ASX 200 Live Today - Thursday, 14th May

The S&P/ASX 200 is set to slip for a fifth straight session. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Thursday, May 14. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 down for a fifth straight day

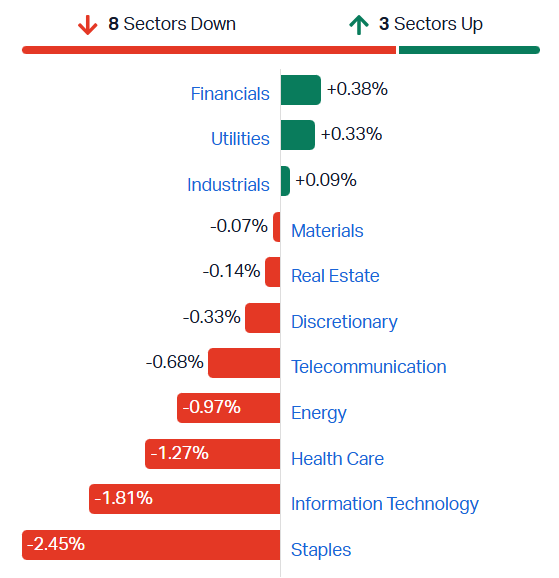

[1:15 pm] Wrapping up a little earlier today. The ASX 200 is currently down 0.19% and on track to record a fifth straight day of declines. Breadth is rather weak, with 124 constituents trading lower (62%). The index has largely been buoyed by a small bounce for most major banks, and BHP and Rio Tinto both gaining around 1%, to fresh all-time highs. Beyond the heavyweights:

Healthcare stocks have continued to trend lower, with CSL (-1.9%) making fresh low nine-year lows today

Tech stocks pulling back, with Xero (-7.4%) sharply lower after a mixed 1H26 result

Staples smashed after the ACCC alleged that Coles made false or misleading representations to consumers about the prices of 245 products

While the Materials index is flat, sub-sectors like lithium, rare earths and gold are also under pressure.

S&P/ASX 200 sectors (Source: Market index)

CBA slightly higher after Wednesday's freefall

[1:00 pm] CBA (+0.85%) is trading slightly higher after yesterday's 10.4% selloff.

CBA's Q3 trading update on Wednesday missed elevated expectations, with flat revenue growth, a material lift in collective loan loss provisions and a weaker CET1 capital position.

Analysts flagged rising derating risk from fading NIM tailwinds, tighter capital limiting shareholder returns, and material headwinds to the dominant investor mortgage book from Federal Budget negative gearing changes.

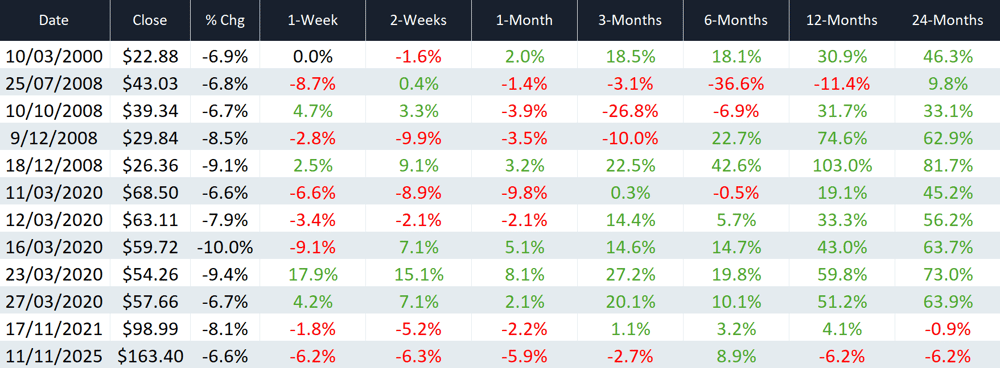

Yesterday, I ran the numbers for how CBA performs after such massive one-day selloffs. Here's what forward returns look like (all but one come off the back of a major economic shock like the Dotcom bubble, GFC or pandemic).

