ASX 200 Live Today - Thursday, 22nd January

The S&P/ASX 200 is set to snap a three-day losing streak after a step-down in Trump and Greenland tensions. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Thursday, January 22. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Be sure to refresh manually for the latest updates — and let us know how we can make it even better.

ASX 200 higher but off best levels

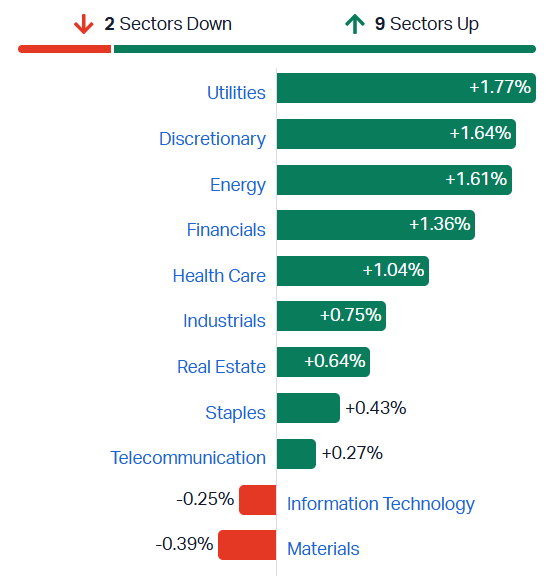

[1:55 pm] ASX 200 currently up 0.5%, down from session highs of 0.93%. The unexpectedly large fall in the unemployment rate has pushed February rate hike expectations to just under 60%, up from ~40% prior. Aussie yields are trading sharply higher, with the 10-year up 6 bps to 4.80%, within an arms reach of its 5-Jan-26 high of 4.83%. Despite growing rate hike risks, plenty of sectors are charging higher today, including:

Energy (+2.3%) is rallying off the back of Santos' Q4 report. The Energy Index is now up 8.8% since 18-Dec-25 and trading at a fresh two-month high

Discretionary (+2.2%) is bouncing from no man's land, still trading around 8-month lows and down 13% since August. Though plenty of household names sharply higher today, including Premier (+8.5%), Eagers Automotive (+4.3%), Breville (+4.0%), Aristocrat Leisure (+3.4%) and Wesfarmers (+2.0%)

Utilities (+1.5%), Healthcare (+1.3%) and Financials (+1.2%) also all up more than 1%

Lithium futures continue to bounce

[1:37 pm] Chinese lithium futures currently up 3.0% to 169,480 yuan a tonne. Prices are now 2.6% away from the recent high of 174,070 yuan and up almost 200% since the Jul-25 low of 58,400 yuan.

Canadian plays like PMET Resources (+8.2%) and Winsome Resources (+3.6%) are trading sharply higher, while local names like PLS (+1.5%), Liontown (+0.9%) and IGO (+0.5%) are nudging higher.

RBC's take on interest rates

[1:30 pm] RBC's Macro Rates Strategist Robert Thompson says the unexpected fall in unemployment "doesn't make the RBA's job any easier heading into 4Q CPI next week against a backdrop of ongoing capacity constraints across the supply side of the economy."

"We retain our base case call that the RBA will not hike rates this year, but freely admit to feeling increasingly nervous about this call. Today’s data adds further risk that the RBA will be forced into a fresh hiking cycle."

Thompson notes markets have moved pricing for a 25 bp hike in February from ~40% pre-employment data to just under 60% now.

Santos rallies on Q4 production report

[1:24 pm] Missed the Santos quarterly from this morning. The stock experienced a sizeable intraday rally, currently up 5.6% vs. 1.3% open. Q4 production was relatively in-line with expectations, with a slight revenue beat while unit costs remain well below guidance. Full-year production numbers fell short of consensus. Pikka and Barossa projects remain on track despite an increase in capex, the loading of a Barossa LNG cargo likely relieved near-term operational concerns.

Fortescue tumbles to six week low

[1:19 pm] Pretty ugly day for Fortescue (-4.2%) despite a relatively flat open. This follows a relatively weaker-than-expected December quarter report, which featured a slight miss across shipped volumes, costs and Iron Bridge performance. You can check out the numbers from the our pre-market posts below.

