ASX 200 Live Today - Wednesday, 29th April

The S&P/ASX 200 is set to open lower, ahead of key Australian inflation data. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Wednesday, April 29. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

A seven day losing streak

[1:58 pm] The S&P/ASX 200 is currently down 0.31% and on track to record a seventh straight day of declines. The funny thing is, the market isn't even oversold – with an RSI reading of 41. The add some perspective, the index fell 9.0% between 2-23 March, where the RSI troughed at 29. But here's a funny thing – since 1994, the ASX 200 recorded a seven day losing streak of 16 occasions as well as a handful of >8 day losing streaks. After the final day of each streak, the index has rallied 1.1% on average. But historically speaking, the bounce tends to be short lived. By the one-month mark, the average return turns slightly negative (−1.17%) and only 7 of 16 episodes were positive.

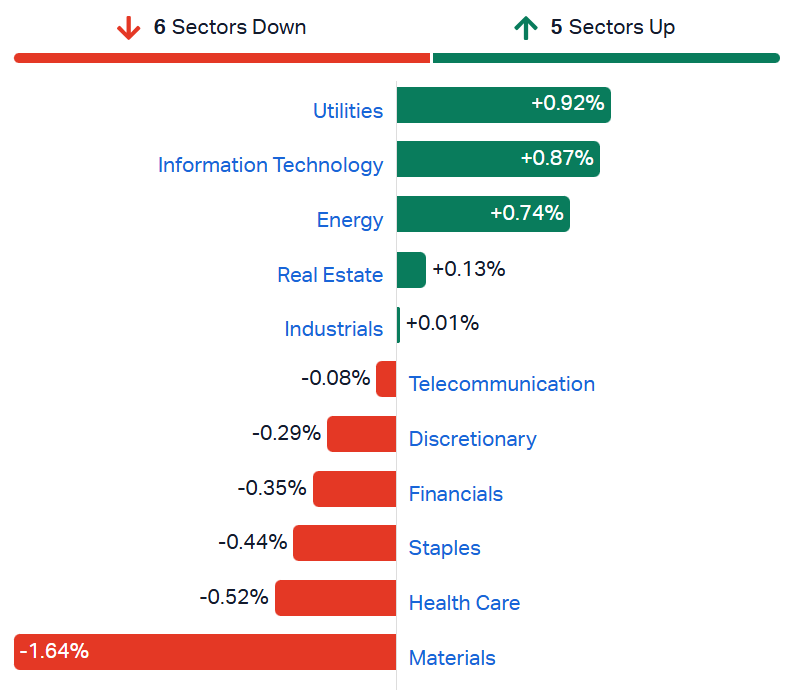

As for today's session, breadth was a relatively even split, with 99 constituents trading higher, largely reflecting gains from Energy and Tech, and a bounce for Real Estate and Discretionary stocks. Financials (-0.54%) still down twelve of the last fourteen sessions, while Materials (-0.87%) trading close to a three-week low.

That's all for today. We've got the Fed decision at 4:00 am tomorrow and Alphabet, Microsoft, Amazon and Meta earnings as well. It's going to be chokkas.

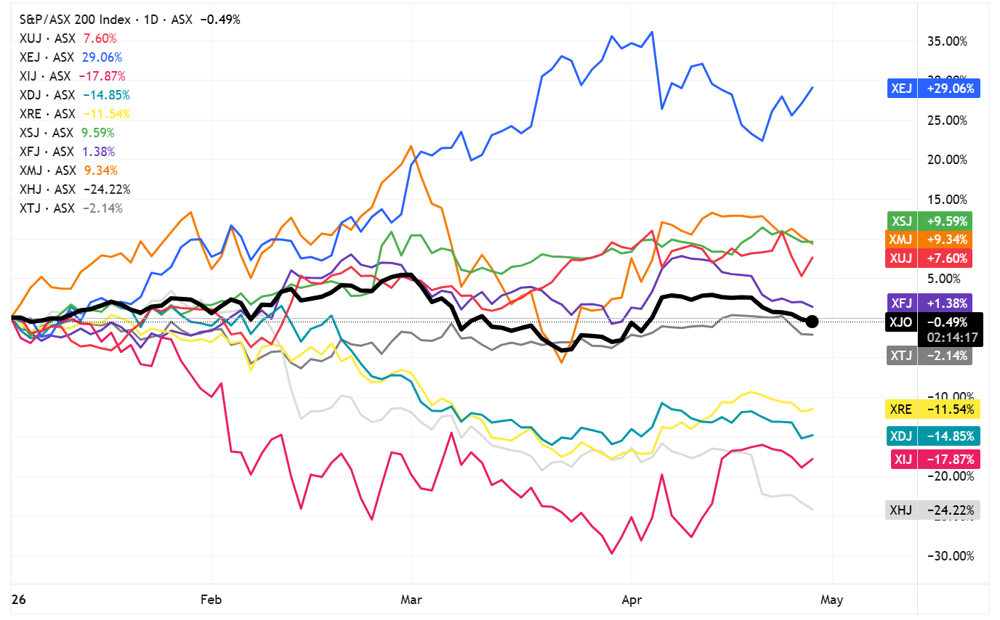

Relative sector performance vs. ASX 200

[1:49 pm] The S&P/ASX 200 is now down 0.5% for the year. In a relative sense, resources (Materials and Energy) and defensives (Staples, Utilities) have performed quite well, while Tech, Retailers and REITs have dramatically underperformed.

