Markets at Midday: ASX 200 falls to near one-month low ahead of RBA decision

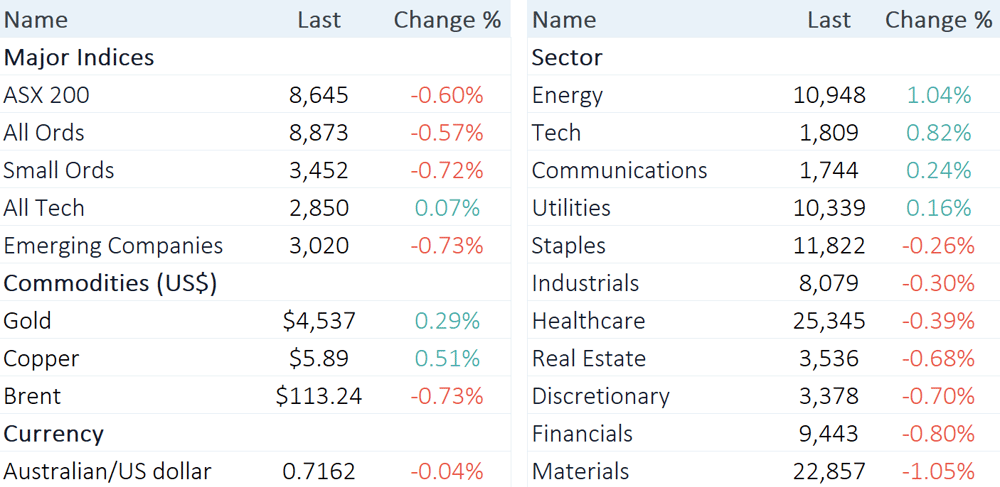

The S&P/ASX 200 is trading 52 pts lower (-0.60%) at noon.

Source: Market Index

The S&P/ASX 200 is trading 52 pts lower (-0.60%) at noon.

Another rough day for markets, ahead of the RBA decision at 2:30 pm AEST. The Index has now undercut the recent 30 April low and trading below the key 200-day moving average for a second session. It's now on track to have fallen in thirteen of the last fourteen sessions.

The Tech sector has bucked the trend thanks to a continued bounce in Nasdaq-listed software stocks, while Energy is also higher after a ~4% spike in oil prices overnight. Soaring energy prices weighed on commodity prices overnight and drove US bond yields notably higher, weighing on local sectors like Materials, Industrials and Real Estate.

Let’s dive in

Midday market summary

Today’s big story: Macquarie Conference Day #1

The Macquarie Conference runs from Tuesday to Thursday, featuring presentations from over 100 mid-to-large cap companies. The sessions explore key macroeconomic themes and trends, but also feature trading updates from the companies – most of which reaffirm the guidance provided at the recent February half-year result.

Here are some of the interesting ones from this morning:

Dexus (-2.8%): " This quarter's results show ongoing improvement in operational performance across our property portfolio, outperformance in our flagship fund, and meaningful progress in attracting capital into the funds platform. However, the shifting macroeconomic environment and interest rate outlook is expected to slow the recovery."

Judo Capital (-1.6%): "Judo completed a detailed customer-by-customer review of the lending portfolio; the vast majority of Judo’s customers remain in good financial health with no observable change in risk profile ... Increased its ECL provision, with a top up of economic overlay related to sectors that are more sensitive to fuel prices and broader economic deterioration including agriculture, construction, retail trade, manufacturing and transport."

Medibank (-0.95%): No change in FY26 outlook, " growth has moderated slightly as expected, increasing participation among younger cohorts continues to support ongoing affordability and long-term industry sustainability."

Nine Entertainment (+3.2%): "Q3 was a strong revenue quarter for the Group ... However, Q4 is being impacted by a confluence of uncertainty - both international and local - which is proving challenging for advertising markets."

