crop forecast at 29,500Mt (range 28,000-31,000Mt), around 18% larger than 2025, with external grower volumes more than doubling to an estimated 15,400MT

Almond price of $10.21/kg, broadly flat on the $10.18/kg achieved in FY2025

Net debt up to $182.6m from $168.2m on crop investment, with facilities increased $60m to $300m at lower cost and extended tenure

Board set new growth targets of 65,000Mt and $700m revenue by 2030, with the buy-back reflecting the view that the current share price does not reflect intrinsic value

I don't have any consensus data handy (newest is ~6 months old). SHV shares are down 27% year-to-date and down 20% in the last twelve months.

Company page: Select Harvests (SHV)

Airlines trade higher on lower oil prices

[9:50 am] The US Global Jets ETF gained 2.9% overnight and now up 17.2% in the last five sessions as oil prices continued to edge lower.

This ETF largely consists of US airlines like Delta, American Airlines, United Airlines etc, but also holds a mix of global airlines like Qantas, Latam Airlines, Air France etc. It's a useful barometer for the travel/airline industry.

NYSE-listed Global Jets ETF (Source: TradingView)

Similarly, Qantas is up 9.9% in the last five sessions and on the cusp of breaking above its recent trading range.

Qantas daily price chart (Source: TradingView)

Oil dips to a six-week low

[9:44 am] Oil prices fell overnight despite Trump saying the US is "not satisfied" with Iran negotiations and Iranian hardliners pushing back on ceding control of the Strait of Hormuz or making nuclear concessions.

Brent daily price chart (Source: TradingView)

Gold stocks set to fall

[9:38 am] A fairly rough overnight session for gold, with prices down 1.13% to a one-month low of US$4,455/oz.

Gold price chart (Source: TradingView)

This drove the NYSE-listed VanEck Gold Miners ETF down 3.4%, with a bellwether name like Newmont down 3.9% to US$107.23 (which implies a ~4.3% drop for ASX-listed Newmont shares).

Advanced Innergy reaffirms FY26 guidance on record $239m orderbook

[9:35 am] Advanced Innergy delivered a softer first half due to second half revenue weighting but reaffirmed full-year guidance, supported by a record orderbook up 33% year-on-year.

Revenue down 2.4% to $157.9m vs $166.5m ests (5% miss), reflecting project delivery scheduling

Underlying EBITDA down 9.6% to $24.7m, weighed by H2 revenue skew and higher base operating and listed company costs

Gross margin up 11.4 percentage points to 36.8%, driven by operational efficiencies and a higher-margin contribution from Ovun

Record orderbook of $239m as at 31 March 2026, up 33% on the prior year

FY26 guidance reaffirmed at revenue of $387.9m vs $380.3m ests (2% beat) and underlying EBITDA of $62.3m vs $61.5m ests (1% beat), excluding any M&A contribution

Post the proposed Matrix Composites acquisition (targeted July 2026), AIH expects to remain within its 2.0x net leverage covenant with headroom for further M&A

Company page: Advanced Innergy Holdings (AIH)

ACL appoints Greg Horan as new Group CEO

[9:31 am] Australian Clinical Labs has appointed Greg Horan as Group CEO and Executive Director, succeeding Melinda McGrath who steps down after 10 years in the role.

Horan joins on 1 June 2026 as Group CEO-elect, with the formal CEO transition effective 31 August 2026

Most recently CEO of Healthscope, where he led 20,000 employees and 5,000 visiting medical officers across 43 hospitals through the post-COVID industry transition

Company page: Australian Clinical Labs (ACL)

IPH names Tony O'Malley as new CEO from 1 July

[9:18 am] IPH has appointed Tony O'Malley as Managing Director and CEO effective 1 July 2026, succeeding Dr Andrew Blattman who flagged his retirement in November 2025.

O'Malley joins from PwC where he most recently led the Global Legal Business Solutions team, a market-facing legal services business operating across more than 100 territories with around 4,000 employees

Prior senior roles include Managing Partner at King & Wood Mallesons and Deputy General Counsel at Telstra, bringing more than 30 years of professional services experience

Blattman will remain to support the transition until 30 November 2026, capping a 30-year career with the group and nine years as CEO

Company page: IPH (IPH)

SHAPE acquires APS for up to $29m

[9:13 am] SHAPE Australia has entered a binding agreement to acquire vertically integrated retail shopfitter APS, expanding its programme-based capability and lifting its margin profile.

