ASX 200 Live Today - Friday, 13th February

The S&P/ASX 200 is set to tumble after closing just shy of fresh all-time highs on Thursday. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Friday, February 13. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. We've got a new refresh button, so you won't have to refresh the page anymore! As always, let us know how we can make it even better.

ASX 200 sharply lower as Tech continues to nosedive and banks pull back

[2:30 pm] What a week ... the ASX 200 is currently down 1.2%, trading a little off session lows. Tech (-4.5%) continues its death spiral, Healthcare (-3.1%) also sharply lower as Cochlear tanks 17% on its weak 1H26 result, the resource sector is broadly lower after the broad-based commodity selloff overnight (jeez it sounds bearish out there doesn't it?) and Financials (-1.0%) take a breather. We're seeing an insane amount of results driven volatility, despite the market trading within an arms reach of all-time highs. Despite today's pullback, the market is still on track to finish the week 2.5% higher.

Came across some similar commentary on Wall Street, where the S&P 500 has observed 115 constituents experiencing a one-day decline of 7% of more in the last eight sessions, according to Compound Media. This hasn't happened since the dot-com bubble burst.

Volatility under the hood is not a good thing, but maybe this time is an exception amid this mass tech exodus. ASX 200 earnings have clearly been sound towards the big end/defensive end of town, with clean beats for most financials (CBA, ANZ and WBC) and utilities (ORG and AGL). The next two weeks represent the lion's share of results, so we'll just have to see where the numbers land. Have a good weekend!

Analysts cut Temple & Webster targets after H1 margin miss

[2:07 pm] Analysts reset targets after yesterday's blood bath, but largely stayed constructive on the sales rebound and longer-term margin recovery path.

Citi upgraded to Buy from Neutral, lowered target from $15.38 to $9.50 (-38.2%). Noted sales momentum improved into H2, but heavier discounting and promotions pressured margins

Bell Potter retained Buy, lowered target from $19.50 to $13.00 (-33.3%). Flagged competition is driving price investment and revenue growth is being prioritised

Goldman Sachs retained Buy, lowered target from $18.70 to $16.05 (-14.2%). Highlighted margin risk remains the key focus and expects only modest sequential improvement

By Warren Masilamony

Breville target price higher on solid 1H26 result

[1:03 pm] Breville shares managed to close 1.7% higher on Thursday, despite falling as much as ~7% intraday. The 1H26 result was in line at EBIT, with gross margin resilience from supply chain diversification and tariff mitigation supporting FY26 guidance and a constructive outlook despite softer regional sales.

RBC Capital Markets retained Sector Perform, raised target from $32 to $34 – EBIT in line with expectations, with gross margin outperformance offsetting top-line softness; US tariff impact easing and FY26 guidance implies ~6% upgrade to 2H26 consensus, though near-term catalysts remain limited.

Goldman Sachs retained Buy, raised target from $37 to $37.60 – EBIT in line and gross margins beat via tariff management and localisation; US sales tailwinds from Best Buy partnerships and inventory aligned with manufacturing transition support outlook.

JPMorgan retained Overweight, raised target from $35.50 to $36.50 – FY26 EBIT ahead of expectations with sequential margin improvement, driven by coffee strength, US growth, localisation and productivity gains; elevated inventory expected to unwind in 1H27.

Analysts broadly positive on Origin's 1H26 result

[1:01 pm] Origin Energy shares closed 7.4% higher yesterday after a strong H1, led by an Energy Markets electricity beat, with brokers highlighting upgraded EBITDA guidance and a constructive outlook despite weaker Integrated Gas and a larger Octopus loss.

RBC Capital Markets retained Sector Perform, target unchanged at $13.50 – Energy Markets EBITDA exceeded expectations driven by electricity tariff repricing and lower green scheme costs, while Integrated Gas declined less than forecast and Octopus losses reflected seasonality; FY26 guidance upgraded overall on stronger electricity and gas margins.

Jarden upgraded to Overweight from Neutral, raised target from $11.65 to $12 – Electricity gross profit and lower coal costs support a 6.5% FY26 Energy Markets upgrade, with APLNG outperforming expectations and Octopus losses manageable, though regulatory clarity remains key for future investment.

