Morning Wrap: ASX 200 futures flat, S&P 500 slips, Oil prices soar past US$100 a barrel

ASX 200 futures are down 4 pts (-0.03%) as of 8:30 am AEST.

In this article

ASX 200 futures are down 4 pts (-0.03%) as of 8:30 am AEST.

In a nutshell:

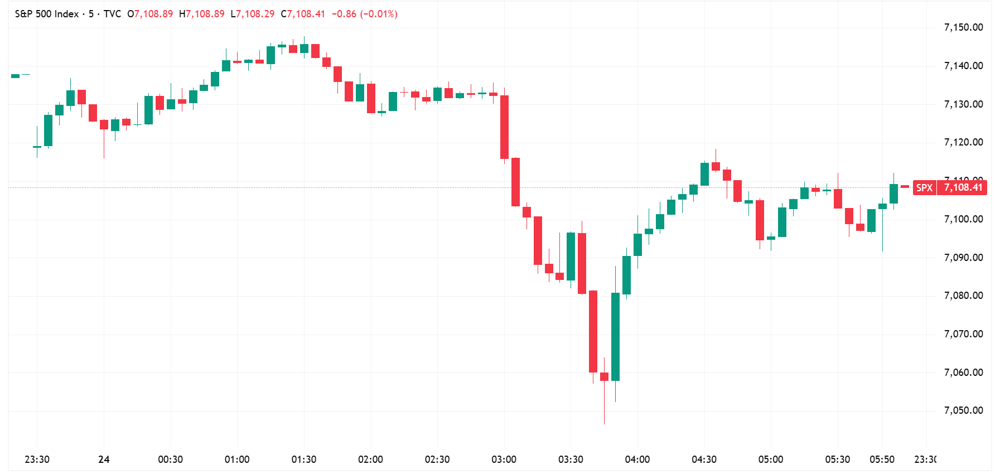

US indices lower but off worst levels, with the S&P 500 (-0.41%) bouncing off session lows of -1.28%

A strong session for defensives, with sectors like Utilities, Industrials, Staples and Real Estate all up at least 1%

Lots of Iran-related headline noise, spanning Iran leadership uncertainty, continued Trump threats and concerns of more Iranian mines in the strait

Brent up 4.4% to US$106.02 to the highest since 7 Apr, prices have now rallied 13% in the last three sessions

Let's dive in.

Overnight Summary

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

S&P 500 | 7,108 | -0.41% |

Dow Jones | 49,310 | -0.36% |

NASDAQ Comp | 24,439 | -0.89% |

Russell 2000 | 2,775 | -0.37% |

Country Indices | ||

Canada | 33,913 | -0.12% |

China | 4,093 | -0.32% |

Germany | 24,155 | -0.16% |

Hong Kong | 25,915 | -0.95% |

India | 77,664 | -1.09% |

Japan | 59,140 | -0.75% |

United Kingdom | 10,457 | -0.19% |

Name | Value | % Chg |

|---|---|---|

Commodities (USD) | ||

Gold | 4,696.78 | -0.91% |

Copper | 6.02 | -1.56% |

WTI Oil | 95.85 | +3.11% |

Currency | ||

AUD/USD | 0.713 | +0.02% |

Cryptocurrency | ||

Bitcoin (USD) | 78,063 | -0.73% |

Ethereum (AUD) | 3,265 | -3.05% |

Miscellaneous | ||

US 10 Yr T-bond | 4.323 | +0.68% |

VIX | 19.31 | +2.06% |

US Sectors

Sector | % Chg |

|---|---|

| Utilities | +2.80% |

| Industrials | +1.75% |

| Consumer Staples | +1.74% |

| Real Estate | +1.28% |

| Energy | +0.76% |

| Health Care | -0.10% |

Sector | % Chg |

|---|---|

| Materials | -0.22% |

| Communication Services | -0.38% |

| Financials | -0.79% |

| Consumer Discretionary | -0.93% |

| Information Technology | -1.47% |

S&P 500 SESSION CHART

S&P 500 lower but well-off worst levels (Source: TradingView)

