ASX 200 Live Today - Wednesday, 4th February

The S&P/ASX 200 is set to slip after a relatively weak overnight session on Wall Street. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Wednesday, February 4. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Be sure to refresh manually for the latest updates — and let us know how we can make it even better.

ASX 200 higher as miners and banks offset everything else

[2:15 pm] ASX 200 has managed to shrug off an early 0.28% slip, currently up 0.63% and trading at intraday highs. A classic sector breakdown, with Materials (+2.9%) and Energy (+2.4%) sharply higher, Financials (+0.5%) also mustering up some strength to trade at a fresh one-month high. Meanwhile, Tech (-7.6%) is getting absolutely slotted, while Utilities (-1.8%), Telcos (-1.4%), Real Estate (-1.2%), Discretionary (-1.0%) and Industrials (-0.9%) are all pretty weak. Looks like some downward pressure across most consumer-facing sectors after yesterday's hawkish RBA hike. The Index charts for many sectors is starting to look a little ugly (e.g. Real Estate, Discretionary, Utilities etc. all below the 200-day and starting to undercut recent lows). I guess the plus side is that the resource sector is holding everything together, along with some renewed strength in banks.

Gold stocks up, Northern Star Resources upgraded

[1:05 pm] Gold stocks are broadly higher today, following bullion’s overnight rebound. Northern Star Resources surged after JPMorgan upgraded the stock to Buy, with focus also turning to its half-year results due on 12 February.

Gold up 2.3% to around US$5,079/oz.

Northern Star Resources (NST) ($26.99) upgraded to Buy from Hold; target lifted +22% to $33

All Ordinaries Gold index is up 3.5%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

NST | Northern Star Resources | 5.89% | $28.48 |

CYL | Catalyst Metals | 4.83% | $8.24 |

RRL | Regis Resources | 4.60% | $8.07 |

RMS | Ramelius Resources | 4.36% | $4.67 |

NEM | Newmont | 3.48% | $170.49 |

BGL | Bellevue Gold | 3.28% | $1.80 |

WGX | Westgold Resources | 3.23% | $7.19 |

EVN | Evolution Mining | 2.84% | $14.87 |

GMD | Genesis Minerals | 2.39% | $7.27 |

EMR | Emerald Resources | 2.25% | $6.83 |

RSG | Resolute Mining | 2.04% | $1.35 |

BY Warren Masilamony | Company page: Northern Star Resources (NST)

Pinnacle 1H26 earnings call highlights

[12:14 pm] Pinnacle rallied as much as 9.4% in early trade but now up just 3.2%. The result was slightly below market expectations across NPAT and funds under management, though the dividend was ahead of consensus. Here are some of the key takeaways from the earnings call:

Acquisition of PAM boosts global expansion, especially in EMEA, without immediate team integration

Offshore distribution capabilities strengthened with two autonomous teams, easing affiliate onboarding

No cost synergies targeted: all staff retained and growth opportunities prioritised over headcount cuts

Strong demand for active equities, retirement income, private credit, and alternative fixed income products

Headcount increases planned in UK, Canada, US, and Middle East to support global distribution growth

Amcor Q2 earnings call highlights

[12:12 pm] Amcor just held its 2Q26 earnings call. Here are some of the key takeaways:

Volume expected to remain stable over the next two quarters, with limited upside in guidance

EBIT improvement in second half driven by seasonality, synergy realisation, and recovery in non-core businesses

Non-core EBIT margins to rebound to 7-9%, supported by better contract terms and pricing stability

Pet care and meat protein outperformed, with pet care achieving high single-digit growth and likely share gains

The stock is currently trading ~2% higher.

Construction activity rebounds despite overall industry contraction

[11:21 am] The Australian Industry Index shows continued contraction overall, but the construction sector returned to positive territory, supported by project inquiries and early 2026 pipelines.