UBS retained Buy, target unchanged at $14 – Energy Markets EBITDA 6% ahead of consensus, with electricity margins strong and multi-year upside from customer growth and battery earnings; FY26 guidance reflects stronger gas/LNG trading partially offset by Octopus performance, and Origin seen as a preferred utility for dividend and growth potential.

Analysts slash Pro Medicus target

[12:59 pm] Pro Medicus shares closed 23.8% lower yesterday after a modest H1 earnings miss driven largely by contract timing, with analysts arguing the sell-off reflects lofty pre-result valuation and sector-wide AI de-rating rather than any deterioration in the company’s durable, recurring-growth outlook.

Bell Potter retained Buy, lowered target from $320 to $240 – Revenue miss seen as poorly timed amid AI-driven market sensitivity, with cost growth and pricing-related contract losses weighing on near-term earnings, but long-term growth outlook remains intact and AI risk viewed as overstated.

E&P retained Neutral, lowered target from $247 to $228.83 – Sell-off attributed to sector-wide AI fears rather than fundamentals, with earnings skew considered timing-related and stronger second-half operational performance expected as product expansion broadens beyond radiology.

RBC Capital Markets retained Sector Perform, lowered target from $225 to $190 – AI fears and FX headwinds dominating sentiment, with some competitive losses linked to premium pricing, but strong hospital relationships and regulatory barriers expected to limit long-term disruption risk.

Silver stocks follow the commodities sell-off

[11:42 am] Silver equities are getting hit after spot silver slumped 10% overnight to US$75/oz.

Ticker | Company | % Chg | Price |

|---|---|---|---|

USL | Unico Silver | -9.72% | $0.82 |

IVR | Investigator Silver | -8.33% | $0.11 |

ARD | Argent Minerals | -8.11% | $0.03 |

MMA | Maronan Metals | -7.60% | $0.46 |

ASL | Andean Silver | -7.21% | $1.87 |

SS1 | Sun Silver | -7.00% | $1.86 |

SVL | Silver Mines | -6.52% | $0.22 |

POL | Polymetals Resources | -5.14% | $1.02 |

By Warren Masilamony

Lithium stocks retreat

[11:28 am] Lithium stocks are sharply lower, despite a slight uptick in Chinese lithium carbonate futures on Thursday (+3.6%).

Ticker | Company | % Chg | Price |

|---|---|---|---|

MIN | Mineral Resources | -3.21% | $51.87 |

IGO | IGO | -4.31% | $8.34 |

PLS | PLS Group | -4.40% | $4.24 |

LTR | Liontown | -4.47% | $1.67 |

By Warren Masilamony

Gold stocks routed

[11:12 am] ASX gold miners are broadly lower today, tracking the overnight weakness of gold prices, which fell 3.3% to USD4,938/oz.

Ticker | Company | % Chg | Price |

|---|---|---|---|

VAU | Vault Minerals | -7.90% | $5.36 |

BGL | Bellevue Gold | -6.20% | $1.74 |

GMD | Genesis Minerals | -6.18% | $6.76 |

CMM | Capricorn Metals | -6.15% | $13.20 |

EMR | Emerald Resources | -5.55% | $6.47 |

ALK | Alkane Resources | -5.05% | $1.51 |

RMS | Ramelius Resources | -4.80% | $4.47 |

OBM | Ora Banda Mining | -4.69% | $1.22 |

WGX | Westgold Resources | -4.36% | $7.02 |

CYL | Catalyst Metals | -4.16% | $7.37 |

By Warren Masilamony

Cochlear, Nick Scali and Webjet all down double digits

[11:05 am] Cochlear (-15.6%) is trading sharply lower after its 1H26 result missed.

Revenue up 1% to $1.18bn vs ests $1.22bn (3% miss)

Underlying NPAT down 9% to $194.8m vs ests $199.7m (2% miss)

Cochlear implants 27,016 units vs ests 27,568 (2% miss)

Interim dividend of 215 cps vs. Morgans ests of 218 cps (1.3% miss)

Nick Scali (-17.9%) is also sharply lower despite beating 1H26 estimates.