OVERNIGHT MARKETS

Major US benchmarks lower, finished well-off worst levels, as software stocks plunged and oil surged on renewed Iran war concerns

Markets anxious after oil prices up for a third straight session, Brent settled 4.4% higher to US$106.02 a barrel after Iran demanded permission for ships to cross Hormuz, while Trump said the US has "total control" of the strait

A fairly resilient session all things considered, S&P 500 (-0.41%) off session lows of -1.28%, Equal-weight S&P 500 (0.00%) flat amid a defensive pivot into Utilities, Industrials, Staples and Real Estate, all of which rallied more than 1%

iShares Expanded Tech-Software ETF dipped 5.8% after an 18.8% rally in the prior eight sessions

Lots of Iran-related headline noise, including Iranian leadership uncertainty, wild Trump threats and reports of Iran deploying more mines in the Strait

PHLX Semiconductor Index records 17-day winning streak, most extended above 200-day moving average since 2000, with chips adding over US$3 trillion in market cap in 17 trading days (YF)

ENERGY

IEA chief Fatih Birol called Iran war the "biggest energy security threat in history", said 13 million barrels a day are gone "with no cure in sight" (F)

Jet fuel prices in North America up 95% since war began, Lufthansa slashed 20,000 flights, United Airlines raising fares by up to 20% on jet fuel shortages

Pentagon told Congress clearing Iranian mines in Strait of Hormuz could take up to six months, further jeopardizing transit

Only 3 tankers moved through Strait of Hormuz Wednesday (5 ships total), vs. pre-war average of 129 per day per UN Trade and Development data

New data shows China came into the Iran war with over 3x the strategic oil reserves of the US (YF)

IRAN

Iranian parliament speaker Ghalibaf reportedly resigns from negotiation team amid internal rift (TI)

Trump orders US Navy "to shoot and kill any boat" that is laying mines in the Strait of Hormuz (CNBC)

Israel's defence minister Katz says Israel waiting for 'green light' to renew war against Iran (TI)

Iran's Revolutionary Guard is sidelining Iranian president, expanding grip on internal decision making (WSJ)

STOCKS

Avis Budget stock has plunged more than 62% in two days after a nearly 600% climb since late March (BBG)

Intel Q1 FY26 revenue up 7% to $13.6bn, ~10% ahead of consensus, EPS $0.29 vs -$0.01 expected, Q2 guidance $13.8-14.8bn vs $13.07bn consensus, shares up ~18% after-hours (CNBC)

ServiceNow Q1 FY26 subscription revenue up 22% to $3.67bn, EPS $0.97 vs $0.96 expected, raised FY26 subscription guidance to $15.74-15.78bn, shares sank ~17% as Iran war hit bookings (CNBC)

IBM Q1 FY26 revenue up 9% to $15.92bn, ~2% ahead of consensus, EPS $1.91 vs $1.81 expected, raised software growth outlook to >10% but held full-year guidance, shares down ~8% (CNBC)

American Express Q1 FY26 revenue up 11% to $18.91bn, ~2% ahead of consensus, EPS $4.28 beat by ~7%, billed business up 10% to $428bn, luxury retail up 18%, shares fell over 4% on investment plans (YF)

Meta confirmed layoffs of 10% of workforce or ~8,000 employees, to free capital for AI investments (CNBC)

Microsoft announced first-ever voluntary employee buyout targeting 7% of US workforce at senior director level (CNBC)

KPMG cutting 10% of US audit partners (FT)

TARIFFS & TRADE

Joint Economic Committee Democrats released report saying Trump's tariffs have cost over 100,000 US manufacturing jobs and cut small manufacturer profit margins by 11% since "Liberation Day" (JEC)

CENTRAL BANKS

Markets still price one Fed cut in 2026, with next FOMC meeting April 28-29 expected to hold at 3.50-3.75% range (JPM)

ECONOMY

US S&P composite PMI rebounded to 3-month high of 52.0 in April from 50.3, manufacturing surged to 54.0 (48-month output high), services up to 51.3, though confidence remains historically low (FXS)

