Latest on lithium — an ASX investor’s guide to this year’s boom or bust trade

Lithium prices are surging again — but is this the start of a new boom or a bull trap? Here’s what every ASX investor needs to know now.

Source: Shutterstock, Market Index

Mentioned

KEY POINTS

- Lithium has roared back from a brutal 90% collapse, with prices and ASX stocks rebounding sharply as the commodity cycle turns once again.

- GFEX trading resumes today after the Lunar New Year break as supply disruptions and policy shifts tighten the market — setting up a pivotal moment for lithium pricing in 2026.

- We break down the latest broker insights and market drivers — and what they mean for positioning in ASX lithium stocks right now.

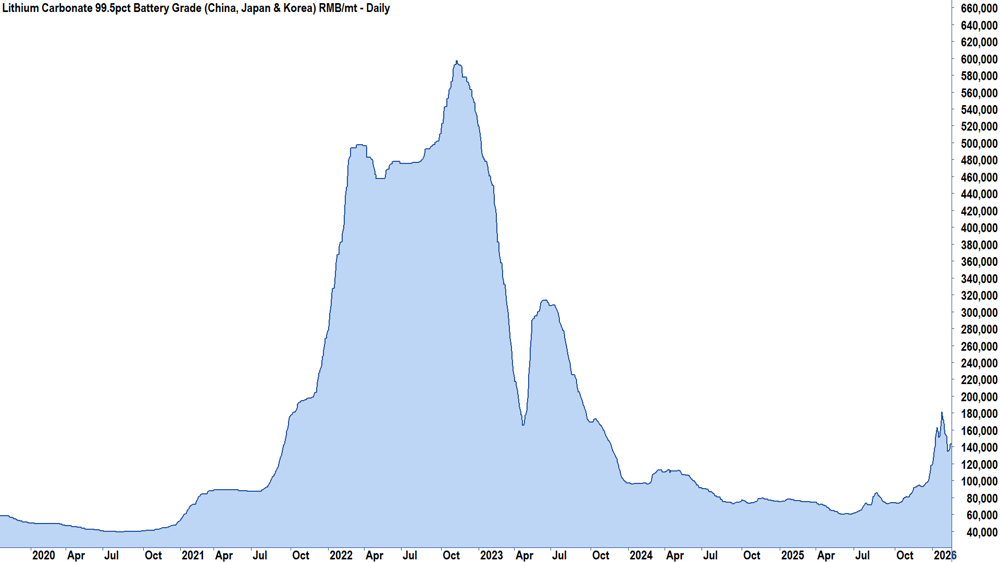

Lithium has a habit of humbling even the most seasoned investors. Just months ago, ASX lithium names like Pilbara Minerals (PLS), Mineral Resources (MIN), and Liontown (LTR) were fighting to preserve margins as prices languished near cycle lows. Fast forward to today, and the script has flipped — spodumene prices have surged more than threefold, cashflows are rebounding, and sentiment has swung sharply back in favour of the sector.

That’s the nature of commodity cycles: brutal on the way down, exhilarating on the way up.

Lithium long-term price cycle chart

But as always, the key question for investors isn’t what has happened — it’s what comes next. And today, that question comes into even sharper focus as China’s Guangzhou Futures Exchange (GFEX) reopens after the Lunar New Year break. Price discovery is back, and the lithium market is once again under the microscope.

To help us unpack where things stand — and where they may be heading — we turn to Macquarie’s latest sector note, “Critical Minerals Chronicle — Emerging from a market vacuum” (20 February 2026), which provides a timely and detailed framework for thinking about the lithium market in 2026.

GFEX reopens: Lithium’s price discovery moment

All eyes are on the reopening of China’s GFEX because this is where lithium prices are increasingly being set.

After more than a week offline during the Lunar New Year holidays, the return of trading restores a critical piece of the market’s price discovery mechanism. As Macquarie notes, “the resumption of GFE trading… should provide an important price reference, with ~50% of global lithium supply estimated to be influenced by futures and spot market dynamics”.

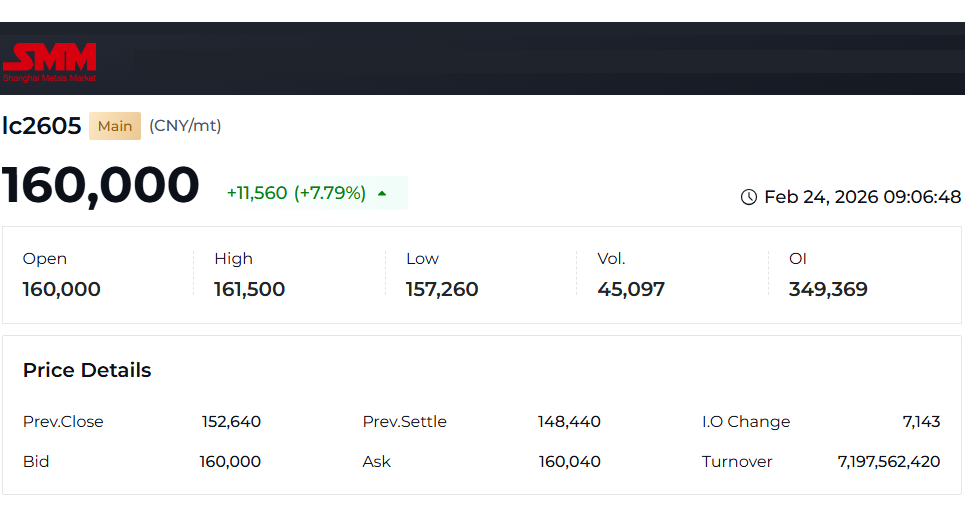

The verdict is in! GFEX lithium prices have reopened strongly following the holiday break. Source: SMM, available from: https://www.metal.com/Lithium/lc2605

That statistic alone underscores why today matters. Pre-holiday, lithium prices corrected sharply lower amid profit-taking and a lack of liquidity. But the broader trend remains one of recovery, with prices still sharply higher year-on-year. The key question now is whether the reopening confirms that strength — or signals that the rally has run out of steam.