Australian Industry Index at -12.3 in Dec/Jan, unchanged from November as activity, employment, new orders, and input volumes contracted at similar rates

Construction Activity (PCI indicator) returned to positive for the first time in two years, driven by strong project inquiries

Metals and food industries posted stronger results, while machinery and chemicals saw seasonal slowdowns

Activity/sales indicator remained at -11.9, employment broadly stable at -4.7, trend steady between -5.0 to -7.0 since H2 2025

New orders indicator rose 4.1 points to -14.2, reflecting early 2026 work pipeline; input volumes slightly down to -15.7

Businesses cite high input costs, taxes, regulatory pressures, international uncertainty, and staff shortages as ongoing constraints

Source: Ai Group Industry Index

Tech stocks tumble

[11:19 am] Tech stocks are getting absolutely obliterated, a move that's relatively in-line with the aggressively selldown of US software-related stocks overnight. The S&P/ASX 200 Tech Index is down 8.1%, trading at its lowest level since January 2024.

Ticker | Company | % Chg | Price |

|---|---|---|---|

NXT | NextDC | -1.51% | $13.06 |

CDA | Codan | -2.71% | $36.96 |

360 | Life360 | -4.38% | $27.39 |

MP1 | Megaport | -7.01% | $10.61 |

TNE | Technology One | -9.35% | $22.94 |

WTC | Wisetech Global | -9.52% | $51.92 |

XRO | Xero | -14.25% | $82.41 |

Neuren enters trading halt pending announcement

[10:33 am] Trading in Neuren Pharmaceuticals has been halted at the company’s request, pending the release of an announcement.

Halt expected to remain in place until the earlier of normal trade on Friday 6 February 2026, or when the announcement is released.

NEU ($14.6) fell 9.9% after news of a negative trend vote in its European regulatory submission on Tuesday

BY Warren Masilamony | Company page: Neuren Pharmaceuticals (NEU)

Top ASX 200 gainers and losers

[10:30 am] Pinnacle is trading sharply higher off the back of its 1H26 result, while resource stocks also bouncing after the recent pullback. Meanwhile, tech names continue to fall, in-line with the overnight obliteration of software-related stocks.

Ticker | Company | % Chg | Price |

|---|---|---|---|

PNI | Pinnacle Investment Management | 7.15% | $18.43 |

LYC | Lynas Rare Earths | 6.43% | $16.23 |

NST | Northern Star Resources | 5.13% | $28.27 |

RRL | Regis Resources | 4.93% | $8.09 |

ILU | Iluka Resources | 4.74% | $5.42 |

SLX | Silex Systems | 4.71% | $6.89 |

GGP | Greatland Resources | 4.66% | $13.24 |

AAI | Alcoa Corporation | 4.32% | $87.17 |

S32 | South32 | 3.88% | $4.69 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

XRO | Xero | -13.19% | $83.42 |

NEU | Neuren Pharmaceuticals | -9.97% | $14.63 |

TNE | Technology One | -7.75% | $23.34 |

PME | Pro Medicus | -6.45% | $166.10 |

XYZ | Block | -6.44% | $80.43 |

SEK | Seek | -6.01% | $19.72 |

MP1 | Megaport | -5.70% | $10.76 |

WTC | Wisetech Global | -5.45% | $54.25 |

REA | REA Group | -5.01% | $182.01 |

4DX | 4DMedical | -4.59% | $3.53 |

Pinnacle and Jumbo intraday swings

[10:15 am] Pinnacle shares opened 2.7% higher, currently up 7.5% despite reporting a relatively softer-than-expected 1H26 result.

NPAT down 11% to $67.3m vs. $70.6m ests (4.6% miss)

Interim dividend 29 cps vs. Macquarie ests of 25 cps (16% beat)

Net inflows $17.2bn vs. Mac ests of $18.4bn (7% miss)

Closing FUM $202.5bn vs. Mac ests of $208.4bn (3% miss)

What makes Pinnacle rather interesting this time round is that the stock is trading around 30x (trailing) heading into the result, as opposed to ~35x in the last three reporting seasons. Macquarie has already cut its target price this morning (since the result was released after hours on Tuesday) by 4.9% to $25.25, though the analysts are still outperform rated with the view that PNI has an attractive growth outlook and potential to add accretive M&A.

Jumbo opened 7.2% higher, now down 1.0% despite preliminary 1H26 numbers tracking slightly ahead of market expectations.