How CBA performed after a major one-day selloff | Source: Author's own calculations

Tech stocks mostly lower

[12:56 pm] A fairly heavy day for most tech stocks, with household names like TechnologyOne, Pro Medicus, Wisetech and Xero all down 2-7%.

The S&P/ASX 200 Tech Index is down 1.5% to a near one-month low, but still ~13% above its 30 March low.

Ticker | Company | % Chg | Price | 1 Year % |

|---|---|---|---|---|

XRO | Xero | -7.2% | $75.17 | -56.9% |

NXL | Nuix | -5.4% | $1.32 | -44.3% |

WTC | Wisetech Global | -4.2% | $36.93 | -64.3% |

PME | Pro Medicus | -3.8% | $120.71 | -54.5% |

TNE | Technology One | -2.4% | $27.63 | -14.6% |

BVS | Bravura Solutions | -2.4% | $2.21 | -0.7% |

IRE | Iress | -2.0% | $5.92 | -29.3% |

OCL | Objective Corporation | -1.9% | $10.48 | -39.1% |

SDR | Siteminder | -1.8% | $2.95 | -30.9% |

DDR | Dicker Data | -1.5% | $9.01 | 2.7% |

CAT | Catapult Sports | -1.4% | $3.15 | -29.3% |

360 | Life360 | -0.8% | $18.61 | -37.5% |

HSN | Hansen Technologies | -0.6% | $4.76 | -3.4% |

AD8 | Audinate Group | 0.0% | $2.17 | -67.7% |

MAQ | Macquarie Technology Group | 0.3% | $75.74 | 16.2% |

NXT | Nextdc | 0.8% | $14.78 | 9.9% |

DTL | Data#3 | 0.9% | $7.96 | 0.8% |

PPS | Praemium | 1.5% | $0.69 | -8.7% |

DGT | Digico Infrastructure Reit | 2.4% | $2.76 | -13.1% |

CDA | Codan | 3.5% | $39.89 | 132.2% |

WBT | Weebit Nano | 17.8% | $5.89 | 216.7% |

MP1 | Megaport | 34.1% | $13.21 | 4.7% |

ACCC wins landmark case against Coles over misleading "Down Down" discounts

[12:26 pm] The AFR reports that the Federal Court has ruled Coles misled shoppers with its discount promotions, with implications for the broader retail sector and a pending Woolworths judgment.

13 of 14 sample products in Coles' "Down Down" promotion ruled to be misleading discounts, having not been sold at the "Was" price for a reasonable period

Justice O'Bryan found a minimum 12-week period at the higher price would have made the promotions non-misleading

Court also found Coles' price increases were commercially justifiable, resulting from supplier cost price increases following COVID-19

Woolworths' "Prices Dropped" judgment still pending after hearing concluded two weeks ago; could have broader implications across the retail sector

Graincorp battered on profit miss

[12:24 pm] Graincorp trading sharply lower (-13.3%) after its 1H26 result missed cash flow and NPAT expectations. While the full-year guidance was reaffirmed, management warned the near-term outlook is dependent on stable weather conditions.

Numbers from the earlier post include:

Revenue of $3.88bn vs $3.89bn ests (in line)

Adjusted EBITDA down 33% to $136m vs $143m ests (5% miss)

Underlying NPAT down 52% to $33m vs $36.9m ests (11% miss)

Interim dividend of 14 cps vs 14 cps ests (in line)

East Coast Australia grain handled down 10% to 26.5mmt

FY26 guidance reaffirmed: Underlying EBITDA $200-240m and underlying NPAT $20-50m

Minimal Middle East conflict impact on supply chain, though global fuel and fertiliser markets affected, weather to drive 2026-27 winter crop outcomes

Lithium stocks broadly lower

[11:57 am] Lithium stocks have pulled back sharply, with most names down 2-4%. Chinese lithium carbonate futures currently down 4.2% to 193,160 yuan a tonne.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