Wisetech (+5.7%): Reaffirmed guidance, noted AI adoption is accelerating across platform features. Stock rallied against some analyst concerns of earnings downgrades.

Must read announcements

PEXA Group (PXA): Q3 reaffirms FY26 guidance with NPAT at top end of range

Regis Resources (RRL): Merger-of-equals with Vault Minerals to create 700koz+ gold producer

Sigma Healthcare (SIG): Strong Chemist Warehouse momentum, enters UK market via JV

The Lottery Corporation (TLC): Secures 40-year Victorian licence extension for $1.15bn premium

Westpac (WBC): 1H26 cash earnings and NIM miss on higher impairments and energy sector overlay

Capital raisings

Belararox (BRX): Secures three new strategic investment partners in $4m raise

Dalaroo Metals (DAL): Raises A$1.75m for gold and Greenland REE exploration

Great Boulder Resources (GBR): $40m placement to fund Peak Hill Gold Project

Navigator Global Investments (NGI): Successful completion of institutional entitlement offer

Resource Minerals International (RMI): Successful $3.5m placement to fund Tanzania drill program

SRJ Technologies Group (SRJ): Secures A$2.57m to advance contract pipeline

Tennant Minerals (TMS): Raises capital to advance Bluebird Au-Cu-Bi project

Xamble Group (XGL): $0.67m placement to accelerate YToday integration

Thinking out loud: Retail REITs

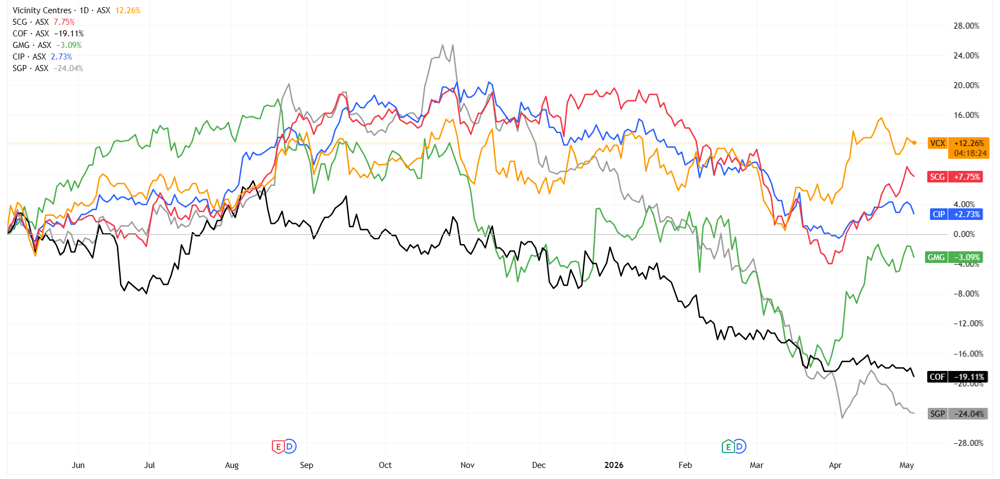

I haven't looked at REITs in a long time – which is why its rather surprising to see retail REITs outperform office, industrial and data centre peers (by a wide margin). The below 12-month charts are on a total return basis.

Vicinity and Scentre Group vs. Centuria Industrial, Goodman, Centuria Office and Stockland over the last twelve months, adjusted for dividends (Source: TradingView)

Some of the recent commentary from the likes of Vicinity and Scentre Group have highlighted high occupancy, solid sales growth among portfolio retail sales, ongoing capital management and reaffirmed guidances.

Vicinity (5-May): Reaffirmed FY26 guidance, with FFO expected to be around the top end of guidance ranges of 15.0-15.2 cents, occupancy at 99.6% and total portfolio retail sales up 3.4% in 3Q26

Scentre Group (22-Apr): Customer visitation year-to-date (19-Apr) is up 3.1% year-on-year, portfolio occupancy of 99.8%, total business partner sales up 5.0% for the 3 months to 31-March and FY26 FFO guidance reaffirmed

Intraday winners and losers

Pinnacle has caught a massive bid after the company acquired an additional 6.8% of equity in Metrics for $100.5 million, Endeavour is trying to bounce off all-time lows, while Magellan was aggressive sold off after announcing plans to close its global equities fund.