Revenue up 7% to $85.3m vs. $86m ests (1% miss)

Underlying EBITDA up 22.6% to $37.5m vs. $35.5m ests (6% beat)

Underlying NPAT up 15% to $19.9m vs. $19m ests (4.7% beat)

Jumbo has been subject to some volatile moves before, with the stock rallying 33% between 14-22 October last year (driven by an earnings accretive acquisition), and then giving back all those gains between 29-Oct and 18-Nov.

Investors favour Rio London shares ahead of Glencore deal

[10:08 am] Investors are shifting to Rio Tinto’s London-listed shares amid merger talks with Glencore, according to the AFR. This reflects expectations that Australian shareholders could face dilution if scrip is used in a deal.

Rio’s Australian shares down 1.5% since Glencore merger talks confirmed, while London shares up ~9% over the same period

Premium of Australian shares over London stock fell from 23% (1 Jan) to 14% (4 Feb), reflecting market repricing amid merger speculation

Large Australian institutions actively reducing Australian holdings and increasing London holdings: Commonwealth Bank cut Aus shares ~6% while London shares rose ~10%

AustralianSuper prefers London shares for lower purchase price and liquidity, it holds ~$7bn of London shares and continues buying more London than Australian scrip

BlackRock also buying almost twice as many London shares as Australian since 1 Jan

Company page: Rio Tinto (RIO)

Centuria Office REIT posts solid leasing and valuation gains

[9:47 am] COF delivered solid leasing volumes, rent growth, and consecutive valuation uplifts, supporting its FY26 FFO and distribution guidance.

Reaffirmed FY26 FFO guidance of 11.1-11.5 cps and distribution guidance 10.1 cps (~9.5% yield)

Half year FY26 FFO $33.4m or 5.6c cps, distribution 5.1 cps

Portfolio valuation up $42.8m, second consecutive period of gains

Portfolio occupancy at 91%, 4.1-year WALE

Second largest ever leasing volume of 29,354sqm across 26 transactions (10.7% of portfolio NLA)

4% year-on-year market rental growth underpinned valuation uplift

9 Help Street, Chatswood divested at 12.5% premium to book value, improving portfolio metrics and balance sheet

Company page: Centuria Office REIT (COF)

Nova Minerals to redomicile to the US and acquire remaining Estelle stake

[9:37 am] Nova Minerals will move its corporate domicile to the United States after losing foreign private issuer status, aligning its structure with its US operations and expanding access to US capital markets.

Nova is advancing one of the world's largest undeveloped gold deposits located in Alaska, and securing a US domestic supply of the critical mineral antimony.

US ownership exceeded 50% as of 31 Dec 2025, Nova will cease qualifying as a foreign private issuer from 1 Jul 2026 and must comply with US domestic securities laws.

Board proposes redomiciliation via a Scheme of Arrangement to a new US parent, expected to be named Nova Minerals Corp, retaining dual ASX and Nasdaq listings under the same tickers.

ASX shareholders expected to receive CDIs, Nasdaq ADS holders to receive common stock.

Redomiciliation benefits include lower-cost US capital access, broader US investor appeal, alignment with core US-based operations, and increased opportunities for US government funding and grants.

Nova plans to acquire the remaining 15% interest in the Estelle Gold and Critical Minerals Project, giving full ownership and supporting progression toward construction and production.

Company page: Nova Minerals (NVA)

Jumbo Interactive 1H26 shows strong growth despite soft jackpots

[9:30 am] Jumbo reported preliminary numbers for 1H26, expecting strong double-digit growth across key metrics, driven by resilient Australian operations, Managed Services and recent acquisitions.

Revenue up 7% to $85.3m vs. $86m ests (1% miss)

Underlying EBITDA up 22.6% to $37.5m vs. $35.5m ests (6% beat)

Underlying NPAT up 15% to $19.9m vs. $19m ests (4.7% beat)

Lottery Retailing TTV broadly flat despite fewer large jackpots

Total Division 1 prize value down 32.8% to $410m, no jackpots over $100m

SaaS segment TTV up 9.9%, or 12.4% excluding Lotterywest

Managed Services delivered strong growth in Canada and disciplined execution in the UK

Acquisitions of Dream Car Giveaways UK and Dream Giveaway USA add incremental non-cash amortisation of ~$2.2m in 1H26 statutory results

Company page: Jumbo Interactive (JIN)

Amcor Q2 delivers solid EPS growth, reaffirms FY26 guidance

[9:20 am] Amcor reported strong adjusted EPS growth in Q2, underpinned by the Berry acquisition and operational synergies, while free cash flow fell short of market expectations due to acquisition and integration costs.