GL1 | Global Lithium | -7.02% | $0.53 | 211.76% |

LKE | Lake Resources | -6.32% | $0.09 | 187.10% |

LTR | Liontown | -5.64% | $2.43 | 223.33% |

AGY | Argosy Minerals | -4.65% | $0.08 | 331.58% |

CXO | Core Lithium | -3.66% | $0.34 | 307.14% |

EUR | European Lithium | -3.41% | $0.43 | 701.89% |

DLI | Delta Lithium | -3.14% | $0.25 | 30.00% |

INR | Ioneer | -3.03% | $0.16 | 14.29% |

PLS | PLS Group | -2.80% | $6.26 | 294.95% |

IGO | IGO | -2.44% | $8.79 | 102.07% |

PAT | Patriot Resources | -2.31% | $0.13 | 111.67% |

VUL | Vulcan Energy Resources | -1.73% | $3.69 | -3.84% |

MIN | Mineral Resources | -1.57% | $69.51 | 178.04% |

PMT | Pmet Resources | -0.63% | $0.79 | 222.45% |

WR1 | Winsome Resources | 0.94% | $0.54 | 224.24% |

WiseTech: UBS sees DSV exit as isolated, minimal contagion risk

[11:22 am] UBS notes DSV has firmed up its ambition to migrate from CargoWise to in-house platform Tango from 2027, though the broker sees DSV as an isolated case with limited risk to other customers.

DSV reaffirmed intention to move Schenker volumes onto CargoWise initially to achieve targeted synergies before transitioning to Tango from 2027 once customer integration is complete

DSV described as "not necessarily in a hurry", Tango will require more investment to reach required productivity

UBS reads commentary as implicit acknowledgement that CW remains the superior system today, with channel checks suggesting tasks requiring 10 clicks in CW need 14-15 in Tango

Contagion risk seen as minimal as building an in-house global freight forwarder system estimated to cost $200-300m and take 5-7 years, with ongoing maintenance requiring "no less than 1000 people" in IT

Company page: WiseTech Global (WTC)

Peninsula Energy seeking $77m funding package

[11:20 am] Peninsula has entered a trading halt to raise a combined equity and debt package, with Soul Patts anchoring the deal, according to the AFR.

Total funding package of ~US$56m (A$77m), comprising a US$30m (A$41m) convertible note and a US$26m (A$36m) equity raising

Equity raise priced at $0.35 per share, a ~10% discount to the last close

Soul Patts understood to be anchoring a portion of the raising, with Canaccord Genuity and Shaw and Partners acting as brokers

Proceeds to fund flagship Lance Uranium project in Wyoming, US

Company page: Peninsula Energy (PEN)

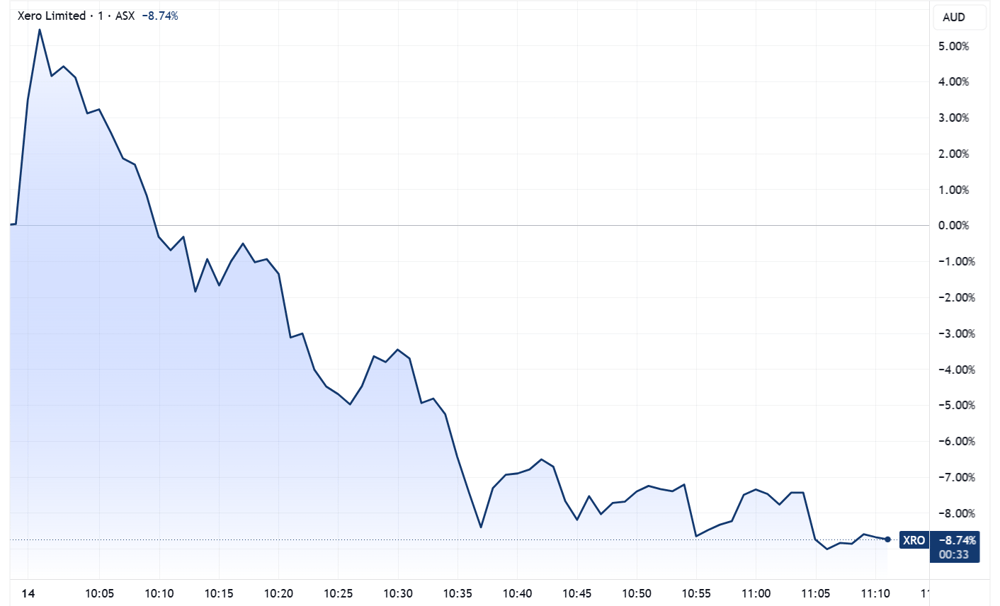

Xero opens higher but aggressively sold down

[11:10 am] A wild morning for Xero – opened 3.0% higher, rallied as much as 6.1% and now down ~9%.