Fortescue daily price chart (Source: TradingView)

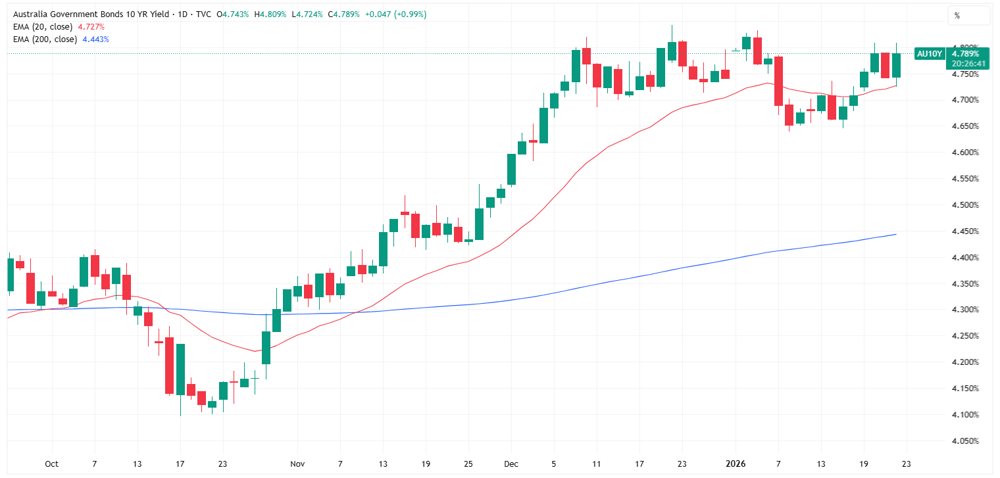

ASX 200 eases from session high, yields jump

[12:36 pm] ASX 200 was trading at session highs of 0.92% heading into the unemployment data, which triggered a sharp pullback to 0.60% by 11:38 am AEST.

The stronger-than-expected print resulted in the 10-year jumping 6 bps to 4.80%, bringing it back near recent highs of 4.84%.

Australia 10-year government bond yield daily chart (Source: TradingView)

Unemployment rate falls

[12:29 am] The unemployment rate fell to 4.1% (vs. 4.4% consensus) in December as employment surged well ahead of expectations and hours worked hit a fresh record, according to the ABS.

Employment: +65.2k actual vs. +28.3k forecast

Full-time +55k, part-time +10k

Participation rate: 66.7% and unemployed people -30k

Hours worked: +0.4%, monthly hours topped 2 billion for the first time

ABS head of labour statistics, Sean Crick said the stronger-than-expected employment gain was supported by more 15- to 24-year-olds moved into jobs, and record hours worked.

By Warren Masilamony

Banks surge +1.8%, lifting ASX 200

[11:38 am] The banks are broadly higher, led by Bank of Queensland (+5.1%) and Bendigo up (+3.3%), while the big four are also sharply higher.

Ticker | Company | % Chg | Price |

|---|---|---|---|

BOQ | Bank Of Queensland | 5.13% | $6.76 |

BEN | Bendigo & Adelaide Bank | 3.30% | $11.12 |

NAB | National Australia Bank | 2.48% | $42.20 |

MQG | Macquarie Group | 2.41% | $210.82 |

CBA | Commonwealth Bank Of Australia | 1.60% | $149.58 |

WBC | Westpac Banking Corporation | 1.10% | $38.53 |

ANZ | ANZ Group | 0.69% | $36.42 |

By Warren Masilamony

South32 rallies on production beat

[11:20 am] South32 (+4.6%) is trading at levels not seen since April 2023 after reporting better-than-expected Q2 report this morning.

Payable copper 18kt vs 18.2kt ests (‑1% miss) at Sierra Gorda, strong by-product credits and provisional pricing

Alumina 1,314kt vs 1,292kt ests (+2% beat)

Aluminium 308kt vs 295kt ests (+4% beat) with Brazil weaker on prices, Hillside near max capacity

Manganese ore 1,312kt vs 1,325kt ests (‑1% miss) with Australia rebounding post-cyclone and South Africa steady but maintenance-affected

Payable silver 2,420koz vs 2,225koz ests (+9% beat)

Payable zinc 10.4kt vs 10.3kt ests (+1% beat)

Nickel 5.6kt vs 7kt ests (‑20% miss)

H1 operating unit costs tracking in line or below guidance

ASX 200 higher but miners take a breather

[10:41 am] ASX 200 up 0.67%, slightly off early intraday high of 0.83%. A relatively broad-based bounce, with 154 constituents (77%) trading higher.