Revenue up 68% $5.45bn vs. $5.51bn ests (1% miss)

Adjusted EBIT up 66% to $603m vs. $638.3m ests (5% miss)

Adjusted EPS up 7% to $0.86 vs. $0.85 ests (1% beat)

Adjusted free cash flow $289m vs. $511.3m ests (43% miss)

Impacted by Berry acquisition, restructuring and integration costs of $69m

Quarterly dividend of 65 cents

Reaffirms FY26 guidance: Adjusted EPS $4.00-4.15 vs. $4.00 ests, free cash flow $1.8-1.9bn vs. $1.7bn ests

NYSE-listed Amcor shares edged 0.1% higher in after hours trade.

Company page: Amcor (AMC)

Pinnacle 1H25 NPAT falls short of estimates

[9:15 am] Pinnacle reported a decline in first-half profits despite strong dividends and record net inflows, with most key metrics slightly missing market expectations.

NPAT down 11% to $67.3m vs. $70.6m ests (4.6% miss)

Interim dividend 29 cps vs. Macquarie ests of 25 cps (16% beat)

Net inflows $17.2bn vs. Mac ests of $18.4bn (7% miss)

Closing FUM $202.5bn vs. Mac ests of $208.4bn (3% miss)

Company page: Pinnacle Investment Management (PNI)

Relentless software selling

[9:04 am] Software stocks continued to nosedive overnight, despite most names already falling 10-20% in the last 5-6 sessions. Notable decliners include Intuit (-10.89%), Shopify (-9.77%), ServiceNow (-6.97%), Salesforce (-6.85%), Adobe (-7.31%), ADP (-5.04%), SAP (-4.8%) and Uber (-3.6%).

A few noteworthy comments from analysts overnight

Jefferies trading desk: "I ask clients, ‘what’s your hold-your-nose level?’ and even with all the capitulation, I haven’t heard any conviction on where that is. People are just selling everything and don’t care about the price."

Goldman Sachs: Analysts cited selloff drivers including Anthropic launching new capabilities for its agentic Cowork facility, a couple of EPS moves lower in AI-at-risk companies across the market and horrible momentum (bad for pro-momentum sector like software)