Revenue up 7.2% to $269.3m vs ests $267.5m (1% beat)

EBITDA up 18.1% to $96.6m vs ests $90.2m (7% beat)

NPAT up 23.1% to $41.0m vs ests $38.0m (8% beat)

It appears the trading update was disappointing, with like-for-like sales growth of 3.2% a miss and January like-for-like sales down 8.6% flagged as a key concern.

Webjet (-24.5%) has also tumbled after takeover discussions with Helloworld and BGH ended. The company also cut its guidance from $30-32m to $28-29m.

Alkane posts record H1 on gold and antimony surge

[10:57 am] Alkane Resources delivered record H1 revenue and earnings, supported by higher production, strong realised prices and a step up in cash generation.

Revenue up 233% to $404m

NPAT up 392% to $64.9m

Adjusted net profit up 445% to $72.5m

Adjusted EBITDA up 384% to $184.7m

Cash generated from operating activities up 418% to $153.8m

Sales benefited from a much higher realised gold price, supporting revenue despite cost pressure.

Gold equivalent sales of 74,094oz generated $404m revenue at an average realised gold price of $5,421/oz (55% higher) and antimony price of $41,023/t

H1 production of 72,732oz gold and 391t antimony

Unit costs broadly stable with cash operating costs up 4.7% to $2,106 per AuEq oz

AISC up 4.6% to $2,841 per AuEq oz

FY26 guidance reiterated, but AuEq production range lowered to 155-168koz, midpoint 161.5koz (3.6% cut vs prior midpoint 167.5koz from 160-175koz). AISC reaffirmed at $2,600-2,900 per AuEq oz, growth and exploration capex $78-88m.

By Warren Masilamony | Company page: Alkane Resources (ALK)

Top ASX 200 gainers and losers

[10:25 am] AMP is bouncing after yesterday's ~30% selloff, GQG higher on a solid 2025 result (and very defensive positioning). Meanwhile, Austal gutted on a guidance downgrade, Cochlear missed 1H26 expectations and Nick Scali's 1H26 was a solid beat (but margins might've been a little soft vs. high expectations).

Ticker | Company | % Chg | Price |

|---|---|---|---|

AMP | AMP | 6.41% | $1.36 |

GQG | GQG Partners | 4.04% | $1.68 |

NXT | NextDC | 3.92% | $14.05 |

ORG | Origin Energy | 3.57% | $11.91 |

IAG | Insurance Australia Group | 2.28% | $6.96 |

CLW | Charter Hall Long Wale Reit | 2.02% | $3.80 |

HDN | Homeco Daily Needs Reit | 1.95% | $1.31 |

WBC | Westpac | 1.84% | $41.76 |

SNZ | Summerset Group | 1.82% | $9.50 |

ASX | ASX | 1.52% | $55.27 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

ASB | Austal | -23.45% | $4.83 |

COH | Cochlear | -14.31% | $210.49 |

NCK | Nick Scali | -12.65% | $20.78 |

WTC | Wisetech Global | -12.60% | $41.58 |

ZIM | Zimplats | -7.69% | $19.93 |

XYZ | Block | -7.27% | $70.05 |

VAU | Vault Minerals | -7.22% | $5.40 |

360 | Life360 | -6.29% | $22.95 |

CMM | Capricorn Metals | -6.26% | $13.18 |

SLX | Silex Systems | -6.25% | $6.60 |

Tech continues to tumble into the abyss

[10:22 am] The S&P/ASX 200 Tech Index is down 4.7%, now trading below last Friday's low to levels not seen since November 2023.

Ticker | Company | % Chg | Price |

|---|---|---|---|

WTC | Wisetech | -11.80% | $41.96 |

SDR | Siteminder | -7.29% | $3.56 |

360 | Life360 | -6.70% | $22.85 |

TNE | Technology One | -5.94% | $20.41 |

AD8 | Audinate Group | -5.60% | $3.71 |

NXL | Nuix | -4.69% | $1.38 |

XRO | Xero | -4.15% | $73.73 |

MP1 | Megaport. | -3.99% | $10.58 |

OCL | Objective Corporation | -3.36% | $12.96 |

HSN | Hansen Technologies | -3.32% | $4.37 |

WBT | Weebit Nano | -3.21% | $5.12 |

DTL | Data#3 | -3.04% | $9.25 |

PPS | Praemium | -2.90% | $0.67 |

BVS | Bravura Solutions | -2.73% | $2.14 |

Nick Scali 1H26 delivers strong ANZ growth, UK recovery underway

[9:50 am] Nick Scali reported solid half-year results, led by strong sales and margin expansion in Australia and New Zealand, with UK performance improving following store refurbishments.