Upfront consideration of $20.4m ($17.4m cash plus $3m scrip), implying around 3.8x future maintainable EBITDA of $5.3m

Up to $9m in contingent consideration payable over a two-year earn-out (50% cash, 50% scrip), with total consideration capped at $29.4m

APS delivered FY25 revenue of $32.5m, with around 80% of projects valued below $500,000, reflecting strong exposure to repeatable retail rollout work

Expected to deliver normalised EPS accretion of approximately 5-7% in the first full year of ownership and be margin additive

Adds a 5,000sqm Melbourne manufacturing facility with spare capacity, plus a 20-year offshore procurement footprint, complementing SHAPE's recently acquired Arden Fitout business

SHAPE has seen its shares soar 15% year-to-date and 116% in the last twelve months off the back of strong contracting activity and backlog growth. The stock now has a market cap of $591 million, though an acquisition at a relatively undemanding 3.8x multiple for 5-7% EPS accretion sounds very good at face value.

Company page: SHAPE Australia (SHA)

AGL Energy taps private capital for 1.7GW wind farm portfolio worth up to $5bn

[9:10 am] AGL is selling majority stakes in three wind farms totalling 1.7GW under Project Constellation, with Macquarie Capital and Bank of America running the process and non-binding bids due late next month, the AFR reports.

Portfolio includes the 831MW Pottinger wind farm and battery in South Australia, the 600MW Hexham wind farm in Victoria and the 304MW Barn Hill wind farm, with potential value of up to $5bn

Pottinger is a 50-50 JV with Someva Renewables (also for sale), while AGL owns 100% of the other two assets

AGL will develop projects to "notice to proceed" stage before selling into an investment vehicle at a pre-agreed valuation, retaining a minority stake and offtake rights

Company page: AGL Energy (AGL)

Mayfield Group placed in $30m line trade by Nightingale Partners

[9:09 am] Bell Potter was offering 10m Mayfield Group shares after market close, representing 8.6% of the $351m specialist engineering group, with private equity holder Nightingale Partners understood to be the seller, according to the AFR.

Block worth around $30m being shopped to investors post-close

Nightingale Partners is Mayfield's largest holder with 40.8m shares and has held the position since 2012, with board representation via chairman Lindsay Phillips

Nightingale brought Mayfield to the ASX in 2020 via a reverse takeover of shell company Stream Group

Mayfield designs and manufactures electrical and telecommunications infrastructure for the energy, mining, data centre and defence sectors, including switchboards and modular substations. The stock is flat year-to-date but up 185% in the last twelve months.

Source: AFR

Hartnett flags AI bubble as biggest since the railroads

[9:07 am] BofA's Michael Hartnett likens the AI-driven rally to historic speculative manias, but argues investors are unlikely to sell aggressively until a marquee IPO cycle and a clear Fed tightening shock materialise.

AI mega-caps now dominate market concentration, with the bubble exceeding past railroad, Japan and dot-com episodes by some metrics

Long-end bond yields flagged as the key warning signal, with rising global cost of capital seen as dangerous for leveraged consumers, private equity, housing and EM

Stress signals flashing across weak Asian currencies (KRW, JPY, INR, IDR), widening high-yield spreads, EM outflows and BofA's Bull & Bear Indicator hitting a contrarian "sell"

Historical pattern shows speculative IPO waves (Alibaba, NTT, Visa) typically marked medium-term tops rather than immediate crashes

Gains remain narrow as a "wealth effect, not wage effect", with equal-weight consumer stocks lagging the S&P 500

Structurally bullish on EM and commodities, with preferred post-bubble plays in consumer names and smaller AI adopters rather than mega-cap platforms

London client feedback summed up as "long and paranoid", with the view that "fear in bonds is nowhere near as strong as greed in equities"

Snowflake beats and raises on AI-driven product revenue acceleration

[9:05 am] Snowflake delivered its strongest sequential dollar growth ever in Q1, with product revenue up 34% and full-year guidance lifted on AI momentum and a new $6bn AWS agreement.

The stock is up 35% after hours on the NYSE, a potentially positive read through for local software stocks.