Big Four banks mostly up 1-2%, notably NAB and Macquarie up 2.3% and 2.4% respectively. Miners a little soft off the back of Fortescue (-1.2%), Northern Star (-3.9%, I thought they pre-released the numbers but looks like today's quarterly had something new) and Evolution (-2.6%, pulling back after yesterday's 9.4% rally).

ASX 200 sector performance (Source: TradingView)

Pantoro December 2Q26 report

[10:40 am] Pantoro’s December quarterly report (announced pre-market) was fairly ugly, with weaker-than-expected production, higher costs and lower guidance expectations.

Gold production of 22.1koz vs 26.0koz ests (15.1% miss)

Realised price of A$6,077/oz vs A$6,061/oz ests (0.3% beat)

AISC of A$2,571/oz vs A$2,348/oz ests (9.5% miss)

EBITDA A$83.6m

Pantoro expects FY26 gold production to come in at the lower end of its 100,000 to 110,000oz guidance range.

The stock is currently down 9.1% ($5.27).

By Warren Masilamony

Resolute Mining meets 2025 guidance

[9:58 am] Resolute Mining reported a very strong December quarter and relatively in-line 2025 production and cost outcome, though not sure why earnings came in below consensus expectations.

Q4 gold production of 65.9koz vs. 59.8koz (10.2% beat)

Q4 AISC of A$1,877/oz vs. A$1,942 (3.3% beat)

FY group production of 277.2koz vs. guidance 275–285koz (within guidance)

FY AISC of A$1,843/oz vs. guidance A$1,750–1,850/oz (within guidance)

FY EBITDA of $382.9m vs. $434.4m ests (11% miss)

FY revenue of $865.6m vs. $919.9M (~6% miss)

Resolute guided to 2026 group production of 250-275koz at AISC of A$2,000-2,200/oz, this is relatively in-line with Macquarie estimates of 250.8koz at AISC of A$2,175/oz.

Company page: Resolute Mining (RSG)

RPMGlobal receives FIRB clearance for Caterpillar scheme

[9:48 am] RPMGlobal has cleared a key regulatory hurdle in its proposed acquisition by Caterpillar, bringing the scheme closer to implementation.

FIRB approval granted on 22 January 2026, satisfying the Commonwealth Government condition under the Foreign Acquisitions and Takeovers Act

Scheme implementation still subject to conditions precedent, including Federal Court approval

Shareholders will be updated on the timetable as approvals progress

Caterpillar offered to acquire RPMGlobal for $5.00 per share (32% premium) on 1 September 2025.

The company is incredibly lucky to have received this buyout, considering many tech/software peers like Qoria, Catapult Sports, Wisetech, Xero, TechnologyOne etc. are all down massively since mid-2025.

Company page: RPMGlobal Holdings (RUL)

Fortescue delivers record first half shipments of 100Mt

[9:45 am] “It was a record first half, with shipments reaching new highs across our operations. This was achieved safely and sets us up well heading into the second half to meet our FY26 shipments and cost guidance," says CEO Dino Otranto.

Total ore mined down 1% year-on-year to 61.4Mt vs. 62.75Mt ests (2.2% miss)

Total ore shipped up 2% to 50.5Mt vs. 50.6Mt ests (0.2% miss)

C1 unit cost up 5% to US$19.10/wmt (not sure of comparable to US$17.86/wmt ests)

Hematite average sale price of US$93/dmt, realising 88% of average Platts 62% index

Iron Bridge concentrate revenue of US$121.68/dmt was 102% of the average Platts 65% index

Net debt was US$1.0bn at 31 December 2025 vs. US$1.9bn in the September quarter

Fortescue left its FY26 guidance unchanged, which includes iron ore shipments of 195-205Mt at C1 costs of US$17.50-18.50/wmt.

Company page: Fortescue (FMG)

Insignia Financial posts modest funds growth amid mixed flows

[9:36 am] Insignia saw Funds Under Management and Administration (FUMA) rise slightly in the December quarter, with positive inflows into Wrap and Multi-Asset solutions offsetting institutional and Master Trust outflows.