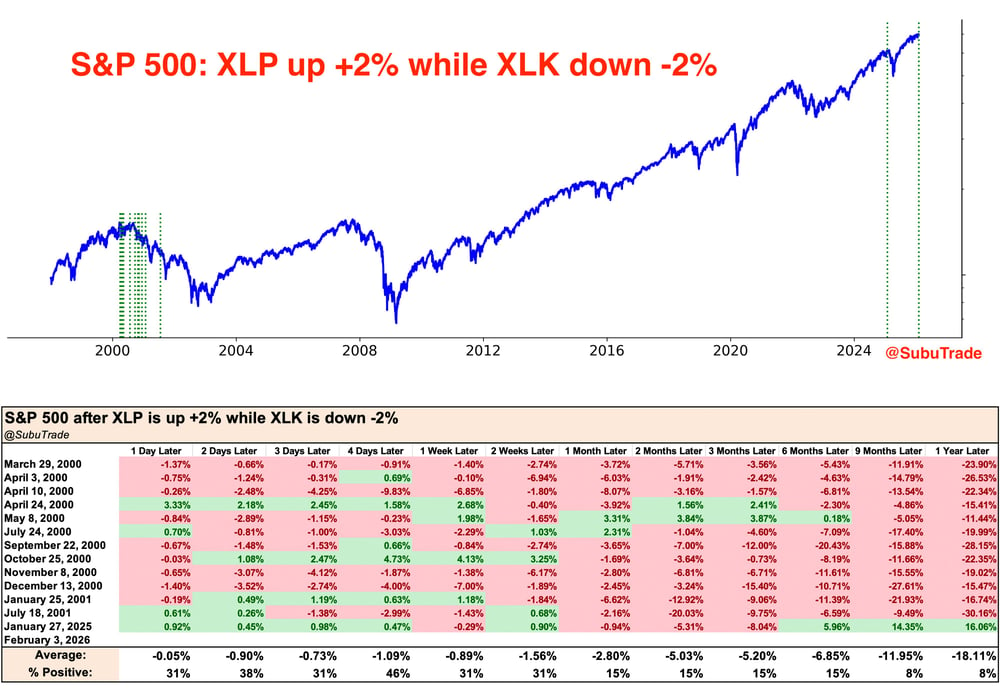

Defensives up, tech down: A bad omen?

[8:59 am] An interesting observation from Subu Trade (@SubuTrade). The S&P 500 Staples sector was up as much as 2% overnight, while the Tech sector tumbled over 2%. This clear risk-off move has only happened in the 2000-2001 dot-com bust and January 2025 (just before Trump's tariff crash). Here's how the market performed after this signal.

Source: SubuTrade

Waymo raises US$16bn to expand robotaxi lead

[8:56 am] Waymo, Alphabet’s autonomous driving unit, secured US$16 billion at a US$126 billion valuation as it seeks to scale its commercial robotaxi operations across the US and globally.

Funding round led by Sequoia Capital, DST Global and Dragoneer Investment Group, with Alphabet contributing $13bn as part of the investment.

Waymo operates fully driverless, fare-charging services in about six US cities and partners with Uber in Austin and Atlanta, providing over 400,000 paid rides per week.

Plans include rapid expansion across the US and into the UK, plus fleet growth and global hiring to support scale.

Industry economics remain challenging, with per-vehicle costs two to three times higher than Tesla, constraining fleet size, but Waymo intends to deepen partnerships with automakers.

US builds critical minerals alliance to counter China

[8:54 am] The US is forming a tariff-free critical minerals trading bloc with allies to reduce dependence on China, according to Reuters.

Around 30 countries are seeking to join the US-led minerals club, with Japan, Australia and South Korea already in, and up to 11 new agreements expected to be announced this week.

A further ~20 countries have signalled strong interest, with the bloc proposing tariff-free trade, coordinated exchanges and price floors for key materials.

The initiative targets Chinese dominance in lithium, nickel and rare earths, where the US argues oversupply can be used to crush pricing and destroy economic value across supply chains.

The US has also launched a strategic minerals stockpile, Project Vault, backed by a $10bn loan from the US Export-Import Bank plus nearly $2bn in private capital.

Price floors are designed to unlock private investment in mining and refining by reducing downside risk and improving project bankability.

Walmart joins the US$1 trillion club

[8:51 am] Walmart shares hit a record high, lifting the retailer’s market capitalisation above US$1 trillion for the first time as investors reward its scale, digital pivot and AI-driven growth strategy.

Shares rose 2.9% to a record $127.71, adding ~$29.1bn in value and pushing market cap just above $1tn

The stock is up 15% YTD vs. the S&P 500’s 1.1% gain.

Walmart is using its scale and supplier network to hold prices while attracting higher-income shoppers through stronger online and convenience offerings, expanding its customer base beyond value buyers.

AI investment is accelerating operations, from scheduling to supply chains, with partnerships across Alphabet’s Gemini platform and OpenAI enabling AI-assisted shopping directly via ChatGPT.

The company was added to the Nasdaq 100, reinforcing its positioning as a tech-enabled retailer rather than a pure brick-and-mortar operator.

Valuation is stretched, trading just above 42x forward earnings

Source: Bloomberg

Commodity prices bounce but still below recent highs

[8:50 am] An almost sea of green for commodity prices overnight, with most prices set to close the session around intraday highs.