Revenue up 33% to $1.39bn vs $1.32bn ests (5% beat)

Product revenue up 34% to $1.33bn, described as the strongest sequential dollar growth in company history

Adjusted EPS of $0.39 vs $0.32 ests (22% beat)

RPO up 38% to $9.21bn, with net revenue retention at 126% and customers generating over $1m in TTM product revenue up 29% to 779

FY26 product revenue guidance lifted to $5.84bn (+31% growth) from $5.66bn, with non-GAAP operating margin guide raised to 13.5% from 12.5%

NZD jumps as RBNZ holds in split decision, signals hikes ahead

[9:04 am] The Reserve Bank of New Zealand held the cash rate at 2.25% on a 3-3 split decided by the governor's casting vote, with new forecasts pointing to at least two 25bp hikes before year-end.

Markets now pricing an 85% chance of a July hike and a September move fully priced

Three external committee members favoured an immediate hike on rising two-year inflation expectations, while the three RBNZ officials voted to hold given contained core inflation and wage growth

Inflation projected to accelerate to 4.2% in Q2 from 3.1% in Q1 and peak at 4.3% in Q3, well above the 1-3% target band, before returning to the 2% midpoint by Q3 2027

Growth forecasts cut materially, with annual GDP growth to March 2027 now seen at 1.4% versus 2.4% in February, and Q3 GDP growth pencilled in at just 0.2%

Source: Bloomberg

China resumes urea exports as Iran war squeezes global fertiliser supply

[8:55 am] China has issued fresh urea export quotas after a March ban, a move that could ease global fertiliser prices disrupted by the closure of the Strait of Hormuz.

Industry sources point to around 1.5m tons being allocated, though Reuters could not verify the total volume

China exported 4.9m tons in 2025, slightly below its historical 5-5.5m ton range and equivalent to roughly 10% of global urea exports

Domestic Chinese urea prices remain well below international levels, supporting the case for releasing supply offshore

India is the key beneficiary, having sourced over 40% of its urea and DAP from the Middle East last year, with importers preferring Chinese cargoes given they bypass the Strait of Hormuz

Source: Reuters

Global EV sales pass 20m in 2025 as battery electric share rebounds

[8:54 am] A pretty interesting IEA report on EV trends dropped about an hour ago. EVs hit a 25% share of global new car sales in 2025, with battery electric vehicles regaining momentum as China's slowdown was offset by a 30% surge in European volumes.

Global EV sales topped 20m, up 20% on 2024, marking the fifth straight year of around 3.5m incremental sales

Battery electric share of EV sales rose to 65%, reversing the prior two-year shift toward extended-range hybrids, which fell back below 7%

China accounted for more than 13m EV sales at a 55% market share, with growth slowing to under 20% as trade-in scheme funding was paused mid-year

European sales jumped 30% to over 4m following the step-up in EU CO2 standards, with Germany up 50% and Türkiye more than doubling to become Europe's fourth-largest EV market

US sales dipped to around 1.5m as Q4 sales fell 45% year-on-year after the OBBBA ended EV tax credits in September, though full-year share held near 10%

Global government support reached $60bn (around 7% of total EV spend, down from over 12% in 2019), with China's purchase tax exemption shifting to a 50% reduction from January 2026

Source: IEA

JPMorgan flags up to $20bn deal capacity as Dimon eyes selective M&A

[8:52 am] Jamie Dimon told a Bernstein conference that JPMorgan could deploy $10-20 billion on an acquisition over the next couple of years, which would mark the largest deal of his 20-year tenure.

Dimon framed M&A as a tool of last resort rather than a growth strategy, criticising management teams that lean on dealmaking to mask weak organic growth

Any target would need to integrate cleanly into existing operations, fit the culture and enhance core businesses, not sit as a standalone unit

JPMorgan has grown mostly organically in recent years, with the notable exception of the 2023 FDIC-assisted First Republic deal, which included a $10.6bn payment to the regulator

Prior major M&A under Dimon was largely crisis-era, including Bear Stearns and Washington Mutual's retail arm, with fintech dealmaking slowing after the $175m Frank acquisition was later exposed as a fraud

Source: CNBC

Oil slides, Trump pushes back on Iran deal timeline

[8:49 am] Brent fell 3.5% overnight on hopes for an interim US-Iran agreement to reopen the Strait of Hormuz, even as Trump said he was "not satisfied" with negotiations and the White House rejected an Iranian report on a draft deal.