FUMA up 0.4% quarter-on-quarter to $342.0bn, supported by market movements and retail inflows (I don't have any consensus/specific broker numbers handy)

Net outflows for the quarter $73m, driven by $1.6bn institutional outflows and $758m from Master Trust, partly offset by $1.5bn net inflows into Wrap

Multi-Asset solutions achieved $779m in net inflows within Asset Management

MLC Expand products continued strong growth with $1.7bn net inflows, partly offset by $0.2bn outflows from Platform Connect

Company page: Insignia Financial (IFL)

Sandfire and Northern Star Q2 reports

[9:30 am] Sandfire and Northern Star reported Q2 production reports this morning. Not going to take a closer look as both companies provided guidance updates/preliminary numbers earlier this month.

Cogstate delivers strong clinical trial growth, diversified revenue base

[9:27 am] Cogstate achieved record sales in 1H26, driven by non‑Alzheimer’s indications and an expanded sponsor base, supporting a more resilient and repeatable revenue profile.

Clinical Trials sales contracts up 105% to $41.7m, above guidance of $37–40m

Total revenue up 12% to $26.9m, exceeding guidance of $25–26m

Gross margin expected at 50–52%, EBITDA margin 20–23%, EBIT margin 14–17.5%, now likely at the top end of each range

Total Group contracted future revenue $104.9m, with $21.7m expected in 2H26 (vs. $17.5m PCP)

Strong diversification with 45% of new contracts from mood, sleep and other neurological conditions, expanding beyond Alzheimer’s

Company page: Cogstate (CGS)

Bhagwan Marine expects steady 1H26 earnings and strong cash flow

[9:25 am] Bhagwan Marine anticipates consistent EBITDA alongside significant free cash flow and reduced debt heading into the second half of FY26.

The company reported preliminary numbers for 1H26 this morning, including:

EBITDA to be in the range of $21.8-22.8m vs. $23.4m a year ago (down 4.7% at the midpoint)

Free cash flow between $8.5-9.0m vs. $1.0m a year ago (up 775%)

Net debt reduced to $1.0m vs. $5.3m at 30 June 2025

Capex totaled $12.5m for the period

Maiden FY25 dividend of $1.4m fully‑franked paid, with an interim dividend planned for 1H26, reflecting commitment to shareholder returns

Company page: Bhagwan Marine (BWN)

Netwealth posts record FUA inflows as momentum continues

[9:18 am] Netwealth delivered another strong quarter with record custodial inflows and robust Managed Account growth, underpinning sustained growth across its wealth management platform.

Total funds under administration (FUA) up 23.6% to $125.6bn at 31 December 2025, driven by $8.4bn of custodial inflows for the quarter, a second consecutive quarterly record

Net FUA flows were $4.2bn, or $4.6bn excluding low-revenue institutional outflows, with positive market movement adding $0.6bn

Managed Accounts saw record net flows of $1.8bn, up 12.8% on the prior quarter and 61.4% on the pcp

Total accounts increased by 4,841 (2.9%) during the quarter to 172,221, up 13.7% on the pcp

Growth was supported by strong contributions from existing financial intermediaries and broad-based momentum across all products and services

To add some perspective, Macquarie (Dec-25) was expecting year-end FUA of $125 billion (vs. $125.6bn reported, or a 0.5% beat).

Netwealth has dramatically underperformed peers like Hub24 (down 29.5% in the last six months vs. Hub24 down 3%) due to First Guardian failure. It'll be interesting to see if this solid result can help close some of that gap.

Company page: Netwealth Group (NWL)

Regis reports record Q2 cash generation, reaffirms FY26 guidance

[9:10 am] "The December quarter saw another consistent and reliable operational performance across Duketon and Tropicana, translating into record cash and bullion generation and continued strengthening of the balance sheet," said Managing Director Jim Beyer.

Gold production of 96.6koz

AISC of A$2,839 vs. A$2,794/oz ests (1.6% miss), though the figure includes A$179/oz of non-cash stockpile drawdown costs

Gold sales of 99.5koz vs. 98.5koz ests (1.0% beat)

Revenue of $640.6m, operating cash flow of $419m

Regis reaffirmed its FY26 guidance of 350-380koz gold production at AISC of A$2,610-2,990/oz.

Company page: Regis Resources (RRL)

Lynas seeks US price support as rare earths geopolitics intensify

[9:07 am] Lynas is in talks with the US Department of Defense to secure government backed price stability, aiming to reduce exposure to Chinese driven volatility without relying on direct funding.