Xero intraday chart (Source: TradingView)

The company reported its 1H26 result this morning, which featured:

Revenue up 31% to NZ$2.75bn vs NZ$2.74bn ests (in line)

NPAT of NZ$167.4m vs NZ$230.9m ests (28% miss), impacted by Melio acquisition costs

Free cash flow of NZ$554.0m, added 506,000 customers in FY26, average monthly churn at 1.14% remains below pre-pandemic trends

FY27 revenue guidance of NZ$3.62-3.73bn vs NZ$3.58bn ests (3% beat)

FY27 adjusted EBITDA guidance of NZ$860-920m vs NZ$876.7m ests (2% beat)

Board authorised up to A$550m in share purchases in FY27 to offset share-based compensation dilution

Analysts' take on CBA

[11:03 am] CBA's Q3 trading update missed elevated expectations, with flat revenue growth, a material lift in collective loan loss provisions and a weaker CET1 capital position driving the stock down 10.4%, its largest one-day decline on record.

Analysts flagged rising derating risk from fading net interest margin tailwinds, tighter capital limiting shareholder returns, and material headwinds to dominant investor mortgage book from Federal Budget negative gearing changes.

Morgans retained Sell, lowered target from $124.26 to $119.40. Elevated trading multiples offer insufficient margin of safety, with unclear NIM trajectory and capital ratio path suggesting a potential capital raising in FY28.

Morgan Stanley retained Underweight, lowered target from $131.00 to $130.00. De-rating risk is rising from macro headwinds and capital tightness, with margin outlook hindered by deposit mix and lending competition limiting scope for dividend growth.

Macquarie retained Underperform, lowered target from $117.00 to $114.00. Sector revenue is clearly deteriorating with CBA relatively less weak, though volume growth is increasingly challenged by rate hikes, tax changes and structural headwinds making valuation difficult to justify.

Bapcor flags higher leverage and subdued trading on business update call

[10:53 am] The auto parts group's call reinforced the deteriorating outlook, with leverage now expected to run above prior guidance and FY27 starting from a lower base.

Leverage at 30-Jun-26 now expected above prior 1.2-1.5x guidance, but still well within covenants

FY26 gross margin running below initial expectations on price rollbacks and higher input costs, not expected to deteriorate further as rollback pace moderates and offsetting margin initiatives accelerate in H2 2026

FY27 likely to start from a lower earnings base than FY26 if current macro headwinds persist, trading conditions in Q2 2026 remain subdued due to global instability

Market share gains being realised broadly across trade businesses in H1 2026, primarily at the expense of smaller competitors

Inventory reduction initiatives ongoing but slower sales will delay the pace of balance improvement through FY26

Company page: Bapcor (BAP)

Bapcor obliterated

[10:50 am] Bapcor opened 7.7% lower, now down 19.4% to an all-time low of 41.5 cents. The stock is now down 94% from its June 2021 all-time high, down 75% year-to-date and 30% below the recent capital raise price of 60 cents per share.

Bapcor released a trading update this morning, which was abysmal on all fronts.

FY26 underlying EBITDA (post-AASB16) guidance cut to $144-150m vs prior $150-160m and $154.9m ests (5% miss)

FY26 underlying EBITDA (pre-AASB16) cut to $62-68m vs prior A$74-79m, a 15% reduction at the midpoint

Feb-Apr trading: Trade +0.7%year-on-year, Networks +3.8, Retail (LFL) +1.6, New Zealand +0.7%

Trading conditions have materially deteriorated since late March with the commencement of the Middle East conflict and rising interest rates

Current conditions could give rise to a non-cash impairment, to be assessed at financial year end

Top ASX 200 gainers

[10:47 am] 4DMedical is bouncing off the 200-day, after falling ~50% between 13 April and 13 May, Codan higher off a broker upgrade and a industrials also edging higher.