S&P/ASX 200 vs. sectors (Source: TradingView)

Albanese rules out LNG contract changes in upcoming budget

[1:35 pm] The Australian government has moved to protect existing LNG export arrangements, pushing back against calls to increase taxes on producers amid the global energy crunch.

Prime Minister Albanese confirmed the federal budget will not undermine existing LNG export contracts, citing national fuel security and the risk of deterring investment during a global energy crisis

Pressure had been building to increase taxes on LNG producers including Chevron and Woodside, which have benefited from higher prices following the Middle East conflict cutting roughly a fifth of global supply

Australia exported almost 80 million tons of LNG last year, primarily to Japan, China and South Korea, making it one of the world's largest exporters and giving it a significant strategic interest in maintaining those relationships

Source: Bloomberg

Taiwan's equity market overtakes Canada to become world's sixth largest

[1:33 pm] AI-driven demand for semiconductors has reshaped global equity rankings, with Taiwan's market surging past Canada on the back of TSMC's remarkable appreciation.

Taiwan's total market cap has surged more than 35% this year to $4.47 trillion, overtaking Canada's $4.44 trillion (up ~5% year-to-date) to become the world's sixth largest equity market

TSMC, which accounts for nearly 45% of Taiwan's benchmark index, has seen its market value swell to $1.8 trillion

Just two days ago, Taiwan overtook the UK market (#7)

Gold stocks mixed

[12:53 pm] A very mixed day for gold miners, though the broader S&P/ASX All Ords Gold Index is currently down 0.34%, bouncing off session lows of (1.85%).

Aurelia Metals sharply higher after upgrading its FY26 gold production guidance on Tuesday, Capricorn (+2.5%) quarterly this morning noted better costs and production towards the upper end of full-year guidance, while Westgold (-3.0%) quarterly flagged costs tracking towards the top end of its $2,600-2,900/oz guidance range.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

AMI | Aurelia Metals | 9.6% | $0.31 | 2.3% |

MEK | Meeka Metals | 3.6% | $0.15 | -3.3% |

CMM | Capricorn Metals | 2.5% | $11.78 | 28.6% |

PRU | Perseus Mining | 2.1% | $5.63 | 70.5% |

ALK | Alkane Resources | 1.7% | $1.58 | 102.2% |

VAU | Vault Minerals | 1.4% | $4.72 | 68.7% |

GMD | Genesis Minerals | 1.0% | $6.34 | 66.7% |

NST | Northern Star Resources | 0.0% | $21.49 | 8.3% |

RRL | Regis Resources | -0.2% | $7.19 | 59.7% |

RMS | Ramelius Resources | -0.3% | $3.66 | 41.3% |

RSG | Resolute Mining | -0.7% | $1.21 | 136.7% |

EVN | Evolution Mining | -0.7% | $12.60 | 58.4% |

BGL | Bellevue Gold | -0.8% | $1.60 | 78.4% |

EMR | Emerald Resources | -1.1% | $6.13 | 56.4% |

BC8 | Black Cat Syndicate. | -2.4% | $1.12 | 13.9% |

PNR | Pantoro Gold | -2.8% | $3.29 | 21.7% |

WGX | Westgold Resources | -3.0% | $5.92 | 99.3% |

NEM | Newmont | -3.0% | $153.99 | 83.3% |

SBM | St. Barbara | -3.1% | $0.62 | 121.4% |

OBM | Ora Banda Mining | -3.7% | $1.42 | 35.2% |

CYL | Catalyst Metals | -5.4% | $5.72 | -10.7% |

Coal stocks broadly higher

[12:50 pm] Coal names are trading 2-5% higher, though most are still down 10-15% from 30 March highs.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