Revenue up 7.2% to $269.3m vs ests $267.5m (1% beat)

EBITDA up 18.1% to $96.6m vs ests $90.2m (7% beat)

NPAT up 23.1% to $41.0m vs ests $38.0m (8% beat)

Statutory NPAT up 36.4% to $41.0m

Fully franked interim dividend up 30% to 39 cps

ANZ: written sales orders up 10.5% to $229.8m, Like-for-like sales up 10.1%, gross margin up 150 bps to 65.9%

UK: written sales orders of $21.7m, revenue $17.6m impacted by store refurbishments, gross margin 59.2% (up from 45.1%)

Expansion ongoing: six new ANZ stores planned for FY26, several UK store opportunities under negotiation

Note: NCK upgraded its 1H26 guidance back in late December, guiding to ANZ revenue growth of 10-12% (from previous guidance of 7-9%), and statutory NPAT of $37-39m (vs. prior $33-35m). Today's numbers have both slightly topped those guidance figures.

Company page: Nick Scali (NCK)

Webjet ends takeover talks, cuts FY26 guidance

[9:44 am] Webjet has ceased discussions with potential acquirers and will now focus on executing its FY30 growth plan, supported by a modest FY26 EBITDA outlook and a share buy-back.

Takeover discussions with Helloworld and BGH Capital have ended, no binding proposals received

FY26 underlying EBITDA expected $28-29m, excluding Webjet Business Travel, which will reduce EBITDA by ~$0.6-0.9m in 2H26

The prior FY26 underlying EBITDA guidance was $30-32m, so this represents an 8% downgrade at the midpoint

Encouraging trends post-OTA brand relaunch, with higher brand awareness and revenue per booking. However, "Webjet's challenging trading environment has continued in 2H26."

On-market share buy-back program of up to $25m now commenced

Company page: Webjet (WJL)

GQG Partners FY25 solid operating leverage and diversified growth

[9:41 am] GQG Partners reported solid full-year results, supported by rising FUM, disciplined cost management, and strong operating margins.

Net revenue up 6.3% to $808.3m vs ests $815.2m (1% miss)

Driven by higher management fees from 10.8% FUM growth to US$164.3bn

Net income up 7.3% to $463.3m vs ests $459.6m (1% beat)

Net operating income $622.5m vs ests $619.5m (1% beat)

Q4 dividend $0.0365 cents per CDI

Closing FUM up 7.1% to $163.9bn vs. Macquarie ests of $166.0bn (1.2% miss)

FUM well diversified: International US$71.4bn, Emerging Markets US$40.8bn, Global US$36.8bn, US Equity US$14.9bn

Over 98% of revenues asset-based, fee realisation 48.4bps, supporting competitive margins and reduced margin pressure vs peers

Overall, the results reads relatively in-line. Though some interesting comments/observations from Macquarie (Jan-26):

"GQG is currently overweight Consumer Staples (+17.9% overweight), Utilities (+12.1%), and Energy (+5.9%). In contrast, GQG is underweight Technology (-18.7% underweight), Consumer Discretionary (-9.1%), and Industrials (-5.8%)."

"GQG is heavily underweight Technology stocks as it believes the AI-linked rally is comparable to the “dotcom‑era” bubble."

"While we see downside risk to Consensus earnings due to continued net outflows, the stock appears to price in most of this risk. With our revised TP implying 12.1% TSR."

Company page: GQG Partners (GQG)

Westpac 1Q26 tops expectations

[9:30 am] Westpac reported a robust start to FY26, underpinned by lending expansion, strong capital, and ongoing digital and productivity initiatives.