Ticker | Company | % Chg | Price |

|---|---|---|---|

4DX | 4DMedical | 5.62% | $3.57 |

CSC | Capstone Copper Corp | 2.33% | $14.25 |

CDA | Codan | 2.33% | $39.45 |

MQG | Macquarie Group | 1.99% | $241.51 |

IAG | Insurance Australia Group | 1.78% | $7.74 |

WOR | Worley | 1.75% | $12.18 |

ALQ | ALS | 1.74% | $22.16 |

FMG | Fortescue | 1.73% | $22.91 |

NWH | NRW | 1.63% | $7.48 |

OBM | Ora Banda Mining | 1.44% | $1.41 |

Top ASX 200 losers

[10:47 am] A very whipsaw session for Xero, which rallied as much as 6% in early trade. The broader tech sector is also selling off, while lithium and rare earths take a breather.

Ticker | Company | % Chg | Price |

|---|---|---|---|

XRO | Xero | -8.64% | $74.00 |

ELV | Elevra Lithium | -6.07% | $11.92 |

LTR | Liontown | -5.45% | $2.43 |

WTC | Wisetech Global | -4.91% | $36.64 |

PDI | Predictive Discovery | -4.37% | $0.99 |

LYC | Lynas Rare Earths | -3.34% | $19.24 |

TNE | Technology One | -3.32% | $27.38 |

XYZ | Block | -3.25% | $96.95 |

PRN | Perenti | -3.18% | $2.13 |

WGX | Westgold Resources | -2.73% | $5.52 |

Australian Banks face credit growth headwinds from FY27 budget tax changes

[9:50 am] Material changes to capital gains and negative gearing in the FY27 budget are expected to slow housing credit growth and weigh on bank earnings, according to Macquarie.

Capital gains 50% deduction to be replaced with inflation indexation and a 30% minimum tax on net gains

Negative gearing limited to deductions against rental income or property capital gains (widely held trusts, super and BTR exempt)

Removal of negative gearing potentially more than doubles post-tax holding costs of investment property, with borrowing power estimated 10-20% lower, or 20-30% lower than Dec-25 when including 100 bps of rate hikes

Treasury estimates house prices grow 2% lower for "a couple of years", modelled estimates suggest 1-4%, with downside risk given rising rates and slowing market

Housing credit growth seen slowing from ~7% to ~5%, downside scenario of ~0% investor credit growth (similar to 2019-21) could see total housing credit growth fall to ~4%, near the 3% all-time low in 2019 when banks underperformed by up to 20%

Bank share prices correlated with house prices/expectations and post-tax interest cost set to rise above gross rental yield, making property less attractive as an investment

Mitigating positives include permanent $20,000 instant asset write-off (supportive for business credit) and eased regulation for smaller banks including higher covered bond caps, which should benefit regionals like Bendigo and Bank of Queensland

oOh!media Q1 revenue growth slightly ahead, but billboards weigh on margins

[9:31 am] The out-of-home media group reported solid Q1 trading, but flagged softer-than-expected gross margins on billboard pressure.

Q1 revenue: Australia up 7%, group up 4%, slightly ahead of February projections

Q2 media revenue pacing similarly: +6% Australia and +2% group, against +19% pcp

1H26 gross margin will be softer than anticipated, with Billboards (~40% of group revenue) performing below expectation and new contracts at higher rents

Underlying adjusted opex in 1H26 expected to be slightly below pcp with further 2H savings

CY26 capex guided lower at$45-55m vs prior A$55-65m

Company page: oOh!media (OML)

Bapcor downgrades FY26 EBITDA guidance

[9:28 am] Bapcor is already down 75% year-to-date and down 90.4% in the last twelve months, which includes an emergency $200 million capital raise (26-Feb) at a massive 65% discount. Now, the auto parts group has cut its FY26 earnings outlook citing a material deterioration in trading conditions since late March, with potential non-cash impairment flagged.