YAL | Yancoal Australia | 5.2% | $7.66 | 53.7% |

NHC | New Hope Corporation | 4.7% | $5.50 | 49.3% |

CRN | Coronado Global | 3.8% | $0.27 | 22.7% |

WHC | Whitehaven Coal | 3.6% | $8.29 | 68.2% |

SMR | Stanmore Resources | 2.2% | $2.29 | 22.5% |

TER | Terracom | -1.3% | $0.07 | 26.7% |

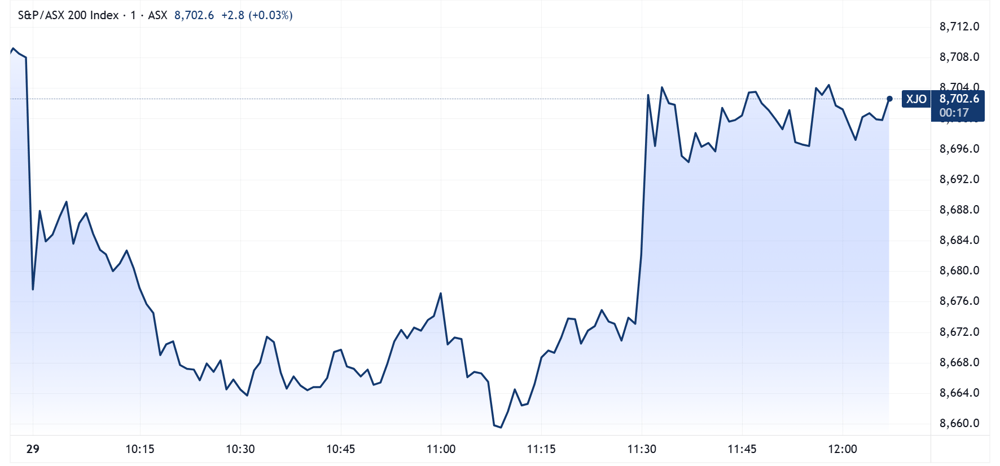

ASX 200 off lows

[12:07 pm] The ASX 200 was down around 0.43% heading into the CPI print, now close to breakeven. Despite March CPI soaring 4.6% year-on-year, it was slightly below market expectations of 4.8%. Trimmed mean CPI was also unchanged month-on-month at 3.3% and in-line with consensus. Face value figures are pretty ugly, but largely expected.

ASX 200 intraday chart (Source: TradingView)

What analysts think about Greatland Gold

[12:06 pm] Greatland Resources delivered a strong Q3 result on Tuesday, beating expectations on both production and costs while adding record cash to a debt-free balance sheet, with Federal environmental approval for Havieron removing a significant development risk ahead of a formal investment decision.

Jarden retained Underweight, raised target from $8.30 to $8.50. Federal environmental approval seen as significantly de-risking the Havieron development pathway, with record cash generation and balance sheet strength supporting the growth program; the reserve update and mine life extension reduce reliance on Havieron success, and O'Callaghans tungsten was flagged as potential hidden value.

RBC Capital Markets retained Outperform, maintained target at $15.60. Balance sheet now provides flexibility to fund both Telfer and Havieron growth phases, though grade pressures and stockpile depletion are expected to drive costs higher into FY27; near-term momentum supportive but the market already seen as pricing in substantial gold price assumptions, with accelerating growth capex increasing execution risk.

Australian CPI surges to 4.6% as fuel prices spike on Iran war fallout

[11:32 am] Headline inflation hit its highest level since September 2023 in March, driven by a record monthly jump in automotive fuel prices, though underlying inflation remained contained.

Headline CPI rose 4.6% in the year to March (vs. 3.7% in February), the highest reading since September 2023 though slightly below market expectations of 4.8%

Monthly CPI movement was 1.1%

Quarterly rise was 1.4%

Transport was the key driver of the monthly move, rising 9.2% in March, with automotive fuel prices surging 32.8% in a single month, the largest monthly increase since the series began in 2017

At the pump, regular unleaded rose 33% to an average of 228 cents per litre, premium unleaded rose 30% to 250 cents per litre, and diesel rose 41% to 256 cents per litre in March

Housing remained the largest annual contributor to CPI, up 6.5% over the year

Electricity costs 25.4% higher than 12 months ago following the expiry of Commonwealth and state government rebates

Trimmed mean inflation, which strips out volatile items like fuel, was unchanged at 3.3% annually and in-line with market expectations, suggesting underlying price pressures remain more contained and the fuel spike is largely war-related rather than a broad-based inflation resurgence

What analysts think about Whitehaven Coal

[11:15 am] Whitehaven Coal delivered a mixed Q3 on Tuesday, with QLD Blackwater ROM production impacted by wet weather, offset by stronger-than-expected coal sales driven by deliberate inventory drawdowns built ahead of the wet season, while NSW assets broadly outperformed. The stock finished the session up 3.9%.

UBS retained Buy, lowered target from $9.60 to $9.10. QLD weather disruptions seen as temporary and recoverable with NSW open cuts outperforming, though diesel and FX headwinds are weighing on near-term earnings and capital returns remain a medium-term rather than near-term focus.

JPMorgan upgraded to Neutral from Underweight, raised target from $8.30 to $8.70. The sales beat and well-executed QLD inventory strategy were the standout positives, with the debt refinancing meaningfully reducing financing burden; downside risk seen as materially reduced following guidance reaffirmation, though Narrabri's longwall extension introduces near-term maintenance risk.

Carma delivers strong Q3 growth as Sell-to Carma channel scales rapidly

[11:13 am] The online used car platform is accelerating across all key operating metrics, with vehicle purchasing and reconditioning throughput inflecting sharply higher through the quarter.

Total units sold up 118% year-on-year to 1,344, comprising retail units up 73% to 774 and wholesale units up 237% to 570

Total revenue up 94% to $28.7m

Gross profit up 128% to $3.0m

Total vehicles purchased up 263% to 1,627 for the quarter, with 733 purchased in March alone and 45% of total quarterly purchases occurring in the final month, pointing to strong Q4 momentum

Reconditioning throughput averaged 15.7 retail units per shift (up 149% on pcp), accelerating to 17.0 in March and surpassing 20 through April, with retail units available for sale reaching 362 at quarter end

Network expanded to eight locations with the addition of Newcastle during the quarter

Despite what reads like a positive announcement, Carma shares are down 9.3% at the time of writing, to a record low of 72.5 cents.