Brent settled at US$92.87 a barrel and now down 16.2% since 19 March

Trump said no one nation will control the Strait of Hormuz and that the US will "watch over" the waterway, dismissing midterm pressure to rush a deal

White House labelled an Iranian state TV report on a draft MOU a "complete fabrication", which had flagged Hormuz traffic returning to normal within a month of the deal taking effect

Key sticking points include control of the strait, Iran's enriched uranium, sanctions relief and the size of frozen assets to be unfrozen, with Tehran seeking $12bn under any interim deal

Ten US companies now sit above $1tn, three of them semis

[8:44 am] Micron's breach of the $1 trillion mark lifts the US trillion-dollar club to ten names, with semiconductors now accounting for three of them as the AI capex cycle reshapes the index.

Nvidia leads at $5.15tn, followed by Alphabet ($4.66tn), Apple ($4.57tn), Microsoft ($3.07tn) and Amazon ($2.92tn)

Broadcom ($2.00tn) and Micron ($1.05tn) join Nvidia as the three semi names in the club, reflecting the concentration of AI infrastructure beneficiaries

Tesla ($1.65tn) and Meta ($1.61tn) round out the mega-cap tech cohort

Berkshire Hathaway ($1.04tn) is the sole non-tech name, sitting just above Micron at the bottom of the list

Six of the ten are direct AI plays across compute, memory, hyperscaler infrastructure and cloud, underscoring how heavily the trillion-dollar tier now skews to the AI buildout

SK Hynix and Micron hit $1tn as memory rally accelerates

[8:42 am] SK Hynix and Micron crossed the US$1 trillion market cap level as investors bet on a sustained revaluation of memory chipmakers, with HBM shortages expected to persist through 2027.

SK Hynix up 9.3% Wednesday, taking 12-month gains past 1,000% and making it the third Asian company in the $1tn club after Samsung

Micron soared 19% Tuesday, its biggest one-day move since 2011, after UBS flagged scope for the stock to double over the next year

SK Hynix controlled 57% of global HBM revenue share in Q4 2025, with Samsung at 22% and Micron at 21%

Shares still trade at around 7x one-year forward earnings vs. 27x for the Philadelphia Semiconductor Index, with some local managers eyeing up to 10x as near-term upside

SK Hynix has filed for a US ADR listing this year, which Barclays flagged as a potential catalyst alongside continued supply tightness

Source: Bloomberg

Goldman lifts S&P 500 target to 8,000 on AI-driven earnings strength

[8:41 am] Goldman Sachs joined Morgan Stanley and Deutsche Bank in calling for a 17% return on the S&P 500 this year, citing exceptional first-quarter earnings momentum.

Year-end S&P 500 target raised to 8,000 from 7,600, with the benchmark already up almost 10% year-to-date and closing at a record 7,519 on Tuesday

2026 EPS forecast lifted to $340, implying 24% growth year-on-year, with a further 13% increase pencilled in for 2027

AI infrastructure beneficiaries expected to drive roughly half of S&P 500 EPS growth this year

Valuation upside likely capped by decelerating earnings growth and macro uncertainty, with AI sentiment and rates cutting both ways

Morgan Stanley sits more bullish at 8,300, highlighting the broader sell-side re-rating underway

Source: Bloomberg

Another round of all-time highs

[8:39 am] US equities edged out fresh record closes with little directional momentum, while Brent fell 3.5% to its lowest since 17 April on fading geopolitical risk.

S&P 500 (+0.02%), Dow (+0.36%) and Nasdaq (+0.07%) notched fresh record closes, though momentum stalled for the first time in five sessions

Big tech mostly higher with Meta the standout gainer; semis weaker but memory stocks firmer, with SK Hynix in focus after Micron's $1tn market cap breach

Brent down 3.5% to US$92.87 as US-Iran tensions appeared to ease, with Trump confirming negotiations are continuing

Goldman Sachs the latest sell-side strategist to lift S&P 500 target, with AI continuing to underpin upbeat sentiment

Good morning!

[8:30 am] ASX 200 futures are down 38 pts (-0.43%)

The overnight session in a nutshell:

Dow hit a fresh record close, while the S&P 500 and Nasdaq eked out tiny gains as chip stocks paused after Wednesday’s Micron-led surge.

Brent tumbled 3.5% to a five-week low of US$92.8 after Iranian state TV reported a draft Hormuz framework deal, before the White House denied the report as a "complete fabrication".

JPMorgan's Jamie Dimon told the Bernstein conference the bank could deploy US$10-20bn on an acquisition over the next couple of years, the largest of his tenure