FY26 underlying EBITDA (post-AASB16) guidance cut to $144-150m vs prior $150-160m and $154.9m ests (5% miss)

FY26 underlying EBITDA (pre-AASB16) cut to $62-68m vs prior A$74-79m, a 15% reduction at the midpoint

Feb-Apr trading: Trade +0.7%year-on-year, Networks +3.8, Retail (LFL) +1.6, New Zealand +0.7%

Trading conditions have materially deteriorated since late March with the commencement of the Middle East conflict and rising interest rates

Current conditions could give rise to a non-cash impairment, to be assessed at financial year end

Company page: Bapcor (BAP)

GrainCorp 1H26 misses on softer grain margins

[9:22 am] The grains handler reported a weaker-than-expected first half reflecting global oversupply and compressed margins, though it maintained full year earnings guidance and held the dividend flat.

Revenue of $3.88bn vs $3.89bn ests (in line)

Adjusted EBITDA down 33% to $136m vs $143m ests (5% miss)

Underlying NPAT down 52% to $33m vs $36.9m ests (11% miss)

Interim dividend of 14 cps vs 14 cps ests (in line)

East Coast Australia grain handled down 10% to 26.5mmt

FY26 guidance reaffirmed: Underlying EBITDA $200-240m and underlying NPAT $20-50m

Minimal Middle East conflict impact on supply chain, though global fuel and fertiliser markets affected, weather to drive 2026-27 winter crop outcomes

Graincorp is down around 30% since mid-October, largely driven by earnings-related announcements.

2-Feb-26: Issued FY26 earnings guidance well-below market expectations, shortfall was attributed to global grain oversupply, low prices, and slow grower selling, all of which continued to weigh on earnings.

17-Dec-25: Preliminary estimate receivable volumes for FY26 was 11-12Mt vs. 13.3Mt in FY25 (this compares to prior commentary of higher volumes year-on-year)

Company page: GrainCorp (GNC)

Worley targets double-digit EBITA growth to FY30 and launches new buyback

[9:10 am] The engineering services group used its Investor Day to outline medium-term ambitions and extend capital returns to shareholders.

Targeting double-digit underlying EBITA growth over the medium-term to FY30

Launching on-market share buyback of up to $300m, running for 12 months from 29 May

This follows the completion of an initial $500m buyback program on 22 April

Company page: Worley (WOR)

Megaport's Latitude.sh secures US$183m in GPU and infrastructure contracts

[9:08 am] The subsidiary has won three major contracts across two customers, materially boosting recurring revenue and capex outlook.

Combined total contract value of ~US$182.9m (A$254.0m), representing ~US$65.2m (A$90.6m) in annualised recurring revenue

Two contracts (~90% of TCV) have 36-month initial terms; the third has a 24-month term

Full ARR contribution expected to be added on a run-rate basis by the end of 1H27

FY26 Group Capex could increase by up to a further A$140.3m if equipment is delivered prior to 30-Jun-26

Company page: Megaport (MP1)

ASX appoints Anthony Attia as MD and CEO

[9:07 am] The exchange operator has named the former Euronext executive to lead the company through its next phase of transformation, effective 1 September 2026.

Attia brings close to three decades of exchange experience across European and US jurisdictions, with senior roles at Euronext, ICE and NYSE Euronext

Most recently Euronext Global Head of Derivatives and Post Trade, and previously CEO of Euronext Paris from 2014 to 2021

Outgoing CEO Helen Lofthouse departs on 29 May 2026

Company page: ASX (ASX)

Xero FY26 earnings beat on revenue but NPAT misses

[9:05 am] Xero delivered strong operating results with 31% revenue growth and 18% EBITDA growth, though Melio acquisition costs weighed on bottom-line earnings.

Revenue up 31% to NZ$2.75bn vs NZ$2.74bn ests (in line)

Adjusted EBITDA up 18% to NZ$757.4m vs NZ$742.4m ests (2% beat)

NPAT of NZ$167.4m vs NZ$230.9m ests (28% miss), impacted by Melio acquisition costs

Free cash flow of NZ$554.0m, added 506,000 customers in FY26, average monthly churn at 1.14% remains below pre-pandemic trends

FY27 revenue guidance of NZ$3.62-3.73bn vs NZ$3.58bn ests (3% beat)

FY27 adjusted EBITDA guidance of NZ$860-920m vs NZ$876.7m ests (2% beat)

Board authorised up to A$550m in share purchases in FY27 to offset share-based compensation dilution

FY28 aspiration reiterated to more than double FY25 group revenue and deliver greater than Rule of 40 outcomes, with Melio expected to reach adj-EBITDA breakeven run-rate in 2H28.