Lynas is discussing price floor style support with the Pentagon, similar to the structure granted to MP Materials, with negotiations delayed by the recent US government shutdown

Management is pushing for policy driven market stability rather than subsidies, arguing this would allow rare earths markets to function more efficiently without government cash outlays

Unlike MP Materials, Lynas faces structural hurdles as a non-US company, despite being the only other major non-Chinese producer and a key supplier of heavy rare earths critical to defence

Heavy rare earth output reached 26 tonnes last quarter from its Malaysian operations, supporting demand from Japanese customers monitoring potential Chinese export disruptions

Source: Bloomberg

Energy Fuels–ASM deal firms up pathway to integrated rare earths platform

[9:05 am] Australian Strategic Metals (ASM) received a takeover from NYSE-listed Energy Fuels on Wednesday, valuing the company at $299 million or $1.60 per share (~120% premium).

ASM hosted a conference call regarding the transaction on Wednesday, the highlights included:

Transaction expected to close around June 2026, subject to regulatory and shareholder approvals, with scheme consideration comprising a 13 cent per share special dividend plus 0.053 Energy Fuels shares per ASM share

Offer value will move with Energy Fuels’ share price, providing upside optionality for ASM shareholders if the acquirer’s equity strengthens

Potential to reduce Dubbo project capital intensity by around $200 million if intermediate product is processed at White Mesa rather than pursuing full oxide separation on site

Expansion of the Korean Metals Plant to 3,600 tonnes per annum is progressing, with initial feedstock expected from the combined group supply chain

White Mesa Phase 2 rare earths plant targeted for 2027 to 2028, lifting capacity to 6,000 tonnes per annum of NdPr oxide and adding meaningful Dy and Tb production

Combined group expected to improve access to government and private funding, supporting discussions with USXM and Export Development Canada, while leveraging ASM’s metallisation capability to build a Western mine to alloy supply chain

Company page: Australian Strategic Materials (ASM)

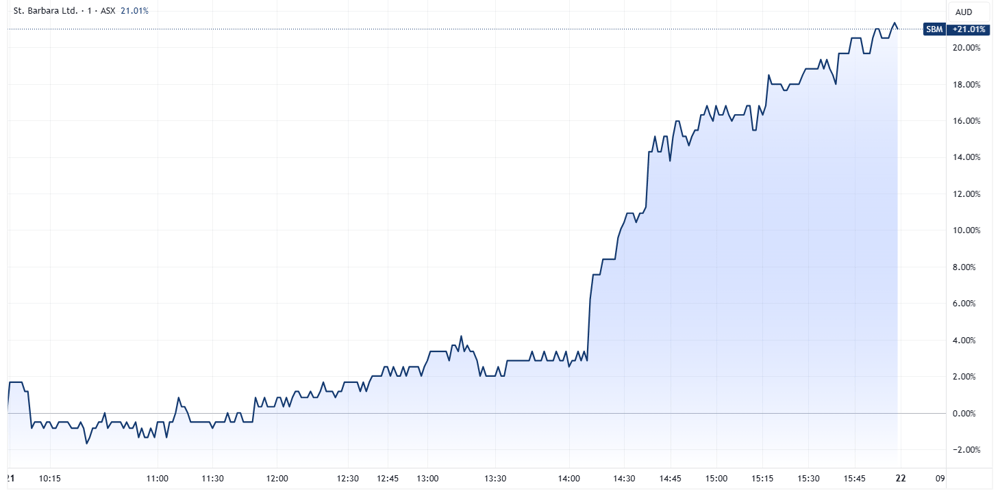

St Barbara surges on 15-Mile Processing Hub study

[9:00 am] St Barbara announced its pre-feasibility study for the 15-Mile Processing Hub at 2:07 pm AEST on Wednesday, which triggered a massive rally through to market close. The stock was up 3% ($0.61) prior to the announcement, and finished the session up 20.3% ($0.71).

St Barbara intraday chart on Wednesday, 21 January 2026

The PFS highlights a low capital, high return processing hub with strong leverage to gold prices and a long life, underpinning a step change in group cash flow.