What analysts think about Pantoro

[11:10 am] Pantoro reported a weak production quarter on Tuesday, with volumes and costs both missing expectations due to weather-related disruptions across mining operations, including a flooding event at Scotia underground linked to Cyclone Mitchell. The stock finished the session down 11.2%.

UBS retained Buy, lowered target from $7.00 to $6.20. Medium-term grade assumptions revised lower on delivery concerns and guidance achievement viewed as increasingly challenging, though valuation remains attractive and upcoming resource drilling is seen as a key positive catalyst.

Canaccord Genuity retained Speculative Buy, lowered target from $7.55 to $7.35. June quarter requires a record operational performance to meet guidance, with Gladstone and Mainfield expected to broaden the production base; the debt-free and unhedged position and the upcoming five-year plan were noted as key positives.

Codan soars 15% to fresh all-time highs

[10:37 am] Codan opened 7.4% higher this morning, now up 14.8% to fresh all-time highs of $41.77.

The catalyst was a clean and above consensus FY26 guidance update, with a notable pull forward in profit margins for its Communications segments. Here's what we noted earlier:

FY26 NPAT guidance of ~$170m vs. ests of $152.5m (11% beat)

FY26 EBIT guidance of ~$235m vs. ests of $212.3m (11% beat)

Communications revenue growth now expected at the top end of the 15-20% target range for FY26, after delivering 19% growth in 1H

Growth is being driven by strong defence customer demand for unmanned systems and software-defined radios amid ongoing geopolitical tensions

Communications segment profit margin now expected to reach 30% in FY26, ahead of the prior FY27 target, representing a meaningful step up from the 26% margin delivered in FY25

Minelab revenue in 2H26 to date is tracking ahead of an already strong 1H, supported by a favourable gold price and recent product launches

ASX 200 lower, Materials tumble

[10:34 am] Another downbeat day for markets, with the ASX 200 down for a seventh straight session. A very weak session for the Materials Index, with heavyweights BHP (-2.2%), Fortescue (-1.4%) and Rio Tinto (-0.90%) broadly lower. This likely reflects a higher US dollar and oil prices overnight, which weighed on most commodity prices. Financials manged to close fractionally higher on Tuesday (+0.06%) but trading 0.35% lower today, now down eleven of the last 13 sessions.

S&P/ASX 200 sectors (Source: Market Index)

Top ASX 200 gainers

[10:05 am] Codan is surging off the back of an FY26 guidance upgrade, while Tech and Discretionary stocks also catch a bid.

Ticker | Company | % Chg | Price |

|---|---|---|---|

CDA | Codan | 10.97% | $40.37 |

VGN | Virgin Australia | 3.69% | $2.25 |

AUB | AUB Group | 2.96% | $25.07 |

RSG | Resolute Mining | 2.88% | $1.25 |

MSB | Mesoblast | 2.56% | $2.21 |

WTC | Wisetech Global | 2.18% | $43.14 |

XRO | Xero | 1.85% | $80.91 |

JBH | JB Hi-Fi | 1.63% | $77.36 |

NHC | New Hope Corporation | 1.52% | $5.33 |

360 | Life360 | 1.49% | $20.45 |

Top ASX 200 losers

[10:05 am] A very ugly open for all things Materials, with a broad-basket of iron ore, copper, gold, lithium, uranium and aluminium miners trading lower.

Ticker | Company | % Chg | Price |

|---|---|---|---|

AAI | Alcoa Corporation | -5.85% | $87.98 |

OBM | Ora Banda Mining | -4.75% | $1.41 |

CSC | Capstone Copper Corp | -3.83% | $11.30 |

NEM | Newmont | -3.35% | $153.37 |

ELV | Elevra Lithium | -3.29% | $13.24 |

NXG | Nexgen Energy | -2.82% | $16.71 |

LIN | Lindian Resources | -2.69% | $0.83 |

BHP | BHP Group | -2.26% | $54.18 |

SFR | Sandfire Resources | -2.03% | $16.38 |

RIO | Rio Tinto | -2.02% | $168.65 |

Nickel Industries delivers strongest earnings since late 2023 on surging NPI margins

[9:50 am] A near-tripling of NPI margins, a major uplift in its Indonesian mining licence, and rising nickel prices drove a blowout quarter for Nickel Industries.