Eurozone April composite PMI fell into contraction at 48.6 vs 50.1 expected, services collapsed to 47.4 vs 49.8 expected, manufacturing surprised at 52.2 vs 50.9 (ING)

HCOB chief economist said Eurozone April PMI signals 0.1% quarterly GDP decline, services hit by war worst since pandemic lockdowns, output price inflation at 37-month high (investingLive)

Industry ETFs

Name | Value | % Chg |

|---|---|---|

Commodities | ||

| Steel | 101.29 | -1.29% |

| Uranium | 56.47 | -2.18% |

| Gold Miners | 92.19 | -2.42% |

| Silver | 68.38 | -2.83% |

| Copper Miners | 82.46 | -2.87% |

| Lithium & Battery Tech | 82.15 | -3.09% |

| Strategic Metals | 98.24 | -5.36% |

Industrials | ||

| Construction | 107.65 | +1.00% |

| Agriculture | 27.4 | +1.00% |

| Aerospace & Defense | 219.11 | -0.02% |

| Global Jets | 25.72 | -0.62% |

Healthcare | ||

| Biotechnology | 171.53 | -1.62% |

Name | Value | % Chg |

|---|---|---|

Cryptocurrency | ||

| Bitcoin | 10.68 | -1.29% |

Renewables | ||

| Solar | 58.6 | +2.75% |

| CleanTech | 66.4811 | -0.43% |

| Hydrogen | 51.2 | -0.51% |

Technology | ||

| Semiconductor | 441.0 | +2.14% |

| Sports Betting/Gaming | 18.9662 | +0.45% |

| Electric Vehicles | 35.5 | -0.80% |

| Robotics & AI | 36.66 | -1.90% |

| E-commerce | 28.49 | -2.03% |

| Video Games/eSports | 91.63 | -3.05% |

| FinTech | 25.57 | -3.98% |

| Cloud Computing | 19.49 | -4.41% |

| Cybersecurity | 26.19 | -4.45% |

ASX TODAY

Iress guides FY26 revenue landing towards bottom of its $520-582m range, remains confident in delivering 25% cash EBITDA exit run rate by Q4 (IRE)

PLS Group reports March quarter production up 12% to 232.4kt, revenue up 52% to $567m, cash balance up 52% to $1.45bn (PLS)

Qoria reports Q3 exit ARR up 20% year-on-year to $151m, net outflow of $4.7m for the quarter (QOR)

Suncorp enters 5-year aggregate reinsurance arrangement, will provide $800m of protection annually for up to $2.4bn, expects underlying Insurance Trading Ratio to be towards upper end of 10-12% range vs. prior top half of the 10-12% range (SUN)

WHAT TO WATCH TODAY

Front running resource weakness: Most of our overnight resource-related ETFs lower, with Uranium, Gold and Copper Miners, Nickel and Rare Earths/Strategic Metals down 2-5%. Though the local market has already priced-in this softness (e.g. yesterday PLS Group down 4.0%, SFR down 3.6% despite opening ~3% higher, PDN up 0.6% also fading big early gains etc.)

Software weakness, defensive strength: Very notable defensive pivot overnight, with the S&P 500 Utilities, Industrials, Staples and Real Estate sectors trading broadly higher. Could see that defensive theme carry over to today's session. Software stocks tanked overnight, though we already started to observe some softness on Thursday, with names like Wisetech (-3.0%) and Xero (-1.7%) lower.

BROKER MOVES

Reliance Worldwide upgraded to Overweight from Neutral; target lowered to $3.65 from $3.75 (JPMorgan)

Sandfire downgraded to Sell from Neutral; target cut to $16.75 from $17.05 (UBS)

Key Events

Stocks trading ex-dividend:

Fri 24 Apr: None

Mon 27 Apr: None

Tue 28 Apr: None

Other ASX corporate actions today:

Dividends paid: Bisalloy Steel (BIS), Cedar Woods (CWP), GenusPlus (GNP), Shine Justice (SHJ)

IPOs: L1 Gold Fund (LGF) – 11:00 am

AGMs: Iress (IRE)

Economic calendar (AEDT):

9:30 am: Japan Inflation

4:00 pm: UK Retail Sales