Post tax NPV of A$1.40bn at a US$3,000/oz gold price, rising to A$2.30bn at $4,000/oz highlighting material upside to bullion

An 80% post tax IRR at US$3,000/oz and 122% IRR at US$4,000/oz

Stable production profile of more than 100koz per annum over an 11 plus year mine life, supporting durable cash generation

Cumulative post tax free cash flow of around A$2bn for an initial capital outlay of roughly A$308m

Development expected to be internally funded through cash flow from New Simberi and the proposed Touquoy restart, limiting balance sheet risk

Back in December, I wrote about how St Barbara was 'cheap', given the company was massively cash backed and de-risked due to:

Sold 20% of Simberi to PNG state owned Kumul for $100m , repayable from future revenues, effectively trading equity for permitting certainty and fiscal stability

A further 40% stake sold to China’s Lingbao for $370m cash, introducing a funding partner and materially derisking project development

Pro-forma cash of roughly $527m, implying around 40 cents per share in cash backing vs. a share price of ~51 cents back in December 2025

Simberi’s feasibility study points to a post tax NPV of US$1.8bn at US$4,000/oz gold, highlighting significant retained value despite lower ownership

Beyond Simberi, St Barbara holds three advanced Canadian gold projects with 1.4 million ounces of reserves (which includes 15-Mile)

Company page: St Barbara (SBM)

Netflix slides as higher spending and deal costs hit near term earnings outlook

[8:48 am] Netflix shares dipped 2.1% to the lowest since April 2025 after management flagged heavier content investment and acquisition related costs, weighing on short term profitability despite solid subscriber and revenue growth.

Netflix plans to lift film and TV spending by 10% in 2026, following roughly US$18bn spent last year, as it expands content, live events, games and prepares a new mobile interface

Earnings guidance disappointed with current quarter EPS forecast at 76 cents versus market expectations of 82 cents, while revenue guidance of $12.2 billion was in-line

The Warner Bros. acquisition adds $275 million of costs this year, prompting Netflix to pause share buybacks to conserve cash, increasing near term margin pressure

Subscribers rose almost 8% to more than 325 million, with double digit revenue growth sustained through price rises and advertising, which is forecast to double to $3 billion in 2026

TACO trade shows signs of strain as markets test Trump’s resolve

[8:47 am] The long running assumption that Trump retreats in the face of market stress is being challenged, with recent volatility suggesting the TACO trade may now require a sharper selloff to remain effective.

The TACO trade has underpinned risk appetite for months, encouraging investors to fade aggressive policy threats after last year’s tariff rollback, but that confidence may now be dulling its own effectiveness

Markets reacted more forcefully to Greenland related tariff threats, with the S&P 500 down 2.1% on Wednesday, the VIX at its highest since November, gold at a record and the dollar posting its worst two day slide in about a month

Elevated equity valuations and low hedging left investors exposed, with the S&P 500 near record highs and Bank of America survey data showing protection against selloffs at multi year lows

Some strategists argue Trump may not back down without a larger, more disorderly market correction, particularly given the political stakes around Greenland and unresolved tariff authority risks

Source: Bloomberg

Risk rally resumes as Trump softens stance on Greenland

[8:44 am] Markets staged a broad relief rally after President Trump signalled a de escalation path on Greenland, easing tariff and geopolitical fears that had driven a sharp cross asset selloff.

US equities rebounded strongly with the S&P 500 up 1.16%, its biggest gain since November, lifting the index back into positive territory for 2026 as more than 400 constituents advanced

The rally was broad in nature with stocks, bonds, credit, emerging markets and ETFs all rising in the strongest cross asset move since August, while gold cooled and Treasury yields fell

Energy stocks hit record highs and small caps outperformed large caps for a 13th straight session, underscoring a rotation back into cyclicals and risk sensitive areas

Relief was driven by Trump ruling out military force over Greenland and suggesting a NATO aligned framework, alongside Supreme Court comments seen as supportive of Fed independence

Good morning!

[8:34 am] ASX 200 futures are up 39 pts (+0.44%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks broadly higher, reversing most of Wednesday's selloff

Russell 2000 (+2.00%) back at fresh all-time highs, solid breadth with all sectors positive and Equal-weight S&P 500 outperforming the cap-weighted index

Trump touted a 'framework' for a future deal for Greenland, holds off on EU tariffs previously set for 1-Feb

To catch up on all overnight developments, check out today's Morning Wrap.