Company page: Xero (XRO)

Analysts slash Temple & Webster target prices

[8:59 am] Temple & Webster has seen its target price slashed from $8-13 to ~$4 this morning.

Temple & Webster downgraded to Neutral from Outperform; target cut to $4.75 from $13.70 (Macquarie)

Temple & Webster downgraded to Underweight from Neutral; target cut to $4.00 from $8.70 (JPMorgan)

On Wednesday, the company cut its FY26 revenue and EBITDA guidance well-below market expectations, though management said current margin run-rate see FY27 EBITDA almost double to $40 million. The stock finished the session down 6.3%, now down ~63% YTD.

The key highlights from yesterday's update include:

FY26 revenue guidance of $665-675m vs. $715.4m ests (6% miss)

FY26 EBITDA guidance of $20-22m vs. $27.2m ests (23% miss)

April EBITDA increased to ~$2.5m, the most profitable April in company history

Current margin run-rates would lead to FY27 EBITDA almost doubling to ~$40m even in a low growth scenario

Alcoa flags strong Q2 and tightening aluminium market

[8:54 am] Alcoa pointed to a solid earnings backdrop, asset monetisation progress, and supportive supply-demand dynamics amid Middle East-driven tightness at the BofA conference.

Anticipating a strong Q2 2026 following solid Q1, production ramping globally with Spain smelter to run at full capacity through 2027

Asset monetisation underway with first sale expected soon, targeting $500m-$1bn in proceeds

$65m investment announced to expand recycling at Mosjøen, Norway facility

Middle East conflict has tightened supply and inflated aluminium prices and premiums, with physical scarcity expected in Europe or North America within six months

Aluminium demand growth projected at 3-4% annually with secondary outpacing primary, Chinese production capped at 45m tons providing supportive supply constraints

Iran war set to constrain Trump's leverage in Xi summit

[8:53 am] Trump's military threats against Iran come ahead of his Beijing trip, with the prolonged Strait of Hormuz closure pressuring oil markets and complicating US-China trade talks.

Ceasefire described by Trump as on "massive life support"

New US intelligence shows Iran retains operational access to 30 of 33 missile sites along Hormuz and ~70% of prewar missile stockpile

Pentagon's acting comptroller put the war's price tag at ~$29bn, up from a prior $25bn estimate, amid a $1.5tn defence spending request for next year

Iran's demands include unfreezing of billions in assets, sanctions relief and an end to the US naval blockade before reopening Hormuz, with Bloomberg Economics seeing a lasting deal as "elusive"

UAE retaliated against earlier Iranian strikes in coordination with Israel; Habshan gas plant operating at 60% capacity, targeting 80% by year-end and full capacity only in 2027

Source: Bloomberg

Oil agencies cut 2026 demand outlook

[8:52 am] OPEC, the IEA and EIA all flagged extended disruption from the Iran war, with Gulf supply running well below pre-war levels and inventories drawing sharply.

OPEC cut April-June oil demand forecast by 500,000 bpd and lowered 2026 demand growth outlook by 210K bpd to ~1.17Mbpd, 2027 growth forecast raised to ~1.54Mbpd

IEA more bearish, sees global oil demand contracting 420,000 bpd in 2026 amid prolonged Strait of Hormuz disruptions, Q2 demand expected to contract 2.4Mbpd led by petrochemical weakness

Global oil supply fell another 1.8Mbpd in April to 95.1Mbpd, with cumulative losses since February at 12.8M bpd

Global inventories drew a combined 246m barrels across March and April, with IEA warning supply will remain below demand this year

EIA sees Strait of Hormuz remaining closed through late May before gradually reopening in June, with ~10.5Mbpd of Middle East production shut in during April as storage hits capacity

Trump-Xi summit looms with trade, Iran and Taiwan in focus

[9:47 am] The high-stakes Beijing meeting on Thursday and Friday brings together economic dealmaking ambitions that could move global markets, accompanied by an unprecedented CEO delegation.