For ASX investors, GFEX is more than just a pricing tool — it’s a transmission mechanism.

Producers with direct exposure to spot markets are far more sensitive to movements in lithium futures, and that includes many of the ASX’s key names such as PLS, MIN and LTR. These companies sit closer to the raw material end of the supply chain, meaning changes in spot pricing tend to flow quickly into realised revenues and margins.

By contrast, more vertically integrated operations — such as China’s Contemporary Amperex Technology Co. Limited (CATL) — are less exposed to short-term price swings, as pricing is often internalised within broader value chains.

And on the topic of CATL, perhaps the most important dynamic sitting behind GFEX right now is uncertainty around Chinese supply — particularly from Jiangxi’s lepidolite mining hub, where CATL’s flagship Jianxiawo operation and several other producers are facing regulatory and permitting headwinds.

Macquarie estimates that “up to ~0.3mt of LCE production could be exposed to Jiangxi lepidolite supply uncertainties”, with multiple projects facing permitting delays, regulatory changes, and potential production outages. The prolonged suspension of key operations — including CATL’s Jianxiawo mine — only adds to the fragility of the current supply picture.

Put it all together, and GFEX is not just reflecting the lithium market — it is actively shaping it. Which brings us to the next critical question: do the underlying supply dynamics support the recent price strength?

Latest lithium supply-side factors

If prices are rising, the natural question is: why?

On the supply side, the answer appears to be a mix of constrained production and ongoing disruption risks.

Macquarie highlights that “the near-term supply backdrop remains unchanged, with Australian supply growth yet to materialise and major Jiangxi lepidolite producers still suspended”.

This is crucial. Despite the rally in prices, new supply hasn’t yet responded in a meaningful way — a classic setup for tighter markets.

Inventory trends are reinforcing the tightening narrative, even if the signals vary across the supply chain. While downstream battery and precursor manufacturers built stocks ahead of Chinese New Year, refinery inventories remain near multi-year lows — a dynamic that, as Macquarie notes, “suggests downstream demand has stayed robust”.

At the same time, traders have been unwinding positions built during the depths of the bear market — locking in profits as prices recover. Yet even with this additional supply coming back into the market, the broader supply-side picture remains unchanged: supply is constrained, inventories are tight, and the system doesn’t have much buffer.

Latest lithium demand-side factors

On the demand side, things are a little more nuanced — but far from weak.

At first glance, China’s January EV sales data looked soft. But as Macquarie points out, the headline numbers are misleading. “Consumption slowdown is unconfirmed… softer Jan passenger EV sales were distorted by policy timing”.

There are several moving parts here:

The expiration of full purchase tax exemptions at the end of 2025 created a temporary demand distortion.

Subsidy changes — shifting from fixed amounts to percentage-based incentives — have altered consumer behaviour.

There was a pull-forward of demand into December as buyers rushed to take advantage of existing incentives.

The result? A weak January print that likely says more about timing than underlying demand.

More importantly, other parts of the demand equation remain strong. Energy storage systems (ESS) are seeing robust uptake, with operators running at high utilisation levels. Macquarie notes that “ESS demand remains robust, with operators running at high utilisation on strong order books”.

This is a key theme for 2026. While EV demand remains the dominant driver, the growth of battery storage is increasingly becoming a second engine for lithium demand — and one that may be less sensitive to short-term policy noise.

Why the lithium market could tighten further

And that’s where the story gets particularly interesting.

Macquarie’s base case is for a broadly balanced lithium market in 2026, followed by modest surpluses in 2027 and 2028. But that outlook comes with important caveats.

The key issue is the delayed restart of CATL’s Jianxiawo mine, alongside broader uncertainty across Jiangxi’s lepidolite operations. As Macquarie notes, “continued suspension… could reduce CY26 market surplus… [and] push the market to a small deficit”.

That’s a big deal.

What was expected to be a balanced market could quickly tighten — or even tip into deficit — depending on how these supply-side risks play out.

Adding to the complexity are policy and regulatory pressures. Macquarie highlights that “policy uncertainty and regulatory pressure… [are] expected to continue constraining supply”, particularly in China’s Jiangxi region.

Conclusion: Boom or bust?

So where does that leave us? Is 2026 shaping as a continuation of the boom, or is it a transitional year back to what will prove to be a secular bear market?

Macquarie’s conclusion is clear — and notably constructive. The broker argues that recent weakness in ASX lithium stocks has been “largely sentiment-driven” rather than fundamentally justified.

In terms of positioning, PLS remains its preferred large-cap exposure, supported by strong operating performance and potential catalysts later in 2026. IGO (IGO) offers longer-term growth through Greenbushes, while names like LTR and Elevra Lithium (ELV) provide leverage to improving cashflows and rising prices.

Perhaps most tellingly, Macquarie points to the potential for significant free cash flow expansion across the sector if current pricing holds — a powerful driver of equity re-rating.

For ASX investors, the takeaway is this:

The lithium market has emerged from its bear market — but it is not yet stable.

Prices have rebounded sharply, supply remains constrained, and demand is proving more resilient than feared.

But the system is finely balanced and highly sensitive to both policy shifts and supply disruptions.

In other words, the boom may be back — but so too is the volatility. As always in commodities, timing and discipline will matter just as much as conviction.

Macquarie’s Outperform-rated ASX lithium stocks (alphabetical):