RKEF EBITDA of US$85.8m vs. ests of US$47.5m (81% beat), up 145% quarter-on-quarter

RKEF production of 30.3kt vs. ests of 30.7kt (in-line), down 4% quarter-on-quarter

NPI margins surged 155% to $2,842/t, while HPAL margins rose 20% to $9,992/t (from $8,307/t), with NPI costs increasing only modestly by 4%

The LME nickel price rose 16% to an average of US$17,338/t in the quarter (from US$14,892/t in Q4 FY25), driven in part by the Indonesian government's RKAB licence cuts across most producers

This fed through to NPI and MHP prices rising 19% and 15% respectively

Nickel Industries' own 2026 RKAB sales licence increased ~60% to 14.3 million wmt per annum (from 9 million wmt), a significant competitive advantage as most Indonesian mining peers saw their licences cut

Post-quarter, Indonesia announced changes to its nickel ore benchmark pricing (HPM)

The new formula could push 1.1% limonite ore prices from ~$26/wmt to ~$41/wmt

This marks a meaningful potential cost headwind for HPAL producers, though Indonesian HPAL operators have not yet adopted the new pricing

Company page: Nickel Industries (NIC)

Woodside beats Q1 production estimates despite weather impacts

[9:40 am] Woodside delivered Q1 production ahead of market expectations as exceptional asset reliability offset weather disruptions.

Production down 8% year-on-year to 45.2 MMboe vs 43.7 MMboe ests (3% beat), impacted by cyclones in Western Australia

Sales volumes up 3% to 51.7 MMboe vs 47.5 MMboe ests (9% beat), with higher LNG and pipeline gas sales offsetting lower liquids

Operating revenue up 7% to US$3.26bn vs US$3.15bn ests (3% beat), driven by 11% rise in average realised price to US$63/boe

Scarborough Energy Project 96% complete, on budget and on track for first LNG cargo in Q4 2026, with FPU moored and commissioning underway

FY26 guidance unchanged at 172-186 MMboe production and $4bn-$4.5bn capex, with new CEO commencing structured business review for cost efficiency

Company page: Woodside Energy Group (WDS)

Liontown kicks off Kathleen Valley expansion early works ahead of FID

[9:35 am] Liontown is committing initial capital to long-lead procurement and pre-development works at Kathleen Valley, signalling confidence in the lithium market recovery ahead of a formal investment decision.

Formal FID is expected at end of Q1 FY27, with early works and long-lead procurement now underway to compress the timeline to incremental capacity once approved

Key early works include procurement of a 5.5MW ball mill (~$12m committed, expended over 12 months), pre-development drilling at the Northwest Flats orebody, Stage 1 of the permanent Mine Services Area, underground development of Northwest Flats, and a third paste plant pump

Expected cash expenditure on early works in FY26 is $15-18m, with total pre-FID expenditure of up to $77m

The expansion study is investigating staged development, with each stage designed to unlock additional production capacity

The decision to proceed reflects Liontown's confidence in the lithium market trajectory and the ongoing operational performance of Kathleen Valley, though the move carries some risk given lithium prices remain well below peak levels

Company page: Liontown (LTR)

G8 Education flags severe occupancy decline and moves to restructure network

[9:30 am] Falling birth rates, affordability pressures, and sector-wide supply growth have pushed G8 occupancy to multi-year lows, prompting a significant restructuring response.

Spot occupancy at 56.4% as at 24 April, down 7.0% year-on-year

Year-to-date occupancy at 56.1%, down 7.9% year-on-year

Management does not expect a material recovery in occupancy relative to pcp this year, citing sustained affordability pressures, falling birth rates, increased long-day care supply, and confidence impacts from child safety incidents across the sector

G8 will suspend operations at approximately 40 centres identified as challenged or underperforming, with the company to then consider lease surrenders, divestments, or other alternatives for those sites

Additional restructuring measures include procurement and cost-saving initiatives and a reorganisation of the Support Office structure to reduce the corporate cost base

Macquarie (23-Feb) forecasts expected a 3.5% decline in centres in FY26 (from 395 to 381), so this marks a much larger-than-expected decline. Their forecasts also had average FY26 occupancy rates of 61.8%, which suggests today's numbers are running well-below expectations.

Company page: G8 Education (GEM)

Codan upgrades FY26 guidance as both divisions fire above expectations

[9:23 am] Strong defence-driven demand in Communications and a buoyant gold price lifting Minelab have pushed Codan well ahead of analyst expectations heading into the second half.

FY26 NPAT guidance of ~$170m vs. ests of $152.5m (11% beat)

FY26 EBIT guidance of ~$235m vs. ests of $212.3m (11% beat)

Communications revenue growth now expected at the top end of the 15-20% target range for FY26, after delivering 19% growth in 1H

Growth is being driven by strong defence customer demand for unmanned systems and software-defined radios amid ongoing geopolitical tensions

Communications segment profit margin now expected to reach 30% in FY26, ahead of the prior FY27 target, representing a meaningful step up from the 26% margin delivered in FY25

Minelab revenue in 2H26 to date is tracking ahead of an already strong 1H, supported by a favourable gold price and recent product launches

This is probably one of the most market-sensitive/material announcements this morning. A massive above consensus beat across business segments and Group NPAT. While the communications segment has pulled forward its FY27 profit margin target (30%) by one year.

Codan is currently up 21% year-to-date, largely off the back of a ~16% one-day rally on 9 January.

Company page: Codan (CDA)

Regis Healthcare names Bupa's Andrew Kinkade as incoming CEO

[9:15 AM] Regis has secured a seasoned aged care operator to take the reins, with Kinkade bringing over 20 years of sector experience including a large-scale transformation role at Bupa.