CEOs flying with Trump includes Musk (Tesla), Huang (Nvidia), Cook (Apple), Fink (BlackRock), Schwarzman (Blackstone), Ortberg (Boeing), Sikes (Cargill), Fraser (Citigroup), Culp (GE), Solomon (Goldman Sachs), Mehrotra (Micron) and Amon (Qualcomm), with more undisclosed

White House framing the summit around trade rebalancing and reciprocity, bilateral boards on trade and investment expected, with potential agreements spanning aerospace, agriculture and energy

Boeing flagged a potential "big number" plane order from China after years of Airbus dominance; soybean and agricultural purchases also anticipated after Beijing's trade war boycott

Rare earths seen as the key driver of Trump's engagement, with China's export controls on materials critical to semiconductors having inflamed tensions last year

Iran war gives China leverage as Tehran's largest trade partner and top oil buyer, with the conflict extending well beyond the administration's initial 4-6 week estimate and pressuring US gas prices

Taiwan a key risk, with analysts warning US focus on Iran has drawn attention from the Pacific, with markets watching for any language shift from Trump that Beijing could exploit

Warsh confirmed as Fed chair in narrowest vote ever

[8:44 am] The Senate confirmed Kevin Warsh as Federal Reserve chair in a 54-45 vote, the closest margin in history, amid concerns over the central bank's independence under Trump.

Warsh confirmed 54-45, the narrowest Fed chair confirmation ever, with only one Democrat (Fetterman) crossing the aisle

Key market question is whether Warsh maintains Fed independence since Trump has demanded immediate rate cuts while a growing number of Fed officials argue the next move could be a hike

Warsh has signalled intent to shrink the Fed's $6.7tn balance sheet over time and argued rate cuts are fairer than balance sheet expansion

Powell will remain on the Fed board after his chair term ends Friday but maintain "a low profile", citing threats to central bank autonomy

Source: Bloomberg

April PPI surges to highest in three years on energy and tariff pressures

[8:43 am] Wholesale prices posted their largest monthly gain since March 2022, with broad-based pressures across goods and services raising the prospect of Fed rate hikes rather than cuts.

Headline PPI up 1.4% m/m vs. 0.7% ests, highest since Mar-22

Annualised headline up 6.0% vs. 5.0% ests, highest since Dec-22

Core PPI ex-food and energy up 1.0% m/m vs. 0.3% ests, highest since Mar-22

Annual core up 5.2% vs. 4.3% ests, highest since Dec-22

Final demand energy up 7.8% m/m drove three-quarters of the goods gain, with gasoline surging 15.6% as pump prices passed US$4/gallon amid the Iran conflict

Services index accelerated 1.2% m/m (biggest since Mar-22), with trade services up 2.7% suggesting tariff costs are flowing through; machinery and equipment wholesaling margins up 3.5%

US equities mixed as tech and semis drive record highs

[8:40 am] The S&P 500 and Nasdaq hit fresh record highs on semiconductor and Mag-7 strength, though breadth was negative and a hot PPI print added inflation concerns.

S&P 500 and Nasdaq set fresh record highs, but breadth was negative with equal-weight S&P lagging the cap-weighted index by ~100 bps

Headline April PPI up 1.4% m/m vs. 0.7% ests

Core PPI ex-food and energy up 1.0% m/m vs. 0.3% ests

10-year yield pulled back after hitting highest level since July 2025

Breadth remains a key area of caution alongside recent consumer/retail underperformance, particularly given affordability pressures from the prolonged Middle East conflict

Good morning!

[8:24 am] ASX 200 futures are down 22 pts (-0.25%).

The overnight session in a nutshell:

S&P 500 and Nasdaq closed at fresh record highs as AI/semiconductor strength offset a shocker April PPI

April US wholesale inflation jumped 6% year-on-year, the largest annual gain since December 2022, driven by a 7.8% surge in final demand energy prices linked to the Iran war

Trump landed in Beijing for his summit with Xi Jinping, with Iran, oil and tariffs front and centre