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

PNI | Pinnacle Investment Management Group | 6.15% | $16.14 |

DRO | Droneshield | 3.49% | $3.86 |

FBU | Fletcher Building | 3.46% | $2.39 |

CMM | Capricorn Metals | 3.22% | $12.04 |

SRL | Sunrise Energy Metals | 3.19% | $12.92 |

EDV | Endeavour Group | 3.04% | $3.23 |

TLC | Lottery Corporation | 2.62% | $5.68 |

WTC | Wisetech Global | 2.53% | $45.73 |

EOS | Electro Optic Systems | 2.53% | $10.15 |

A2M | A2 Milk Company | 2.23% | $6.65 |

Data as at 12:19 pm AEST, % change measures the move from today's open price

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

MFG | Magellan Financial Group | -6.11% | $9.52 |

CDA | Codan | -5.20% | $39.77 |

REG | Regis Healthcare | -4.99% | $6.48 |

SGM | Sims | -4.85% | $19.83 |

SHL | Sonic Healthcare | -3.50% | $19.16 |

DXS | Dexus | -2.72% | $6.09 |

LYC | Lynas Rare Earths | -2.61% | $18.48 |

CSL | CSL | -2.23% | $123.00 |

YAL | Yancoal Australia | -2.06% | $7.39 |

CBO | Cobram Estate Olives | -2.05% | $3.82 |

Data as at 12:19 pm AEST, % change measures the move from today's open price

Broker moves

Accent Group (AX1)

Downgraded to neutral from buy at Citi; Price Target: $0.57 from $1.25

Retained at hold at CLSA; Price Target: $0.50 from $0.80

Retained at neutral at Jarden; Price Target: $0.70 from $1.20

Retained at underweight at Morgan Stanley; Price Target: $0.55 from $1.04

Retained at sector perform at RBC Capital Markets; Price Target: $0.80 from $1.30

Coles Group (COL)

Downgraded to hold from buy at Bell Potter; Price Target: $22.80 from $22.35

Endeavour Group (EDV)

Retained at outperform at CLSA; Price Target: $4.50 from $4.70

Retained at hold at Jefferies; Price Target: $3.50 from $3.60

Downgraded to underweight from neutral at JPMorgan; Price Target: $3.10 from $3.50

Retained at sector perform at RBC Capital Markets; Price Target: $3.50 from $4.00

Retained at neutral at UBS; Price Target: $3.45 from $3.60

National Australia Bank (NAB)

Upgraded to neutral from negative at E&P; Price Target: $38.00

Upgraded to trim from sell at Morgans; Price Target: $36.10 from $34.56

Retained at buy at UBS; Price Target: $48.50 from $50.50

PEXA Group (PXA)

Retained at outperform at CLSA; Price Target: $16.40 from $17.70

Downgraded to underweight from neutral at Jarden; Price Target: $11.35 from $12.40

Retained at outperform at Macquarie; Price Target: $19.05 from $18.35

Retained at neutral at UBS; Price Target: $15.70

Sonic Healthcare (SHL)

Downgraded to underweight from equal-weight at Morgan Stanley; Price Target: $20.30 from $24.20

Sigma Healthcare (SIG)

Retained at buy at Jarden; Price Target: $3.60

Retained at overweight at JPMorgan; Price Target: $3.50 from $3.40

Retained at sector perform at RBC Capital Markets; Price Target: $2.60 from $2.50

Retained at buy at UBS; Price Target: $3.40 from $3.35

Ventia Services Group (VNT)

Upgraded to outperform from hold at CLSA; Price Target: $6.20 from $6.00