Commodity | % Chg | Price (US$) |

|---|---|---|

Silver | +7.3% | $85.1/oz |

Gold | +5.9% | $4,935/oz |

Platinum | +4.3% | $2,211/t |

Copper | +4.3% | $6.13/lb |

Brent | +2.3% | $67.90/bbl |

Nickel | +2.0% | $17,287/t |

Palladium | +1.3% | $1,751/t |

Aluminium | +1.3% | $3,086/t |

Precious metals volatility resets after historic crash

[8:46 am] Gold and silver volatility is expected to stay structurally higher after a sharp washout from record highs, with Bank of America arguing the recent collapse has cleared excess speculation without breaking the long-term bull case.

Gold volatility is now at its most unstable level since the 2008 financial crisis, while silver is seeing its most extreme turbulence since 1980, highlighting how disorderly the recent price action has become.

Both metals surged last month on speculative positioning, geopolitical risk and concerns over US Federal Reserve independence, before abruptly reversing with gold posting its biggest drop in more than a decade and silver its worst day on record.

BofA says the last two sessions triggered a market “washout” that cleaned up leveraged and crowded positions, reducing the risk of immediate speculative excess.

Dip buyers quickly returned, with BofA arguing gold retains a stronger long-term investment thesis, meaning higher volatility may shrink position sizes but not investor participation.

Source: Bloomberg

Major US benchmarks off worst levels

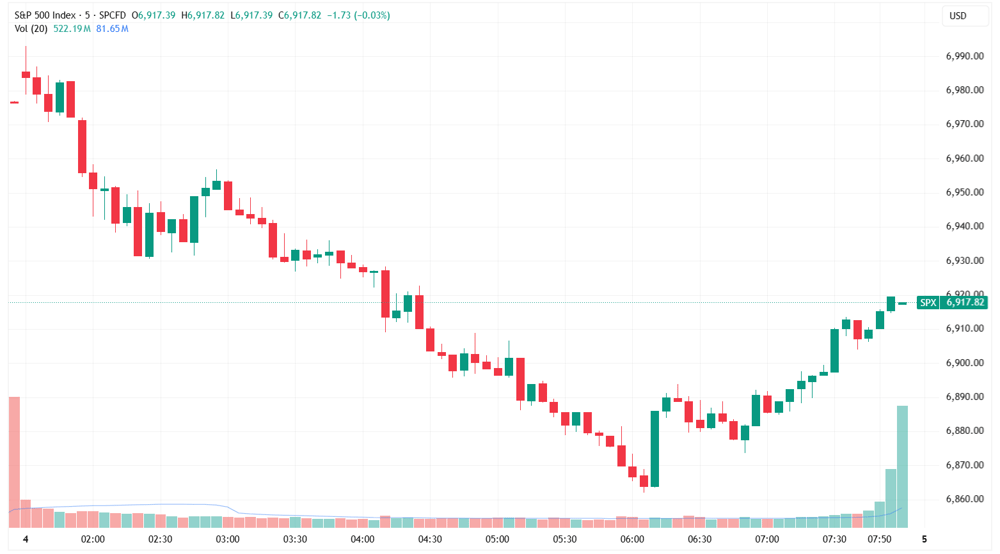

[8:42 am] A very interesting overnight session, where major US benchmarks finished mostly lower but off worst levels.

Nasdaq (-1.43%), S&P 500 (-0.84%), Dow (-0.34%) and Russell 2000 (+0.31%)

S&P 500 and Nasdaq down as much as 1.6% and 2.4% respectively in early trade

Software obliteration continued, with notable decliners including SAP (-4.8%), Salesforce (-6.8%), Shopify (-9.7%), Adobe (-7.3%), Snowflake (-9.1%), Workday (-7.0%)

Clear defensive rotation into select cyclicals and defensives

Energy (+3.2%) and Materials (+2.0%) sharply higher, Staples (+1.7%) and Utilities (+1.5%) also very strong

S&P 500 intraday chart (Source: TradingView)

Good morning!

[8:34 am] ASX 200 futures are down 40pts (-0.45%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks mostly lower but finished off worst levels

Software stocks continued to tumble, with most names down 5-10%

Commodity prices bounced, with gold up ~6%, silver up 8%, copper up 4.5% and back above US$6/lb

To catch up on all overnight developments, check out today's Morning Wrap.