Kinkade joins on 20 July, succeeding Linda Mellors whose resignation was announced in December 2025

He is currently Managing Director of Bupa Villages & Aged Care, leading 8,000 staff across 57 locations, and has been credited with delivering operational and cultural transformation, growth, and improved clinical outcomes

Company page: Regis Healthcare (REG)

Bellevue Gold reports record cash flow as production rises and costs fall consensus

[9:10 am] Bellevue Gold delivered March quarter production and costs in line with market expectations, with underlying free cash flow hitting a record $158 million before voluntary hedge book reductions.

Gold production up 27% quarter-on-quarter to 40,745oz, in-line with 40.7Koz ests

Gold sold 39,754oz vs 38.8Koz ests (3% beat)

AISC down 14% to $2,578/oz vs $2,676 ests (4% beat)

Average realised gold price of $3,459/oz vs $4,674 ests (26% miss), due to voluntary early delivery of 32.5Koz into forward sales contracts at lower locked-in prices

Forward hedge commitments reduced by 32.5Koz to 91.7Koz through voluntary pre-deliveries

FY26 production guidance of 130-150Koz and AISC of $2,600-2,900/oz reaffirmed

Company page: Bellevue Gold (BGL)

Westgold Resources delivers production miss and higher costs consensus

[9:10 am] Westgold reported Q3 gold production that was relatively in-line with expectations, amid temporary ventilation constraints at Beta Hunt.

Gold production of 93,145oz vs 94,300oz ests (1% miss)

Year-to-date production of 288,500oz with FY26 guidance of 345,000-385,000oz maintained

AISC of $2,931/oz excluding OPA vs $3,294/oz ests (11% beat)

Full year costs now expected at top end of $2,600-2,900/oz guidance range

Underlying cash build of $285m before growth investments and share buybacks lifts total cash, bullion and liquid investments to $856m, up $202m quarter-on-quarter

Board approved Higginsville expansion to 2.6Mtpa processing capacity for $145m capital expenditure, expected to lift Southern Goldfields gold production by 60koz per annum at steady state

Company page: Westgold Resources (WGX)

Ramelius Resources delivers Q3 production, lifts AISC guidance on diesel and royalties consensus

[9:10 am] Ramelius reported a slightly softer-than-expected Q3, with full-year cost guidance increased due to diesel prices and earlier commercial production at Dalgaranga.

Gold production was pre-reported at 38,093oz

AISC of $2,211/oz vs $2,171/oz ests (2% miss)

Average realised gold price of A$5,795/oz vs A$6,045/oz ests (4% miss), impacted by 34% of sales under hedge commitments or pre-delivery of June quarter contracts

Operating cash flow of $171.3m for the quarter, delivering underlying free cash flow of $101.9m after growth capital of $51.2m and exploration of $26.4m

FY26 AISC guidance raised to $1,900-2,050/oz (previously $1,700-1,900/oz), driven by earlier Dalgaranga commercial production reclassifying costs, diesel price increases and higher gold royalties

This represents a 10% increase at the midpoint

Company page: Ramelius Resources (RMS)

Capricorn Metals beats March quarter costs despite gold sales miss consensus

[9:10 am] Capricorn Metals is tracking towards the upper end of its FY26 gold production guidance, though cost are now expected to hit the upper end.

Gold production steady at 30,358 ounces vs 30,476 ounces in the prior quarter, with year-to-date production of 93,152 ounces tracking to the upper end of FY26 guidance of 115,000 to 125,000 ounces

AISC down 1% to $1,617 per ounce vs $1,708 per ounce ests (5% beat)

Full-year AISC expected at the upper end of guidance range of $1,530 to $1,630 per ounce

Record operating cash flow up 17% to $143.1 million QoQ, with cash and gold on hand of $507.6 million after capital expenditure of $50.0 million on the Karlawinda Expansion Project ($47.3 million) and Mt Gibson Gold Project ($2.7 million)

Company page: Capricorn Metals (CMM)

PEP lobs ~$750 million takeover bid for oOh!media

[9:00 am] Private equity firm Pacific Equity Partners has made an unsolicited, non-binding indicative offer to acquire oOh!media at $1.40 per share via scheme of arrangement, representing a 65% premium to the last traded price of $0.85.

The all-cash proposal values oOh! at $1.40 per share, a 65% premium to the prior close of $0.85, via scheme of arrangement

The offer is non-binding and subject to several conditions including satisfactory due diligence, unanimous board recommendation, PEP Investment Committee approval, execution of a binding scheme implementation deed, and FIRB and New Zealand OIO regulatory approvals

PEP has reserved the right to adjust the offer price to account for any buybacks, dividends, distributions, capital changes, acquisitions, divestments, or material undisclosed liabilities

The oOh! board is evaluating the proposal with UBS as financial adviser and King & Wood Mallesons as legal adviser, and is recommending shareholders take no action at this stage

OML shares are down 43% in the last twelve months, with its latest 1H26 result (16-Feb) flagging challenging advertising conditions, the loss of Auckland-related contracts and ongoing mix shift towards lower-margin segments. The consensus target price for OML after the result was $1.55.