Net interest income up 2% to $5.0bn vs ests $5.02bn (in-line)

NIM down 1 bp to 1.94% vs. 1.93% ests (1 bp beat)

Net profit ex-items $1.9bn vs ests $1.80bn (6% beat)

This represents a 6% increase on 2H25 average

Deposit growth of $12bn and lending growth of $22bn

CET1 ratio 12.3% vs target 11.25%

Interim initiatives include UNITE, BizEdge, Westpac One rollout, AI training for all staff, and sale of RAMS mortgage portfolio

FY26 productivity savings target over $500m, with focus on simplification, digital transformation, and improved customer service

Overall, a very strong but unsurprising result, since CBA and ANZ both reported stronger-than-expected results in the past few days. The lookthrough from CBA and ANZ has already helped Westpac shares rally 4.3% in the last two sessions to fresh all-time highs.

Company page: Westpac (WBC)

Cochlear 1H26 affected by Nexa launch delays, strong H2 expected

[9:25 am] Cochlear delivered a soft first half with underlying NPAT slightly below market expectations, reflecting extended registration and contracting for the new Nexa System.

Revenue up 1% to $1.18bn vs ests $1.22bn (3% miss)

Underlying NPAT down 9% to $194.8m vs ests $199.7m (2% miss)

Cochlear implants 27,016 units vs ests 27,568 (2% miss)

Interim dividend of 215 cps vs. Morgans ests of 218 cps (1.3% miss)

FY26 guidance underlying NPAT $435-460m, likely at lower end due to first-half delays and FX impact (~$30m reduction if AUD stays at current levels)

Consensus sits at ~$433m, so not a big surprise by all means

Strong second half expected from broad Nexa availability, growth in Services, and improved momentum in Acoustics

A few random observations: Just had a flick through some slightly dated analyst models (Morgan Stanley Oct-25), where they have FY26 gross margins forecasts of 73.8% vs. today's outlook commentary of "around 73%". In FY25, Cochlear's first half generated approximately ~52% of NPAT, while today's announcement/result has 1H26 NPAT of just 44% of the FY26 guidance (assuming $435m NPAT).

Company page: Cochlear (COH)

Civmec delivers steady 1H26 with growing order book

[9:18 am] Civmec reported solid half-year results for 1H26, underpinned by stable margins and an expanding order book.

Revenue of $380.4m vs ests $379.8m (in-line)

EBITDA of $46m vs ests $42.8m (7% beat)

NPAT of $21.4m vs ests $20.7m (3% beat)

Interim dividend flat at 2.5 cents, fully franked

Order book grows to $1.35bn from $1.25bn, driven by new contracts and early contractor involvement projects

Company page: Civmec (CVL)

Austal trims FY26 EBIT guidance

[9:14 am] Austal identified a US$17.1 million overstatement in incentives for its T-ATS program recognised by Austal USA, previously included in full-year EBIT forecasts. As a result, the company now updates its FY26 EBIT guidance to approximately $110 million.

Consensus for FY26 EBIT currently sits at $130 million, so the new guidance represents a ~15% miss. It isn't exactly a downgrade or deterioration in business conditions ... but it does read like a net negative I guess?

Company page: Austal (ASB)

ASX announcements and results coverage

[9:12 am] That pretty much wraps up the overnight stuff. I'll be trawling through as many earnings as I can before the market opens. At a glance, Westpac (like all the other banks) has smashed 1Q26 expectations, Cochlear a broad miss and Austal is guiding to lower than expected earnings.

Macquarie exits Star Entertainment debt

[9:10 am] The AFR reports that Macquarie sold its entire exposure to Star Entertainment Group, leaving Soul Patts as the largest creditor and signalling a shift in the casino operator’s capital structure.

Soul Patts acquired Macquarie’s debt at around 94-95 cents in the dollar, raising its stake to roughly 50% of Star’s debt alongside smaller positions held by Regal, AlphaWave and Perpetual

Macquarie’s exit marks the end of significant bank participation in Star’s capital stack

Westpac’s remaining exposure is limited to $34.5m in bank guarantees

Star is preparing a new refinancing under its recently appointed management team, with MA Moelis replacing UBS as house bankers

Syndicated debt totals $354m with an all-in cost of 15%, secured against Gold Coast assets, with maturity in December 2027

I haven’t followed this closely, but based on my experience, Soul Patts has delivered some solid debt outcomes, such as with Aeris Resources and Electro Optic Systems. Might take a closer look later on in the day.

Company page: Star Entertainment Group (SGR)

Real estate services hit by AI fears

[9:05 am] Shares of major commercial real estate firms fell sharply as investors weighed potential disruption from AI tools, despite limited immediate impact on complex deal-making.

CBRE and Jones Lang LaSalle shares dropped 12%, Cushman & Wakefield down 14%, marking the largest falls since 2020 for CBRE and Cushman

Investors rotating out of high-fee, labour-intensive models seen as vulnerable to AI-driven automation, though short-term risk remains limited

Sector still struggling post-pandemic amid weak office demand and higher interest rates, with AI potentially pressuring tasks and deal processes

Analysts note the selloff may be overblown, with scale, industry relationships, and role as intermediaries in large transactions limiting AI’s immediate impact

Source: Bloomberg

RBA signals data-driven approach amid persistent inflation

[9:00 am] A Bloomberg article notes how the RBA is prepared to raise rates further if inflation remains high, stressing caution and ongoing assessment of economic data.

RBA Governor Michele Bullock said inflation “with a three in front of it” is unacceptable and further hikes are possible if inflation proves entrenched

Last week’s rate increase marked the first among major central banks this year, with forecasts suggesting headline and core inflation will exceed the 2–3% target in 2026

Economic growth constrained by weak productivity, with Bullock noting Australia may struggle to grow above 2% annually without triggering inflation pressures

Consumer inflation expectations jumped to 5% in February, the highest since June 2025, while unemployment remains low at 4.1% (full employment estimated at 4.6%)

Next RBA meeting in mid-March will incorporate January employment and inflation data and Q4 GDP, with economists widely expecting a May rate hike to 4.1% from 3.85%

Source: Bloomberg

Unilever flags slower 2026 growth as US and Europe soften

[8:57 am] A small handful of interesting results overnight (McDonalds rallied, Cisco tumbled, Birkenstock slipped) but Unilever stands out as the most interesting given its broad macro commentary and guidance. The multinational consumer packaged goods company said it expects sales growth at the low end of guidance despite strong emerging market performance and cost-of-living pressures in developed markets.

2026 underlying sales growth expected at 4%–6%, likely at the bottom end due to softer conditions in the US and Europe

Fourth-quarter underlying sales up 4.2% versus 3.9% ests, driven by emerging markets including India, Indonesia, and China

North America sales grew 2.8%, Europe 0.1%, both slowing from Q3, though market share gains continued in North America

CEO Fernandez signals modest price rises of ~2% in 2026, below the 3% decade average, while a €1.5bn ($1.8bn) share buyback supports shareholder returns

Energy sector in a rotational bull market says BofA

[8:55 am] Bank of America sees strong rotation into energy but warns valuations are constrained by supply dynamics and capital limitations.

XLE outperformed the S&P 500 by 13% in January as investors rotated out of large-cap tech due to overspending concerns

Global oil remains oversupplied by ~2.5m b/d despite OPEC+ pausing cuts, with Brent gains largely driven by short-term Iran-related risks

WTI expected to remain range-bound around $60/bbl, supported by continued Iranian supply and emerging Venezuelan production declines

Valuations for oil and gas are anchored to free cash yields rather than revenue growth, limiting scope for multiple expansion

Bank sees more attractive opportunities in mid-cap names including DVN, CTRA, OVV, and CRC, as upside in large-caps becomes increasingly constrained

AI automation fears hit trucking stocks

[8:54 am] Investor concern over new AI freight optimisation tools triggered a sharp sell-off across major US trucking and logistics names, despite mixed fundamental implications.

C.H. Robinson fell 14.5%, RXO dropped 20.5%, Expeditors declined 13.2%, XPO lost nearly 6% and J.B. Hunt fell about 5% amid fears AI could compress industry demand

Algorhythm’s SemiCab platform claims customers can scale freight volumes 300% to 400% without adding headcount and cut empty miles by more than 70%, targeting a market where trucks run empty nearly one in three miles

The company argues coordinated network management materially improves asset utilisation, framing AI as structurally deflationary for freight inefficiencies and potentially industry margins

Baird reiterated outperform ratings on C.H. Robinson and Expeditors, noting automation is not new and suggesting incumbent operators may adapt rather than be displaced

Source: CNBC

US IPO momentum stalls as tech debuts slump

[8:52 am] Recent tech-linked IPOs are trading poorly, forcing valuation cuts and raising doubts ahead of major listings later this year.