Company page: oOh!media (OML)

US earnings season highlights: AI tailwinds, Iran headwinds, and consumer stress

[8:57 am] Corporate commentary from the current earnings season reveals a clear split between beneficiaries of the AI infrastructure boom and businesses absorbing commodity inflation and softening consumer demand.

Downstream AI capex momentum remains strong: Nucor called the data centre market "white hot," Corning reported a 36% jump in Optical Communications sales driven by AI demand, Armstrong World Industries flagged urgent grid stability project needs, and Polaris cited strong commercial utility vehicle demand for data centre construction sites

Iran war-driven commodity inflation is hitting margins broadly: Sherwin-Williams expects propylene prices to rise 50% with solvents and epoxies already elevated, lifting its full-year raw material inflation outlook; General Motors is reallocating SUV and pickup deliveries from the Middle East back to North America; Hilton revised its Middle East full-year RevPAR outlook to down mid/high-teens (from prior up mid-single-digits) on regional travel disruptions

Lower-income consumer stress is building: Domino's noted weakening sentiment and pressure on purchase decisions throughout the quarter, while Coca-Cola is rolling out more affordable options to retain brand engagement; Kimberly-Clark offered a counterpoint, noting private-label penetration is actually declining, though it acknowledged lower-income consumers are becoming more "choiceful"

Automation is emerging as a key margin lever: UPS reported cost-per-piece fell 28% in automated facilities with more than two-thirds of its buildings now automated; Brown & Brown is using AI agents to automate more than 25% of its submission process, saving 50,000 hours annually from its automated billing platform

Bank of Japan holds at 0.75% but signals June hike as inflation forecasts jump

[8:57 am] A hawkish split vote and sharply revised inflation outlook point to a likely near-term rate rise, even as the Iran war clouds Japan's growth picture.

The BOJ held its policy rate at 0.75% in a 6-3 vote on Tuesday, with three dissenting members pushing for an immediate hike to 1%, citing upside inflation risks from the Middle East conflict

Core inflation forecasts were raised sharply to 2.8% from 1.9% for fiscal 2026, while the growth outlook was cut to 0.5% from 1%, reflecting the drag on corporate profits and real household incomes from elevated crude prices

Japan faces a "stagflation-lite" scenario: real disposable incomes have been negative for some time, headline CPI accelerated to 1.8% in March, and the country only narrowly avoided a technical recession in Q4 2025 with 0.3% quarter-on-quarter growth

Strategists broadly interpret the hawkish hold as laying the groundwork for a June hike, with the vote split and upward inflation revisions seen as a clear signal, though Governor Ueda's non-committal press conference tempered expectations somewhat

Source: Bloomberg

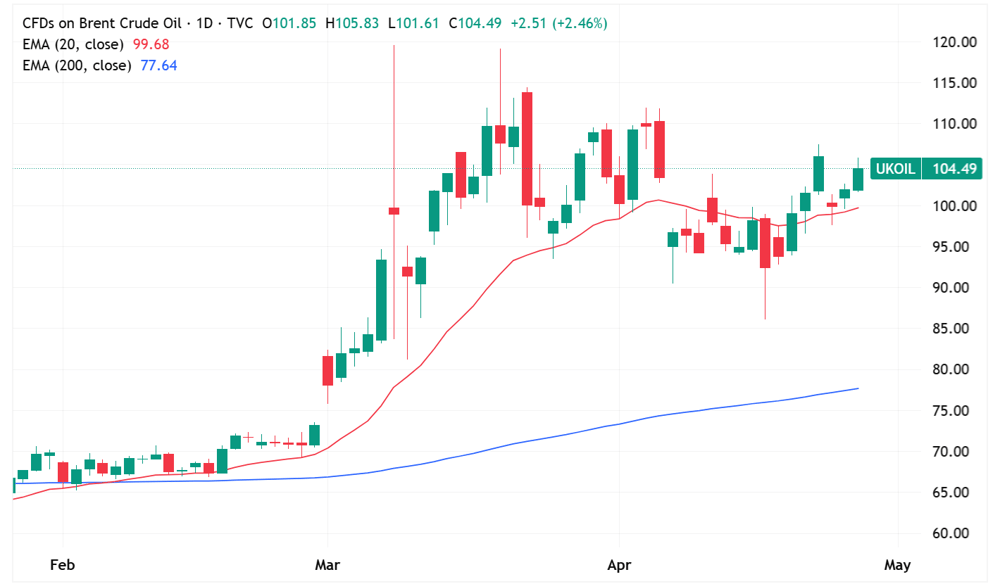

Hormuz reopening timelines slip as analysts lift oil price targets

[8:54 am] Analysts are pushing out their base cases for a return to normal Gulf shipping flows, with Brent targets moving sharply higher even as diplomatic backchannels offer some hope.

Citigroup shifted its base case for Hormuz reopening to end-May (from mid/late April) and reiterated a near-term Brent target of US$120/bbl, noting that muted oil price moves to date reflect prior inventory builds, IEA stock releases, and earlier optimism around a quick resolution

Goldman Sachs pushed its Gulf export normalisation assumption to end-June (from mid-May) and raised its Q4 Brent forecast to US$90/bbl (from US$80) and WTI to US$83/bbl (from US$75), also flagging a slower Gulf production recovery

Brent gained 2.4% overnight to US$104.49 a barrel. Prices have now rallied ~13% since 17 April.

Brent daily price chart (Source: TradingView)

Iran-US ceasefire talks stall as revised nuclear deal proposal awaited

[8:51 am] Diplomatic progress toward ending the two-month US-Iran war remains slow, with oil markets on edge as the Strait of Hormuz stays effectively shut.

Iran is expected to submit a revised peace proposal to Pakistani mediators within days, though the process is complicated by difficulties communicating with injured Supreme Leader Mojtaba Khamenei

Trump has signalled he will reject Iran's earlier offer, which sought to defer nuclear program negotiations, with the White House insisting any deal must include commitments to curb Iran's nuclear activities

Iran has asked the US to lift its naval blockade of the Strait of Hormuz as a precondition for reopening the waterway, while reportedly seeking to retain some control over shipping through the strait, a position Washington is unlikely to accept

UAE quits OPEC, opening the door to a future oil price war

[8:47 am] The UAE's exit marks the most significant blow to OPEC in its history, with long-term bearish implications for crude prices once the Iran war concludes.

The UAE, OPEC's third-largest producer at roughly 3.3 million barrels per day pre-war, formally exits on 1 May after nearly 60 years of membership, accounting for around ~12% of OPEC supply and up to ~15% of the group's total capacity

The exit reflects years of tension with Saudi Arabia over output policy

The UAE has been producing above its official OPEC quota but remains constrained well below its ~4.85 million bpd capacity

Has ambitions to reach 5 million bpd by 2027 and potentially 6 million bpd longer-term

Near-term market impact is limited given the Strait of Hormuz closure has already forced the UAE to slash production by around 40% in March

Longer-term, the UAE's exit is structurally bearish for oil as its no longer constrained by quotas

The departure raises broader questions about OPEC's cohesion, with Venezuela and Kazakhstan flagged as potential next movers, and weakens Saudi Arabia's role as the market's central stabiliser

OpenAI misses user and sales targets amid rising competition

[8:44 am] Internal concerns grow over whether OpenAI can fund its AI infrastructure ambitions as rivals eat into its market share.

ChatGPT fell short of OpenAI's target of 1 billion weekly active users by end of 2025, with subscriber churn remaining a persistent challenge as Google's Gemini gained popularity

OpenAI missed several monthly sales targets in 2026, with Anthropic taking ground in the high-value coding and enterprise segments

CFO Sarah Friar has raised concerns internally that insufficient sales growth could leave OpenAI unable to afford its future computing needs, with the company having committed to spend more than $1.4 trillion on AI infrastructure

OpenAI's most recent funding round raised $110 billion at a $730 billion valuation, with SoftBank committing $30 billion, bringing its total OpenAI investment to $64.6 billion (roughly 13% stake) by year-end; SoftBank shares fell as much as 7.5% on the news

OpenAI pushed back strongly on the WSJ report, stating the business is "firing on all cylinders" across consumer, enterprise, and compute, and flagged the new Microsoft deal and exponential growth in its Codex product as evidence of enterprise momentum

US stocks slip as AI spend concerns resurface

[8:42 am] US equities finished lower, ending off worst levels as a defensive shift took hold amid renewed questions over the sustainability of AI infrastructure spending.

Big tech mostly lower with semis falling after breaking an 18-day winning streak, triggered by reports OpenAI missed internal targets for weekly users and revenue (company rebutted, saying it is "firing on all cylinders"), weighing on names like Oracle and CoreWeave

Brent crude settled up 2.4% to US$104.49 a barrel as the US-Iran standstill drives concerns about looming physical market shortages, with the higher yield backdrop partly reflecting this dynamic

Q1 earnings metrics remain elevated with >15% S&P 500 EPS growth, >82% beat rate and 12.5% positive surprise rate, though the market is in holding pattern awaiting a flurry of Mag 7 names on Wednesday and Thursday

BoJ kicked off a big week of central bank decisions with a hawkish hold overnight, with the FOMC decision due Thursday afternoon followed by Powell's press conference

Good morning!

[8:28 am] ASX 200 futures are down 37 pts (-0.42%) as of 8:30 am AEST.

The overnight session in a nutshell:

Major US benchmarks lower after OpenAI reportedly missed internal targets for new users and revenue, with CFO Sarah Friar warning that the company may not be able to pay for future computing contracts if revenue does not growth fast enough

US-Iran peace talks remain in a standstill, with Brent up 2.4% to US$104.49 overnight and analysts pushing out Hormuz reopening timelines towards May-June

UAE will exit OPEC next month after six decades of membership, marking a significant blow to the Group

A wild 24 hours ahead: Alphabet, Microsoft, Amazon and Meta earnings due tomorrow, Australian inflation data this morning and FOMC tonight