More than half of the 15 US IPOs that raised over $100m each are now below issue price, with five stocks down at least 15% from their offer levels

Clear Street cut its IPO size to $364m from up to $1.05bn, a 65% reduction, with implied valuation above $7bn versus $12bn in a private round last month, around a 42% step down

Blackstone-backed Liftoff postponed its IPO after peers AppLovin and Unity fell more than 40% in the lead up, highlighting fragile tech sentiment

Brazilian fintech AGI scaled back ambitions after peer PicS dropped following its late January IPO, reinforcing weak appetite for fintech listings

Source: Bloomberg

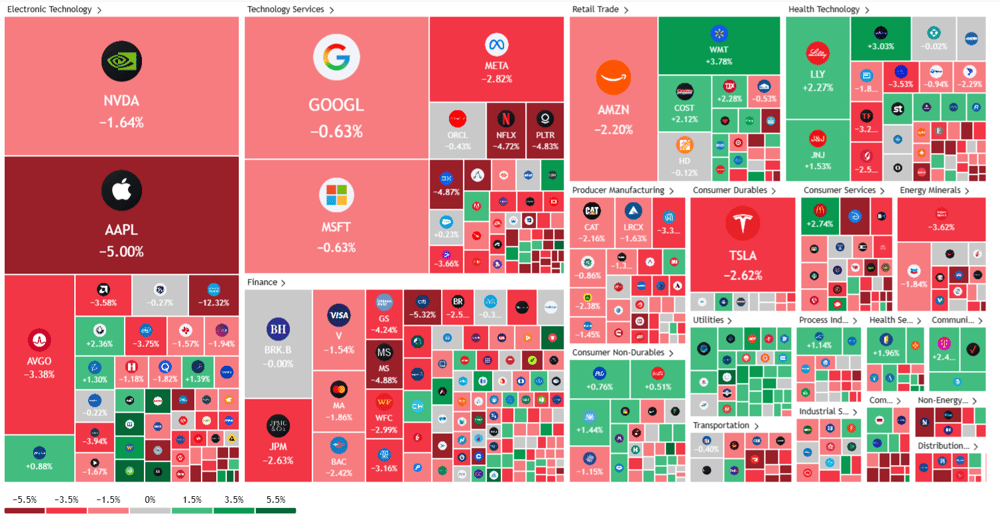

Tech and cyclicals dip, defensives shine

[8:49 am] Mag-7 led the decline, with a notable 5% dip from Apple. Defensives outperformed by a wide margin, with sectors like Utilities (+1.5%), Staples (+1.2%), Real Estate (+0.3%) and Healthcare (+0.06%) trading higher, while the rest (Industrials, Telcos, Materials, Discretionary, Financials, Energy and Tech) all fell more than 1.0%. So a very big spread between winners and losers.

AI is becoming an increasingly broader market headwind amid:

Mag-7 capex is soaring, shifting them from asset-light to asset-heavy with minimal cashflows moving forward

AI concerns has smashed the software sector, now spreading to other sectors like commercial real estate brokers, insurance brokers and trucking/logistics

Memory headwinds is weighing on margins, with Cisco the latest victim

S&P 500 heatmap (Source: TradingView)

Wall Street weakness, commodities tumble and more results

[8:41 am] Not the busiest morning, though a very weak lead from Wall Street. We'll take a look at some key overnight headlines and data points, before moving on to the handful of companies that report today (ALK, BWP, CEH, COH, DSK and NCK).

Good morning!

[8:29 am] ASX 200 futures are down 67 pts (-0.75%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks broadly lower and finished near worst levels

S&P 500 (-1.57%), Dow (-1.34%), Nasdaq (-2.03%) and Russell 2000 (-2.19%)

Risk-off session, with Mag-7 stocks trading sharply lower amid continued capex and cash flow concerns, software stocks continue to tumble into oblivion and now AI fears spreading to trucking and logistics

Commodity prices experienced a broad and abrupt selloff around ~3 am AEDT, driving resource stocks sharply lower

To catch up on all overnight developments, check out today's Morning Wrap.